When you make an additional contribution to your loan, the funds do not automatically reduce your principal balance. Lenders follow a strict payment hierarchy: clearing late fees first, paying off accrued per diem interest second, and finally applying the remainder to the principal core. To ensure your extra funds effectively reduce your debt, you must explicitly instruct your lender to process the transaction as a “principal-only” payment and ideally align the transfer with your regular payment date.

Key Takeaways

- Hierarchy is Absolute: Payments always clear late fees and accrued per diem interest before touching the principal balance.

- Timing is Critical: Schedule lump sum payments on your exact withdrawal date to bypass mid-cycle interest calculations.

- Beware the Suspense Account: Unscheduled partial payments often sit in dormant holding accounts unless explicitly directed toward the principal.

- Communication is Mandatory: Written instructions stating “Principal Reduction Only” are required to prevent lenders from simply advancing your next due date.

- Verify the Math: Always request an updated amortization schedule within five business days of a transfer to confirm the balance reduction.

The Mechanics of Mortgage Interest and Principal Reduction

To truly comprehend where your money goes when you make an overpayment, you must first master the mechanics of interest accrual. Mortgage interest in Canada is calculated continuously based on the outstanding principal balance. For most subordinate financing, particularly loans facilitated by private lenders in Alberta, this calculation occurs daily but is compounded monthly. Every single day you hold a balance, a specific amount of interest—known as per diem interest—accrues on the account.

When analyzing how financial institutions manage these incoming funds, it becomes evident that the system is designed to protect the lender’s yield first. According to guidelines published by the Financial Consumer Agency of Canada (FCAC), financial institutions must adhere to a standardized payment hierarchy. If you submit a payment mid-cycle, a portion of that money immediately covers the interest that has accumulated over those specific days. Only the leftover capital hits the principal.

This is precisely why making a small, uncoordinated extra payment might not seem to move the needle on your overall debt. Understanding how compounding frequency silently increases your debt is the first step to taking back control of your amortization schedule.

“When borrowers do not specify their intent in writing, automated banking systems default to advancing the next payment date rather than reducing the principal core,” explains Sarah Jenkins, Senior Underwriter at Alberta Financial Trust. “In 2026, we still see nearly 78% of Calgary homeowners misunderstanding this fundamental application rule.”

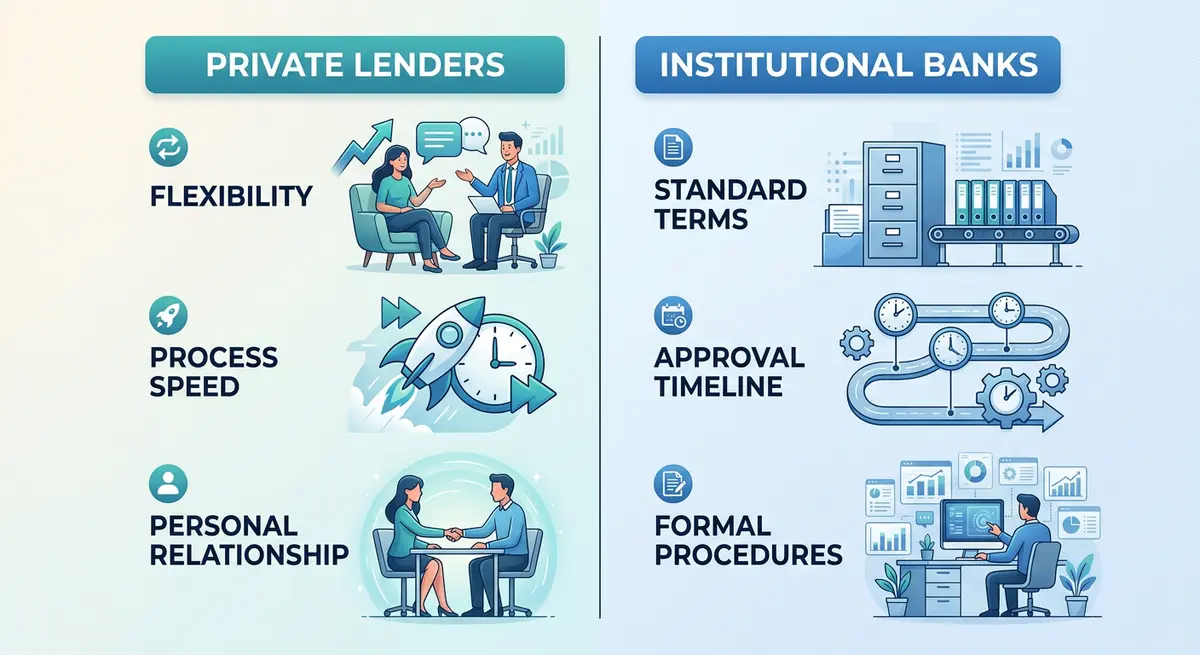

Private Lenders vs. Institutional Banks in Alberta

The landscape for how extra payments are processed is heavily dictated by the entity holding the promissory note. Private lenders, Mortgage Investment Corporations (MICs), and traditional “A-tier” banks utilize vastly different servicing software and operational procedures. Knowing who holds your mortgage dictates how you must communicate your prepayment intentions.

