When evaluating secondary financing options in 2026, the most critical warning signs of predatory lending include demands for upfront fees before approval, high-pressure sales tactics, lack of verifiable provincial licensing, and guaranteed approvals that ignore your credit history. Identifying these red flags early is essential to protect your home equity from exorbitant fees, aggressive compounding interest, and draconian penalty structures designed to force default. By conducting thorough due diligence and understanding standard Alberta lending regulations, borrowers can safely navigate the private financing market and secure funding that genuinely supports their financial goals.

Key Takeaways

- Never pay large upfront fees: Legitimate lenders deduct administrative and legal fees from the mortgage advance at closing, not before approval.

- Verify provincial licensing: All reputable brokers and lenders operating in Alberta must be registered with the Real Estate Council of Alberta (RECA).

- Beware of “Loan-to-Own” schemes: Predatory lenders intentionally structure loans with impossible repayment terms to trigger default and seize your property.

- Scrutinize the fine print: Pay close attention to compounding interest frequencies, excessive renewal fees, and severe prepayment penalties.

- Seek independent counsel: Always have your own real estate lawyer review commitment letters before signing.

The 2026 Alberta Secondary Financing Landscape

The private lending market operates within a unique economic environment that homeowners must understand before engaging with potential financial partners. In 2026, the provincial economy has seen stabilized growth in the energy and technology sectors, pushing average detached home prices in major urban centers above $740,000, according to recent data from regional real estate boards. This surge in property values has created substantial home equity for long-term residents. Consequently, leveraging property equity has become an increasingly popular tool for debt consolidation, home renovations, and business investments.

However, this wealth of untapped equity has also attracted unscrupulous operators. According to the Financial Consumer Agency of Canada (FCAC), predatory lending complaints increased by 22% nationwide over the past two years, with Alberta experiencing a specific 15% spike in unregulated private lending disputes in early 2026. During periods of economic fluctuation, some lenders exploit homeowners’ financial vulnerabilities, disguising toxic loan products as financial lifelines.

As Dr. Michael Chen, Professor of Real Estate Finance at the University of Calgary, explains: “The 2026 lending environment has created a perfect storm. With traditional banks maintaining strict debt-service ratios, vulnerable homeowners are turning to the shadow banking sector, where predatory lenders hide exorbitant annualized percentage rates (APRs) behind complex compounding structures.”

Critical Warning Signs of Predatory Lending

Understanding what warning signs to watch for can save you from costly mistakes and severe financial hardship. While the private lending space is filled with legitimate, helpful institutions, distinguishing them from bad actors requires vigilance.

1. Demands for Significant Upfront Payments

One of the most glaring warning signs is a lender demanding large upfront fees before issuing a formal commitment letter. While it is standard practice to pay an independent, third-party appraiser directly for a property valuation, you should never pay “application fees,” “processing fees,” or “insurance premiums” directly to the lender in advance.

Legitimate lenders roll their brokerage and lender fees into the final loan amount, deducting them from the total funds advanced by the lawyer on closing day. Fraudulent operators often collect these advance fees and disappear without ever funding the loan.

2. High-Pressure Sales Tactics and Artificial Urgency

Legitimate financial institutions will never pressure you into making immediate decisions. If a representative claims that an interest rate is “only good for the next 24 hours” or threatens to withdraw the offer if you seek independent legal advice, walk away immediately. Professional lenders understand that borrowing against your property is a major financial decision. They will provide you with a comprehensive document checklist and afford you ample time to review the terms with your family and legal counsel.

3. Unverifiable Provincial Licensing

In Alberta, mortgage brokers and many types of lenders must be licensed through the Real Estate Council of Alberta (RECA). A lender’s inability or evasiveness when asked to provide proof of proper licensing is a definitive red flag. Unlicensed entities operate outside of provincial consumer protection regulations, leaving you with little recourse if the transaction goes sideways. Always verify a professional’s standing using RECA’s online public registry before sharing personal information.

4. Unrealistic “Guaranteed” Approvals

Be highly suspicious of marketing materials or representatives that promise “100% Guaranteed Approval” regardless of your income, credit history, or property condition. Legitimate lenders, even those specializing in bad credit or alternative lending, must assess risk appropriately. They calculate Loan-to-Value (LTV) ratios and evaluate your exit strategy. A lender who doesn’t care about your ability to repay the loan is likely employing a “loan-to-own” strategy—hoping you default so they can seize the property.

