Alberta homeowners facing provincial tax arrears have a powerful financial tool available: the equity built up in their property. When tax debts accumulate—whether from property tax shortfalls, provincial income tax obligations, or related assessments—homeowners can leverage their real estate assets through specialized financing solutions to resolve these liabilities before they escalate to liens or worse. This guide explains exactly how Alberta homeowners can use home equity to pay off provincial tax arrears, the options available, and the steps required to execute this strategy successfully.

Key Takeaways

- Home equity can be accessed through second mortgages or home equity lines of credit to settle provincial tax arrears before penalties compound

- Alberta provincial tax arrears include property tax deficiencies, provincial income tax debts, and related government assessments

- Second mortgages typically offer faster approval than traditional bank financing, with some lenders closing in as little as 3-5 business days

- Interest rates on equity-based financing range from 7.99% to 14.99% depending on credit profile and loan structure

- Unpaid provincial tax debts can result in property liens, making early action critical for homeowners

- Independent legal advice is strongly recommended before signing any equity-based loan agreement

Understanding Alberta Provincial Tax Arrears

Provincial tax arrears in Alberta arise when homeowners fail to pay obligations owed to the provincial government. These can include property tax deficiencies when municipal tax accounts are forwarded to the province for collection, outstanding provincial income tax balances assessed by the Canada Revenue Agency on behalf of Alberta, or special provincial assessments related to education property taxes, conservation levies, or other government-mandated charges.

According to research from the Government of Alberta, provincial tax arrears can accumulate significant penalties—often 10-15% annually on outstanding balances—making early intervention essential for homeowners. When these debts remain unpaid, the province can register a tax recovery certificate against the property, effectively creating a lien that clouds the title and complicates any future sale or refinancing.

The Financial Consumer Agency of Canada notes that tax debts take priority over most other secured claims, meaning a provincial tax lien can supersede even registered mortgages in certain circumstances. This priority status makes resolving tax arrears a top priority for homeowners who want to protect their equity and maintain clear title to their property.

How Home Equity Works as a Tax Arrears Solution

Home equity represents the difference between your property’s current market value and the outstanding balance on your primary mortgage. For example, if your Calgary home is worth $550,000 and your existing mortgage balance is $320,000, you have approximately $230,000 in usable equity. This equity can be accessed through two primary mechanisms to pay off provincial tax arrears.

Second Mortgages for Tax Arrears

A second mortgage is a separate loan registered against your property in second position behind your existing mortgage. These loans are typically offered by private lenders, alternative lenders, or specialized financing companies rather than traditional banks. Second mortgages allow homeowners to access lump-sum amounts ranging from $25,000 to $500,000 or more, depending on available equity.

The key advantage of second mortgages for tax arrears situations is speed. While traditional bank financing may take 45-90 days to approve, private second mortgage lenders can often close within 3-5 business days. This rapid turnaround is crucial when provincial tax liens are imminent or already registered against your property.

Home Equity Lines of Credit

A home equity line of credit (HELOC) provides revolving access to funds based on your available equity. Unlike a second mortgage’s lump-sum approach, a HELOC allows you to draw funds as needed, paying interest only on the amount used. HELOCs typically require more time to establish and involve stricter qualification requirements, making them less suitable for urgent tax arrears situations.

