When deciding between leveraging your property or utilizing signature-based credit, the definitive choice depends entirely on your capital requirements and available equity. A secured property loan is superior for accessing large sums (over $50,000) at lower interest rates because it uses your real estate as collateral. Conversely, an unsecured line of credit is better suited for short-term, smaller borrowing needs under $20,000, though it carries higher variable rates and demands strict credit score requirements. Choosing the wrong financial vehicle can cost you thousands in compounding interest and severely restrict your monthly cash flow. For many Calgary homeowners in 2026, leveraging property equity has become the most effective defense against rising consumer debt costs.

Key Takeaways for Calgary Homeowners

- Interest Rate Advantage: Secured loans offer significantly lower interest rates than unsecured lines because your home serves as collateral, mitigating the lender’s risk.

- Borrowing Limits: Unsecured lines are typically capped at $50,000, while secured equity loans allow you to access up to 80% of your home’s appraised value.

- Qualification Criteria: Banks demand high beacon scores (700+) and verifiable T4 income for unsecured lending, whereas equity lenders focus primarily on the physical value and marketability of your property.

- Repayment Terms: Equity loans offer structured repayment plans (often interest-only for better cash flow), whereas unsecured lines have variable rates that fluctuate with central bank policies.

- Debt Consolidation: Transitioning high-interest revolving debt into a structured secured loan can improve monthly household cash flow by up to 45%.

Understanding the Core Mechanics of Borrowing in 2026

To make an informed financial decision, you must first understand the fundamental difference in how these credit facilities are structured. The presence or absence of collateralization dictates the entire risk profile of the loan, which directly impacts your borrowing limit and interest rate.

The Unsecured Line of Credit Explained

An unsecured line of credit is a revolving account that allows you to borrow up to a predetermined limit without providing any physical asset as collateral. The financial institution grants this facility based entirely on your promise to repay, backed by your historical credit performance and verifiable income.

Because there is no asset for the lender to seize in the event of default, banks view this as a high-risk loan. Consequently, they charge a premium interest rate to offset potential losses. If your financial situation changes, the bank can also unilaterally reduce your credit limit or demand immediate repayment.

The Secured Equity Advantage

A secured equity loan—often registered behind your primary mortgage on your property title—is backed by a tangible asset: your house. Because the loan is secured by real estate, the lender has a legal safety net known as a lien. This security allows them to offer substantially larger loan amounts and generally more competitive interest rates.

If you own a home in Alberta, you possess an asset that can actively work to reduce your cost of borrowing. As property values have stabilized at higher baselines in 2026, the dormant equity sitting in these homes has become a powerful financial tool.

Interest Rates and the Cost of Capital

The presence of collateral is the single biggest factor influencing the cost of your loan. Unsecured lines of credit feature variable interest rates tied directly to the Bank of Canada Prime Rate plus a substantial premium. In 2026, it is common to see unsecured personal lines of credit priced at Prime + 4.5% or higher.

If the central bank raises its benchmark rate, your monthly minimum payment increases immediately, squeezing your household budget. In a direct comparison, the secured option provides significantly more stability and cost-efficiency. While these secondary secured rates are higher than first mortgages, they remain drastically lower than the double-digit rates seen on unsecured products.

“Pledging an appreciating asset fundamentally alters your risk profile, allowing lenders to offer capital at a fraction of unsecured costs,” explains Dr. Sarah Jenkins, Senior Economist at the Alberta Financial Research Institute. “In 2026, the spread between secured and unsecured borrowing costs has widened to nearly 500 basis points for the average consumer.”

Borrowing Power: Calculating Your Calgary Home Equity

One of the most significant limitations of an unsecured line of credit is the credit limit itself. Most major Canadian banks will cap an unsecured personal line of credit at roughly $50,000, even for borrowers with pristine credit histories. If you are planning a major home addition, a business acquisition, or significant debt consolidation, $50,000 is rarely sufficient.

Secured equity lending operates on an entirely different scale. Lenders typically allow you to borrow up to 80% of your home’s appraised value—known as the Loan-to-Value (LTV) ratio—minus your existing first mortgage balance. According to Statistics Canada data and local real estate boards, the average detached home price in Calgary hovers around $785,000 in 2026. This mechanism can unlock hundreds of thousands of dollars.

Step-by-Step: Calculating Your Available Equity

To determine your exact borrowing power, follow this standard institutional calculation:

- Determine Appraised Value: Obtain a current 2026 market valuation of your property (e.g., $785,000).

- Calculate Maximum LTV: Multiply the home value by 80% ($785,000 x 0.80 = $628,000).

- Subtract Existing Debt: Deduct the outstanding balance of your first mortgage (e.g., $400,000).

- Identify Usable Equity: The remaining figure is your maximum borrowing limit ($628,000 – $400,000 = $228,000).

