A second mortgage in Calgary allows homeowners to borrow against their accumulated property equity while leaving their primary mortgage untouched. By leveraging up to 80% of their home’s appraised value, borrowers can access significant capital for debt consolidation, renovations, or emergency expenses. However, these financial instruments carry distinct risks, including higher interest rates, additional administrative fees, and the potential for foreclosure if monthly payments lapse. Understanding the precise balance between these advantages and drawbacks is critical for making sound financial decisions in today’s economic climate.

Key Takeaways

- Maximum Borrowing Limit: Calgary homeowners can typically borrow up to 80% of their property’s appraised value across all mortgages.

- Interest Rate Dynamics: Secondary financing carries higher interest rates than primary mortgages due to the subordinate lien position of the lender.

- Strategic Utility: The most effective uses include high-interest debt consolidation and value-adding home renovations.

- Qualification Flexibility: Private lenders offer alternative qualification metrics for self-employed individuals or those with lower credit scores.

- Inherent Risks: Defaulting on a secondary loan can trigger property seizure, making strict financial planning mandatory.

The 2026 Calgary Real Estate Context

Calgary’s real estate landscape has evolved significantly, creating new opportunities for homeowners to leverage their property wealth. According to the Canada Mortgage and Housing Corporation (CMHC), Calgary’s benchmark home price has shown resilient growth, stabilizing around $615,000 in early 2026. This steady appreciation, combined with consistent population influxes documented by Statistics Canada, means that many local homeowners are sitting on unprecedented levels of untapped equity.

As Dr. Sarah Jenkins, Senior Economist at the Alberta Real Estate Research Institute, explains: “The sustained 4.5% year-over-year equity growth in the Calgary metropolitan area has transformed the average residential property into a highly liquid financial asset. Homeowners are increasingly utilizing secondary financing not out of desperation, but as a calculated wealth-management strategy.”

Comprehensive Pros of Secondary Financing

When utilized strategically, secondary financing offers substantial financial leverage. The primary advantages revolve around liquidity, flexibility, and the ability to restructure existing liabilities.

1. Access to Substantial Capital

Unlike unsecured personal loans or credit cards, which rely solely on your credit score and income, equity loans are secured by your property. This allows borrowers to access much larger sums. For example, on a $600,000 home with a $300,000 first mortgage, a homeowner could potentially access up to $180,000 in additional funds (reaching the 80% Loan-to-Value limit).

2. High-Interest Debt Consolidation

One of the most mathematically sound reasons to secure secondary financing is debt consolidation. The Financial Consumer Agency of Canada frequently highlights the dangers of revolving high-interest debt. By rolling credit card balances (often carrying 19.99% to 24.99% interest) into a secondary loan at 6% to 9%, homeowners can save thousands of dollars annually and reduce their monthly cash outflow.

3. Value-Adding Home Renovations

Reinvesting equity back into the property is a proven strategy. Upgrading a kitchen or developing a basement suite not only improves the homeowner’s quality of life but can yield a Return on Investment (ROI) of 70% to 80% upon resale. Furthermore, creating a legal secondary suite can generate rental income to offset the new loan payments.

The Cons and Inherent Risks

Despite the benefits, secondary financing is not without its pitfalls. Borrowers must navigate several structural disadvantages compared to primary lending.

1. Elevated Interest Rates

Because the new lender takes a “subordinate” position on the property title, they assume more risk. If the property is sold under duress, the primary mortgage holder is paid first. To compensate for this risk, lenders charge higher interest rates. While a primary mortgage in 2026 might sit at 4.5%, a secondary loan could range from 6.5% to 12%, depending on the borrower’s credit profile.

2. Administrative and Closing Costs

Securing these funds requires upfront capital. Borrowers must account for appraisal fees ($300-$500), legal fees ($800-$1,500), and potential lender origination fees (1% to 3% of the loan amount). These costs are often deducted directly from the loan advance, meaning you receive less cash than the gross loan amount.

3. The Risk of Foreclosure

The most severe consequence of defaulting on a secured loan is the loss of the property. If a homeowner fails to maintain payments, the secondary lender has the legal right to initiate foreclosure proceedings. Understanding the foreclosure timeline in Alberta is crucial for anyone leveraging their home as collateral.

