The most effective strategies for reducing a second mortgage principal in Calgary involve combining accelerated bi-weekly payments, maximizing annual lump-sum privileges, and leveraging income sweeping through a Home Equity Line of Credit (HELOC). By directly attacking the principal balance, borrowers bypass high compounding interest rates and shorten their amortization periods significantly. In the 2026 economic landscape, where secondary financing rates hover between 9.5% and 13.2%, making only the minimum scheduled payments guarantees that you will pay exponentially more in interest than originally borrowed. The key to achieving financial freedom and protecting your home equity lies in implementing a structured, mathematically proven repayment plan that attacks the core debt directly.

Key Takeaways

- Every dollar paid above your scheduled interest cost goes 100% toward reducing the principal balance, permanently lowering all future interest calculations.

- Most closed secondary mortgages in Alberta allow penalty-free annual lump-sum payments of 10% to 20% of the original loan amount.

- Switching to an accelerated bi-weekly payment schedule creates a “13th month” of payments every year, drastically reducing your amortization timeline.

- Income sweeping using a HELOC minimizes daily per diem interest charges and maximizes the utility of your regular household income.

- Always verify your specific prepayment limits with your lender to avoid triggering costly Interest Rate Differential (IRD) or three-month interest penalties.

The Mechanics of Mortgage Debt: Interest vs. Principal

To effectively dismantle your debt, you must first understand the mathematical framework of how your payments are applied. In a standard amortized loan, every payment you make is split into two distinct components: the interest charge and the principal reduction. During the early years of a loan, the vast majority of your payment services the interest, with only a microscopic fraction chipping away at the actual debt. This dynamic is particularly aggressive with secondary financing, which inherently carries higher interest rates than primary bank mortgages.

The higher the borrowing rate, the more of your monthly payment is consumed by the cost of borrowing. However, this mathematical equation flips the moment you introduce extra capital. Any amount paid over the required interest threshold is applied 100% directly to the principal balance. When you lower the principal today, the amount of interest calculated for tomorrow drops. This creates a compounding snowball effect where a slightly larger portion of your next regular payment automatically goes toward the principal.

Understanding how compounding frequency impacts your debt is crucial for maximizing this effect. According to the Financial Consumer Agency of Canada, even modest increases in payment amounts can shave years off your amortization schedule.

“Treating your secondary financing like a high-yield savings account flips the script. Every dollar of principal paid is a guaranteed tax-free return equal to your exact borrowing rate.”

— Dr. Marcus Thorne, Chief Economist at the Canadian Housing Research Board

Top Strategies to Accelerate Principal Reduction in 2026

1. Maximize Annual Lump Sum Prepayments

The fastest mechanism to reduce your outstanding balance is deploying lump-sum payments. A lump sum is a single, large capital injection made directly against the principal, entirely separate from your regular monthly installments. Savvy Calgary homeowners routinely utilize their annual Canada Revenue Agency (CRA) tax refunds, workplace performance bonuses, or proceeds from vehicle sales to make significant dents in their balances.

Before transferring funds, you must review your initial commitment letter. Most “closed” contracts allow borrowers to prepay a specific percentage of the original principal each year—typically between 10% and 20%—without facing a financial penalty. For instance, if your initial loan was $75,000, a 15% privilege allows you to pay down $11,250 extra per calendar year. Exceeding this strict limit will trigger an Interest Rate Differential (IRD) or a standard three-month interest penalty.

