A second mortgage is a secured loan that allows property owners to borrow against their accumulated home equity without altering or refinancing their original, primary mortgage. By registering a secondary charge on the property title, borrowers can access lump-sum funds or revolving credit lines at rates generally lower than unsecured debt, all while preserving the favorable terms and amortization schedule of their initial financing.

Key Takeaways

- Access up to 80% of your property’s appraised value minus existing mortgage balances.

- Preserve the low interest rate and terms of your primary mortgage while accessing new capital.

- Choose between flexible revolving credit (HELOCs) and predictable fixed-term lump-sum loans.

- Consolidate high-interest unsecured debt to potentially reduce monthly financial obligations by up to 50%.

- Understand the legal hierarchy of liens and how defaulting can lead to severe consequences, including foreclosure.

The Mechanics of Secondary Financing in Canada

In 2026, Canadian homeowners collectively hold over $2.4 trillion in untapped home equity. This staggering accumulation of wealth has prompted a surge in property owners seeking efficient ways to liquefy their assets. Tapping into your property’s value while keeping your original financing intact requires a strategic understanding of how property liens function.

When you secure additional financing against your home, the new lender registers a “junior lien” on your property title. This legal structure means the new loan holds secondary priority behind your primary financing. If financial challenges arise and the property is sold to recover debts, the original lender maintains the first claim on the proceeds. Because of this subordinate position, secondary lenders assume slightly higher risk, which is typically reflected in marginally higher interest rates compared to first mortgages.

According to Dr. Marcus Thorne, Chief Economist at the National Housing Research Institute: “Secondary financing remains the most efficient vehicle for Canadian homeowners to liquefy their real estate assets without surrendering favorable primary mortgage terms or incurring steep prepayment penalties.”

How to Calculate Your Accessible Home Equity

Financial institutions enforce strict Loan-to-Value (LTV) limits to mitigate risk. In Canada, regulations generally permit homeowners to borrow up to 80% of their property’s appraised value across all secured loans. Determining your accessible equity involves a straightforward mathematical process:

- Determine Current Market Value: Obtain a professional appraisal to establish your home’s exact worth in the current 2026 housing market.

- Calculate the 80% Threshold: Multiply your home’s appraised value by 0.80 to find the maximum allowable secured debt.

- Deduct Existing Balances: Subtract the outstanding principal of your first mortgage from the 80% threshold.

- Identify Available Funds: The remaining figure represents the maximum equity you can access through secondary financing.

For example, if your home is valued at $600,000, the 80% maximum LTV is $480,000. If you still owe $300,000 on your primary mortgage, you have $180,000 in accessible equity.

Types of Home Equity Solutions Available in 2026

Canadian property owners have multiple pathways to access their equity. Each financial instrument serves different scenarios, from spontaneous emergency expenses to meticulously planned real estate investments. When comparing cash-out refinancing alternatives, two primary structures dominate the market.

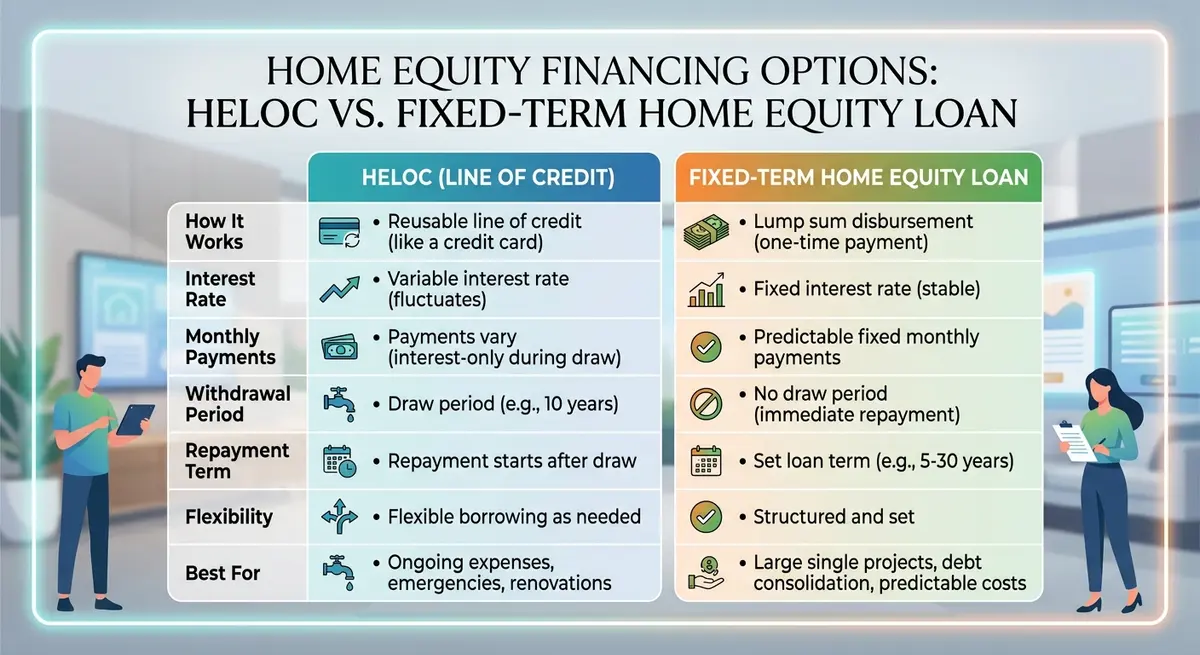

Home Equity Line of Credit (HELOC)

A Home Equity Line of Credit (HELOC) functions as a revolving financial safety net tied directly to your property’s value. The Financial Consumer Agency of Canada notes that HELOCs allow borrowers to withdraw funds up to 65% of their home’s lending value on an as-needed basis. You only pay interest on the exact amount you withdraw, making this structure highly efficient for unpredictable costs like phased renovation projects or supplementing business cash flow.

