The primary difference between a Notice of Default and a Statement of Claim in Alberta is their legal standing and required response time. A Notice of Default (often called a Demand Letter) is a formal warning from a lender’s lawyer granting you 10 days to pay missed mortgage arrears before court action begins. Conversely, a Statement of Claim is an active, public lawsuit filed in the Court of King’s Bench that triggers a strict 20-day deadline to file a legal defense or risk losing your property entirely.

Key Takeaways

- Legal Status: A Notice of Default is a private warning; a Statement of Claim is a public lawsuit.

- Critical Deadlines: You have 10 days to respond to a Demand Letter, but exactly 20 calendar days to respond to a Statement of Claim.

- Financial Impact: Resolving default at the warning stage costs roughly $300 to $600 in legal fees, whereas a filed lawsuit instantly escalates costs to $2,500 or more.

- Required Action: Ignoring court documents leads to being “Noted in Default,” meaning the lender can seize the property without your input.

- Strategic Defense: Filing a Demand of Notice ensures you are legally informed of every step the bank takes during the litigation process.

- Equity Solutions: Alternative financing can be used to pay out the reinstatement amount and halt the legal machinery entirely.

Understanding the Alberta Foreclosure Timeline in 2026

Finding a dense, aggressive legal document from your mortgage lender in the mailbox is a heart-stopping moment. The threat of losing your home feels immediate, and the legal jargon is intentionally intimidating. However, not all legal notices carry the same weight. In the 2026 Alberta real estate landscape, understanding exactly where you stand in the foreclosure timeline is the single most important step in preserving your home equity.

Before a lender can seize your property, they must follow a strict judicial process governed by provincial law. According to the Alberta Court of King’s Bench, property seizure is a multi-step legal procedure designed to give homeowners specific windows of opportunity to remedy their default. The confusion often lies in distinguishing between the preliminary warning and the actual lawsuit.

Data from the Bank of Canada‘s early 2026 Financial System Review indicates that mortgage arrears have increased by 14% year-over-year, making it more critical than ever for homeowners to understand their rights. Grasping the distinction between these two documents dictates your urgency level, your legal costs, and your available defense strategies.

What is a Notice of Default (Demand Letter)?

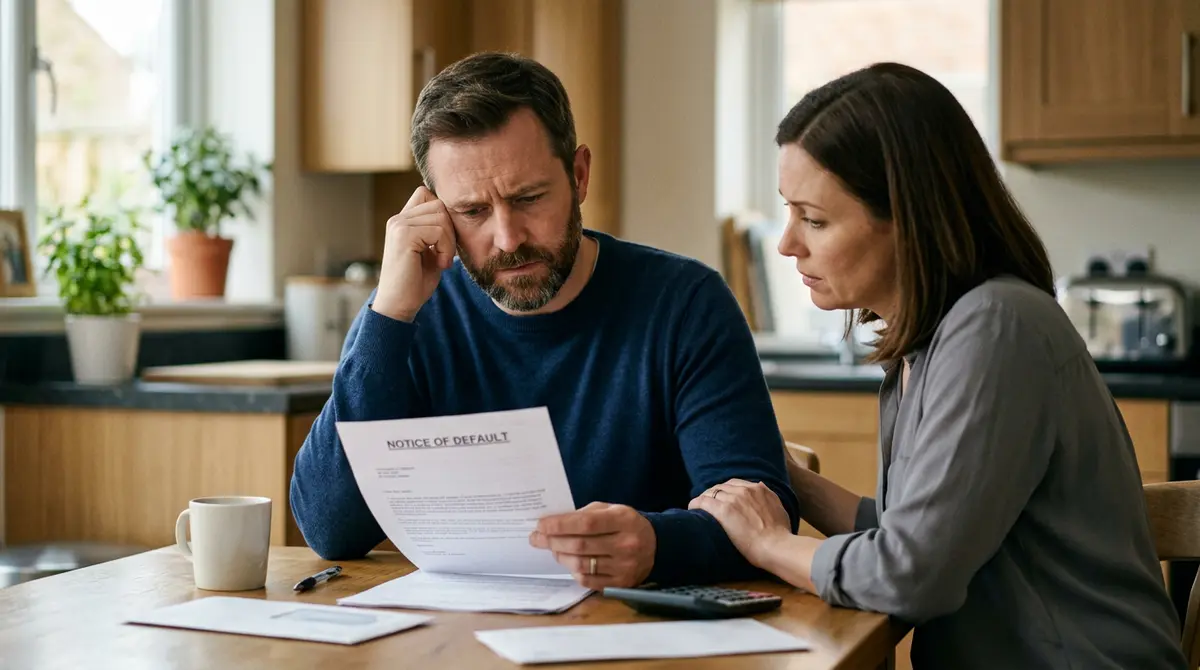

Before a financial institution can sue you, they generally must give you a formal chance to fix the contractual breach. This comes in the form of a Demand Letter, frequently referred to as a Notice of Default, sent by the lender’s legal counsel. While it is not a court order, it is the final barrier before the judicial system gets involved.

