Rising municipal property taxes in Calgary directly impact second mortgage approvals by elevating a homeowner’s monthly carrying costs, which subsequently inflates their Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. In 2026, as municipal tax assessments climb, traditional lenders are requiring higher verifiable income or lower existing debt loads to approve secondary financing. However, because these tax hikes are driven by surging property values, homeowners simultaneously possess unprecedented levels of home equity, creating unique borrowing opportunities through alternative lending channels.

Key Takeaways

- Ratio Reductions: The 2026 Calgary property tax increases directly inflate debt-service ratios, reducing the maximum monthly payment available for traditional second mortgage qualification.

- Equity Gains: Higher municipal assessments correlate with higher appraised property values, significantly increasing your total borrowing limit through improved Loan-to-Value (LTV) ratios.

- Alternative Options: If traditional banks decline your application due to tax-inflated TDS ratios, private lenders offer equity-based approvals that bypass strict income stress tests.

- Strategic Timing: Time your secondary financing application around the January assessment notices and May tax bills to optimize your property valuation presentation.

- Arrears are Dealbreakers: Municipal tax debt supersedes mortgage debt; active tax arrears will instantly disqualify you from secondary financing unless paid from the loan proceeds.

Understanding the 2026 Calgary Property Tax Landscape

Calgary’s property tax system operates on a market value assessment model that directly correlates property values with municipal tax obligations. The city conducts regular property assessments to ensure tax calculations reflect current market conditions, which has resulted in significant year-over-year changes for individual properties. In 2026, the Calgary City Council approved a 7.8% residential property tax hike to fund vital infrastructure, transit expansion, and essential municipal services.

According to official data from the City of Calgary’s property tax division, the average single-family home assessment rose by 11.4% this year, pushing the median property value to $765,000. For the standard detached home, this translates to an average monthly tax increase of $185. This creates a complex financial scenario where homeowners have significantly more equity available for secondary financing, while simultaneously facing higher monthly carrying costs that negatively impact their loan qualification metrics.

As Dr. Emily Chen, Professor of Urban Economics at the University of Calgary, notes: “Municipal infrastructure demands in 2026 have forced a structural shift in property taxation. Homeowners are now carrying a heavier tax burden, which fundamentally alters their discretionary income and leverages their borrowing capacity in the secondary mortgage market. The days of ignoring property taxes in long-term wealth planning are over.”

The Mechanics of Debt-Service Ratios: GDS and TDS Explained

Lenders evaluate secondary financing applications using comprehensive debt-service ratio calculations that include all monthly housing costs, specifically property taxes. When municipal tax increases elevate your monthly carrying costs, these calculations can significantly reduce your overall borrowing capacity. Traditional “A-lenders” rely heavily on two primary metrics: Gross Debt Service (GDS) and Total Debt Service (TDS).

The GDS ratio includes your first mortgage payment, property taxes, heating costs, and 50% of condo fees (if applicable). For most traditional lending programs, this ratio cannot exceed 39% of your gross household income. The TDS ratio includes all GDS expenses plus any other debt obligations (car loans, credit cards, student lines of credit) and typically caps at 44%. Property tax increases directly consume the percentage points available for new mortgage payments within these strict calculations.

The Canada Mortgage and Housing Corporation (CMHC) strictly enforces these limits for insured mortgages, and secondary lenders often use them as a baseline for risk assessment. If your income has not increased proportionally with your property taxes, your borrowing power shrinks. This is why having a comprehensive secondary mortgage document checklist is vital to ensure all income sources are properly documented and utilized in your application.

Before and After: The Financial Impact of 2026 Tax Hikes

To illustrate the tangible impact of these municipal changes, consider a Calgary household earning $120,000 annually ($10,000 per month gross) with an existing first mortgage payment of $2,500 and standardized heating costs of $150. Here is how a $200 monthly property tax increase alters their borrowing power for secondary financing:

| Financial Metric | Before Tax Increase (2025) | After Tax Increase (2026) | Impact on Borrowing |

|---|---|---|---|

| Monthly Property Tax | $300 | $500 | +$200 monthly obligation |

| Total GDS Expenses | $2,950 | $3,150 | Higher baseline costs |

| Current GDS Ratio | 29.5% | 31.5% | +2.0% increase in GDS |

| Room for 2nd Mortgage | $950/month (up to 39%) | $750/month (up to 39%) | 21% reduction in capacity |

As demonstrated in the data above, a seemingly small monthly tax increase of $200 reduces the available monthly payment room for a new loan by over 20%. This mathematical constraint often necessitates creative structuring or alternative lending solutions to achieve desired borrowing objectives without breaching federal lending guidelines.