Fixed-Term Home Equity Loans

For predictable, structured funding needs, a traditional home equity loan provides a single lump-sum disbursement with fixed repayment terms. This approach suits borrowers who prefer the stability of consistent monthly payments and a clear amortization schedule. Qualification criteria for these loans often accommodate varying credit profiles, expanding access to capital for self-employed individuals who might rely on alternative documentation options.

Comparing Your Equity Options

| Feature | HELOC (Revolving) | Home Equity Loan (Fixed) |

|---|---|---|

| Fund Disbursement | Draw as needed up to a limit | Single lump-sum payout |

| Interest Rate Structure | Variable (tied to Prime Rate) | Typically fixed for the term |

| Repayment Style | Interest-only minimums available | Set principal and interest payments |

| Best Use Case | Ongoing expenses, emergency funds | Debt consolidation, large single purchases |

Strategic Uses for Your Accumulated Wealth

Unlocking your property’s potential creates immense financial flexibility. Smart equity utilization helps manage existing liabilities while funding improvements that actively boost your home’s market worth. When leveraging home equity versus unsecured credit, the cost of borrowing is substantially lower, allowing for more aggressive wealth-building strategies.

Debt Consolidation and Financial Restructuring

Data from Statistics Canada indicates that household debt service ratios remain a significant pressure point for many families. Combining high-interest credit card balances and unsecured personal loans into one manageable, secured payment simplifies your monthly budget. Because unsecured debts often carry interest rates three to four times higher than secured options, consolidating these liabilities through equity extraction can reduce monthly carrying costs by 30% to 50%.

Funding High-ROI Home Renovations

Strategic property upgrades serve a dual purpose: they improve your daily living experience while simultaneously increasing the underlying asset’s value. According to the Canada Mortgage and Housing Corporation, energy-efficient upgrades and modern kitchen remodels yield some of the highest returns on investment in the residential sector. Using a secondary loan to fund these projects ensures you aren’t draining liquid savings to build property value.

Qualification Criteria and Lender Requirements

Securing additional financing against your property involves a comprehensive evaluation of your financial health. Lenders must assess multiple risk factors to ensure you can comfortably manage multiple debt obligations.

Credit Score and Income Verification

Your credit history demonstrates your reliability in managing debt. While prime lenders (like major banks) typically require a credit score of 650 or higher, the alternative lending market in 2026 is robust. Private lenders and trust companies often place more weight on the property’s equity than the borrower’s credit score. Regardless of the lender, you must prove steady income. Lenders calculate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios to confirm your income can support the new payment structure.

Properly organizing your mortgage paperwork—including recent tax assessments, pay stubs, and property tax statements—can significantly expedite the approval process.

Navigating Interest Rates: Fixed vs. Variable

Your choice of rate structure dictates both short-term cash flow and long-term financial outcomes. Fixed-rate options lock in your interest percentage for the entire repayment period, offering absolute stability. This is ideal for borrowers on strict budgets who need predictable expenses.

Conversely, variable-rate products adjust based on the Bank of Canada‘s overnight lending rate. While these often start lower than fixed alternatives, they carry the inherent risk of rate hikes. Furthermore, borrowers must understand how compounding frequency affects your debt. A loan compounding monthly will accrue interest faster than one compounding semi-annually, subtly increasing the total cost of borrowing over the term.

Risks, Challenges, and Default Consequences

Balancing financial opportunities with potential pitfalls requires pragmatic consideration. While accessing your property’s value provides immense flexibility, it introduces strict legal obligations. Recognizing these challenges is paramount to protecting your most valuable asset.

Understanding Foreclosure Implications

Falling behind on secured loan payments puts your property at immediate risk. If you default on a secondary loan, the junior lender has the legal right to initiate foreclosure proceedings to recover their capital. However, because of the lien hierarchy, the primary mortgage holder must be paid in full from the property sale before the secondary lender receives any funds.

Navigating the foreclosure timeline is complex and stressful. If the forced sale of the property does not cover both mortgage balances, the borrower may still be held personally liable for the remaining deficiency. To mitigate these risks, homeowners should actively employ principal reduction strategies and maintain a robust emergency fund equivalent to at least three months of total debt obligations.

Conclusion

Leveraging your home’s accumulated wealth through secondary financing is a powerful strategy for Canadian homeowners in 2026. Whether you are consolidating high-interest debt, funding transformative renovations, or injecting capital into a new business venture, these secured instruments offer unparalleled flexibility. However, the benefits must be carefully weighed against the risks of increased debt loads and the severe consequences of default. By understanding the mechanics of junior liens, accurately calculating your accessible equity, and choosing the right product for your goals, you can safely turn your stagnant property value into active financial momentum. If you are ready to explore your equity options, contact our team today for a personalized assessment.