When a homeowner in Calgary falls behind on mortgage payments, lenders may initiate foreclosure proceedings. This legal action transfers ownership of the property back to the lender, often leading to eviction. Understanding this sequence helps homeowners navigate challenges and explore options early.

When a homeowner in Calgary falls behind on mortgage payments, lenders may initiate foreclosure proceedings. This legal action transfers ownership of the property back to the lender, often leading to eviction. Understanding this sequence helps homeowners navigate challenges and explore options early.

Foreclosure typically begins after multiple missed payments, triggering a formal notice from the bank. Courts then review the case to confirm the debt and authorize a sale. Once finalized, the lender regains control of the home, and occupants may face removal under a court-issued order.

Timely communication with your mortgage provider can sometimes delay or prevent this outcome. For personalized guidance, contact The Second Mortgage Store at +1 403-827-6630. Their team helps Calgary residents evaluate financial solutions tailored to their situation.

Key Takeaways

- Foreclosure transfers ownership to lenders when payments lapse, often leading to eviction.

- Courts validate debts and approve property sales during legal proceedings.

- Lenders manage foreclosure timelines and auction processes to recover loan amounts.

- Redemption periods or agreements may temporarily halt eviction in specific cases.

- Proactive communication with mortgage providers can create alternatives to foreclosure.

Introduction to Foreclosure and Eviction in Calgary

In Calgary’s real estate market, financial challenges sometimes lead to lenders reclaiming homes through legal channels. This occurs when owners struggle with payment obligations, initiating a sequence of events that impacts both parties. Navigating these situations requires awareness of rights, timelines, and available resources.

Expert Guidance Through Complex Transitions

The Second Mortgage Store specializes in helping residents manage difficult financial circumstances. Their advisors work directly with homeowners to explore alternatives like payment restructuring or refinancing. “Early intervention often creates pathways to retain ownership,” notes a company representative. Reach their team at +1 403-827-6630 for tailored strategies.

Common Triggers for Ownership Changes

Multiple missed installments typically activate lender protocols. Financial institutions must follow provincial regulations when pursuing remedies:

- Three consecutive overdue notices usually precede formal action

- Judicial reviews validate debt amounts before property listing

- Power of sale arrangements allow faster resolution than full foreclosure

Understanding loan agreements helps prevent surprises. Regular communication with creditors can identify solutions before accounts reach critical status. Professionals like those at The Second Mortgage Store analyze individual circumstances to suggest practical next steps.

What is the eviction process after foreclosure calgary

Legal property transfers in Alberta follow strict protocols once lenders secure ownership rights. Former occupants receive formal documentation outlining their obligations and deadlines. This phase involves coordinated actions between financial institutions and judicial authorities.

Step-by-Step Overview of the Process

After a court-approved foreclosure, lenders must follow these stages:

- Notice of Possession: Sent via registered mail, giving 30 days to vacate

- Redemption Order: Final opportunity to settle debts (typically 6 months)

- Writ of Possession: Court enforcement if occupants remain post-deadline

“Many homeowners don’t realize they can negotiate move-out extensions,” advises The Second Mortgage Store. “Early dialogue prevents abrupt displacement.”

Court Involvement and Lender Notifications

Judicial oversight ensures compliance with Alberta’s Civil Enforcement Act. Key interactions include:

| Stage | Timeframe | Required Documents |

|---|---|---|

| Statement of Claim Filing | 21 days post-default | Mortgage agreement, payment history |

| Redemption Period Start | Court order date | Certificate of Title search |

| Eviction Enforcement | 30 days post-judgment | Writ of Possession |

Financial institutions often pursue power of sale arrangements to expedite property transitions. This approach allows faster resolution than traditional foreclosure while protecting borrower equity. Professionals like those at +1 403-827-6630 help interpret lender communications and explore alternatives.

