Yes, the bank can absolutely take your paycheque after a foreclosure in Alberta if you hold an insured, high-ratio mortgage. When a property sells for less than the outstanding loan balance, lenders secure a deficiency judgment from the Court of King’s Bench, allowing them to issue a Garnishee Summons directly to your employer. Facing income seizure after losing a home means Calgary residents often lose up to 50% of their net income, making immediate legal and financial intervention critical in 2026.

Key Takeaways

- The Recourse Reality: If your mortgage was insured by CMHC, Sagen, or Canada Guaranty, the insurer has the legal right to sue you for the financial shortfall after a foreclosure.

- The Base Exemption: Under 2026 Alberta law, the first $800 of your net monthly income is strictly protected from wage garnishment.

- Dependent Allowances: For every dependent you actively support, your minimum protected income exemption increases by an additional $200 per month.

- The 50% Rule: Any net income you earn between your minimum exemption and $2,400 per month is subject to a 50% seizure rate by the courts.

- Bank Account Freezes: Unlike employment garnishment, a Garnishee Summons served to your bank can freeze and empty 100% of the available funds in your checking or savings accounts.

- Stopping the Seizure: Filing a Consumer Proposal or declaring Bankruptcy triggers an immediate “Stay of Proceedings,” legally forcing all wage garnishments to stop instantly.

Understanding the Recourse Mortgage Trap in Alberta

Losing your home to foreclosure is a devastating financial event that leaves deep emotional scars. For many Calgarians, the assumption is that once the bank takes the keys, the nightmare is officially over. You might believe that handing over the property settles your debt entirely, allowing you to walk away and start fresh. Unfortunately, if you hold a specific type of mortgage, the financial bleeding does not stop at the property line. When a property is sold by the court for less than the total amount you owe, a “shortfall” or “deficiency” is created. If your loan allows for it, the lender or mortgage insurer will sue you personally for this remaining balance. Once they secure a deficiency judgment, they have the legal authority to seize your assets.

To comprehend how a lender can seize your paycheque after taking your house, you must understand the two distinct types of mortgages in Alberta. The province has specific property laws that protect some homeowners while leaving others exposed to severe financial liability. The determining factor is the size of your original down payment and whether mortgage default insurance was required. If you purchased your home with a down payment of 20% or more, you hold a conventional, non-recourse mortgage. Under the provincial statutes, non-recourse means the lender’s only remedy for default is to take the property itself. If the court sells your house for $400,000 but you owe $500,000, the bank simply absorbs the $100,000 loss. They cannot sue you for the remaining balance. You can review these specific protections directly through the Alberta Law of Property Act.

However, if your down payment was less than 20%, your mortgage is classified as high-ratio and required default insurance from providers like CMHC, Sagen, or Canada Guaranty. These are “recourse” mortgages. If the bank loses money on the foreclosure sale, they file an insurance claim, and the insurer pays the bank the difference. The insurer then assumes the debt and has the legal right to pursue you for the full shortfall. Research from the Canada Mortgage and Housing Corporation (CMHC) shows that their mandate requires the aggressive recovery of these taxpayer funds.

According to Sarah Jenkins, Lead Foreclosure Counsel at Alberta Property Law Group: “Homeowners falsely believe handing over the keys ends the nightmare. If CMHC insured the loan, the legal pursuit has only just begun, and wage seizure is their primary weapon.”

The 4-Step Legal Process: How a Shortfall Becomes a Garnishee Summons

The path from a missed mortgage payment to a seized paycheque involves several escalating legal steps. The process begins during the final stages of the foreclosure lawsuit, specifically when the court issues the Order for Sale or Order Absolute. Understanding the calculating a deficiency judgment process is the first step in predicting your financial exposure. Here is the exact 4-step legal process creditors use to garnish your wages in 2026:

- The Deficiency Calculation: If the sale proceeds are less than your total debt (including principal, interest, and thousands in legal fees), the court calculates the exact shortfall amount.