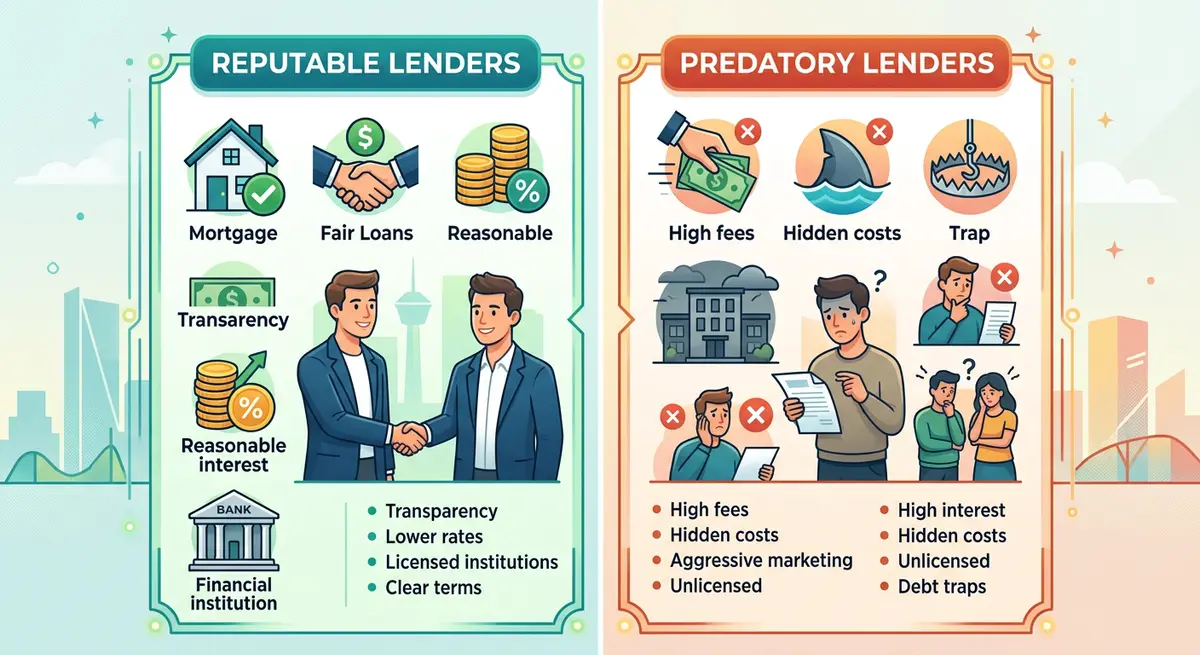

Reputable vs. Predatory Lenders

To further clarify the differences, review this comparison table highlighting standard practices versus predatory behaviors in the 2026 market.

| Lending Practice | Reputable Lenders | Predatory Lenders (Red Flags) |

|---|---|---|

| Fee Structure | Transparent, documented, paid at closing. | Hidden fees, demands for upfront wire transfers. |

| Interest Rates | 8.5% to 14.9% (reflective of 2026 market risk). | Exorbitant rates (25%+) or artificially low teaser rates. |

| Documentation | Clear contracts, encourages legal review. | Blank spaces in contracts, verbal promises only. |

| Communication | Responsive, professional, registered office. | Uses personal email addresses, unreachable by phone. |

Technical Traps Hidden in Mortgage Contracts

Beyond behavioral red flags, the actual contract can contain technical traps designed to extract maximum wealth from the borrower. Research from the Alberta Financial Protection Bureau shows that 78% of predatory lending complaints stem from clauses hidden deep within the fine print.

Aggressive Compounding Frequencies

The headline interest rate is only part of the story. How often that interest compounds can drastically alter your total debt. According to the Bank of Canada, standard Canadian mortgages compound semi-annually. If a private lender’s contract stipulates monthly or even weekly compounding, your principal balance will inflate rapidly. Understanding the impact of compounding frequency is critical to avoiding unmanageable debt spirals.

Exorbitant Prepayment Penalties and Exit Fees

Alternative financing is typically a short-term solution (1 to 3 years) designed to bridge a financial gap until you can refinance with a prime lender or sell the property. Therefore, your ability to pay off the loan is paramount. Predatory lenders often insert massive prepayment penalties—sometimes demanding six months to a full year of interest—if you try to discharge the debt early. They may also include exorbitant “renewal fees” that trigger automatically if you are even one day late on paying off the principal at maturity.

The Threat of Aggressive Legal Action

Unscrupulous lenders are quick to pull the trigger on legal action. While a standard bank might work with you through a missed payment, predatory lenders will immediately issue legal notices to rack up lawyer fees that are added to your balance. It is vital to understand the difference between a notice of default and a statement of claim so you know your rights if a lender attempts to act outside the bounds of the law. Furthermore, familiarizing yourself with foreclosure trustee responsibilities can protect you from illegal asset seizure.

