Securing emergency mortgage assistance in Calgary requires immediately contacting your lender to request a forbearance agreement, applying for provincial relief through programs like the Basic Needs Fund, and documenting your financial hardship. Homeowners can access temporary payment deferrals, interest rate adjustments, or extended amortization periods to prevent default during unexpected income disruptions. Navigating these options quickly ensures you protect your property equity and avoid irreversible damage to your credit profile.

Key Takeaways

- Immediate Action is Required: Contacting your lender before missing a payment unlocks loss mitigation tools that disappear once an account enters default.

- Provincial Relief Exists: Calgary residents earning under $75,000 annually can access the Basic Needs Fund for urgent housing cost subsidies.

- Deferrals Have Long-Term Costs: Pausing payments for up to six months adds capitalized interest to your principal, increasing the total cost of borrowing.

- Documentation is Critical: Approval for hardship programs requires 90 days of bank statements, proof of income loss, and a formal letter of explanation.

- Alternative Financing Bridges Gaps: Leveraging home equity through secondary financing provides a viable lifeline when traditional lenders refuse restructuring.

Understanding Emergency Mortgage Relief in Calgary’s 2026 Economy

When sudden financial pressures disrupt household stability, Calgary homeowners require immediate clarity on available relief mechanisms. Emergency mortgage assistance encompasses a variety of temporary and permanent loan modifications designed to prevent defaults during unforeseen hardships. These interventions allow borrowers to adjust payment schedules, reduce immediate cash outflows, or pause obligations entirely while maintaining legal ownership of the property.

The economic landscape of 2026 presents unique challenges for Alberta homeowners. With inflation stabilizing but living costs remaining elevated, household budgets face unprecedented strain. According to the Financial Consumer Agency of Canada (FCAC), 28% of variable-rate mortgage holders in Alberta reached their trigger rate by early 2026, necessitating immediate structural intervention to prevent negative amortization.

The Mechanics of Trigger Rates and Negative Amortization

A trigger rate is the specific mathematical threshold where a borrower’s fixed monthly payment on a variable-rate mortgage only covers the accrued interest, leaving zero funds applied to the principal balance. Once this rate is breached, the loan enters negative amortization—meaning the total debt grows larger every month despite the homeowner making regular payments.

As David Chen, Senior Policy Analyst at the FCAC, explains: “Homeowners who ignore their trigger rate face severe equity erosion. Emergency assistance programs are specifically designed to restructure these failing loans before the accrued interest triggers a mandatory payment shock.”

Understanding these technical terms empowers homeowners to negotiate effectively with their financial institutions. Recognizing the impact of compounding frequency on deferred interest ensures borrowers make mathematically sound decisions regarding their housing debt.

How to Qualify for Financial Hardship Programs

Unexpected life events transform manageable housing costs into urgent crises overnight. Financial institutions and government agencies require quantifiable proof of distress before deploying relief resources. Preparation and meticulous documentation streamline access to these critical lifelines.

Documenting Your Income Disruption

Lenders utilize strict underwriting matrices to evaluate hardship applications. To qualify for forbearance or loan modification, borrowers must demonstrate a material change in their financial circumstances that is outside their direct control. Acceptable qualifying events include involuntary job loss, severe medical emergencies, marital separation, or natural disasters impacting the property’s structural integrity.

Applicants must compile a comprehensive financial dossier. This includes the last 90 days of pay stubs, six months of consecutive bank statements, recent tax assessments, and a formal hardship letter. The hardship letter serves as a narrative bridge, explaining exactly why the income disruption occurred and providing a realistic timeline for financial recovery.

The Role of the Basic Needs Fund and Community Advocates

Beyond lender-specific programs, Calgary offers localized community support. The Basic Needs Fund, administered through local non-profits like Rise Calgary, provides direct financial subsidies to households facing imminent displacement. To qualify in 2026, applicants must demonstrate a household income below $75,000 and provide evidence of an income drop exceeding 30% over a three-month period.

Research from Rise Calgary indicates that complete, well-documented applications reduce processing delays by 60% compared to incomplete submissions. Engaging with community housing counselors ensures your application meets all stringent provincial criteria on the first attempt.

