When a homeowner in Calgary falls behind on mortgage payments, the lender initiates the judicial foreclosure process by filing specific legal documents, most notably the Statement of Claim. Receiving this document triggers a strict 20-day legal window for the homeowner to file a formal response at the Court of King’s Bench. Failing to answer these filings results in a default judgment, accelerating the loss of the property and stripping the homeowner of their right to negotiate redemption options or alternative resolutions.

Key Takeaways

- Judicial Oversight: Alberta operates under a judicial foreclosure system, meaning lenders cannot seize property without formal approval from the Court of King’s Bench.

- The 20-Day Rule: Homeowners have exactly 20 days from the date of service to respond to a Statement of Claim to prevent a default judgment.

- Order Nisi: This critical court order establishes the redemption period (typically six months) during which you can pay arrears to save your home.

- Do Not Evade Service: Avoiding process servers does not stop the lawsuit; it simply leads to substitutional service and increases your legal fees.

- Professional Help is Vital: Consulting with legal counsel or a specialized mortgage broker immediately upon receiving a Demand Letter can open doors to alternative financing or forbearance.

The Judicial Foreclosure Process in Alberta (2026 Context)

Unlike some jurisdictions in North America that allow lenders to execute power of sale or seize property directly, Alberta operates under a strict judicial foreclosure system. This framework dictates that every step of the foreclosure process must be meticulously documented and approved by the Court of King’s Bench of Alberta. Lenders cannot simply change the locks on your home; they must prove their case before a judge or a Master in Chambers.

This judicial oversight is fundamentally designed to protect consumers. It ensures that all financial calculations are accurate, that interest is applied legally, and that homeowners are granted a fair opportunity to respond to allegations. The process begins long before the court gets involved, typically starting with missed payments and internal bank collections. However, once the matter is escalated to the lender’s legal counsel, the formal generation of legal paperwork begins.

Understanding the difference between a notice of default and a formal claim is essential for gauging how much time you have left to act. In 2026, the average timeline from the first missed payment to a final foreclosure order in Calgary spans approximately 9 to 12 months, heavily dependent on court backlogs and the homeowner’s proactive responses.

Critical Foreclosure Legal Documents Explained

When reviewing foreclosure paperwork, Calgary residents must understand that each piece of paper serves a distinct procedural purpose. The hierarchy of these documents dictates your required actions and the severity of the legal threat.

1. The Demand Letter (Pre-Litigation)

Before formal litigation begins, the lender’s lawyer will send a Demand Letter. This is a pre-legal notice stating that your mortgage is in arrears and demanding full payment of the missed amounts, plus legal fees, by a specific date—usually within 10 to 15 days. While not a court document, it is the final warning before a lawsuit is filed.

According to the Canadian Bankers Association, nearly 40% of mortgage arrears are resolved at this demand stage before court intervention becomes necessary. Taking immediate action at this juncture is the most cost-effective way to halt the process.