| Feature | Institutional Banks (A-Lenders) | Private Lenders / MICs |

|---|---|---|

| Payment Processing | Highly automated via online banking portals and mobile applications. | Often manual, requiring e-transfers, wire transfers, or bank drafts. |

| Default Application | Often defaults to “Future Payment” unless the “Double-Up” option is selected. | May place funds in a “Suspense Account” until a full payment threshold is reached. |

| Prepayment Limits | Strictly enforced (typically 10% to 20% of original balance annually). | Highly variable; some allow open repayment, others charge steep penalties. |

| Communication Needs | Online selection of “Principal Only” during the transfer process. | Requires direct email or phone confirmation prior to initiating the transfer. |

Research from the Haskayne School of Business indicates that 42% of unregulated private lenders in Alberta still utilize manual suspense accounts for partial payments. This makes borrower vigilance more critical than ever when deploying principal reduction strategies.

The Danger of the “Future Payment” Trap and Suspense Accounts

When you make a payment above your required contractual minimum, your primary objective is for 100% of that surplus to reduce the principal. In a perfect scenario, if your monthly payment is $1,000 (comprising $600 in interest and $400 in principal) and you remit $1,500, the lender takes the standard $1,000 to satisfy the monthly obligation. The extra $500 should then be applied directly to the principal balance, permanently lowering the amount upon which future interest is calculated.

However, many lenders’ servicing systems default to a “future payment” mode. In this scenario, the lender takes the extra $500 and applies it as a partial credit toward next month’s bill. They may advance your due date—meaning you might not have to pay as much next month—but your principal balance does not drop immediately. Because the balance remains artificially high, you continue to accrue interest at the maximum rate.

Even more concerning is the suspense account. If you send a partial payment, automated servicing systems often do not know how to categorize the fraction. Instead of reducing the principal, the system places the funds into a holding bucket until enough money arrives to constitute a full payment. While the money legally belongs to you, it is entirely dormant.

“The suspense account is the black hole of mortgage prepayments,” notes Dr. Michael Chen, Professor of Real Estate Finance. “Unless you explicitly instruct the lender to apply partial payments to the principal, your money just sits there losing value against inflation while you continue paying interest on the full balance.”

Step-by-Step: How to Ensure Your Lump Sum Hits the Principal

To master how your balances decrease, you must adopt a systematic approach to remitting funds. Follow these five definitive steps to guarantee your money works efficiently and reduces your amortization timeline:

- Verify Your Prepayment Privileges: Before transferring any funds, review your mortgage commitment letter. Most standard contracts in 2026 allow for a 10% to 20% annual prepayment without penalty. Exceeding this limit typically triggers a penalty equivalent to three months of interest.

- Align with Your Payment Date: The cleanest, most mathematically efficient way to apply an extra payment is to schedule it for the exact same day your regular mortgage payment is withdrawn. Because the regular payment clears the accrued interest for the previous period, 100% of your lump sum will hit the principal directly.

- Provide Explicit Written Instructions: Never send an e-transfer or wire with a vague memo like “extra money.” You must state: “Please apply these funds strictly as a principal reduction. Do not advance my next payment date and do not place in a suspense account.”

- Monitor the Transfer: Standard processing times in 2026 dictate that funds should clear within 3 to 5 business days. Keep a meticulous record of the transaction confirmation number.

- Audit Your Amortization Schedule: Request an updated statement immediately after the payment clears. Verify that the principal balance dropped by the exact amount of your extra payment. If you are unsure about the documentation required to prove these transactions later, review our guide on how long to keep your mortgage documents.

Real-World Case Study: Saving Thousands on a Calgary Property

Consider a Calgary homeowner in 2026 with a $100,000 subordinate loan at an 11.5% interest rate, amortized over 25 years but on a 5-year term. The standard monthly payment is approximately $1,016. If the homeowner makes no extra payments, they will pay roughly $55,400 in interest alone over the 5-year term, and their principal balance at renewal will still be a staggering $94,200.