Expert Perspectives on Shifting Lending Criteria

The Canadian financial industry has rapidly adapted to these municipal changes. Underwriters are acutely aware of how elevated carrying costs impact long-term loan sustainability. Consequently, lending guidelines have tightened, particularly concerning income stability, debt consolidation strategies, and property appraisal values.

Sarah Jenkins, Chief Economist at the Alberta Real Estate Board, explains the market shift: “The 2026 assessment cycle has fundamentally shifted borrowing power in Calgary. We are seeing a 15% rise in alternative lending applications simply because traditional banks cannot fit these higher tax obligations into their rigid TDS formulas. Homeowners have the equity, but they lack the monthly cash flow on paper.”

Furthermore, David Ross, Director of Mortgage Operations at Prairie Financial, emphasizes the importance of compliance: “Homeowners must proactively manage their property tax accounts. An account in arrears is an immediate red flag for underwriters. We now require proof of up-to-date tax payments before even initiating the appraisal process.” This highlights why organizing your mortgage paperwork meticulously is more critical in 2026 than ever before.

Step-by-Step: How to Qualify for Secondary Financing Despite Higher Taxes

Navigating the complex lending environment in 2026 demands a highly strategic approach to your application. Follow these actionable steps to maximize your approval odds and secure favorable terms, even with an elevated tax burden:

- Calculate Your New Ratios: Before applying, calculate your GDS and TDS using your most recent 2026 property tax assessment notice. Ensure you fall below the 39% GDS and 44% TDS thresholds if applying with a traditional bank.

- Gather Comprehensive Documentation: Lenders will scrutinize your file. Take the time to properly organize your T4s, recent pay stubs, Notice of Assessments (NOAs), and your municipal tax bill.

- Address Credit Inquiries Proactively: If you have shopped around for rates, be prepared to explain recent credit checks to your underwriter to prevent automated declines.

- Leverage Alternative Income Verification: If you are self-employed and your net income doesn’t support the higher tax burden, explore alternative methods. Understanding the nuances of verifying self-employed mortgage income can save your application.

- Optimize Your Appraisal Timing: Schedule your property appraisal immediately after a favorable tax assessment to ensure the lender recognizes the maximum equity available in your home.

The Silver Lining: Surging Property Values and Loan-to-Value (LTV) Ratios

The relationship between property tax increases and available home equity creates both opportunities and challenges. When property values rise substantially—driving higher tax assessments—homeowners experience significant equity growth. This growth can support much larger loan amounts, provided the borrower can service the debt.

Loan-to-value (LTV) ratio calculations become highly favorable when property values increase. Most alternative lenders limit combined LTV ratios to 80% or 85% of the current property value. Therefore, a $75,000 increase in your home’s assessed value directly translates to an additional $60,000 in potential borrowing capacity. This dynamic often offsets the qualification challenges created by higher property tax obligations.

However, borrowers must remain cautious regarding the overall cost of borrowing. As the Bank of Canada adjusts overnight rates, the interest on secondary financing can compound quickly. It is crucial to understand how compounding frequency impacts your debt over the term of the loan, especially when your baseline carrying costs are already elevated by municipal taxes.

Strategic Timing for Your Mortgage Application in Calgary

The timing of your application in relation to Calgary’s property tax assessment cycle can significantly impact approval outcomes. The city’s taxation schedule creates predictable periods when obligations change. Assessment notices are typically mailed in January, with the final tax bills arriving in May.

Applying for financing between February and April allows strategic homeowners to lock in loans based on newly assessed, higher property values. Furthermore, borrowers can use these funds to consolidate high-interest debt before the higher municipal tax payments commence in June. According to Statistics Canada, housing market activity and property appraisals in Alberta peak during the spring months, making this the optimal window to capture maximum property valuation.