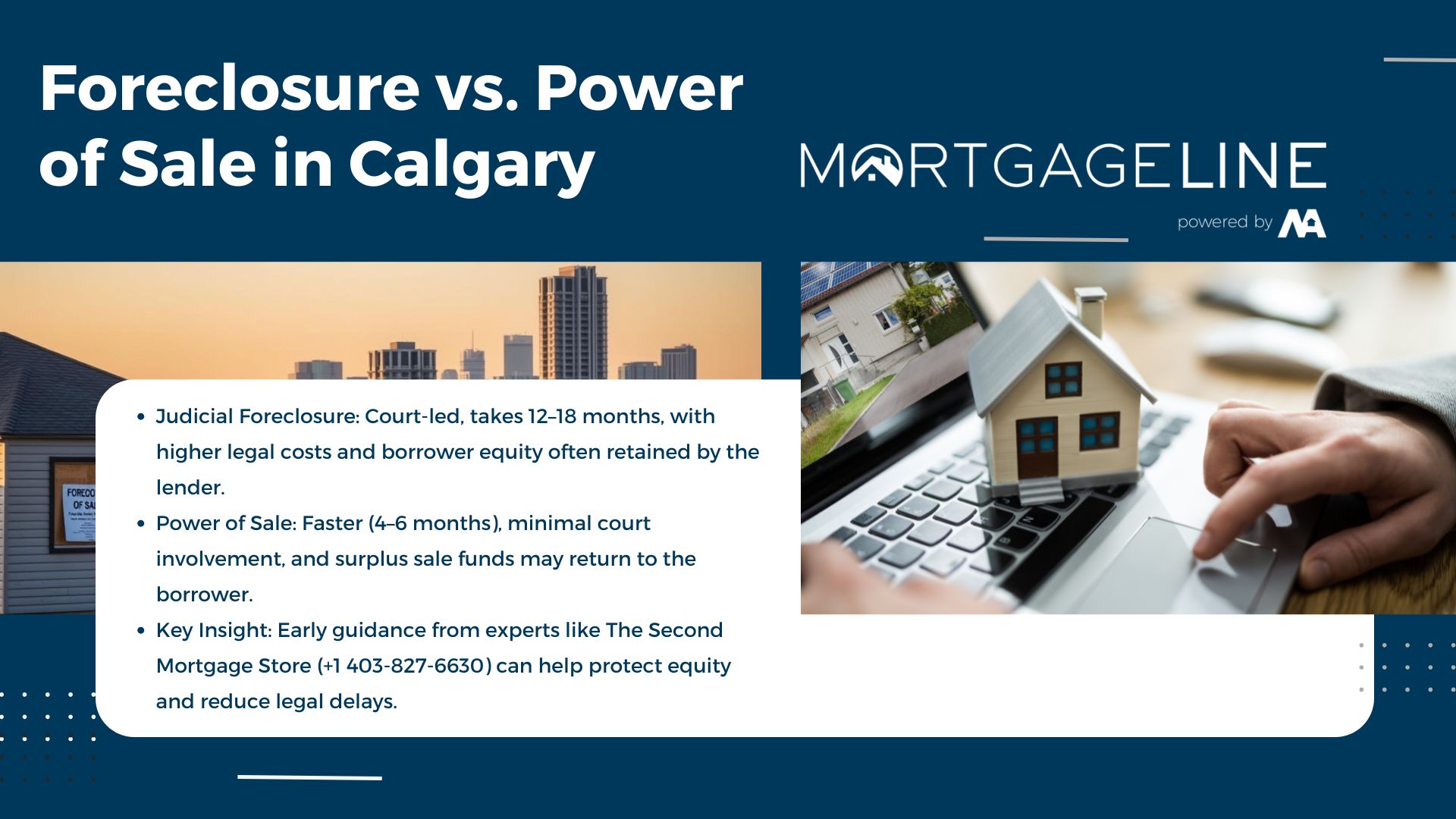

Foreclosure vs. Power of Sale: Lender Actions in Calgary

Lenders in Calgary employ distinct strategies when reclaiming properties from borrowers facing financial strain. Two primary methods govern these transitions: judicial foreclosure and power of sale. Each approach carries unique implications for timelines, equity retention, and legal oversight.

Judicial Foreclosure Process Explained

Judicial foreclosure requires full court supervision. Lenders must file a statement of claim and prove mortgage defaults through hearings. Alberta’s courts typically allow a 6-month redemption period post-judgment, giving borrowers time to settle debts. This method often takes 12-18 months to complete.

“Court-managed foreclosures protect borrower rights but extend uncertainty for both parties,” explains The Second Mortgage Store advisor. “Exploring alternatives early can prevent lengthy battles.”

