When facing the terrifying prospect of property seizure, homeowners immediately search for fast, definitive answers. If you are frantically researching foreclosure trustee responsibilities Alberta regulations, the definitive answer is this: traditional “foreclosure trustees”—third-party companies hired by banks to quickly auction off homes without court approval—do not exist in Alberta. Instead, Alberta operates under a strict judicial foreclosure system overseen entirely by the Court of King’s Bench. However, the term “trustee” remains highly relevant in Canada, as a Licensed Insolvency Trustee (LIT) plays a critical role in managing the overwhelming unsecured debt that often accompanies a mortgage default, even though they do not directly sell your home for the bank.

Key Takeaways for Alberta Homeowners

- No Non-Judicial Trustees: Alberta lenders cannot bypass the courts to seize your property using a third-party trustee.

- Strict Judicial Oversight: Every step of property seizure in Alberta is controlled by a judge or Master in Chambers.

- The Real Trustee Role: In Canada, a “trustee” refers to a Licensed Insolvency Trustee (LIT), who handles consumer proposals and bankruptcies, not direct property auctions.

- The Stay of Proceedings Limit: Filing with an LIT stops unsecured creditors but does not permanently halt a secured mortgage foreclosure.

- Equity is Your Shield: Proactive equity management, such as securing alternative financing, is the most effective way to bypass the courts and save your home.

The Myth vs. Reality of Foreclosure Trustees in Alberta

Much of the financial advice populating search engines originates in the United States, where property laws vary wildly by jurisdiction. In many US states, lenders utilize a “Deed of Trust” rather than a traditional mortgage. Under this non-judicial system, a neutral third party holds the legal title to the property. If the homeowner defaults, the lender simply notifies this third party to initiate a foreclosure.

In a non-judicial system, the trustee’s primary job is to send a notice, advertise the property, and sell it at a public auction—often within a matter of 30 to 90 days. The court system is entirely bypassed, making the process incredibly fast and cheap for the bank. Because this system is illegal in our province, searching for foreclosure trustee responsibilities Alberta guidelines will yield results that simply do not apply to your situation.

Alberta property rights are heavily protected under the provincial Law of Property Act, which mandates a completely different, highly regulated approach. Lenders cannot bypass the courts, and they certainly cannot change your locks after a single missed payment.

Alberta’s Strict Judicial Foreclosure Process Explained

In Alberta, a mortgage is a registered charge against your land title, not a transfer of the title to a third party. If you stop making payments, the bank must formally sue you to recover their funds. This is known as a judicial foreclosure. The lender must file a Statement of Claim at the Court of King’s Bench, and from that moment forward, a judge or Master in Chambers oversees the entire timeline.

According to 2026 data from the Canadian Bankers Association, the mortgage arrears rate in Alberta fluctuates around 0.48%. While this percentage seems low, it means thousands of homeowners face this intimidating legal process annually due to economic shifts and rising living costs.

As David Smith, a senior Calgary real estate litigator, explains: “The biggest mistake homeowners make is assuming the bank holds all the power. The judicial process demands strict proof from the lender and offers multiple defense windows for the homeowner. Understanding the difference between a notice of default and a statement of claim is your first line of defense.”

Step-by-Step: The 2026 Alberta Foreclosure Timeline

Since we have established that a third party won’t be selling your home, it is crucial to understand how the actual legal process unfolds. The responsibility for driving this process lies with the lender’s lawyer, while the responsibility for protecting your equity lies with you.

- The Demand Letter: After 2 to 3 missed payments, the lender’s lawyer sends a formal demand for payment, giving you a short window to catch up on arrears.

- Statement of Claim: The lender files a formal lawsuit. You have exactly 20 days to file a Statement of Defense or a Demand for Notice. Understanding the transition from a notice of default to a formal lawsuit is critical at this stage.

- The Redemption Period: A judge grants a specific timeframe, usually six months, allowing you to pay the arrears, refinance, or sell the property. Accurately navigating your redemption period timeframe is vital to maximizing your opportunity to save the home.

- Order for Sale: If you cannot pay the arrears before the redemption period expires, the judge orders the property listed with a court-approved realtor.

- Order Absolute: If the property does not sell on the open market, the court grants a final order, transferring the title directly to the bank. You can review the complete final order eviction timeline to understand the absolute end of the process.

