Yes, you can legally use a second mortgage to fund the down payment on a new property in 2026. However, because these are borrowed funds, Canadian lenders require a strict, documented chain of custody to satisfy federal Anti-Money Laundering (AML) laws. To secure underwriter approval, you must provide three specific documents: the formal second mortgage commitment letter, the real estate lawyer’s statement of adjustments, and the final bank statement showing the exact matching deposit.

Key Takeaways for 2026 Homebuyers

- Borrowed Funds are Legal: You can use a second mortgage or Home Equity Line of Credit (HELOC) as a down payment, provided you qualify for the combined debt load.

- The Paper Trail is Mandatory: Lenders must trace the money from the second mortgage lender directly into your personal bank account.

- AML Compliance: Strict federal laws require lenders to identify the exact source of all large deposits to prevent money laundering.

- Debt-Servicing Impact: The monthly payment for the second mortgage must be factored into your Total Debt Service (TDS) ratio, capped at 44%.

- Timing Matters: Always fund your second mortgage before writing an offer on the new property to avoid conditional approval delays.

The 2026 Calgary Real Estate Landscape: House Rich, Cash Poor

When planning to purchase a new property in the competitive 2026 Calgary real estate market—whether it is a move-up family home, a downsized condo, or an investment rental—the biggest hurdle is usually liquidity. You might be sitting in a house that has appreciated significantly over the last decade, yet your checking account does not reflect that wealth. This creates a frustrating scenario where you are “house rich but cash poor.”

To solve this, many homeowners turn to their existing property, taking out a second mortgage to access their equity and convert it into the cash needed to purchase the next asset. While this leverage strategy is powerful and frequently used by seasoned investors, it introduces a specific set of regulatory hurdles. Lenders for your new property will rigorously scrutinize where your down payment came from. Understanding how to leverage your home equity effectively is the first step toward expanding your real estate portfolio.

Why Lenders Scrutinize Borrowed Down Payments

Traditionally, when a homebuyer applies for a mortgage, the lender asks for 90 days of bank statements. They want to see a history of savings accumulating over time. If they see a sudden, large deposit, they will immediately ask for the source. According to the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC), this is standard procedure to prevent money laundering and to confirm the borrower has not taken out an undisclosed loan that would affect their affordability metrics.

When you use a second mortgage, you are explicitly using borrowed funds. This changes the underwriter’s approach. Instead of looking for 90 days of slow accumulation, they require a precise paper trail. As David Chen, a Senior Underwriter based in Alberta, explains: “Underwriters do not reject money simply because it is borrowed. They reject files where the borrower cannot mathematically prove the origin of the capital.” They need to verify that it is a registered, legal loan and that the terms of that loan are factored into your overall financial picture. Without the acceptable proof of down payment that Calgary institutions mandate, your application will immediately stall.

The 3-Step Document Trail: Acceptable Proof of Borrowed Equity

To satisfy the lender for your new home, you must prove the chain of custody of the funds. A simple screenshot of a high bank balance is useless if you cannot prove how the money got there. Here is the exact 3-step paper trail you must establish to organize your application files effectively:

- The Second Mortgage Commitment Letter: Provide the formal approval letter or commitment from the lender who provided the second mortgage on your current home. This proves the loan exists, outlines the terms, and confirms the interest rate.

- The Statement of Adjustments: This document, provided by your real estate lawyer when the second mortgage closed, shows the total loan amount and how the funds were disbursed. It details the payoff of small debts, legal fees, and the exact net proceeds sent to you.

- The Bank Deposit Record: A bank statement showing the exact net proceeds from the lawyer’s trust account being deposited into your personal checking or savings account. The deposit amount must match the lawyer’s statement to the penny.

By providing these three documents, you create an unbroken line from the equity in your old home to the cash in your bank account. To ensure you don’t miss any critical paperwork, review our complete 2026 second mortgage document checklist before submitting your file.

How Borrowed Equity Impacts Your Debt Service Ratios

Using a second mortgage for a down payment is a “leverage on leverage” strategy. While it gives you the cash you need, it also increases your debt obligations. When you apply for the mortgage on the new home, the lender will calculate your Debt Service Ratios. In 2026, prime lenders regulated by the Office of the Superintendent of Financial Institutions (OSFI) enforce a strict 39% Gross Debt Service (GDS) and 44% Total Debt Service (TDS) limit.

Your new TDS calculation will include:

- The proposed mortgage payment on the new home.