The Power of Sale and Its Benefits

Power of sale clauses in mortgage agreements enable faster resolutions. Lenders can sell property without court orders, often within 4-6 months. This method requires fewer fees and allows borrowers to recover surplus funds if the sale exceeds owed amounts.

| Factor | Judicial Foreclosure | Power of Sale |

|---|---|---|

| Average Timeline | 12-18 months | 4-6 months |

| Court Involvement | Mandatory | Minimal |

| Equity Handling | Retained by lender | Surplus returned |

| Average Legal Costs | $8,000-$12,000 | $3,000-$5,000 |

While power sales expedite property transitions, they offer less oversight. The Second Mortgage Store (+1 403-827-6630) helps homeowners evaluate which approach aligns with their financial recovery goals. Understanding these options empowers informed decisions during challenging circumstances.

Key Factors Influencing Foreclosure and Eviction Outcomes

Financial missteps and legal timelines often determine whether homeowners retain or lose their properties. Missed obligations and procedural deadlines create ripple effects that shape long-term stability. Recognizing these elements helps individuals address risks proactively.

Mortgage Payment Defaults and Legal Notice Periods

Consistent payment gaps trigger lender responses. Creditors typically issue formal notices after 30-60 days of delinquency, initiating Alberta’s foreclosure framework. A statement of claim filed in court starts the countdown for debt resolution or property loss.

| Days Delinquent | Lender Action | Credit Impact |

|---|---|---|

| 30 | Default notice sent | Score drops 50-100 points |

| 90 | Court filing initiated | Additional 50-point decline |

| 180+ | Redemption period expires | Foreclosure recorded |

Longer delinquency periods reduce negotiation leverage. Banks may accelerate proceedings if multiple notices go unanswered. Legal fees and penalties also accumulate, eroding potential equity.

Impact on Credit and Home Equity

Foreclosures remain on credit reports for six years, limiting future loan approvals. Homeowners often lose accumulated equity unless surplus funds exist post-sale. The Second Mortgage Store notes: “Even one late payment can lower scores, but strategic planning can minimize damage.”

Key financial consequences include:

- Credit utilization ratios spike as available limits shrink

- Equity recovery requires prompt debt settlement before auctions

- Refinancing options diminish without stable payment histories

Consulting advisors early helps preserve financial health. Contact The Second Mortgage Store at +1 403-827-6630 to explore tailored solutions before accounts reach critical stages.

Strategies to Avoid and Navigate Eviction Challenges

Homeowners facing financial hurdles can take proactive steps to protect their residences and financial stability. Early intervention often creates opportunities to renegotiate terms or explore alternative solutions. Below are practical approaches to manage lender relationships and legal obligations effectively.

Negotiating with Lenders and Refinancing Options

Open communication with creditors is critical when mortgage payments become unmanageable. Many institutions offer temporary relief through:

- Payment deferrals (3-6 month pauses)

- Interest rate reductions (0.5%-2% decreases)

- Loan term extensions (adding 5-10 years)

| Refinancing Option | Typical Terms | Approval Time |

|---|---|---|

| Rate Revisions | Fixed rates for 2-5 years | 2-4 weeks |

| Debt Consolidation | Combines multiple loans | 3-6 weeks |

| Equity Access | 80%-95% LTV ratios | 4-8 weeks |

Legal and Financial Remedies to Protect Your Home

When negotiations stall, legal avenues may delay or prevent displacement. Filing a statement of claim challenges improper lender actions, while consumer proposals freeze proceedings for up to five years. Bankruptcy remains a last-resort option but stops immediate foreclosure.

“Legal tools require precise execution—professional guidance ensures compliance with Alberta’s timelines,” advises The Second Mortgage Store team. Contact them at +1 403-827-6630 for structured plans.

Key considerations for preserving equity:

- Act within 21 days of receiving default notices

- Document all lender communications

- Review property valuations before agreeing to sales

Conclusion

Navigating financial hardships requires understanding both risks and remedies. From initial default notices to final court orders, each phase demands informed decisions. Timely communication with your lender can unlock alternatives like revised payment plans or refinancing agreements.

Critical factors—like equity retention and credit protection—hinge on swift action during redemption periods. Knowledge of power sale options versus judicial processes helps prioritize financial recovery. Professionals analyze mortgage terms and provincial regulations to identify optimal paths forward.

The Second Mortgage Store offers Calgary homeowners tailored strategies to address complex real estate challenges. Their team clarifies timelines, evaluates property valuations, and negotiates with creditors. Contact them at +1 403-827-6630 to explore solutions before accounts escalate to critical stages.

Empowerment through expertise transforms overwhelming situations into manageable steps. With proactive planning and trusted guidance, residents can safeguard their home and financial future.