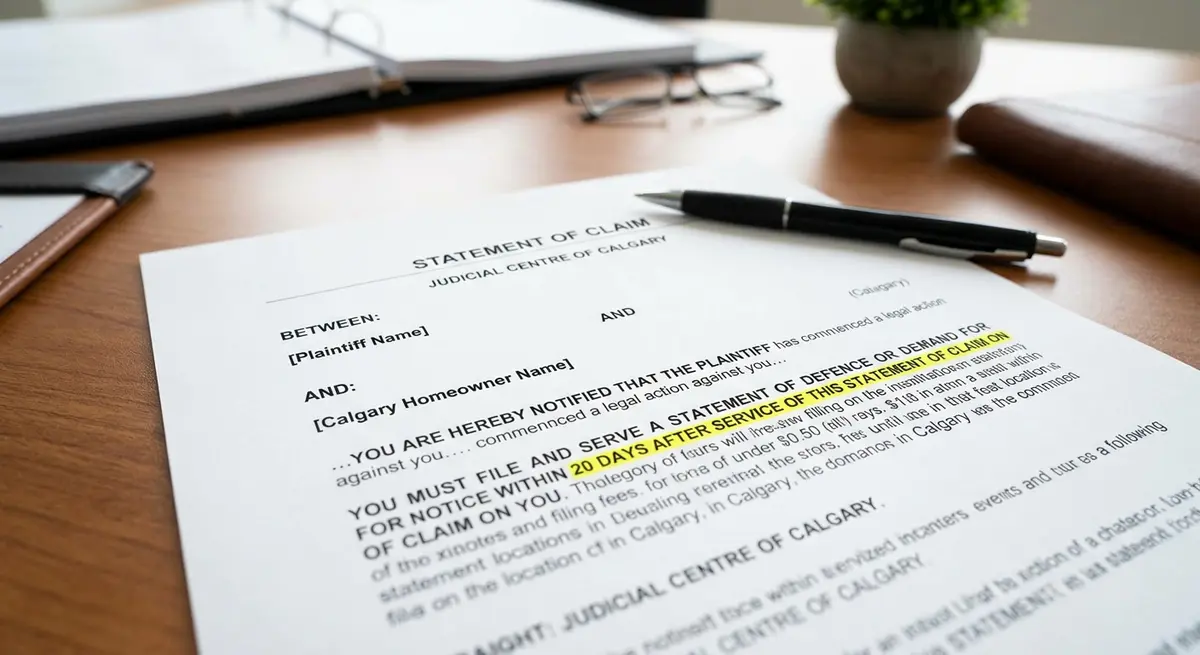

2. The Statement of Claim (The 20-Day Clock)

The most critical of all foreclosure legal documents processed by Calgary courts is the Statement of Claim. This document officially commences the lawsuit. It outlines the lender’s allegations, the exact amount owed (including principal, interest, and costs), and the “Prayer for Relief”—a section detailing exactly what the lender is asking the court to grant, such as possession of the property and a judgment for the debt.

Data from the Alberta Ministry of Justice indicates that in early 2026, over 72% of default judgments occurred simply because defendants failed to file a formal response. You have exactly 20 days from the date you are served to respond to this document.

3. Certificate of Lis Pendens

Often filed concurrently with the Statement of Claim, a Certificate of Lis Pendens (Latin for “suit pending”) is registered directly against your property’s title at the Alberta Land Titles Office. This document serves as a public warning to any potential buyers or secondary lenders that the property is subject to ongoing litigation.

If you manage to refinance or sell the property to pay off the debt, you will need to go through the legal process of removing a Lis Pendens from your title before the real estate transaction can successfully close.

4. Affidavits of Value and Default

To prove their case in court, the lender will file an Affidavit of Default, a sworn statement detailing your missed payments and the total debt. They will also file an Affidavit of Value, which includes an appraisal of your home’s current market worth.

Homeowners should scrutinize this appraisal carefully; lenders often use conservative valuations. If the property is valued lower than the mortgage balance, you could be facing a massive shortfall, making it vital to understand the rules around calculating potential deficiency judgments.

Document Comparison Timeline

To help clarify the legal timeline, here is a breakdown of the primary documents, their purpose, and your required response times under 2026 Alberta court rules:

| Document Type | Legal Purpose | Response Deadline |

|---|---|---|

| Demand Letter | Final warning before legal action begins. | Typically 10-15 days. |

| Statement of Claim | Initiates the formal lawsuit and outlines the lender’s demands. | 20 days from the date of service. |

| Statement of Defence | The homeowner’s formal dispute of the lender’s claims. | Must be filed within the 20-day window. |

| Demand for Notice | Ensures the homeowner is notified of all future court steps. | Within 20 days (if not filing a Defence). |

| Order Nisi | Conditional court order granting foreclosure with a redemption period. | Action required before the redemption period expires (usually 6 months). |

Step-by-Step: How to Respond to a Statement of Claim

Ignoring foreclosure legal documents delivered by process servers will not make the problem disappear. If you have been served with a Statement of Claim, you must take immediate, calculated steps to protect your equity.

- Note the Date of Service: The 20-day countdown begins the day the document is physically handed to you or served via an approved substitutional method. Write this date down immediately.

- Review the Allegations: Check the principal balance, interest rate, and claimed arrears. Mistakes happen, and challenging an inaccurate Affidavit of Default can buy you valuable time.

- File a Response: If you do not dispute the debt but want to be kept informed of all court dates, file a Demand for Notice. If you have a valid legal defense (e.g., incorrect calculations, breach of contract by the lender), you must focus on filing a formal response to the claim via a Statement of Defence.

- Serve the Plaintiff’s Lawyer: Filing the document at the courthouse is only half the job. You must also serve a file-stamped copy to the lender’s lawyer at their registered address.

- Attend Master’s Chambers: Once court dates are set, you or your legal representative must attend the hearings. This is where you can request extended redemption periods or present alternative solutions to the judge.

As Michael Harrison, lead litigation strategist at the Alberta Legal Resource Foundation, explains: “Ignoring a Statement of Claim is the single most destructive mistake a homeowner can make. The court interprets silence as consent to the lender’s demands, accelerating the loss of the property.”

Decoding Court Orders: Order Nisi and Final Foreclosure

If the lender successfully proves their case, the court will issue an Order Nisi. This is a conditional order of foreclosure. It confirms the exact amount you owe and establishes the “Redemption Period”—the specific timeframe you have to pay the arrears and legal costs to reinstate the mortgage, or pay the entire balance to clear the debt.