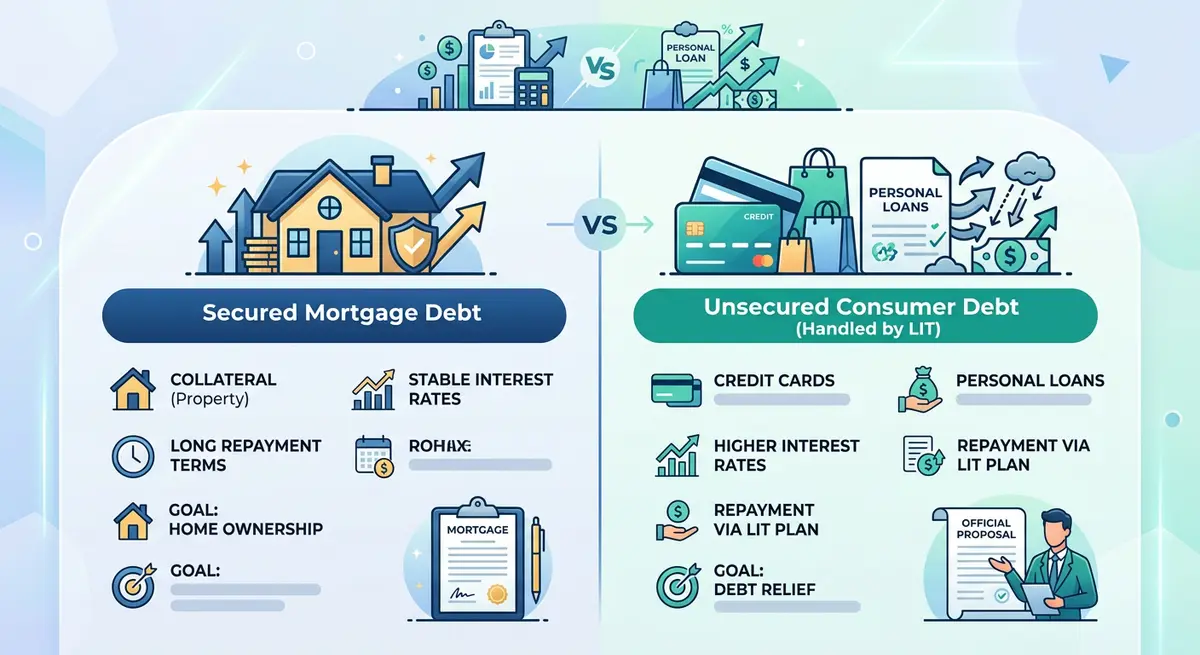

What is a Licensed Insolvency Trustee (LIT)?

While you will not find a professional auctioning off your house for the bank, you may need a different kind of trustee to save yourself from financial ruin. In Canada, a Licensed Insolvency Trustee (LIT) is a professional authorized by the federal government to administer bankruptcies and consumer proposals. If you are facing property seizure in 2026, it is rarely just the mortgage causing the problem. Usually, homeowners are drowning in credit card debt, car loans, and tax arrears.

This is where the true foreclosure trustee responsibilities Alberta residents search for come into play, albeit in a different context than expected.

Core Responsibilities of an LIT

If you hire an LIT, their duties are strictly regulated by the Office of the Superintendent of Bankruptcy (OSB). An LIT’s primary responsibilities include:

- Financial Assessment: Reviewing your entire financial situation to determine if you are officially insolvent.

- Filing Legal Paperwork: Submitting the documents for a Consumer Proposal or Bankruptcy to the federal government.

- Notifying Creditors: Informing all your unsecured creditors that legal action and collection calls must stop immediately.

- Administering the Estate: Managing the monthly payments you make in a proposal, or managing your non-exempt assets in a bankruptcy.

The “Stay of Proceedings” Limitation

It is vital to understand the limits of federal insolvency laws when dealing with a provincial property lawsuit. A mortgage is a “secured debt,” meaning the house acts as collateral. Credit cards and personal loans are “unsecured debt.” An LIT deals primarily with unsecured debt.

When an LIT files a consumer proposal for you, it triggers an automatic “Stay of Proceedings.” This legal shield immediately stops wage garnishment and lawsuits from unsecured creditors. However, this stay does not permanently stop a secured creditor like your mortgage lender. While the bank might pause their lawsuit briefly to review your bankruptcy filing, they will eventually ask the Court of King’s Bench to lift the stay so they can proceed with taking the house. Therefore, relying solely on an LIT will not save your home if you cannot resume your mortgage payments.

Comparison: Non-Judicial vs. Judicial vs. LIT

To clear up the confusion surrounding foreclosure trustee responsibilities Alberta laws, review this comparison table detailing the different roles and systems:

| Feature | US Non-Judicial Trustee | Alberta Judicial Process | Licensed Insolvency Trustee (LIT) |

|---|---|---|---|

| Primary Role | Sells property for the lender | Court oversees property seizure | Manages unsecured consumer debt |

| Court Involvement | None (Bypasses courts) | High (Court of King’s Bench) | Federal (Superintendent of Bankruptcy) |

| Speed of Process | Very Fast (30-90 days) | Slow (6-12 months) | Variable (Up to 5 years for proposals) |

| Handles Mortgages? | Yes (Directly auctions home) | Yes (Judge orders the sale) | No (Deals with credit cards/taxes) |

Managing the Shortfall: When an LIT Actually Helps

There is one specific scenario where the foreclosure trustee responsibilities Alberta residents search for actually intersect directly with property loss. This occurs after the legal process is complete, specifically if you had a high-ratio, insured mortgage backed by the Canada Mortgage and Housing Corporation (CMHC).