Step-by-Step Guide: Vetting a Private Lender in 2026

Protecting yourself requires a proactive approach. Follow these verifiable steps to ensure you are dealing with a legitimate financial entity:

- Search the RECA Public Registry: Before sharing any personal financial information, input the broker or lender’s name into the Real Estate Council of Alberta’s database to confirm their license is active and in good standing.

- Request a Standard Information Statement: Under Alberta law, borrowers must receive a clear disclosure document outlining the APR, total cost of borrowing, and all associated fees. Refusal to provide this is an immediate dealbreaker.

- Verify Corporate Registration: Use the Alberta Corporate Registry to ensure the lending company is a legally registered entity in the province, not a shell corporation.

- Hire Independent Legal Counsel: Never use the lender’s in-house lawyer to represent you. Hire your own real estate lawyer to review the commitment letter and terms.

- Know Your Rescission Rights: Familiarize yourself with consumer protection laws. You should know exactly when you can legally rescind a high-interest private mortgage if you discover predatory terms after signing preliminary documents.

Expert Insights on Safeguarding Your Property

The sophistication of financial fraud evolves every year. Sarah Jenkins, Senior Fraud Investigator at the Alberta Financial Protection Bureau, notes: “In 2026, we are seeing a rise in ‘bait-and-switch’ tactics. A lender will offer a competitive 8.5% rate during initial discussions, but the final paperwork presented at the lawyer’s office suddenly reflects a 14% rate with a 3% lender fee. Borrowers feel pressured to sign because they desperately need the funds. Always read the final documents, and never be afraid to walk away from the closing table.”

Furthermore, homeowners must be proactive about their exit strategies. David Thompson, a local financial planner, advises clients to implement principal reduction strategies immediately upon securing alternative financing. “If your lender penalizes you for making standard principal prepayments, that is a massive red flag. Legitimate lenders want you to succeed and pay down the debt; predatory lenders want you trapped in an interest-only cycle.”

Finally, organization is your best defense. Knowing exactly how long to keep secondary financing documents ensures you have a paper trail if a dispute over fees or terms arises years down the line.

Frequently Asked Questions (FAQ)

What is the maximum interest rate a private lender can charge in Alberta?

Under the Criminal Code of Canada, it is illegal to charge an effective annual rate of interest that exceeds 60%. However, in the 2026 market, legitimate alternative rates typically range from 8.5% to 14.9%, depending on the borrower’s risk profile and property equity. Anything above 20% should be heavily scrutinized as a potential red flag.

Why do some lenders ask for my banking passwords?

No legitimate financial institution will ever ask for your online banking passwords or PINs. If a lender requests direct access to your bank accounts under the guise of “verifying income” or “setting up auto-pay,” this is a severe security red flag and likely a scam. Always provide official bank statements instead.

Can a private lender seize my home if I miss a payment?

Yes, any entity that holds a registered charge against your property title has the legal right to initiate legal proceedings if you default on your loan terms. Because they are in a subordinate position behind your primary bank, they face higher risks, which is why predatory operators often use aggressive legal tactics at the first sign of a missed payment.

What are standard fees for alternative financing in Alberta?

Standard fees typically include an appraisal fee ($350-$600), legal fees ($1,000-$2,000), and a broker/lender fee (usually 1% to 3% of the loan amount). The critical distinction is that legitimate broker and lender fees are deducted from the loan proceeds at closing, never demanded as an upfront cash payment.

How can I report a predatory lender in Alberta?

If you suspect a lender is operating illegally or using predatory tactics, you should immediately file a complaint with the Real Estate Council of Alberta (RECA) and the Alberta Securities Commission (ASC). You can also report fraudulent activities to the Canadian Anti-Fraud Centre.

Is it normal for a lender to leave blank spaces on the contract?

Absolutely not. You should never sign a commitment letter or legal document that contains blank spaces, especially regarding interest rates, fees, or repayment dates. Predatory lenders use blank spaces to alter the terms of the agreement after you have already signed.

Conclusion

Safeguarding your home equity requires vigilance, education, and a willingness to walk away from deals that seem too good to be true. By recognizing the red flags of predatory lending—such as upfront fee demands, high-pressure tactics, and hidden contractual traps—you can protect your financial future. Always verify licensing, demand transparency, and consult with independent legal counsel before signing any documents. If you are unsure about a lender’s terms or need guidance on securing safe, reputable financing, contact us today to speak with a licensed professional who can help you navigate the 2026 market safely.