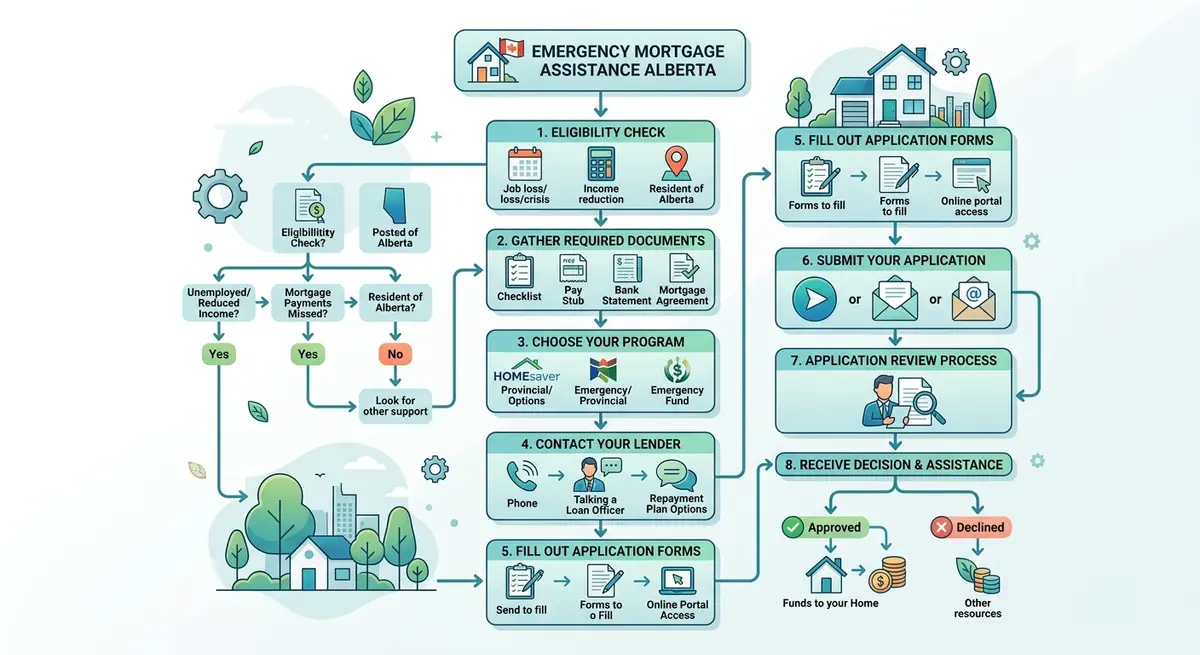

Step-by-Step Guide: Applying for Mortgage Assistance

Taking decisive, structured action transforms an overwhelming threat into a manageable administrative process. Follow this systematic method to address arrears efficiently and secure viable relief.

- Audit Your Financial Position: Calculate your exact monthly deficit. Track all housing-related expenditures, utility costs, and unsecured debt obligations. Determine exactly how much you can realistically afford to pay toward your mortgage right now.

- Review Your Existing Mortgage Contract: Examine your original loan documents for built-in relief clauses. Many standard Canadian mortgages include “skip-a-payment” privileges or prepayment retrieval options that can be activated without formal hardship approval.

- Contact Your Lender’s Loss Mitigation Department: Do not call the general customer service line. Request a direct transfer to the loss mitigation or home retention department. Present your financial audit and explicitly ask for a forbearance agreement.

- Submit a Complete Hardship Package: Deliver your bank statements, pay stubs, and hardship letter within 48 hours of your initial phone call. Delays in documentation submission frequently result in automated file closures.

- Explore Alternative Equity Solutions: If traditional lenders deny your modification request, immediately investigate secondary financing. Understanding stated income financing options provides a crucial backup plan for self-employed individuals facing temporary cash flow crises.

Lender-Specific Relief Options: Deferrals vs. Restructuring

Financial institutions possess a diverse toolkit for managing distressed accounts. The optimal solution depends entirely on whether your financial hardship is temporary (e.g., a short-term layoff) or permanent (e.g., a disabling injury reducing long-term earning capacity).

Comparing Mortgage Relief Mechanisms

| Relief Option | Immediate Benefit | Long-Term Impact | Best Suited For |

|---|---|---|---|

| Payment Deferral | Pauses payments for 3-6 months. | Interest capitalizes, increasing total loan balance. | Short-term job loss or medical emergencies. |

| Extended Amortization | Lowers monthly payment amount permanently. | Adds years to the loan, maximizing lifetime interest paid. | Permanent reductions in household income. |

| Blended Rate Conversion | Stabilizes volatile variable rate payments. | Locks borrower into a potentially higher fixed rate. | Borrowers hitting their trigger rate. |

| Capitalized Arrears | Cures default status immediately. | Increases principal balance and subsequent payments. | Homeowners recovering from a resolved crisis. |

Navigating Payment Pauses and Skip-a-Payment Features

Many modern Canadian mortgages include built-in flexibility. Skip-a-payment privileges allow borrowers in good standing to bypass one monthly installment per calendar year without penalty. This is an ideal tool for covering sudden, localized expenses like a major vehicle repair or an unexpected tax bill.

However, formal payment deferrals require rigorous approval. During a deferral, the lender suspends the obligation to make principal and interest payments for a specified period (typically up to six months). Crucially, interest continues to accrue daily on the outstanding balance. At the end of the deferral period, this accrued interest is added to the principal balance—a process known as capitalization.

As Sarah Jenkins, Senior Housing Counselor at the Canada Mortgage and Housing Corporation (CMHC), explains: “Proactive communication with your lender is the single most effective strategy to prevent foreclosure proceedings. Lenders possess a mandate to exhaust all loss mitigation tools before initiating legal action, but they cannot help a borrower who refuses to answer the phone.”

