Foreclosure rights in Alberta dictate that lenders cannot arbitrarily seize your property after a missed payment. Under provincial law, homeowners are guaranteed a formal judicial process, a strict 20-day response window following a Statement of Claim, and a standard six-month redemption period to settle arrears or sell the property. Understanding these statutory protections empowers you to negotiate with lenders, leverage your home equity, and potentially halt legal proceedings before you lose your investment.

Key Takeaways

- Judicial Process: Alberta is a judicial foreclosure province, meaning lenders must process all actions through the Court of King’s Bench.

- Response Window: You have exactly 20 days to file a Statement of Defence or Demand for Notice after receiving a Statement of Claim.

- Redemption Period: Courts typically grant a six-month window to pay off the arrears or sell the property, though this can be shortened if the property lacks equity.

- Deficiency Judgments: Conventional mortgages are generally protected from deficiency judgments, whereas insured mortgages (CMHC) are not.

- Proactive Solutions: Refinancing, negotiating forbearance, or securing alternative financing are highly effective if initiated early.

The Legal Framework Governing Alberta Foreclosures in 2026

Property ownership and lender rights in the province are strictly regulated by the Law of Property Act. Unlike jurisdictions that allow power-of-sale evictions, Alberta requires banks to prove their case before a judge. This judicial oversight provides a vital layer of protection for borrowers facing financial distress.

According to 2026 data from the Canadian Bankers Association, mortgage arrears in Alberta currently sit at approximately 0.45%. While this represents a fraction of total homeowners, the economic shifts of recent years have made lenders more systematic in their recovery efforts. Financial institutions now rely heavily on automated tracking systems to issue demand letters the moment an account falls 60 days past due.

As David Thompson, Senior Legal Counsel at the Alberta Real Estate Institute, explains: “The judicial nature of Alberta’s system is a double-edged sword. It guarantees homeowners a fair hearing and ample time to respond, but it also means that legal fees accumulate rapidly, directly eating into the homeowner’s remaining equity.”

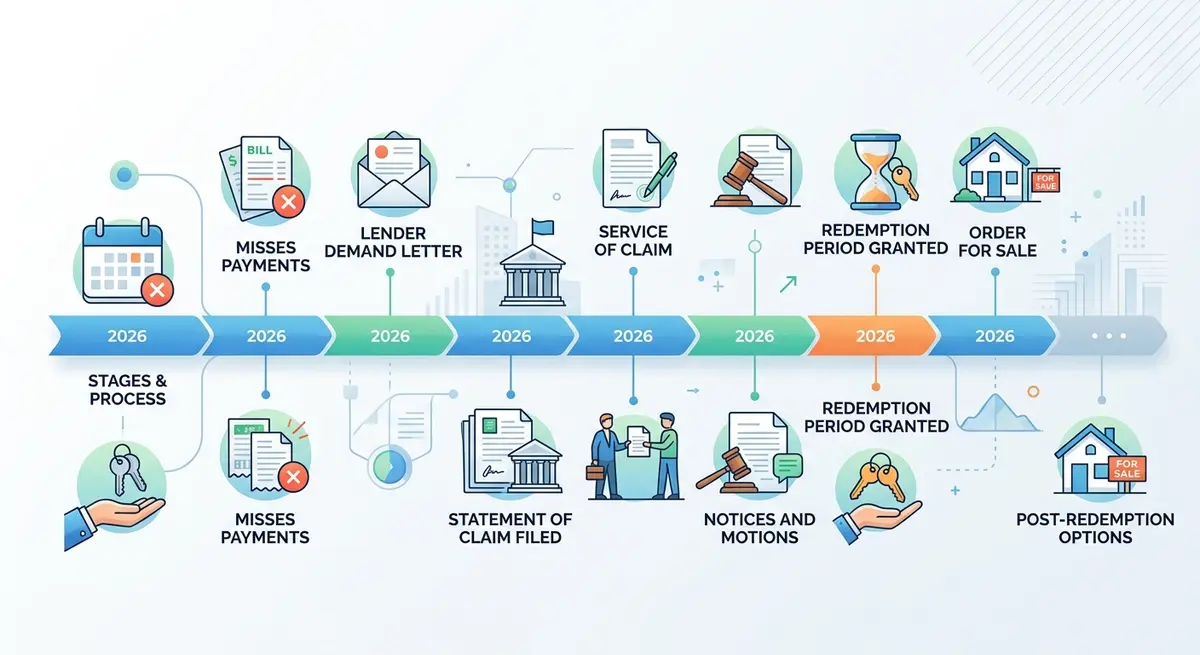

The Step-by-Step Foreclosure Timeline

Navigating property disputes requires a clear understanding of the legal timeline. Lenders follow a highly structured progression when initiating legal action against a borrower.

- Missed Payments and Internal Collections (Days 1-60): After your first missed payment, the lender’s internal collections department will reach out. By the third consecutive missed payment, the file is typically flagged for legal escalation.

- The Demand Letter (Days 60-90): The lender’s legal counsel sends a formal demand letter via registered mail. This document provides a final deadline to pay the arrears before court action begins.

- Filing the Statement of Claim (Day 90+): This marks the official start of the lawsuit. The document outlines the exact amount owed, including principal, interest, and legal fees. Understanding the difference between a Notice of Default and a Statement of Claim is critical at this juncture.

- The 20-Day Response Window: Upon being served, you have 20 days to file a legal response. Failing to act allows the lender to note you in default and proceed unopposed.

- The Redemption Period: If the court rules in the lender’s favor, a judge will issue a Redemption Order. This grants the homeowner a specific timeframe—usually six months—to redeem the mortgage by paying the outstanding balance.