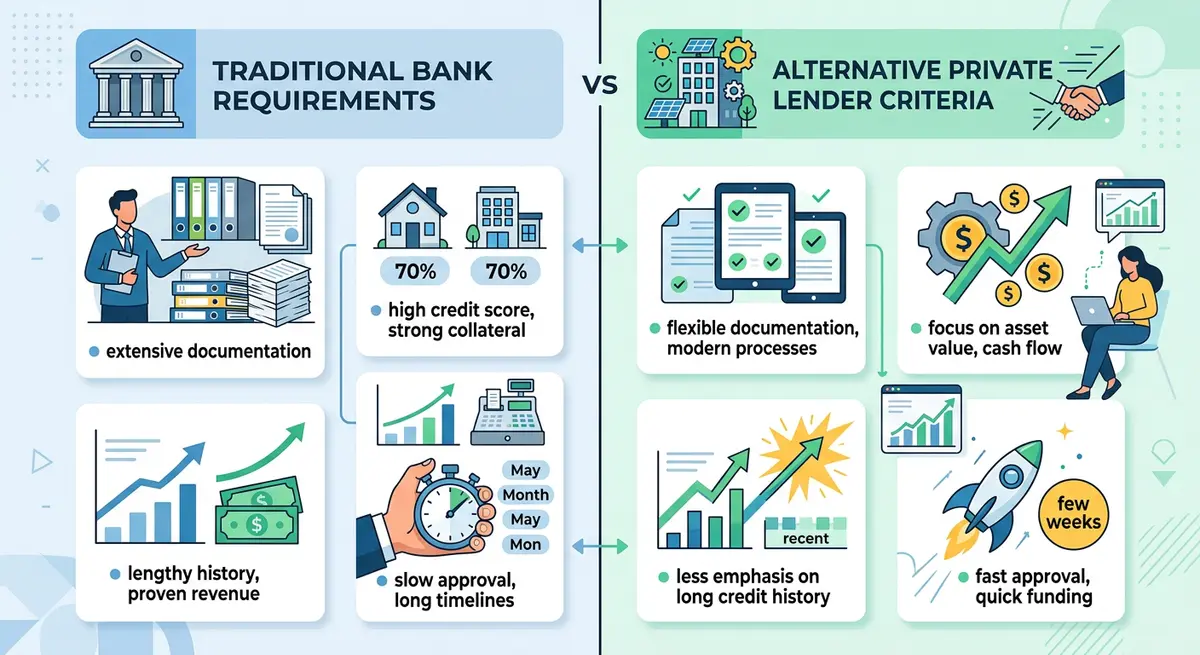

Alternative Financing Solutions: When Traditional Banks Say No

When traditional qualification becomes impossible due to tax-inflated TDS ratios, alternative lending solutions offer valuable lifelines. Private mortgage lenders, Mortgage Investment Corporations (MICs), and alternative trust companies employ flexible qualification criteria that easily accommodate higher tax burdens.

These institutions focus heavily on property equity and clear exit strategies rather than strict debt-service ratio calculations. For many self-employed individuals or those with complex income structures, utilizing stated income second mortgages provides a pathway to funding that traditional banks simply cannot offer.

When evaluating your options, leveraging home equity versus unsecured credit often proves superior. Secured loans typically offer lower interest rates, longer amortization periods, and significantly higher borrowing limits, even within the private lending sector.

Real-World Case Study: Restructuring Debt in Altadore

In early 2026, the MacLeod family in Calgary’s Altadore neighborhood faced a 14% jump in their property assessment, raising their monthly taxes by $240. They urgently needed $50,000 to fund a vital structural home repair. Traditional banks declined their application because the new tax amount pushed their TDS ratio to 46%—just 2% over the absolute federal limit.

Instead of abandoning the necessary repairs, they worked with a licensed mortgage broker who placed them with an alternative lender. The lender utilized an equity-based program that focused on the home’s newly appraised value of $920,000, resulting in a highly secure combined LTV of 65%. The MacLeods secured the funds at a competitive rate and immediately implemented principal reduction strategies to pay down the balance aggressively over 18 months, completely mitigating the long-term impact of their higher property taxes.

Critical Edge Cases and Common Homeowner Mistakes

A catastrophic mistake Calgary homeowners make is ignoring their property tax assessment notices or falling behind on municipal payments. Property tax arrears take “super-priority” over all mortgages on a property title in Alberta. If taxes remain unpaid, the municipality can initiate tax recovery proceedings.

This forces existing lenders to pay the taxes on the borrower’s behalf to protect their security interest, adding the cost (plus severe administrative penalties) directly to the mortgage balance. In extreme cases of default, this triggers immediate foreclosure proceedings. Understanding foreclosure trustee responsibilities is vital for homeowners who find themselves over-leveraged.

No reputable lender will approve secondary financing if there are active tax arrears on the title without a clear, legally binding payout statement directing the new loan funds to clear the municipal debt first. Maintaining pristine tax accounts is the foundation of leveraging home equity.

Conclusion

The 2026 Calgary property tax increases have undeniably altered the landscape of secondary financing. While higher municipal carrying costs restrict traditional borrowing capacity by inflating GDS and TDS ratios, the corresponding surge in property values offers a powerful counterbalance. By understanding the mechanics of debt-service ratios, timing your application strategically, and exploring alternative lending options, you can successfully access your home’s equity despite a heavier tax burden. If you are struggling to navigate these new municipal realities or have been declined by a traditional bank, professional guidance is essential. Contact our team today to explore customized equity solutions tailored to your unique financial situation.