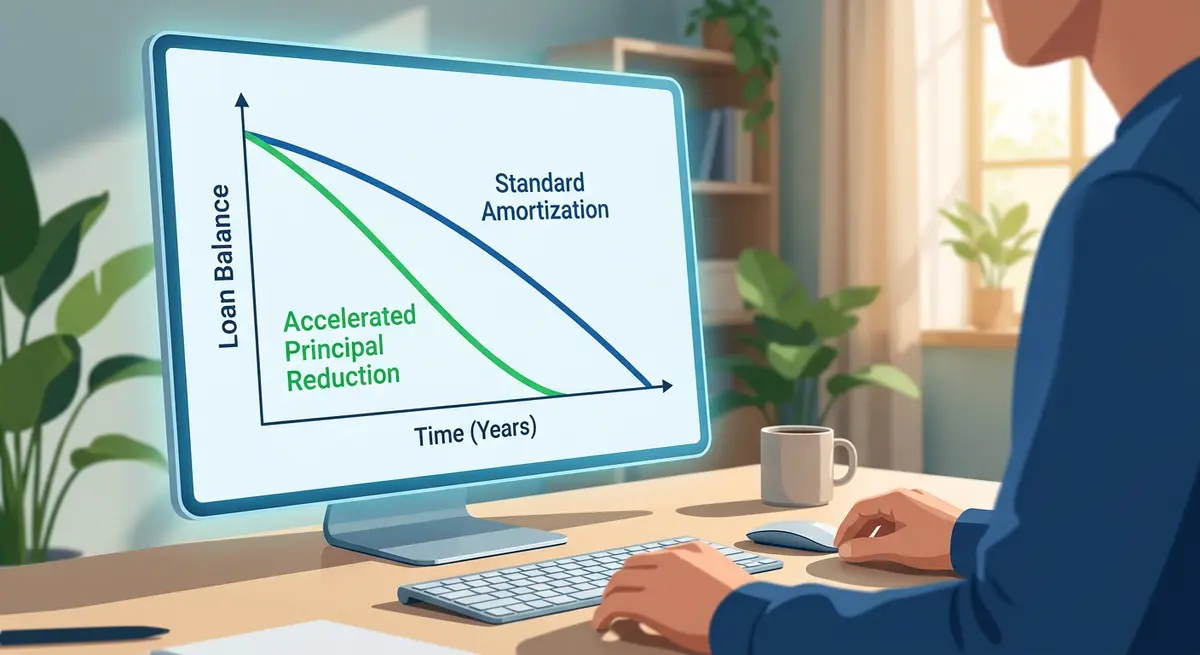

2. Implement Accelerated Bi-Weekly Payments

If your employer pays you on a bi-weekly schedule, aligning your debt obligations with your paycheque is a frictionless way to accelerate principal reduction. Standard monthly schedules involve 12 payments a year. Accelerated bi-weekly schedules involve 26 payments a year, with each payment equal to exactly half of a standard monthly installment.

Mathematically, 26 bi-weekly payments equal 13 full monthly payments. That one extra “invisible” payment per year is applied entirely to the principal balance. Over the life of a standard 25-year amortization, this strategy alone can reduce your payoff timeline by 3.5 to 4.2 years. Many private lenders in Calgary offer flexible payment schedules upon request.

3. The “Round-Up” Micro-Payment Method

Another highly effective, automated strategy is the “round-up” method. If your scheduled payment is an odd number, such as $642, you instruct your lender to round it up to $700. The extra $58 bypasses interest entirely and attacks the principal. This micro-investing concept applied to debt is highly successful because small, incremental increases are easier to absorb into a household budget than massive lump sums.

Because this happens automatically every month, it removes the need for ongoing financial discipline. Over a standard 5-year term, an extra $58 per month amounts to $3,480 in direct principal reduction, plus the compounded interest you saved on that capital. To see the exact mathematical breakdown of this strategy, review how extra payments hit your principal.