In this scenario, leveraging your property provides $228,000 in usable funds, whereas an unsecured line of credit would abruptly stop at $50,000.

| Feature | Secured Property Loan | Unsecured Line of Credit |

|---|---|---|

| Maximum Limit | Up to 80% of Home Value | Typically capped at $50,000 |

| Interest Rate Type | Fixed or Variable (Lower) | Strictly Variable (Higher) |

| Approval Basis | Property Equity & Marketability | Credit Score & T4 Income |

| Funding Timeline | 1 to 2 Weeks | Instant to 5 Days |

Overcoming Strict Bank Qualifications

Qualifying for an unsecured line of credit is becoming increasingly difficult. Banks rely heavily on automated underwriting systems that scrutinize beacon scores and Debt-to-Income (DTI) ratios. If your credit score is below 700, or if you have a high utilization rate on existing revolving credit, your application will likely be rejected by the algorithm without human review.

Equity lenders, particularly private capital firms, utilize a common-sense underwriting approach. While they review credit history, their primary focus is the equity in the property. If you have sufficient equity, you can often secure approval even with bruised credit or non-traditional income sources.

Solutions for Self-Employed Albertans

Calgary boasts a high density of entrepreneurs, contractors, and energy sector consultants. For these individuals, aggressive tax write-offs can make net taxable income appear artificially low, leading to automatic rejections for unsecured bank credit. If you have low taxable income as a business owner, navigating traditional bank requirements can be incredibly frustrating.

A secured equity loan bypasses this hurdle. By utilizing alternative documentation options, self-employed Albertans can bridge cash flow gaps or fund business expansion without the rigorous income stress tests required by major financial institutions.

Strategic Use Cases: Matching the Tool to the Goal

Knowing the mechanical differences is only half the battle; applying the right financial tool to your specific scenario is where true wealth preservation occurs. Consider these strategic use cases to guide your decision.

When to Choose an Unsecured Line of Credit

- You require a relatively small amount of capital (under $20,000).

- You possess an excellent credit score (750+) and highly verifiable T4 income.

- You need the funds for a very short duration (e.g., 30 to 60 days) and have a guaranteed exit strategy to pay it off quickly, avoiding prolonged interest accumulation.

When to Choose a Secured Equity Loan

- You need a substantial sum (over $50,000) for major home renovations, business investments, or purchasing a secondary property.

- You are funding big projects where peer-to-peer options fall short.

- You are consolidating multiple high-interest credit cards and want to drastically lower your blended monthly payments.

- Your credit score has been damaged by past life events, preventing you from accessing prime bank rates.

The Hidden Danger of Compounding Interest

One of the most dangerous aspects of unsecured debt is the velocity at which it grows. Credit cards and many unsecured lines of credit compound interest daily. If you are only making minimum payments, you are likely barely covering the interest charges, leaving the principal balance untouched. As highlighted by recent economic analyses on household debt, this cycle traps many Canadians.

Understanding the impact of compounding frequency on your debt is vital for long-term financial health. By converting this revolving debt into a secured loan, you effectively halt the compound interest cycle. You transition the debt into a simple interest loan with a clearly defined term and amortization schedule.

Furthermore, when you have excess cash, learning how extra payments hit your principal balance allows you to pay down the debt faster than you ever could with a revolving unsecured product. The Financial Consumer Agency of Canada strongly recommends structured repayment plans over perpetual revolving debt for this exact reason.