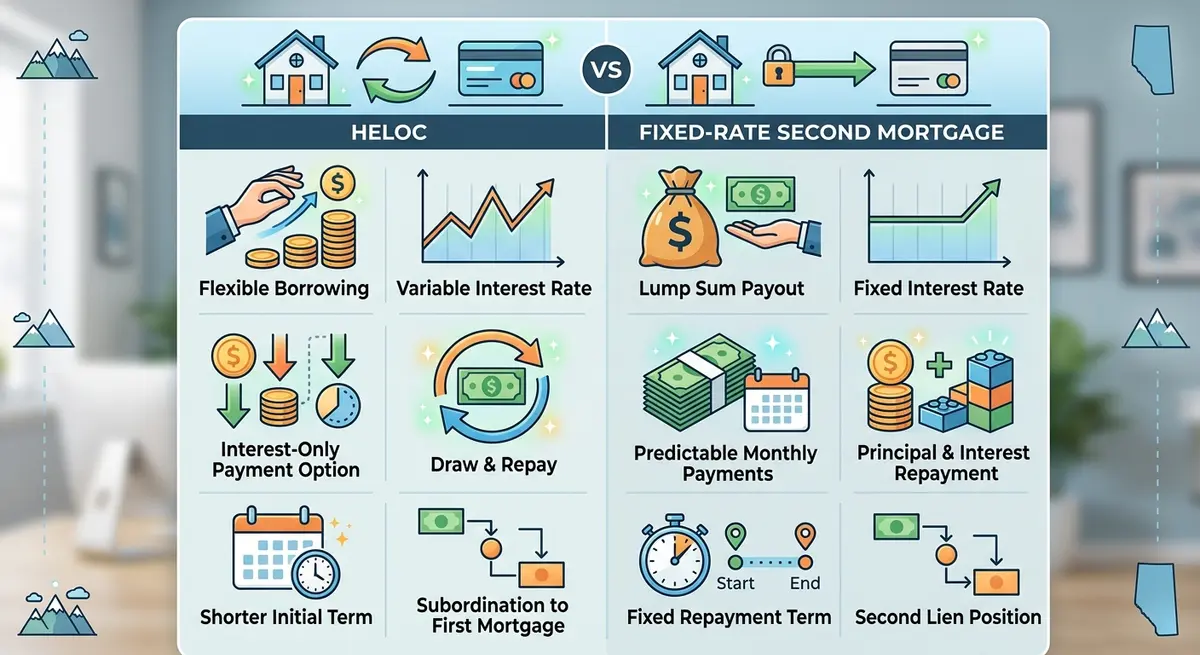

HELOC vs. Second Mortgages: Understanding the Difference

Homeowners often confuse Home Equity Lines of Credit (HELOCs) with traditional secondary mortgages. While both utilize property equity, their mechanics differ significantly.

| Feature | Traditional Second Mortgage | HELOC (Home Equity Line of Credit) |

|---|---|---|

| Fund Disbursement | Single lump-sum payment upfront. | Revolving credit; draw funds as needed. |

| Interest Rates | Typically fixed for the term. | Variable, tied to the Bank of Canada prime rate. |

| Repayment Structure | Fixed monthly payments (principal + interest). | Interest-only minimum payments during the draw period. |

| Best Used For | Large, one-time expenses (e.g., major renovations, debt consolidation). | Ongoing expenses (e.g., tuition, phased construction). |

As Marcus Thorne, a Calgary-based certified financial planner, notes: “Choosing between a HELOC and a fixed-term equity loan comes down to cash flow predictability. If you need absolute certainty in your monthly budget, the fixed-rate option is superior. If you require flexible, ongoing access to capital, the revolving line of credit wins out.”

Step-by-Step Guide to Qualifying in 2026

The application process requires meticulous preparation. Lenders scrutinize several key metrics to ensure the borrower can handle the additional debt load.

- Calculate Your Available Equity: Determine your home’s current market value and subtract your outstanding primary mortgage balance. Multiply the home’s value by 0.80 (80%) to find your maximum total borrowing limit.

- Assess Your Debt Service Ratios: Traditional lenders require your Gross Debt Service (GDS) ratio to be under 39% and your Total Debt Service (TDS) ratio to be under 44%.

- Gather Required Documentation: You will need recent pay stubs, T4s, a Notice of Assessment, property tax statements, and a recent mortgage statement. Reviewing a complete document checklist beforehand accelerates the process.

- Submit to the Right Lender: Depending on your credit score and income type, you will apply to an A-lender (bank), B-lender (trust company), or a private mortgage investment corporation (MIC).