Advanced Tactics: Income Sweeping and HELOCs

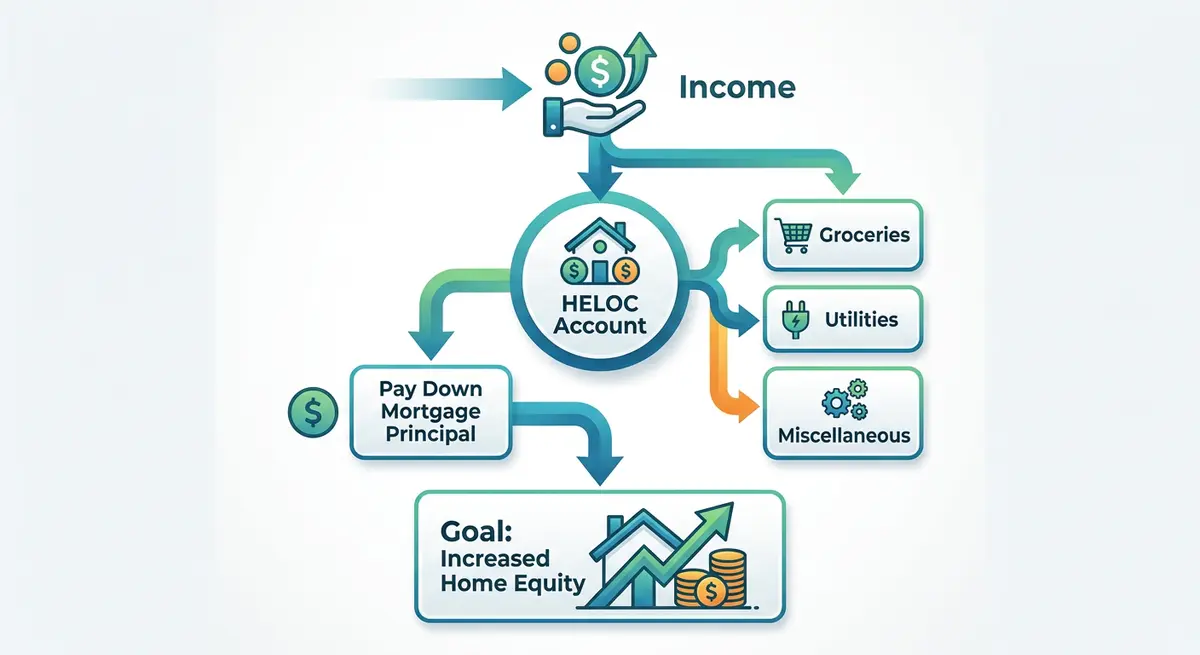

If your secondary financing is structured as a Home Equity Line of Credit (HELOC) rather than a fixed-term loan, you possess the ultimate financial flexibility. Unlike a rigid mortgage, a HELOC functions as a revolving credit facility secured by your property. You can pay it down to zero, draw it back up, and make payments whenever you choose without triggering prepayment penalties. This flexibility is why many wealth managers suggest comparing a unsecured line of credit comparison against secured home equity products.

The Mechanics of Income Sweeping

Advanced borrowers utilize a sophisticated strategy known as “income sweeping.” In this model, homeowners deposit their entire bi-weekly paycheque directly into the HELOC, instantly reducing the outstanding balance. Because HELOC interest is calculated daily (per diem), dropping the balance by $4,000 for even a few days drastically reduces the interest calculated for that month.

As household bills (groceries, utilities, property taxes) come due throughout the month, the borrower withdraws only what is strictly necessary from the HELOC to cover those expenses. Data from the Bank of Canada indicates that daily interest reduction strategies can improve household cash flow efficiency by up to 14% annually.

“Income sweeping requires surgical precision in household budgeting, but the mathematical advantage of reducing daily per diem interest cannot be overstated.”

— David Chen, Director of Lending at the Calgary Financial Consumer Alliance

Navigating Prepayment Privileges: Open vs. Closed Mortgages

Understanding the legal and contractual framework of your specific loan is essential before deploying capital. The Alberta Real Estate Association mandates that lending institutions clearly disclose all prepayment penalties in the commitment documents. Mortgages generally fall into two distinct categories: open and closed. Knowing the difference dictates which strategies you can safely deploy.

| Feature | Open Second Mortgage | Closed Second Mortgage |

|---|---|---|

| Prepayment Penalties | None. Pay off any amount at any time. | Strict financial penalties apply if limits are exceeded. |

| Interest Rates | Typically 1.5% to 2.5% higher than closed rates. | Lower, more competitive rates due to the guaranteed term. |

| Lump Sum Limits | Unlimited (up to the full outstanding balance). | Usually capped strictly at 10% to 20% annually. |

| Best Suited For | Short-term borrowing, imminent property sales, flipping. | Long-term debt consolidation, stable repayment plans. |

As Sarah Jenkins, Senior Financial Analyst, notes: “Borrowers often default to closed terms for the lower rate, but if you plan to aggressively pay down the principal within 12 to 24 months, the premium on an open facility is usually cheaper than the penalty on a closed one.”

Refinancing and Restructuring Your Debt

Sometimes, the most mathematically sound way to attack the principal is to stop paying exorbitant interest rates. If your credit score has improved significantly since you first secured the loan, or if property values in your specific Calgary quadrant have appreciated, you may be eligible to restructure the debt at a lower rate.

Refinancing involves breaking your current contract to initiate a new one with superior terms. While there is almost always a penalty to break a closed term early, the long-term interest savings can heavily outweigh the immediate cost. A lower interest rate means that even if you keep your monthly payment exactly the same, a much larger percentage of that payment automatically diverts toward principal reduction. Homeowners should always run a cash out refinance comparison before making a final decision.

This strategy is particularly relevant for self-employed individuals who initially relied on alternative documentation for business owners. As their business matures and tax returns show higher verifiable income, they can graduate from high-rate private lenders to competitive “B-lenders” or even prime banks.

Edge Cases and Common Pitfalls to Avoid

While aggressive repayment is universally advisable, there are specific edge cases and structural pitfalls that Calgary borrowers must actively avoid.