- The Deficiency Judgment: The lender or insurer asks the judge for a formal judgment for that specific amount, converting the mortgage shortfall into an unsecured personal liability.

- The Writ of Enforcement: To collect this money, the creditor files a Writ of Enforcement with the Court of King’s Bench. This document is registered with Service Alberta’s Personal Property Registry, formally declaring you a judgment debtor.

- The Garnishee Summons: With the Writ active, the creditor applies for a Garnishee Summons. The creditor’s lawyer serves this court order directly to your company’s payroll department, legally forcing them to deduct funds from your net pay.

By law, your employer has no choice but to comply. They must calculate the legally required deductions and remit those funds directly to the court, bypassing your bank account entirely. If you recently received a legal notice, understanding the difference between a notice of default versus a formal claim is vital to understanding your timeline and legal standing.

2026 Alberta Wage Garnishment Exemptions: What You Actually Keep

When a Garnishee Summons lands on your employer’s desk, you do not lose your entire paycheque. The provincial government recognizes that debtors must retain a baseline of income to survive. The Alberta Civil Enforcement Act dictates specific exemption formulas that employers must strictly follow. These calculations are always based on your net income, meaning your pay after mandatory deductions like taxes, CPP, and EI are removed.

The primary protection is the base exemption. In 2026, the first $800 of your net monthly income is 100% exempt from seizure. Furthermore, the province provides allowances for families. For every dependent you actively support, your base exemption increases by $200. For example, a single parent with two children has a fully protected base exemption of $1,200 per month. For any net income earned above your protected base, a tiered system applies. Any income between your base exemption and $2,400 per month is subject to a 50% garnishment rate. Half goes to you, and half goes to the court.

However, there is a hard cap on protections. Any net income you earn exceeding $2,400 per month is 100% garnished. Every dollar above that threshold is seized until the entire deficiency judgment is paid in full. If you are currently responding to a statement of claim, you must prepare for these strict financial limitations.

As Dr. Emily Carter, Economic Researcher at the University of Calgary, notes: “The 2026 cost of living makes the provincial $800 base exemption mathematically insufficient for basic survival in major urban centers, pushing garnished individuals into secondary debt cycles.”