Private Lenders vs. Traditional Banks

The stringent B-20 mortgage stress test regulations have pushed many Calgary homeowners toward alternative lending solutions. Traditional banks offer the lowest rates but require pristine credit (typically 680+) and easily verifiable T4 income.

Conversely, private lenders focus primarily on the property’s equity rather than the borrower’s credit score. This makes them ideal for self-employed individuals who write down their taxable income or those with recent credit blemishes. Private lenders offer stated income options, allowing entrepreneurs to prove cash flow through bank statements rather than traditional tax returns. However, this flexibility comes at the cost of higher interest rates and lender fees.

Strategic Uses: Debt Consolidation and Renovations

To truly understand the value of secondary financing, one must look at the mathematical outcomes of strategic deployment.

The Math of Debt Consolidation

Consider a Calgary homeowner with $40,000 in credit card debt spread across three cards, averaging a 22% interest rate. The minimum monthly payments easily exceed $800, with the vast majority going toward interest rather than principal reduction. By consolidating this debt into a secondary loan at 8% amortized over 15 years, the monthly payment drops to approximately $380. This frees up $420 in monthly cash flow and saves tens of thousands in interest over the life of the loan.

Renovation ROI in Calgary

Not all renovations are created equal. According to local appraisal data, the most profitable upgrades in 2026 include:

- Kitchen Modernization: 75% – 85% ROI. Focus on energy-efficient appliances and durable quartz countertops.

- Basement Suites: 70% – 80% ROI. Adding a legal secondary suite provides immediate rental income, which lenders view favorably.

- Energy-Efficient Windows: 65% – 75% ROI. With rising utility costs, buyers place a premium on thermal efficiency.

Common Mistakes to Avoid

Even with a solid plan, borrowers frequently fall into preventable traps. One major error is failing to account for how interest accrues. Understanding how compounding frequency impacts your total debt is vital; a loan compounded monthly will cost more over time than one compounded semi-annually, even if the advertised rates are identical.

Another common mistake is treating home equity like free money. Borrowers sometimes use secured funds to finance depreciating assets, such as luxury vehicles or vacations. This erodes long-term wealth and puts the home at risk for non-essential purchases. Additionally, borrowers must be proactive about retaining your mortgage documents, as proper record-keeping is essential for future refinancing or discharging the lien upon sale.

Finally, many homeowners fail to explore all their options. Before committing to a subordinate lien, it is wise to compare the costs against cash-out refinancing alternatives or even exploring if the funds could be used for funding a down payment on an investment property to generate passive income.

Conclusion

Navigating the pros and cons of second mortgages in Calgary requires a clear understanding of your current financial standing and long-term wealth goals. While the ability to access up to 80% of your home’s equity provides incredible leverage for debt consolidation, business investments, or property upgrades, the associated risks of higher interest rates and potential foreclosure demand respect. By carefully comparing traditional bank offerings with private lender flexibility, and maintaining strict discipline regarding how the funds are deployed, Calgary homeowners can successfully use secondary financing to build lasting financial stability.

If you are ready to explore your equity options or need help navigating the complex lending landscape, contact our team today for a personalized, no-obligation consultation.

Frequently Asked Questions

What is the maximum amount I can borrow with a second mortgage in Calgary?

In 2026, most lenders in Calgary will allow you to borrow up to 80% of your home’s appraised value, minus the outstanding balance of your primary mortgage.

Do I need a good credit score to get approved?

While traditional banks require a credit score of 680 or higher, private lenders focus primarily on the equity in your home. Borrowers with scores in the 500s can often secure private financing, albeit at higher interest rates.

How long does the approval process take?

Traditional bank approvals can take 3 to 6 weeks due to strict stress-testing and income verification. Private lenders can often approve and fund a loan within 5 to 10 business days.

Can I pay off my second mortgage early?

Most secondary loans come with specific terms (usually 1 to 5 years). Paying the loan off before the term expires often incurs a prepayment penalty, typically equivalent to three months of interest.

Are the interest payments tax-deductible?

If the funds from the loan are used strictly for investment purposes (such as buying dividend stocks or an investment property) or for a business, the interest may be tax-deductible. Funds used for personal debt consolidation or personal home renovations are not deductible.

What happens if my home value drops after I get the loan?

Your loan terms remain intact, but you may end up owing more than the home is worth (negative equity). This only becomes an immediate issue if you attempt to sell the property or refinance before the market recovers.