The Demand Letter confirms that you have defaulted on your mortgage contract, usually triggered after two to three consecutive missed payments. It formally demands that you pay the total arrears (the sum of your missed payments) plus accumulated interest and initial legal fees by a specific calendar date.

You typically have exactly 10 days from the date of the letter to remit payment. If you pay the requested amount, the file is immediately closed, and you resume your normal mortgage schedule. If you ignore it, the lawyer is legally instructed by the bank to draft and file a Statement of Claim. At this preliminary stage, the legal fees added to your mortgage balance are relatively low—usually between $300 and $600. Paying now prevents these solicitor-client costs from ballooning into the thousands.

What is a Statement of Claim?

If the deadline in the Demand Letter passes without payment or negotiation, the lender files a Statement of Claim at the courthouse. This represents the “point of no return” where a private financial dispute escalates into a public lawsuit. You are officially a Defendant in a legal proceeding.

The Statement of Claim outlines the specific mortgage details, the exact default amount, and the remedy the lender is seeking—which is invariably the judicial sale of your home or direct possession of the property. You will be served this document either personally by a process server or via registered mail.

As Dr. Michael Chen, Professor of Property Law at the University of Calgary, explains: “Homeowners often paralyze themselves with fear upon receiving court documents. Understanding the exact procedural differences between these notices is the only way to effectively halt the foreclosure machinery before equity is entirely eroded by legal fees.”

Once served, the clock starts ticking. If you need guidance on filing a response to a foreclosure claim, it is imperative to act swiftly to protect your rights.

Side-by-Side Comparison: Warning vs. Lawsuit

To fully grasp the dynamics of these two distinct legal phases, review this direct comparison. This table outlines the critical differences in origin, deadlines, and financial impact in 2026.

| Feature | Notice of Default (Demand Letter) | Statement of Claim |

|---|---|---|

| Source Document | Lender’s Private Lawyer | Court of King’s Bench |

| Legal Status | Formal Warning | Active Public Lawsuit |

| Action Deadline | Usually 10 Days | Strictly 20 Calendar Days |

| Average Legal Costs | Low ($300 – $600) | High ($1,500 – $3,500+) |

| Consequence of Inaction | Escalation to Lawsuit | Loss of Title / Judicial Sale |

| Required Action | Pay Arrears Immediately | File Demand of Notice |

The Critical 20-Day Deadline: Step-by-Step Response Guide

This is the most critical number in Alberta property law. Once you are served with a Statement of Claim, you have exactly 20 calendar days to file a formal response with the court. If you are holding either of these documents right now, time is your most valuable asset. Follow this exact step-by-step process to protect your property rights.

- Calculate Your Deadline: Read the date on the document immediately. If it is a Statement of Claim, count 20 calendar days (including weekends) from the day you were served. This is your absolute deadline.

- Request a Payout Statement: Contact your lender’s lawyer in writing and ask for the exact “reinstatement amount.” This figure includes your missed payments, accumulated interest, and current legal fees.

- File a Demand of Notice: If you admit you owe the money but want to be legally notified of every subsequent step the lender takes, go to the courthouse and file a Demand of Notice. This legally forces the bank to keep you informed, preventing them from securing a default judgment behind your back.

- Consider a Statement of Defence: This should only be filed if the lender made a factual legal error (e.g., you actually made the payments, or the accounting is demonstrably false).

- Assess Your Home Equity: Determine the current 2026 market value of your home minus your outstanding mortgage balance. If you have more than 25% equity, you have strong refinancing options available outside the traditional banking system.

If you fail to act within this 20-day window, the lender will “Note you in Default.” This severe consequence means the lender can walk into court and ask a judge for an order to sell your house without your input or presence. You completely lose your voice in the legal process.

The Financial Impact: Why Legal Fees Explode

One of the most misunderstood aspects of this legal transition is the exponential growth of legal fees. Standard Alberta mortgages contain a “solicitor-client costs” clause. This means you, the borrower, are 100% responsible for paying the bank’s legal bills to sue you.

At the Demand Letter stage, the lawyer simply drafts a standardized letter. The cost is minimal. However, once a Statement of Claim is initiated, the lawyer must draft a complex legal claim, pay provincial court filing fees, hire a private process server to locate you, and prepare sworn affidavits. Legal fees instantly jump from an average of $450 to over $2,500.

As Sarah Jenkins, Senior Foreclosure Counsel at the Canadian Bar Association, notes: “The transition from a demand letter to a statement of claim is the point of no return for legal costs. Every single day a homeowner waits to address a filed claim adds hundreds of dollars to their final redemption bill.”

Navigating the Redemption Period and Questioning Process

Receiving a Statement of Claim does not mean the sheriff is arriving tomorrow to change your locks. The Alberta judicial system provides specific mechanisms to protect homeowners, provided you actively participate in the process.