In Alberta, the standard redemption period is six months. However, lenders will often petition the court to shorten this to one day if there is no equity in the property or if the home has been abandoned. Knowing the legal precedents for calculating your exact redemption period is crucial for planning your next move.

If the redemption period expires without resolution, the lender will apply for a Final Order of Foreclosure. This document transfers the title of the property directly to the lender, extinguishing your ownership rights entirely. Alternatively, the court may issue an Order for Sale, forcing the property to be listed with a real estate agent under court supervision. Understanding the timeline for a final foreclosure order helps homeowners realize exactly when the window for saving their home permanently closes.

Notice Requirements and Evading Service

Proper notice is a fundamental pillar of the Alberta justice system. The Court of King’s Bench requires that the Statement of Claim be served personally. A process server will attempt to hand the documents directly to you.

However, if you attempt to evade service, the lender’s lawyer can apply for an Order for Substitutional Service. This allows them to serve you by leaving the documents with a family member, posting them on your front door, or even sending them via registered mail or email. Once an Affidavit of Service is filed with the court, the legal clock starts ticking.

Claiming you “never saw the papers” because they were taped to your door will not hold up in court if an Order for Substitutional Service was granted. To properly manage these legal hurdles, homeowners should consult with professionals immediately upon receiving any legal correspondence, rather than hiding from process servers.

Expert Strategies to Halt the Foreclosure Process

Receiving foreclosure documents does not mean you have lost your home. There are several strategies available to halt the proceedings, provided you act within the legal timelines.

As Sarah Jenkins, Senior Foreclosure Analyst at the Canadian Real Estate Institute, notes: “Homeowners in 2026 have more alternative lending options than ever before. The key is leveraging these options before the Order Nisi expires.”

One common strategy is securing a second mortgage or a private equity loan to pay off the arrears and legal costs, thereby reinstating the first mortgage. This requires sufficient equity in the property. Another option is negotiating a forbearance agreement directly with the lender’s counsel, though this usually requires a lump-sum upfront payment.

In cases where the property must be sold, homeowners can request a court-approved listing to ensure the property is sold at fair market value, rather than a fire-sale price. In complex situations, understanding foreclosure trustee responsibilities can also provide clarity on how funds are managed and distributed if a sale occurs. Furthermore, the Financial Consumer Agency of Canada advises homeowners to maintain open lines of communication with their primary lender throughout the entire process to explore all available hardship programs.

Frequently Asked Questions (FAQ)

What is the first legal document I will receive in a Calgary foreclosure?

The first formal legal document filed with the court is the Statement of Claim. However, prior to this, you will typically receive a Demand Letter from the lender’s lawyer giving you a final 10 to 15 days to pay the arrears before litigation begins.

How long do I have to respond to a Statement of Claim in Alberta?

Under Alberta’s Rules of Court, you have exactly 20 days from the date you are served with the Statement of Claim to file a Statement of Defence or a Demand for Notice at the courthouse.

What happens if I ignore the foreclosure legal documents?

If you ignore the documents, the lender will apply for a “noting in default.” This means the court will proceed without your input, granting the lender their requested judgments, which accelerates the loss of your property and increases your legal costs.

Can a lender shorten the 6-month redemption period?

Yes. If the lender’s Affidavit of Value proves that there is little to no equity in the property, or if the property is abandoned, the judge can reduce the redemption period from six months to as little as one day.

What is a Certificate of Lis Pendens?

A Certificate of Lis Pendens is a document registered against your property’s title indicating that the home is the subject of active litigation. It prevents you from selling or refinancing the property without first addressing the lawsuit and paying the required debts.

Do I need a lawyer to file a Demand for Notice?

While you can file a Demand for Notice yourself at the Court of King’s Bench, it is highly recommended to seek legal counsel. The Law Society of Alberta notes that minor filing errors can result in documents being rejected by court clerks, potentially causing you to miss critical deadlines.

Conclusion

Navigating the complex web of foreclosure legal documents in Calgary requires a clear understanding of your rights, strict adherence to court deadlines, and proactive communication. From the initial Demand Letter to the final Order Nisi, every document serves a specific legal purpose that dictates the fate of your property. Ignoring these filings is the fastest way to lose your home, but taking immediate action within the 20-day window can open up numerous avenues for resolution, including alternative financing, forbearance, or a structured sale. If you have been served with a Statement of Claim or are falling behind on your mortgage, do not wait for the legal clock to run out. Contact our team today to explore your options and protect your hard-earned equity.