- The property taxes and heating costs for the new home.

- The first mortgage payment on your existing home.

- The new second mortgage payment on your existing home.

If the combined payments push your TDS ratio over the allowable 44% limit, you will not qualify for the new purchase, even though you have the cash in hand. For details on consumer debt ratios, the Financial Consumer Agency of Canada (FCAC) provides helpful calculators and guidelines. If your ratios are tight, you might consider adding a non-occupant co-borrower to increase your qualifying income.

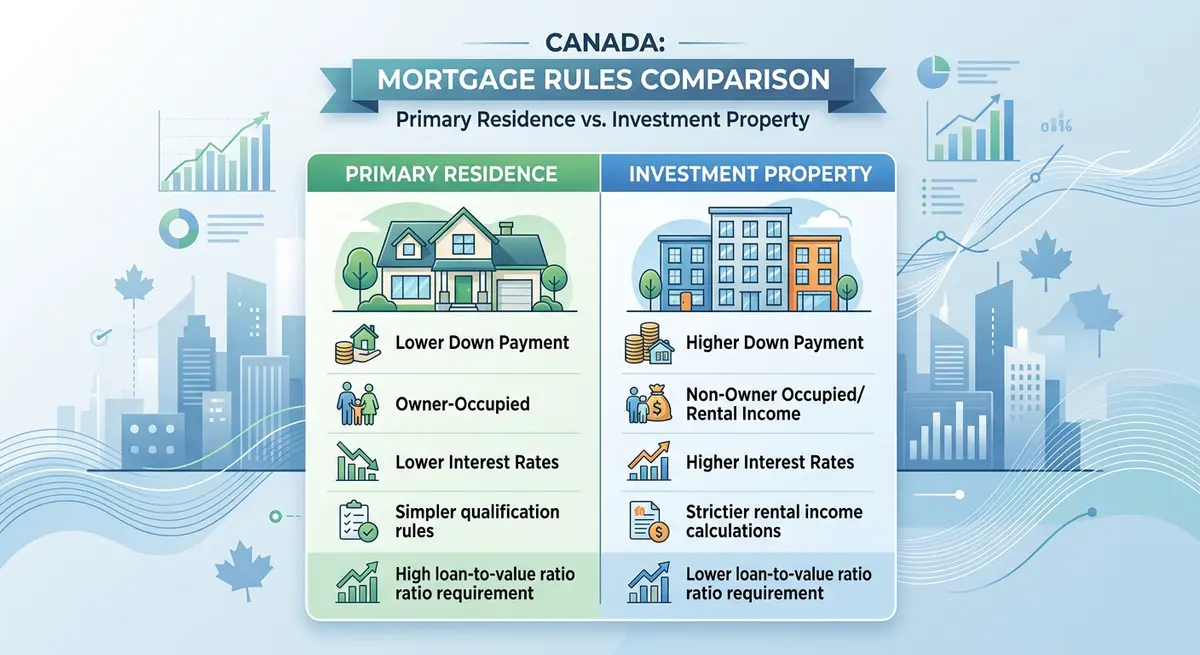

Primary Residence vs. Investment Property Rules

The rules regarding borrowed down payments change based on what you are buying. In 2026, research indicates that approximately 31% of Calgary real estate investors leverage existing equity to expand their portfolios, making this a highly scrutinized area of lending.

| Property Type | Minimum Down Payment | Borrowed Funds Allowed? | Underwriting Scrutiny Level |

|---|---|---|---|

| Primary Residence | 5% (up to $500k) | Yes (Subject to strict TDS limits) | High (Standard AML compliance) |

| Investment/Rental | 20% Mandatory | Yes (Very Common practice) | Very High (Strict Chain of Custody) |

If you are pulling equity from your primary residence to buy a rental property, you are typically required to put down at least 20%. The good news is that using a second mortgage to fund this 20% is a very common and accepted practice among Calgary investors. The key, again, is simply providing the required documentation.

Timing Your Transactions for a Smooth Closing

Timing is everything when using this strategy. The smoothest path is to finalize the second mortgage and have the funds deposited into your account before you apply for the mortgage on the new property. Standard wire transfers from a lawyer’s trust account can take up to 48 hours to clear, and underwriters will not issue a final approval without seeing the cleared funds.

As Marcus Thorne, Chief Risk Officer at Alberta Mortgage Solutions, notes: “In 2026, the origin of funds is scrutinized more heavily than ever. A sudden $100,000 deposit without a clear, documented chain of custody will trigger an immediate AML freeze on the file. Always fund your second mortgage before writing an offer on the new property.”

