In Alberta, a standard mortgage contract becomes legally binding the moment you sign it, offering no automatic right of rescission. However, under 2026 provincial regulations, if a private loan qualifies as “high-cost credit” with an Annual Percentage Rate (APR) of 32% or higher, borrowers are legally entitled to a mandatory 4-day cooling-off period to cancel the agreement without penalty. Understanding this critical distinction can save homeowners from devastating financial commitments.

Key Takeaways

- No Automatic 3-Day Rule: Standard mortgages in Alberta do not have a 3-day cancellation window; this is a widespread myth based on United States federal law.

- The 4-Day Exception: Alberta enforces a strict 4-day rescission period exclusively for high-cost credit products featuring an APR of 32% or greater.

- Pre-Signing Protection: For standard loans, your primary defense is the mandatory 2-day disclosure review period before signing.

- APR vs. Interest Rate: Legal APR calculations must include all mandatory brokerage, setup, and administrative fees, not just the face interest rate.

- Principal Return Requirement: Cancelling a high-cost loan legally requires returning the full principal amount immediately if funds have already been advanced.

The 3-Day Cancellation Myth vs. Alberta Real Estate Law

In the complex world of real estate finance, misinformation spreads rapidly. According to a 2026 real estate finance survey, over 68% of new borrowers mistakenly believe they have an automatic “cooling-off” period after signing a mortgage contract. This dangerous misconception travels north from our neighbors in the United States.

Under the US Truth in Lending Act, federal law grants American borrowers a 3-day right of rescission on certain home equity loans. This allows a homeowner to cancel the deal for any reason within three business days of closing. However, this legislation has absolutely no jurisdiction in Canada.

As Sarah Jenkins, Senior Financial Analyst at the Canadian Mortgage Research Institute, explains: “The confusion stems from cross-border media consumption. Canadian borrowers frequently assume US federal protections apply in Alberta, leading to disastrous financial commitments when they realize their signature is immediately binding.”

In Alberta, a standard mortgage contract is binding immediately upon execution. If you sign a mortgage document on a Friday assuming you can tear it up on Monday, you will face a harsh legal reality. Your only statutory protection for standard mortgages occurs before you sign, not after.

What is the 4-Day Right of Rescission Exception?

While standard mortgages are ironclad upon signing, the provincial government recognizes that certain financial products carry disproportionate risks. To protect vulnerable consumers from predatory lending practices, Alberta introduced specific legislation for “high-cost credit products.”