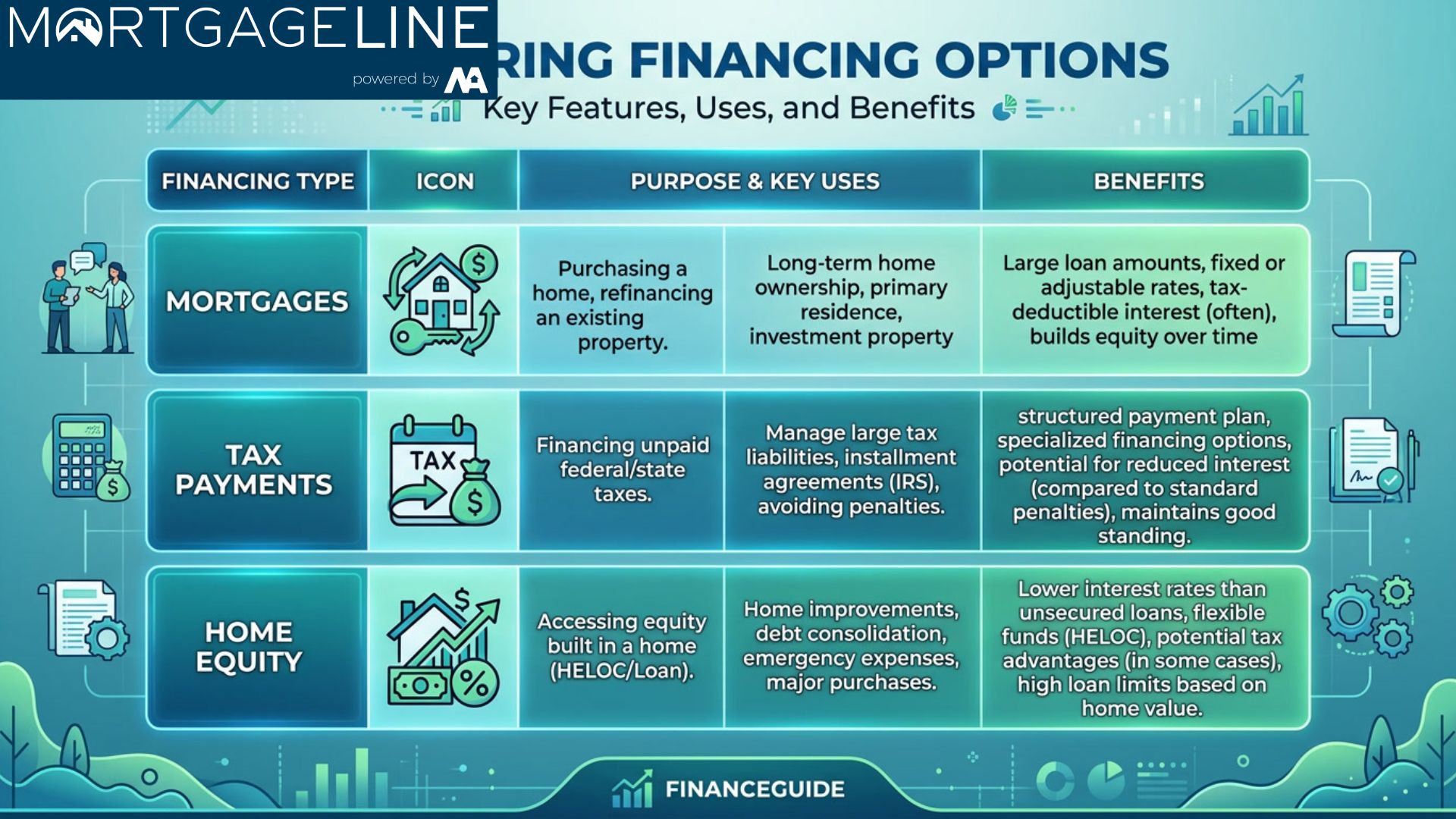

Comparing Second Mortgages vs. Other Tax Arrears Solutions

Homeowners facing provincial tax arrears have several options available. Understanding how equity-based solutions compare to alternatives helps you make an informed decision.

| Solution | Speed | Qualification Requirements | Interest Rates | Best For |

|---|---|---|---|---|

| Second Mortgage | 3-7 business days | Flexible; focuses on equity | 7.99% – 14.99% | Urgent tax arrears, poor credit |

| HELOC | 3-6 weeks | Strict; credit score 680+ | Prime + 0.5% to 2% | Established credit, planned expenses |

| Refinancing Primary Mortgage | 30-60 days | Strict; income verification | 4.5% – 6.5% | Excellent credit, lower rates desired |

| Payment Arrangement with Province | Varies | Income documentation required | Penalty rates may apply | Minor arrears, temporary cash flow issues |

As mortgage industry expert Sarah Mitchell, Senior Broker at Calgary Equity Partners, explains: “For homeowners dealing with provincial tax arrears, second mortgages often represent the fastest path to resolution. The key is ensuring the new debt service fits comfortably within your monthly budget to avoid creating a new problem while solving the old one.”

The Step-by-Step Process for Using Home Equity

Successfully using home equity to pay off Alberta provincial tax arrears involves several distinct phases. Understanding this process helps homeowners prepare accordingly and avoid common pitfalls.

Step 1: Assess Your Available Equity

Before pursuing any equity-based solution, you need an accurate picture of your available equity. Request a current property valuation from a licensed Alberta real estate appraiser, or obtain a broker price opinion from a mortgage professional. Subtract your existing mortgage balance(s) from the property value to determine your usable equity position.