The Interest-Only Trap

The most dangerous pitfall is the “Interest-Only Trap.” Many private lenders structure their loans as “interest-only” to keep the borrower’s monthly cash flow requirements low. While this prevents immediate financial strain, it does absolutely nothing to reduce the core debt. The $80,000 you owe on day one of the term is exactly the $80,000 you will owe on the maturity date.

If you are currently trapped in an interest-only product, you must manually engineer your own amortization schedule. Treat the loan as if it legally requires principal payments. Calculate what a blended principal-and-interest payment would be, and voluntarily transfer that exact amount each month. By taking control of the amortization, you prevent the shock of a massive balloon payment when the term expires.

Navigating Relationship Changes

Another complex edge case involves marital separation or divorce. If you are going through a relationship breakdown, aggressive principal paydown might severely complicate the legal division of marital assets. In these highly sensitive scenarios, you must prioritize handling mortgages during a separation correctly.

Before committing large lump sums to the property’s equity, you may need to consult a family lawyer about removing a co-borrower from the title. Injecting cash into a jointly owned asset during a dispute can result in losing half of that capital during the final settlement.

Step-by-Step Guide: Executing Your Payoff Plan

To successfully execute these principal reduction strategies without triggering hidden penalties, follow this structured, five-step approach:

- Audit Your Commitment Letter: Locate your original legal documents and identify your exact prepayment privileges. Look specifically for the annual lump-sum percentage limit and any “double-up” payment clauses.

- Calculate Your Financial Buffer: Review your household budget to determine exactly how much extra monthly cash flow you can safely dedicate to debt reduction without compromising your six-month emergency savings fund.

- Automate the Process: Contact your lender’s servicing department to officially switch to an accelerated bi-weekly payment schedule or set up an automatic monthly “round-up” bank transfer.

- Deploy Windfalls Immediately: Commit to applying 100% of tax refunds, corporate bonuses, and unexpected cash inheritances directly to the principal within 48 hours of receipt. Delaying allows the money to be absorbed by lifestyle inflation.

- Monitor Your Amortization: Request an updated amortization schedule from your lender every six months. Visually tracking how your extra payments are destroying the interest curve provides the psychological motivation needed to stay the course.

Frequently Asked Questions (FAQ)

What is the maximum amount I can prepay on my second mortgage without penalty?

This depends entirely on your specific legal contract. Most closed mortgages in Alberta allow you to prepay between 10% and 20% of the original principal amount each calendar year without penalty. Open mortgages have no restrictions, allowing you to pay off the entire balance at any time.

Does making regular bi-weekly payments actually save me money?

Yes, but only if they are structured as “accelerated” bi-weekly payments. Regular bi-weekly payments simply divide your annual total by 26, whereas accelerated payments divide your standard monthly payment by two and pay it 26 times a year, resulting in one full extra monthly payment annually.

Can I pay off my private second mortgage early if I sell my house?

Private lenders often enforce different rules than traditional banks. Some mandate a strict 3-month interest penalty for early payout regardless of a property sale, while others might become fully open after an initial 3 to 6-month closed period. Always review your commitment letter for the exact discharge terms.

Is it better to invest my extra money or pay down my mortgage?

This depends on the interest rate of your debt versus the guaranteed after-tax return on your investments. Since secondary financing in 2026 often carries higher interest rates (e.g., 9.5% to 13.2%), paying down the debt provides a guaranteed, tax-free return that mathematically outperforms most safe stock market investments.

What happens if I accidentally overpay my annual prepayment privilege limit?

If you exceed your annual contractual limit, the lending institution will automatically charge a financial penalty on the excess amount. This is typically calculated using an Interest Rate Differential (IRD) or a simple 3-month interest charge, depending on the lender’s specific policies.

Are prepayment penalties tax-deductible in Canada?

If the property is your primary personal residence, prepayment penalties are never tax-deductible. However, according to the Canada Mortgage and Housing Corporation (CMHC), if the property is an active rental or investment property, you may be able to deduct the penalty as a legitimate business borrowing cost.

Conclusion

Successfully reducing your principal balance requires a combination of mathematical understanding, strategic planning, and consistent execution. By leveraging accelerated payments, maximizing your lump-sum privileges, and avoiding the interest-only trap, Calgary homeowners can save tens of thousands of dollars in unnecessary interest charges. The 2026 economic environment demands proactive debt management. If you are struggling to structure an effective payoff plan, or if you want to explore refinancing options to secure a lower rate, professional guidance is invaluable. Contact us today to speak with a Calgary-based mortgage specialist who can help you optimize your debt strategy and protect your hard-earned home equity.