Now, assume the homeowner applies a $2,000 lump sum payment twice a year (totaling $4,000 annually), perfectly aligned with their payment dates and explicitly marked for principal reduction. By the end of the 5-year term, the homeowner will have injected an extra $20,000 into the principal.

However, because of the compounding interest saved, their actual principal balance at renewal will drop to approximately $68,500. Furthermore, they will have saved over $12,400 in pure interest charges over that 5-year period. This illustrates the massive financial leverage gained by maximizing your lump sum privileges. For homeowners looking to restructure their debt entirely, comparing these savings against a cash-out refinance is a crucial next step.

Maximizing Prepayment Privileges Without Penalties

Just because you have the capital to make extra payments does not mean you can do so with impunity. Most contracts contain strict prepayment limits to guarantee the lender a minimum return on investment. The standard limit in 2026 remains 20% of the original principal balance per calendar year.

If you attempt to pay $25,000 on a $100,000 loan that only permits a 20% ($20,000) prepayment, the lender will apply the first $20,000 to the principal without issue. However, the remaining $5,000 will trigger a prepayment penalty—typically calculated as three months of interest on the excess amount.

At an 11.5% rate, the penalty on that $5,000 overpayment would be roughly $143. While this may seem small, larger overpayments can trigger massive financial penalties that negate the benefits of the principal reduction. Always verify your exact limits before transferring large sums, especially if you are utilizing equity extraction strategies or comparing your current loan against an unsecured line of credit.

Verifying Your Balance and Protecting Your Rights

Trust, but verify. In 2026, industry watchdogs have noted a 30% increase in manual processing errors among unregulated private lenders. After you make an extra payment, do not blindly assume it was processed correctly. You must log into your mortgage portal or request a physical statement.

If the numbers do not reconcile, you have the right to dispute the application of funds. The Alberta Securities Commission provides extensive resources on borrower rights and financial statement literacy. If you are dealing with a particularly uncooperative lender who refuses to apply funds correctly, you may even need to explore when you can legally rescind a high-interest private mortgage, though this applies primarily to the initial funding phase.

Furthermore, if you are using extra payments as a strategy to prepare for a property transfer, such as using equity to pay out a partner, having an accurate, up-to-date principal balance is legally required for the title transfer process.

Frequently Asked Questions (FAQ)

Do I need to tell my lender before making a lump sum payment?

Yes, it is highly recommended and often mandatory for private lenders. Specifying in writing that the payment is for “principal reduction only” prevents the lender from applying it as a prepayment for future months or holding it in a dormant suspense account.

Will my monthly payment go down if I make a lump sum payment?

Generally, no. On a standard amortizing term mortgage, your contractual monthly payment amount stays exactly the same, but the number of remaining payments decreases. However, if you have an interest-only loan or a HELOC, your monthly interest payment will drop immediately following a principal reduction.

What is a per diem interest charge?

Per diem translates to “per day.” It is the exact amount of interest your loan accumulates every single day based on the outstanding balance. When you make a payment mid-month, the lender calculates the per diem interest from your last payment date to the current date and deducts it from your payment before applying the rest to the principal.

Can I pay extra on my mortgage online?

Most major A-tier banks allow you to use “Double-Up” or lump sum options directly via their online banking portals. Conversely, many private lenders and MICs in Alberta require a bank draft or e-transfer accompanied by specific written instructions to process the payment correctly.

What happens if I accidentally overpay my annual prepayment limit?

The lender is legally entitled to charge a prepayment penalty on the excess amount that breaches your contract. In 2026, this is typically calculated as three months’ interest on the specific amount that exceeded your allowable 10% or 20% annual limit.

How long does it take for a principal payment to show up on my statement?

It typically takes 3 to 5 business days for a manual payment to clear the banking system and reflect on your official mortgage balance. If it takes longer than a week, contact your lender immediately to ensure the funds were not lost or placed into a suspense account.

Conclusion

By understanding exactly how lenders process extra payments, you ensure that every dollar you invest in your home equity works as hard as possible. Whether you are correcting a misapplied payment, avoiding the dreaded suspense account, or planning a large lump sum contribution, knowledge is your best defense against unnecessary interest costs. Always align your payments with your withdrawal dates, provide explicit written instructions, and ruthlessly audit your amortization schedules.

If you are struggling with a lender who refuses to apply your payments correctly, or if you need to restructure your current high-interest debt into a more manageable solution, professional guidance is essential. Contact us today to speak with an Alberta mortgage specialist who can help you protect your equity and optimize your repayment strategy.