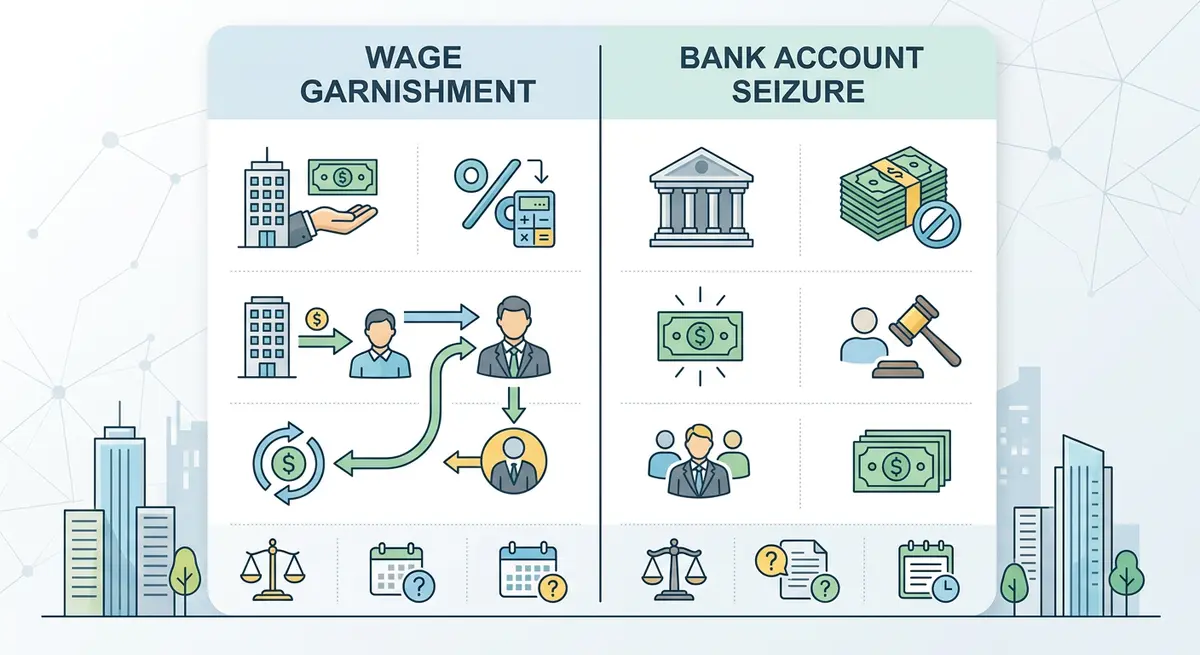

Bank Account Freezes vs. Employment Seizures

While employment garnishment leaves you with a survival income, the rules for bank account seizures are entirely different and far more dangerous. Creditors hold the right to serve a Garnishee Summons directly to your financial institution instead of your employer. When a bank receives this order, the results are immediate and severe. Unlike paycheques, there are no base exemptions for standard bank accounts.

If CMHC or another judgment creditor serves your bank, the institution is legally obligated to freeze the account immediately. They must withdraw all available funds up to the total amount of the judgment and remit them to the court. This means your rent money, grocery budget, and emergency savings can vanish overnight. To understand your banking rights, the Financial Consumer Agency of Canada offers extensive resources on account freezes.

| Feature | Wage Garnishment (Employer) | Bank Account Seizure (Financial Institution) |

|---|---|---|

| Base Exemption | $800 minimum protected (plus $200/dependent) | $0 protected (100% seizure of available funds) |

| Seizure Rate | 50% between base and $2,400; 100% over $2,400 | 100% of all funds up to the judgment amount |

| Duration of Order | Valid for 1 year (must be renewed annually) | Valid for a strict 60-day window per summons |

| Future Deposits | Applies to all future paycheques while active | Captures any new deposits made within the 60 days |

A Garnishee Summons on a bank account is valid for 60 days. Any new deposits made into that account during the 60-day window, including e-transfers from family or cash deposits, will also be seized automatically.

The Psychological and Financial Impact of Income Seizure

The psychological toll of having your wages seized is heavy. Many Calgarians feel a profound sense of embarrassment when their employer receives a court order regarding their personal debts. You may worry that your boss or HR manager will view you as financially irresponsible, leading to missed promotions or termination. It is crucial to know that under Alberta employment standards, it is strictly illegal for an employer to fire you, demote you, or discipline you simply because your wages are being garnished.

Despite this legal protection, the financial reality remains grim. Living on a heavily reduced income makes it nearly impossible to cover basic living expenses in a major city like Calgary. You will likely fall behind on other obligations, triggering a cascade of secondary financial emergencies. Your credit score, already heavily damaged by the foreclosure itself, will suffer further as the judgment remains a permanent fixture on your public record for up to 10 years. This cycle of debt can feel inescapable. If you are trying to rebuild your financial profile, learning how to draft a perfect letter of explanation for future lenders is a necessary step in your recovery.

Actionable Strategies to Stop Wage Seizure in 2026

If you have received notice of a deficiency judgment or an active garnishment, ignoring the problem will only guarantee continued financial loss. You have legal rights and options to stop the bleeding. The first option is direct negotiation. You can contact the creditor’s lawyer or CMHC collections directly to propose a voluntary payment plan or a lump-sum settlement. If they accept, they will withdraw the Garnishee Summons.

For most people facing wage seizure, the most effective strategy is utilizing federal insolvency laws. Filing a Consumer Proposal or declaring Bankruptcy through a Licensed Insolvency Trustee triggers an immediate, nationwide “Stay of Proceedings.” This is a powerful legal injunction that forces all creditors to stop collection actions instantly. The moment your proposal or bankruptcy is filed, the trustee notifies the court and your employer, and the wage garnishment is legally terminated. The Office of the Superintendent of Bankruptcy provides extensive information on how these federal programs protect Canadian debtors.