If you try to do both simultaneously, the lender for the new home will approve you conditionally, stating “Subject to verification of down payment funds.” You will then be racing the clock to get the second mortgage closed and the paperwork submitted before your possession date. Securing the funds first removes this stress. It is also wise to understand how long to keep your second mortgage documents in case of future audits.

The “Gift Letter” Trap: Why Honesty is Mandatory

A common mistake borrowers make is trying to simplify the paperwork by calling the second mortgage funds a “gift.” For example, a parent takes out a second mortgage on their home and gives the money to their adult child to buy a condo. The child cannot simply submit a standard gift letter if the parents borrowed the money.

Lenders trace gift funds back to the donor’s account. If the lender sees that the parent’s account received a sudden lump sum from a mortgage company, they will trace the debt. “Attempting to mask a second mortgage as a familial gift is one of the most common triggers for mortgage fraud investigations,” warns Sarah Jenkins, a Calgary-based real estate attorney. Honesty and transparency about the source of funds are always the best policies. Attempting to disguise borrowed funds as a pure gift is considered mortgage misrepresentation by the Real Estate Council of Alberta (RECA). If you are receiving legitimate gift funds, ensure you follow the proper gift letter requirements for Calgary lenders.

Alternative Lending: When Traditional Ratios Fail

If your debt ratios are too high to qualify for a prime mortgage on the new property (because of the new second mortgage payment), you may need to look at alternative lending options for the purchase. Private lenders in Calgary are generally much more flexible. Because private lenders focus heavily on the equity and the asset itself, they are often less concerned with traditional TDS ratios.

If you are a business owner struggling with traditional bank metrics, you might explore stated income second mortgages for business owners to secure the initial equity takeout. Furthermore, private lenders use a different reasonability test to verify self-employed income, making it easier to qualify for the second mortgage in the first place.

Conclusion

Leveraging the equity in your current home is a smart, efficient way to build a real estate portfolio or move into your dream home without waiting years to save cash. The key to making this strategy work in 2026 is understanding that lenders require strict, documented evidence to satisfy federal regulations. By keeping meticulous records of your loan commitments, lawyer’s statements, and bank deposits, you create an unassailable paper trail. Gathering the acceptable proof of down payment that Calgary lenders expect is the ultimate key to unlocking your equity and ensuring your next real estate transaction closes smoothly and on time. If you need assistance structuring your equity takeout, contact our team today for expert guidance.

Frequently Asked Questions (FAQ)

Can I use a HELOC instead of a second mortgage for the down payment?

Yes, a Home Equity Line of Credit (HELOC) is perfectly acceptable in 2026. You will need to provide your most recent HELOC statement showing the available limit and a bank statement showing the transfer of funds from the HELOC to your personal checking account.

Do I need a 90-day history if the money came from a second mortgage?

No, the 90-day rule is primarily for saved cash. For borrowed funds, you only need to show the paper trail of the loan being deposited into your account, even if the transaction happened yesterday. The chain of custody replaces the need for a 90-day history.

What constitutes acceptable proof of a borrowed down payment?

Acceptable proof consists of three specific items: the official mortgage commitment letter from the lender, the lawyer’s statement of adjustments showing the payout details, and your bank statement showing the exact matching deposit clearing your account.

Will the bank reject me simply because I borrowed the down payment?

Not inherently. They will only reject you if adding the new loan payment pushes your Total Debt Service (TDS) ratio above the maximum allowable limit, which is typically 44%. The source of the funds is acceptable; the affordability is what they test.

Can I borrow 100% of the down payment?

Often, yes. If you have enough equity in your current home to pull out 5%, 10%, or 20% for the new purchase, you can effectively buy a home with “zero down” from your personal savings, provided your income allows you to qualify for both mortgages simultaneously.

Does using a second mortgage affect my CMHC insurance?

If you are buying a home with less than 20% down, you need default insurance through providers like the Canada Mortgage and Housing Corporation (CMHC). Some insurers have specific rules, slightly higher premiums, or surcharges for borrowed down payments, so your broker will need to navigate which insurer is best for your specific file.

How long does it take for second mortgage funds to clear?

Once your real estate lawyer finalizes the second mortgage, the funds are typically wired to your account. In 2026, standard wire transfers from a lawyer’s trust account take between 24 to 48 hours to fully clear and reflect on your bank statement.