Most lenders will lend between 75% and 85% of your home’s value minus existing mortgage balances. If your property is worth $400,000 with a $280,000 first mortgage, you have $120,000 in gross equity. At an 80% loan-to-value ceiling, the maximum total mortgage exposure would be $320,000, leaving $40,000 in available borrowing capacity.

Step 2: Quantify Your Tax Arrears

Obtain a current statement of your provincial tax arrears directly from the relevant government office. Ensure you have the exact amount owed, including any accrued penalties or interest. This figure becomes your target borrowing amount, though you’ll want to borrow enough to clear the debt completely plus a small buffer for potential adjustments.

Step 3: Research and Compare Lenders

Second mortgage lenders vary significantly in their terms, rates, and service quality. Research multiple options, comparing not just interest rates but also origination fees, prepayment privileges, and lender reputation. The Financial Consumer Agency of Canada recommends obtaining quotes from at least three different lenders before committing.

Step 4: Apply for Financing

Once you’ve identified suitable lenders, complete applications with accurate information. Be prepared to provide property documentation, identification, proof of income, and details about your existing mortgage. Many private lenders offer online applications with same-day preliminary approvals based on property equity alone.

Step 5: Secure Independent Legal Advice

Before signing any second mortgage documents, consult with an Alberta lawyer who specializes in real estate and mortgage transactions. Independent legal advice ensures you fully understand your obligations, the consequences of default, and whether the proposed financing truly serves your best interests. This step is particularly critical when dealing with private or alternative lenders.

Step 6: Close the Transaction and Pay Tax Arrears

Once your second mortgage is registered, the lender disburses funds directly to you or arranges payment to your existing mortgage holder. You’ll then contact the provincial tax authority to arrange payment of your arrears, ensuring you receive official receipt documentation confirming the debt is cleared.

Costs and Considerations

Using home equity to pay tax arrears involves several cost components that homeowners must factor into their decision-making. Understanding these costs ensures there are no surprises after closing.

Interest Costs: Second mortgage rates typically range from 7.99% to 14.99% annually, significantly higher than primary mortgage rates. On a $50,000 second mortgage at 10.99% over 5 years, total interest costs could reach $15,000 or more depending on repayment terms.

Origination Fees: Most second mortgage lenders charge origination fees of 1-3% of the borrowed amount. A $50,000 loan might incur $1,000-$1,500 in upfront fees.

Legal Fees: Independent legal advice, title searches, and mortgage registration typically cost $1,500-$3,000 depending on transaction complexity.

Appraisal Fees: Property appraisals for second mortgage purposes usually cost $400-$600.

Despite these costs, the total expense of a second mortgage often remains lower than allowing provincial tax arrears to compound with penalty interest rates that can reach 15% annually or higher. Additionally, clearing tax liens protects your property’s title and preserves your ability to sell or refinance in the future.

Common Mistakes to Avoid

Homeowners who move too quickly or lack complete information often make costly errors when using home equity for tax arrears. Being aware of these pitfalls helps you navigate the process more successfully.

Borrowing Too Little: Failing to account for accrued interest, penalties, or potential adjustments can leave you with a remaining balance after closing. Always request a small buffer above your stated arrears amount.

Ignoring Total Debt Service: Taking on a second mortgage without honestly assessing your ability to service both your existing mortgage and new debt frequently leads to default. Calculate your complete monthly obligation and ensure it remains sustainable.

Skipping Legal Advice: Some homeowners attempt to save money by foregoing independent legal counsel, only to discover unfavorable terms or hidden obligations after signing. This economy often proves false.

Not Verifying Tax Clearance: After paying your arrears, obtain written confirmation from the provincial authority that your account shows zero balance. Keep this documentation permanently.

When Second Mortgages May Not Be Suitable

While second mortgages represent an effective solution for many Alberta homeowners, certain situations may call for alternative approaches.

If your available equity is minimal—typically less than 10-15% of property value—lenders may decline your application or offer unfavorable terms. In these cases, negotiating a payment arrangement directly with the provincial tax authority or exploring government assistance programs might prove more practical.

Homeowners with sufficient equity but extremely poor credit may face prohibitively high interest rates that make second mortgage borrowing economically inadvisable. In these situations, selling the property and using proceeds to clear tax arrears while renting instead might represent the more responsible choice.

Those facing immediate tax sale proceedings may find that even a second mortgage’s speed proves insufficient. In extreme cases, bankruptcy or consumer proposal considerations may warrant discussion with a licensed insolvency trustee.