John Smith, Senior Insolvency Trustee at Calgary Financial Rescue, explains: “A Garnishee Summons does not just take your money; it paralyzes your ability to survive in a high-inflation economy. A Consumer Proposal immediately halts the garnishment and often reduces the total deficiency debt by up to 80%.”

A Consumer Proposal allows you to consolidate the deficiency judgment and your other unsecured debts into a single, affordable monthly payment. You retain your assets and avoid bankruptcy while permanently solving the garnishment crisis. Understanding the final order of foreclosure timeline ensures you do not miss your window of opportunity to act before judgments are filed.

Using Home Equity to Prevent Deficiency Judgments

The absolute best defense against a deficiency judgment and subsequent wage seizure is to prevent the foreclosure from finalizing in the first place. Once the Order Absolute is granted, your options shrink dramatically. If you are still in the redemption period and the bank is threatening to take the property, you must find a way to pay the arrears and legal fees to cure the default. Knowing how to calculate your exact redemption period is critical for your survival timeline.

Traditional banks will instantly reject your application if you are in active foreclosure. To survive, you must secure alternative capital. We specialize in providing a private second mortgage that leverages the remaining equity in your home. By securing this funding, you can pay out the aggressive lender, satisfy their demands, and stop the lawsuit entirely. This strategy allows you to keep your property, protect your equity from fire-sale court valuations, and eliminate the risk of a future CMHC shortfall lawsuit.

David Chen, Director of Underwriting at The Second Mortgage Store, emphasizes: “Stopping the foreclosure during the redemption period is the only guaranteed way to prevent a deficiency judgment and protect your future income from aggressive insurers.”

If you are struggling to find a mortgage solution to halt the legal timeline, acting quickly is your only leverage. We focus on the value of your asset, not your bruised credit score, to deliver the financial rescue you need.

Frequently Asked Questions (FAQ)

Can the CRA garnish my wages without a court order in Alberta?

Yes. Unlike private lenders or mortgage insurers who must sue you and get a deficiency judgment, the Canada Revenue Agency (CRA) has special federal powers. They can issue a Requirement to Pay directly to your employer without ever going to court.

How long does a deficiency judgment stay on my credit report?

A deficiency judgment resulting from a foreclosure shortfall will remain on your public credit record for up to 10 years in Alberta. This severely impacts your ability to secure traditional financing, rent apartments, or obtain certain types of employment.

Can my employer fire me because my wages are being garnished?

No. Under the Alberta Employment Standards Code, it is strictly illegal for an employer to terminate, demote, or discipline an employee solely because they have received a Garnishee Summons for their wages.

Does a Consumer Proposal stop a bank account freeze?

Yes. Filing a Consumer Proposal triggers a Stay of Proceedings, which legally halts all collection actions, including both wage garnishments and bank account freezes, immediately upon filing.

Are joint bank accounts safe from a Garnishee Summons?

No. If your name is on a joint bank account, creditors can freeze the entire account and seize the funds up to the judgment amount, regardless of whether the co-owner of the account owes the debt.

Can I negotiate a lower payment with CMHC after a judgment?

Yes, but it is entirely at their discretion. You or your legal representative can contact the collection agency or law firm representing CMHC to negotiate a voluntary payment plan or a lump-sum settlement to avoid formal garnishment.

Conclusion

Facing wage garnishment after a foreclosure in Calgary is a daunting reality for homeowners with insured, high-ratio mortgages. The legal mechanisms used by lenders and insurers are aggressive, and the financial toll of losing up to 50% of your net income can push families to the brink. However, you are not powerless. By understanding Alberta’s exemption laws, utilizing federal insolvency protections like a Consumer Proposal, or leveraging your home’s equity before the foreclosure finalizes, you can protect your paycheque and secure your financial future. If you are terrified of facing a garnishment and need emergency funding to stop the banks in their tracks, do not wait until the judge signs your financial future away. Get in touch with our team today to discuss your mortgage options and stop the collection nightmare.