Deficiency Judgments and CMHC

If the bank takes your house and sells it for less than what you owe, you are left with a massive unsecured debt known as a shortfall. The court will issue a Deficiency Judgment against you. CMHC will then aggressively pursue you, freezing bank accounts and garnishing wages to collect this remaining balance. Understanding your deficiency judgment liability is vital to preparing for this financial blow.

At this stage, the debt is no longer secured by the house. This is when a Licensed Insolvency Trustee becomes your most valuable asset. The LIT’s responsibility is to roll that massive shortfall into a consumer proposal or bankruptcy. Filing with the LIT instantly stops the CMHC wage garnishment and allows you to settle the terrifying leftover debt for a fraction of the cost, giving you a fresh financial start.

3 Strategies to Stop Foreclosure Without a Trustee

Both the court process and the insolvency process have severe, long-lasting consequences. Losing your home destroys your credit, and declaring bankruptcy subjects your finances to federal oversight for years. Fortunately, research from the University of Calgary’s School of Public Policy indicates that proactive equity management can save over 60% of at-risk homes. If you have built up equity in your property, you can bypass both the courts and the LIT.

1. Leveraging Home Equity with a Second Mortgage

When traditional A-lenders refuse to help because of your missed payments, private equity lenders focus on the value of the asset itself. A private second mortgage provides the lump sum of cash necessary to pay out the aggressive lender’s arrears and legal fees. This satisfies the lawsuit completely. You retain ownership of your home and protect your credit from catastrophic damage. For many homeowners, comparing a second mortgage versus a cash out refinance is the first step to recovery.

2. Filing a Demand for Notice

If you cannot secure financing immediately, filing a Demand for Notice ensures the bank’s lawyer cannot proceed with court applications without notifying you first. By properly responding to the formal statement of claim, you buy critical time to negotiate or list the property yourself before the bank places a restrictive encumbrance on your title.

3. Negotiating a Forbearance Agreement

In some cases, if your financial hardship was temporary (such as a brief job loss or medical emergency), you can negotiate directly with the lender’s lawyer to capitalize the arrears. This means adding the missed payments to the back of the mortgage loan, though banks in 2026 are increasingly strict about approving these agreements without proof of restored income.

Expert Insights on Navigating Property Debt in 2026

Understanding the nuances of foreclosure trustee responsibilities Alberta regulations is just the first step. Taking decisive action is what ultimately saves your home. The intersection of property law and insolvency requires a clear, strategic approach.

As Sarah Jenkins, a Calgary-based Licensed Insolvency Trustee, explains: “Homeowners often confuse our role with that of an American foreclosure trustee. We don’t take your house; we try to restructure your unsecured debt so you can afford to keep your house. However, if the mortgage itself is too far gone, alternative private lending is often the only bridge back to financial stability.”

By securing alternative financing to pay out the arrears, you can halt the legal machine entirely, retain your property, and secure your financial future without relying on the courts or insolvency proceedings. If you decide to sell the property yourself to pay off the debt, you may need assistance discharging a Lis Pendens from your title to ensure the transaction closes smoothly.

Frequently Asked Questions (FAQ)

Can the bank just change the locks on my house in Alberta?

No. Because Alberta uses a strict judicial process, the bank cannot simply lock you out. They must obtain an Order for Possession from a judge first, and you must be served with official notice giving you a specific date to vacate.

Does a Consumer Proposal wipe out my mortgage?

No. A consumer proposal administered by an LIT only deals with unsecured debt like credit cards, payday loans, and taxes. Your mortgage is secured by the property, so you must continue paying it to keep the home.

What is the Office of the Public Guardian and Trustee?

The Office of the Public Guardian and Trustee (OPGT) is a provincial government office. They only become involved in property disputes if the homeowner is a dependent adult lacking mental capacity, or if the homeowner has died and no one is managing the estate.

Can I sell my house while the bank is suing me?

Yes. Until the judge grants the Final Order (Order Absolute) transferring the title to the bank, you still own the home. However, you must ensure the sale price covers the entire mortgage balance, legal fees, and any registered liens.

How long does the Alberta judicial foreclosure process take?

It is significantly slower than the US non-judicial trustee system. From the first missed payment to the final eviction, the process in Alberta usually takes anywhere from 6 to 12 months, depending on your equity and defense strategy.

Will an Insolvency Trustee help me if I have a CMHC shortfall?

Yes. If the bank sells your home for less than you owe, the remaining deficiency judgment becomes an unsecured debt. An LIT can include this massive shortfall in a consumer proposal or bankruptcy, protecting your wages from CMHC garnishment.

Conclusion

Navigating the complexities of property seizure requires a clear understanding of the law. The reality of foreclosure trustee responsibilities Alberta residents face is that the courts, not third-party trustees, dictate the loss of a home. While Licensed Insolvency Trustees are invaluable for managing unsecured debt and CMHC shortfalls, they cannot magically erase a secured mortgage default. The most effective way to protect your family and your financial future is to leverage your home’s equity before the court grants a final order. If you are facing legal action from your lender and need immediate alternative financing to stop the process, do not wait until it is too late. Get in touch with our team today to explore your equity options and keep your home.