Protecting Your Property After Clearing Tax Arrears

Successfully clearing provincial tax arrears through home equity represents only half the battle. Protecting your property from future tax debt accumulation requires ongoing attention to your financial management practices.

Establish automatic payments or reminders for all property-related tax obligations. Consider setting aside monthly amounts in a dedicated savings account specifically for tax payments. Monitor your property tax assessments annually and budget accordingly for any increases.

If your tax arrears arose from income tax issues rather than property taxes, work with a qualified tax professional to ensure proper withholding or quarterly installment arrangements going forward. The Canada Revenue Agency offers taxpayer relief provisions for those experiencing temporary financial hardship, but proactive management remains preferable to reactive solutions.

Frequently Asked Questions

Can I use home equity to pay off provincial income tax arrears in Alberta?

Yes, homeowners can use home equity through second mortgages or other equity-based products to pay provincial income tax arrears. The funds can be used for any purpose, including settling debts owed to the Canada Revenue Agency on behalf of Alberta. However, you should obtain written confirmation of the exact amount owed before closing your equity transaction to ensure full payment.

How quickly can I get a second mortgage to pay tax arrears?

Private second mortgage lenders can often approve and fund transactions within 3-7 business days, depending on document readiness and property location. Traditional bank financing or home equity lines of credit typically require 3-8 weeks. If your tax arrears situation is urgent, private lenders offer the fastest path to resolution.

Will taking a second mortgage affect my credit score?

Initially, applying for and receiving a second mortgage may cause a modest temporary dip in your credit score due to the inquiry and new account opening. However, if you make payments consistently and reduce your overall debt burden, your credit profile typically improves over time. The key factor is whether the second mortgage helps you achieve better financial stability.

What happens if I default on a second mortgage used for tax arrears?

Defaulting on a second mortgage can result in foreclosure proceedings, potentially causing you to lose your property. Second mortgage lenders have the legal right to enforce their security through judicial foreclosure. Before taking on any second mortgage obligation, ensure your budget can comfortably accommodate the additional monthly payments.

Do I need a lawyer to set up a second mortgage in Alberta?

While not legally required in all circumstances, obtaining independent legal advice before signing second mortgage documents is strongly recommended. An Alberta real estate lawyer can review terms, explain your obligations, identify potential issues, and ensure the transaction serves your interests. This investment typically costs $1,500-$3,000 but provides valuable protection.

What portion of my home equity can I borrow?

Most second mortgage lenders will advance up to 75-85% of your home’s appraised value minus existing mortgage balances. For example, on a $500,000 property with a $300,000 first mortgage, you might access $50,000-$125,000 in second mortgage financing depending on the lender’s specific policies and your credit profile.

Are interest rates on second mortgages tax deductible?

In certain circumstances, yes. Under Canadian tax law, interest on borrowed funds used to generate investment income or for business purposes may be tax deductible. However, interest on funds used for personal purposes—including paying personal tax arrears—typically is not deductible. Consult a qualified tax professional for guidance specific to your situation.

Conclusion

Using home equity to pay off Alberta provincial tax arrears represents a practical financial strategy for homeowners who have built substantial equity in their properties but face immediate tax debt obligations. By accessing second mortgage financing or home equity lines of credit, property owners can resolve provincial tax liabilities quickly, avoid escalating penalty interest, and protect their property title from potentially devastating liens.

The process requires careful assessment of available equity, honest evaluation of repayment capacity, and thorough due diligence on lender options. While second mortgage interest rates exceed those of traditional bank financing, the speed of approval and flexibility offered make these products particularly valuable when tax arrears threaten property security.

If you’re an Alberta homeowner facing provincial tax arrears and want to explore whether home equity solutions fit your situation, the first step is a confidential conversation with a qualified mortgage professional. Understanding your options empowers you to make informed decisions that protect both your property and your financial future.

Contact our team today to discuss your home equity options for resolving provincial tax arrears. Our specialists can assess your situation, explain available solutions, and help you navigate toward a clear tax standing.

References

- Government of Alberta – Provincial tax administration and recovery procedures

- Canada Revenue Agency – Federal and provincial tax collection information

- Financial Consumer Agency of Canada – Consumer protection and financial literacy resources

- Using Second Mortgage to Pay CRA Tax Arrears Alberta – Related financing guidance

- Independent Legal Advice for Alberta Second Mortgages – Legal considerations

- Pros and Cons of Second Mortgages Calgary Expert Guide – Comprehensive comparison

- How Long Does Second Mortgage Approval Take Calgary – Timeline expectations