If the lender successfully proves your default in court, the judge will issue an Order Nisi. This order establishes a Redemption Period—a specific timeframe granted by the court for you to pay the arrears, pay out the entire mortgage, or sell the property yourself. While the standard period is six months, lenders will aggressively petition the court to shorten this to as little as one day if you have minimal equity. It is vital to accurately calculate your redemption period to know exactly how much time you have to secure alternative financing.

In contested cases, the lender’s lawyer may require you to answer questions under oath regarding your finances and the property’s condition. Understanding the questioning for discovery process is essential if you plan to file a Statement of Defence rather than a simple Demand of Notice.

Using Home Equity to Halt Legal Proceedings

If you have received a Statement of Claim, your traditional bank will no longer accept a simple promise to pay. They require certified funds. Furthermore, because your credit score has been severely damaged by the missed payments, you will not qualify for a standard bank loan to consolidate the debt.

This is where alternative equity lending becomes a vital tool. A private mortgage utilizes the existing equity in your home to generate a lump sum of cash, bypassing strict bank income requirements. You use this cash to pay the exact reinstatement amount (arrears plus legal fees), which legally forces the bank to halt the action and return your mortgage to “good standing.”

Statistics from the Canada Mortgage and Housing Corporation (CMHC) show that in 2026, over 35% of halted legal actions in Alberta were resolved through private equity refinancing rather than property sales.

Case Study: Preserving Equity in Calgary

Consider a recent 2026 scenario where a homeowner received a Statement of Claim for $12,000 in arrears and $3,500 in legal fees. Their home was valued at $600,000, with a first mortgage of $400,000. Because they had $200,000 in equity, an alternative lender approved a $25,000 loan within 48 hours. The funds were sent directly to the bank’s lawyer in trust, immediately stopping the final order timeline and saving the family’s home.

Edge Cases and Devastating Mistakes to Avoid

The most devastating mistake Alberta homeowners make is practicing “avoidance behavior.” Ignoring registered mail or refusing to answer the door for a process server does not stop the lawsuit; it simply accelerates the lender’s ability to secure a default judgment.

Elena Rostova, a representative with the Financial Consumer Agency of Canada (FCAC), warns: “Burying your head in the sand is the most expensive mistake a borrower can make. The legal system operates on strict timelines, and silence is legally interpreted as surrender.”

Another common error is relying on verbal promises from bank branch employees. Once your file is transferred to the bank’s legal department, the branch manager has zero authority to stop the process. Only certified funds delivered to the foreclosing lawyer can halt the machinery.

Furthermore, homeowners must be aware of post-litigation risks. If the property is eventually sold by the court for less than the mortgage balance, you may face severe consequences. Understanding deficiency judgment calculations and the reality of wage garnishment risks is crucial for anyone navigating these turbulent waters. Additionally, if you are attempting to sell the home yourself, you will likely need to navigate discharging a lis pendens from your property title before a buyer can take possession.

Conclusion

Navigating property dispute resolutions requires clear-headed action. The difference between a Demand Letter and a Statement of Claim is the difference between a warning shot and a declaration of war. By understanding the strict 2026 timelines of the Alberta legal process, you can make informed, strategic decisions that protect your hard-earned equity. If you are facing mounting legal fees and aggressive bank lawyers, do not wait until your 20-day window expires. Contact our team today to explore your equity-based financing options and stop the legal machinery in its tracks.

Frequently Asked Questions (FAQ)

Can I stop a foreclosure after receiving a Statement of Claim?

Yes. You can legally stop the process at any time before the final judicial sale by paying the “reinstatement amount.” This amount includes all missed payments, accumulated interest, and the lender’s legal fees to date.

What happens if I completely ignore the Statement of Claim?

If you ignore the document for 20 days, the lender will note you in default. They will then proceed to ask the court for an Order Nisi and eventually a judicial sale or final order, entirely without your input or defense.

Do I need to hire a lawyer to file a Demand of Notice?

Technically, no. You can obtain the standard forms from the Alberta Court of King’s Bench and file them yourself as a self-represented litigant. However, consulting with a legal professional ensures the paperwork is filed correctly and on time.

Does a Demand Letter ruin my credit score?

The Demand Letter itself is not reported to credit bureaus, but the 60 to 90 days of missed mortgage payments that triggered the letter will severely damage your credit score. A filed Statement of Claim, however, becomes a matter of public record.

Can I sell my house myself after the lawsuit starts?

Yes. During the court-ordered Redemption Period, you retain the right to list and sell the property yourself. Selling it privately is almost always more profitable than allowing the court to conduct a judicial sale.

Will alternative financing cover the bank’s legal fees?

Yes. When arranging emergency equity financing, private lenders calculate the total loan amount to cover your mortgage arrears, the bank’s legal fees, and any associated closing costs, providing a complete buyout solution.