Alternative Financing: Leveraging Home Equity During a Crisis

When traditional banks refuse to extend forbearance, or when arrears have already triggered legal action, homeowners must look toward alternative financial instruments. Calgary’s robust private lending market offers solutions based on property equity rather than strict credit scores or immediate income verification.

When to Consider a Second Mortgage for Arrears

If you possess substantial equity in your home (typically 20% or more), a second mortgage can provide the immediate capital required to cure arrears, pay off high-interest unsecured debt, and establish a prepaid interest reserve. This strategy effectively buys the homeowner 12 to 24 months of breathing room to secure new employment or sell the property on their own terms, rather than under the duress of a bank-forced sale.

Evaluating cash-out refinancing alternatives against secondary financing is critical. While a first-mortgage refinance offers lower interest rates, breaking a fixed-term contract often triggers exorbitant prepayment penalties (Interest Rate Differential fees) that negate the benefits. In these scenarios, a short-term second mortgage proves mathematically superior.

Furthermore, homeowners can implement principal reduction strategies once their financial situation stabilizes, aggressively paying down the secondary financing to restore their equity position.

The Long-Term Consequences of Mortgage Deferrals

While emergency assistance provides indispensable short-term relief, homeowners must acknowledge the long-term financial ramifications. Deferring payments or extending amortization periods fundamentally alters the trajectory of your wealth accumulation.

Protecting Your Credit Score and Property Title

A formal forbearance agreement, when executed properly before a missed payment, protects your credit score. The lender reports the account as “paying as agreed” during the deferral period. However, if you miss a payment before securing the agreement, that 30-day late mark remains on your Equifax and TransUnion reports for up to six years, severely impacting future borrowing capacity.

Failure to secure assistance leads directly to legal action. In Alberta, the foreclosure process moves swiftly. Once a lender files a Statement of Claim, a Lis Pendens (notice of pending litigation) is registered against your property title. Understanding the foreclosure timeline in Calgary is vital; homeowners have specific statutory rights, but the window to exercise them closes rapidly.

If you are served with legal documents, knowing the difference between a receiving a statement of claim and a simple notice of default dictates your required legal response. Furthermore, familiarizing yourself with Alberta’s redemption period—the court-ordered timeframe allowing you to pay off the arrears and halt the foreclosure—is your ultimate safety net.

Conclusion

Navigating financial hardship requires a combination of rapid action, transparent communication with lenders, and a thorough understanding of available provincial resources. Whether you utilize a temporary payment deferral, access the Basic Needs Fund, or leverage your home’s equity through alternative financing, solutions exist to keep Calgary homeowners in their properties during economic downturns. The most critical mistake a borrower can make is ignoring the problem until legal action commences. By documenting your hardship and proactively seeking assistance, you preserve your equity, protect your credit, and maintain control over your financial future. If you are facing imminent default and traditional lenders have denied your requests for restructuring, contact our team today to explore equity-based relief options tailored to your specific situation.

Frequently Asked Questions (FAQ)

What qualifies as a legitimate financial hardship for mortgage assistance?

Lenders define financial hardship as an unexpected, involuntary event that significantly reduces household income or increases essential expenses. Qualifying events typically include sudden job loss, severe medical emergencies, death of a co-borrower, or marital separation. Voluntary job changes or poor budget management do not qualify for emergency relief programs.

Will a mortgage payment deferral ruin my credit score in Canada?

No, a formally approved payment deferral will not damage your credit score, provided it is negotiated before you miss a payment. The lender will report the account as current to credit bureaus during the agreed-upon pause. However, missing a payment prior to the agreement’s approval will result in a negative mark on your credit report.

How long does it take to get approved for the Basic Needs Fund in Calgary?

Processing times for the Basic Needs Fund typically range from 5 to 10 business days, provided the applicant submits a fully complete documentation package. Delays occur primarily when applicants fail to provide consecutive bank statements or adequate proof of income disruption. Emergency fast-tracking is sometimes available for households facing imminent utility disconnection or foreclosure.

Can I use a second mortgage to pay off my mortgage arrears?

Yes, if you have sufficient equity in your property, a second mortgage can be utilized to pay off arrears, cover legal fees, and bring your first mortgage back into good standing. This strategy halts foreclosure proceedings immediately and provides a financial bridge until your regular income stabilizes.

What happens to the interest during a mortgage deferral period?

During a deferral, you are not required to make payments, but interest continues to accrue daily on your outstanding loan balance. At the end of the deferral period, this accumulated interest is capitalized (added to your principal balance). Consequently, your total debt increases, and your future monthly payments will likely rise to ensure the loan is paid off within the original amortization schedule.

Is it better to extend my amortization or take a payment deferral?

The optimal choice depends on the nature of your hardship. A payment deferral is best for short-term, acute crises (like a 3-month layoff) where income will fully recover. Extending your amortization permanently lowers your monthly payment, making it the superior choice for long-term or permanent reductions in household income, though it significantly increases the total lifetime interest paid.