Critical Legal Thresholds and Homeowner Protections

The court system provides several off-ramps for homeowners willing to take decisive action. The amount of equity in your property heavily influences the options available to you during the redemption phase. If your home’s market value significantly exceeds the mortgage balance, judges are far more likely to grant maximum redemption times.

To fully grasp your timeline, you must understand the mechanics of calculating your exact redemption period. Courts evaluate the property’s appraised value, the total debt, and the current real estate market conditions before setting this deadline.

| Legal Stage | Timeframe | Financial Impact | Homeowner Action Required |

|---|---|---|---|

| Demand Letter | 10-15 Days | Minimal legal fees added | Negotiate forbearance or pay arrears |

| Statement of Claim | 20 Days to Respond | Significant legal costs begin | File Statement of Defence/Demand for Notice |

| Redemption Order | Up to 6 Months | Compounding interest & court costs | Refinance, sell property, or secure alternative lending |

| Final Order | Immediate | Total loss of property equity | Vacate premises |

Financial Repercussions: Credit Impact and Deficiency Judgments

The financial damage of a property seizure extends far beyond the loss of the physical asset. When a lender files a Statement of Claim, the action is recorded on your credit profile. According to Equifax Canada, a completed foreclosure can plummet a borrower’s credit score by 120 to 160 points, remaining on the report for up to six years.

Furthermore, homeowners must be acutely aware of their liability regarding unsecured shortfalls. If the property is sold for less than the outstanding mortgage balance, the lender may pursue the borrower for the difference. However, Alberta law distinguishes between conventional and insured mortgages. Conventional mortgages (where the borrower put down 20% or more) are generally non-recourse, protecting the borrower from deficiency judgment calculations.

Conversely, if your mortgage is insured by the CMHC, Sagen, or Canada Guaranty, the insurer can and will pursue you for the shortfall. This reality makes understanding wage garnishment risks essential for anyone holding a high-ratio mortgage in 2026.

Strategic Defenses: How to Halt Legal Proceedings

Inaction is the single biggest mistake a homeowner can make. Courts heavily favor borrowers who demonstrate a genuine effort to resolve their financial obligations. Research from the Bank of Canada indicates that over 68% of homeowners who engage in early mediation with their lenders successfully avoid losing their homes.

Sarah Jenkins, Chief Financial Analyst at Calgary Housing Metrics, notes: “In 2026, leveraging existing home equity is the most viable defense mechanism. Even with damaged credit, homeowners can often secure secondary financing to pay out the demanding lender and pause the legal clock.”

When responding to a Statement of Claim, you must immediately assess your refinancing options. If traditional banks refuse to renew your term due to missed payments, private lenders or alternative financing institutions can provide bridge loans. It is vital to weigh the costs of second mortgages versus cash-out refinancing to determine the most sustainable path forward.

Navigating Court Proceedings and Legal Documentation

The terminology used in the Court of King’s Bench can be intimidating. A “lis pendens” (Certificate of Lis Pendens) is registered against your property title to notify the public of pending litigation. This effectively freezes your ability to sell or refinance the property without the court’s or lender’s permission.

If you fail to resolve the debt during the redemption period, the lender will apply for a Final Order. The final order of foreclosure timeline moves rapidly once the redemption period expires. Depending on the property’s value, the judge will issue either an Order for Sale (listing the property with a realtor) or a Rice Order (transferring the title directly to the lender).

Marcus Thorne, a Calgary-based mortgage strategist, states: “Ignoring court documents accelerates your loss of control. Filing a Demand for Notice ensures the lender cannot proceed with any court applications without notifying you first. This simple legal step buys you crucial time to arrange alternative financing.”

Conclusion

Facing property litigation is undeniably stressful, but understanding your legal rights in Alberta transforms you from a passive participant into an empowered negotiator. The judicial system is designed to give you time—time to respond, time to secure financing, and time to protect your equity. From the moment a Statement of Claim is filed to the expiration of the redemption period, every day counts.

By tracking strict deadlines, maintaining open communication with your lender, and exploring alternative equity solutions, you can successfully navigate these complex legal waters. Do not wait until a Final Order is imminent to seek professional guidance. Contact our team today to explore your refinancing options and build a strategic defense for your property.

Frequently Asked Questions

How long does the legal process take if a lender initiates proceedings in Alberta?

The timeline varies based on court availability and homeowner response, but it generally takes between 6 to 10 months from the first missed payment to a final order. The mandatory redemption period alone typically accounts for six months of this timeline.

Can you stop a lender from taking control of your home after a Statement of Claim is filed?

Yes. You can halt the process by paying the arrears and legal costs, negotiating a forbearance agreement, or refinancing the debt. Filing a Statement of Defence or Demand for Notice ensures you remain involved in the judicial process.

How does equity influence outcomes during court proceedings?

Equity is your strongest asset. If you have substantial equity, judges are more likely to grant longer redemption periods. Furthermore, high equity allows you to secure alternative financing to pay off the demanding lender entirely.

What happens to other debts if a bank repossesses your house?

Losing your home does not erase unsecured debts like credit cards or personal loans. If your mortgage was CMHC-insured, you might also face a deficiency judgment for any shortfall after the property is sold.

Are there early signs that might help avoid legal action?

Consistent late payments, penalty fees, and internal collection calls are immediate red flags. Addressing these issues before the file is transferred to the lender’s legal department saves thousands in legal fees and prevents credit damage.

Why is it important to file a Demand for Notice?

Filing a Demand for Notice legally requires the lender to inform you of any future court applications regarding your property. This prevents them from obtaining default judgments behind your back and keeps you informed of all legal maneuvers.