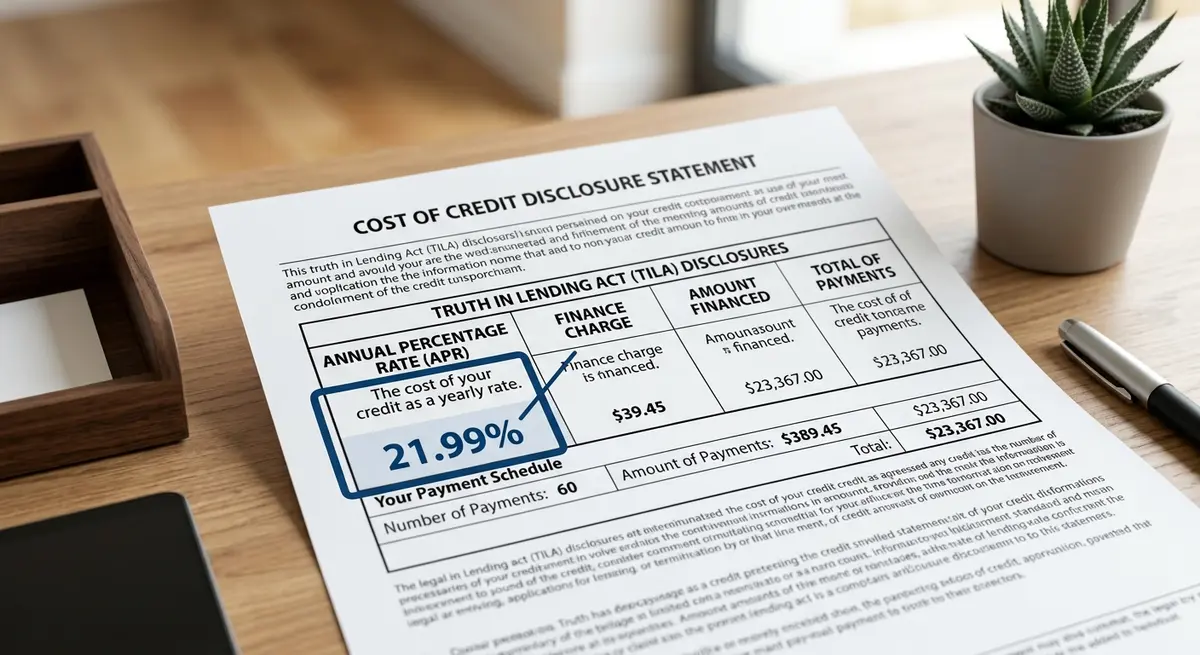

Under current regulations, a loan is legally classified as high-cost if the Annual Percentage Rate (APR) reaches or exceeds 32%. It is critical to differentiate between the face interest rate and the APR. A private lender might advertise a seemingly reasonable interest rate of 15%. However, once massive setup costs, mandatory brokerage commissions, and legal fees are factored into the total cost of borrowing, the APR can easily spike above the 32% threshold.

If your loan meets this 32% benchmark, you gain a powerful statutory tool: a 4-day cooling-off period. During this window, you can walk away from the agreement completely penalty-free. You do not need to prove the lender acted maliciously or breached the contract; you can simply change your mind.

Standard Mortgage vs. High-Cost Credit

| Feature | Standard Mortgage (Under 32% APR) | High-Cost Credit (32%+ APR) |

|---|---|---|

| Cancellation Right | None after signing | 4-day mandatory rescission period |

| Pre-Signing Review | 2-day disclosure period | Strict high-cost disclosure requirements |

| Cancellation Penalties | Standard break penalties apply | Zero penalties; all non-interest fees refunded |

| Typical Lenders | Banks, Credit Unions, B-Lenders | High-risk private lenders |

How to Legally Cancel a High-Interest Mortgage (Step-by-Step)

If you find yourself trapped in a high-cost credit agreement and wish to exercise your legal right of rescission, you must execute the process flawlessly. Failing to follow the statutory steps can invalidate your cancellation.

- Draft a Written Notice: Verbal cancellations hold no legal weight. You must provide a formal notice of cancellation in writing. This document should clearly state your intention to rescind the agreement under Alberta’s high-cost credit regulations.

- Deliver the Notice Promptly: The notice must be delivered within the 4-day window. It can be served personally, sent via registered mail, or emailed (provided the lender explicitly agreed to electronic communication). Legally, the cancellation is effective on the date it is sent, not the date the lender processes it.

- Return the Principal Immediately: This is the most challenging hurdle. To validly cancel the agreement, you must return the full principal amount of the loan if the funds have already been deposited into your account. You cannot keep the cash and simply cancel the exorbitant interest terms.

- Collect Your Refunded Fees: Once the principal is returned, the lender is legally obligated to refund any non-interest fees you paid upfront, including administrative charges and brokerage fees.

According to Marcus Thorne, a Calgary-based real estate litigator: “If a lender obscures their setup and brokerage fees to keep the stated interest rate artificially low, the true Annual Percentage Rate often breaches the 32 percent threshold, instantly triggering the borrower’s statutory right to rescind. Borrowers must scrutinize the math.”

The 2-Day Disclosure Rule: Your Primary Defense

Because the vast majority of private loans feature an APR below 32%, most borrowers will never have access to the 4-day cancellation right. For these individuals, the true battleground is the pre-signing phase.

Under the provincial Cost of Credit Disclosure Regulation, lenders are legally mandated to provide a comprehensive disclosure statement at least two business days before you incur any financial obligation. This document is your financial blueprint. It explicitly lists the APR, the Total Cost of Credit, and every single fee associated with the transaction. It is highly recommended to use this time to review the impacts of compounding frequency on your total debt load.

Lenders frequently pressure borrowers to sign a “Waiver of Time Period” to expedite funding. While tempting when you need capital quickly, waiving this right removes your only opportunity to step back and evaluate the deal objectively.

Dr. Elena Rostova, Professor of Contract Law at the University of Alberta, notes: “The two-day disclosure window is the most critical, yet most frequently waived, consumer protection mechanism in provincial lending. Waiving it to expedite funding is a catastrophic error for vulnerable borrowers.”

During this period, you should also be organizing and retaining your mortgage documents for future reference, ensuring you have a paper trail if a dispute arises.

Legal Recourse if You Were Misled by a Private Lender

What happens if you discover predatory terms after the contract is signed, and your loan does not qualify for the 4-day rescission rule? You may still have legal avenues, though they require significant effort.

If a lender failed to provide a disclosure statement entirely, or if the provided statement was materially misleading (such as hiding five-figure administrative fees), you might have grounds for action under the Alberta Consumer Protection Act. In specific scenarios, courts can order the lender to return the cost of borrowing, even if the borrower remains responsible for the principal amount.