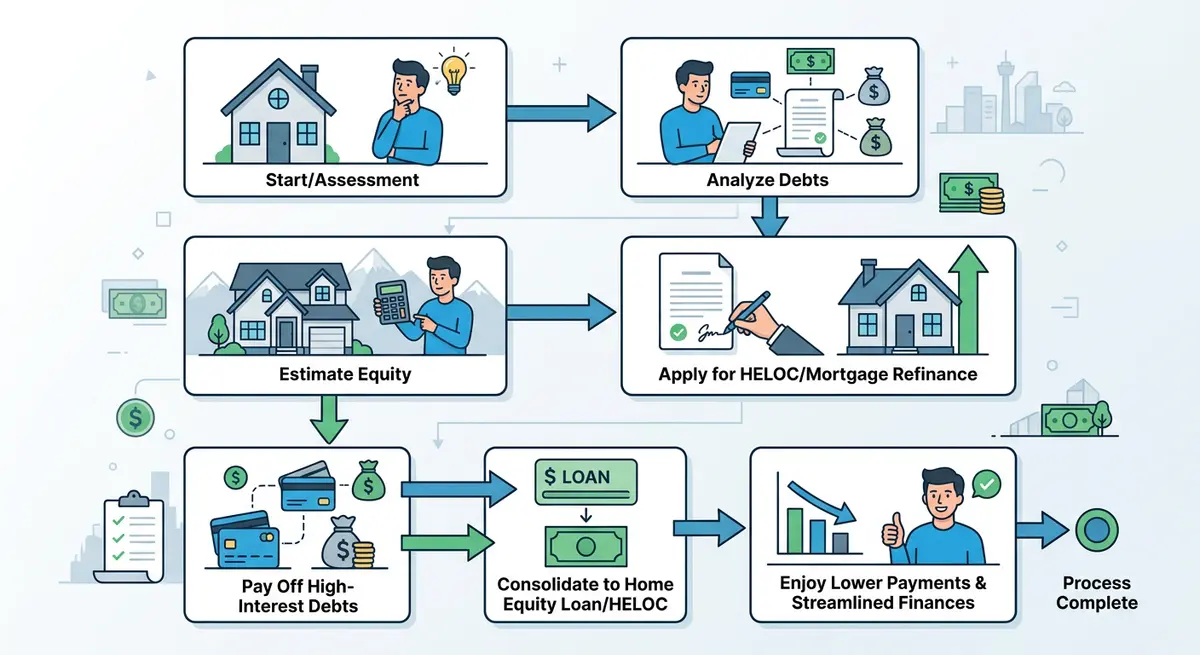

Step-by-Step: Transitioning from Unsecured Debt to a Secured Loan

If you are currently drowning in high-interest unsecured debt, transitioning to a secured equity loan is a proven strategy to regain financial control. “Homeowners who consolidate high-interest revolving credit into a structured secured loan typically improve their monthly cash flow by 35% to 45%,” states Elena Rostova, Director of Consumer Finance at the Canadian Debt Advisory Council.

Follow these steps to execute the transition smoothly:

- Tally Your Unsecured Debt: Compile all credit card balances, personal loans, and unsecured lines of credit to determine the total payoff amount.

- Estimate Your Home Equity: Use a conservative estimate of your home’s current market value and subtract your first mortgage balance.

- Gather Documentation: Prepare your property tax statement, first mortgage statement, and valid identification. Reviewing a comprehensive document checklist for your application ensures nothing is missed.

- Order an Appraisal: A licensed appraiser will visit your home to determine its exact market value for the lender.

- Fund and Disburse: Once approved, the lender’s legal counsel will register the lien and disburse the funds directly to your unsecured creditors, instantly wiping out those high-interest balances.

Once the consolidation is complete, implementing principal reduction strategies can accelerate your journey to becoming entirely debt-free.

Frequently Asked Questions (FAQ)

Which option has a lower interest rate in 2026?

Generally, a secured property loan has a significantly lower interest rate because it is backed by your home. Unsecured lines of credit carry higher rates (often Prime + 4.5% or more) to offset the lender’s risk since they have no collateral to seize in the event of default.

Can I get a secured equity loan if I have bad credit?

Yes, you can absolutely secure equity financing with bad credit. While unsecured lines of credit strictly require good to excellent credit scores (typically 700+), equity loans are underwritten primarily based on the available equity in your property, making them highly accessible for borrowers with bruised credit.

How much more money can I borrow against my house?

Unsecured lines of credit are typically capped at $50,000 by major Canadian banks. In contrast, leveraging your property allows you to access up to 80% of your home’s appraised value, which can easily amount to hundreds of thousands of dollars depending on your local Calgary market valuation.

Is the approval process faster for a line of credit?

For small amounts with perfect credit, an unsecured line of credit can be approved instantly via automated banking algorithms. However, secured loans require a physical property appraisal and legal registration, meaning funding typically takes between one to two weeks.

What are the closing cost differences between the two?

Unsecured lines of credit usually have minimal to zero setup costs. Secured loans involve appraisal fees, lender fees, and legal costs because a lien is being registered on the property title; however, the massive interest savings on a larger loan quickly outweigh these initial setup costs.

Can I use my home equity to pay off my unsecured line of credit?

Absolutely, this is one of the most common and effective financial strategies. By using your property’s equity to pay off an unsecured line of credit and high-interest credit cards, you consolidate your debt into one manageable payment, instantly improving your monthly cash flow.

Conclusion

Navigating the financial landscape in 2026 requires a clear understanding of how different credit facilities impact your long-term wealth. While unsecured lines of credit offer convenience for minor, short-term expenses, they fall short when you need substantial capital or are looking to escape the crushing weight of compounding interest. By leveraging the equity in your Calgary home, you unlock access to larger funds, lower interest rates, and flexible qualification criteria that traditional banks simply cannot match.

If you are ready to take control of your finances, consolidate high-interest debt, or fund your next major project, expert guidance is essential to ensure you secure the best possible terms. Contact our team today to discuss your specific situation and discover how your home equity can work for you.