Furthermore, Canadian courts can strike down “unconscionable transactions”—agreements where the terms are so grossly one-sided and unfair that they shock the conscience of the court. However, pursuing this route is arduous. Legal fees for unconscionable transaction litigation often exceed $15,000, making prevention far more cost-effective than a courtroom cure. Before entering any complex agreement, especially those involving family members, ensure you understand spousal consent and Dower Act requirements to avoid title disputes.

Strategic Alternatives to High-Cost Private Loans

If you are considering a loan with an APR approaching 32%, it is crucial to pause and evaluate alternative financing strategies. High-cost credit should be an absolute last resort, utilized only when a clear, short-term exit strategy is in place.

- B-Lender Debt Consolidation: Institutional B-lenders offer a middle ground between prime bank rates and private lending. In 2026, B-lender rates typically hover between 7% and 12%. While higher than traditional banks, they are vastly superior to high-cost credit products.

- Credit Rehabilitation: If poor credit is forcing you toward predatory lenders, delaying your borrowing by six months to repair your credit score can save you tens of thousands of dollars in interest.

- Refinancing Options: Explore cash-out refinancing alternatives with your current primary mortgage holder before taking on expensive secondary debt.

It is also vital to understand how interest accrues. Many borrowers focus solely on the monthly payment, ignoring how compounding frequency silently increases your debt over the lifespan of the loan.

The Crucial Role of Independent Legal Advice (ILA)

In almost all private lending transactions in Alberta, the borrower is required to obtain Independent Legal Advice (ILA). This is not a mere administrative formality; it is your final safeguard against predatory lending.

Your lawyer has a fiduciary duty to explain the exact nature and legal effect of the documents you are signing. If you harbor any illusions about a 10-day or 3-day cancellation right, this is the moment to ask explicitly: “If I sign this contract today, what are the exact financial penalties if I change my mind tomorrow?”

As David Chen, Director of Consumer Advocacy at the Alberta Financial Protection Bureau, states: “High-cost credit regulations were explicitly designed in 2026 to curb predatory lending practices, ensuring that borrowers trapped in exorbitant loans have a legally protected escape hatch. However, a proactive lawyer is always better than a reactive cancellation.”

A competent lawyer will also ensure you have a comprehensive document checklist completed and will advise you on principal reduction strategies to help you exit the high-interest loan as quickly as possible.

Frequently Asked Questions (FAQ)

Do I have 10 days to cancel a private mortgage in Alberta?

No. The 10-day cooling-off period under the Consumer Protection Act applies strictly to prepaid contracting and direct door-to-door sales. It does not apply to real estate finance or mortgage contracts.

Does the 4-day rescission rule apply to standard bank loans?

Technically yes, but practically no. Major financial institutions and credit unions do not issue loans with an APR of 32% or higher. Therefore, their mortgage products never trigger the high-cost credit rescission regulations.

Can I cancel the agreement if the lender hasn’t given me the money yet?

Generally, yes. Until the funds are formally advanced, you can typically withdraw from the agreement. However, you will likely remain liable for any out-of-pocket costs the lender has already incurred, such as property appraisal fees or legal drafting costs.

What happens if I signed a waiver for the 2-day review period?

If you voluntarily signed a waiver of the 2-day disclosure period, you legally forfeited your right to that waiting window. The mortgage documents you signed immediately afterward are considered fully binding and enforceable.

Is the 32% APR threshold calculated monthly or annually?

APR stands for Annual Percentage Rate. It represents the total yearly cost of borrowing, expressed as a percentage. It includes the base interest rate plus all mandatory non-interest fees associated with securing the loan.

What if the private lender is unlicensed in Alberta?

If a lender is issuing high-cost credit (over 32% APR) without holding the proper provincial licensing from the Financial Consumer Agency or provincial authorities, the agreement may be deemed legally unenforceable, potentially entitling you to recover all paid interest and fees.

Conclusion

The realization that there is no automatic right to cancel a standard mortgage in Alberta is often a sobering moment for borrowers. It underscores the immense importance of due diligence before closing day. While the 4-day rescission rule provides a vital safety net for those caught in exorbitant high-cost credit agreements, the vast majority of borrowers must rely on proactive protection. Read your disclosure statements meticulously, calculate the true APR, and never waive your right to review the terms.

Don’t navigate complex real estate finance laws in the dark. If you are unsure about the terms of a loan or need help understanding your legal rights in 2026, professional guidance is essential. Contact us today to discuss your financing options and ensure your home equity is protected.