Facing eviction in Calgary can feel overwhelming, but homeowners have multiple emergency funding options available to stop the process and keep their homes. From second mortgages and emergency loans to government assistance programs, acting quickly and knowing your rights under Alberta law are essential to protecting your housing stability.

Facing eviction in Calgary can feel overwhelming, but homeowners have multiple emergency funding options available to stop the process and keep their homes. From second mortgages and emergency loans to government assistance programs, acting quickly and knowing your rights under Alberta law are essential to protecting your housing stability.

Key Takeaways

- Alberta’s Residential Tenancy Act provides specific eviction notice periods that vary by reason for termination

- Second mortgages can provide rapid funding (often within 7-14 days) using your home equity

- Government programs like the Canada-Alberta Housing Benefit offer emergency rental assistance

- Legal options exist to challenge wrongful evictions through the Residential Tenancy Dispute Resolution Service

- Acting within notice periods is critical—delays can result in irreversible loss of housing

- Multiple funding sources can be combined for faster emergency cash access

- Professional financial and legal advice significantly improves outcomes in eviction situations

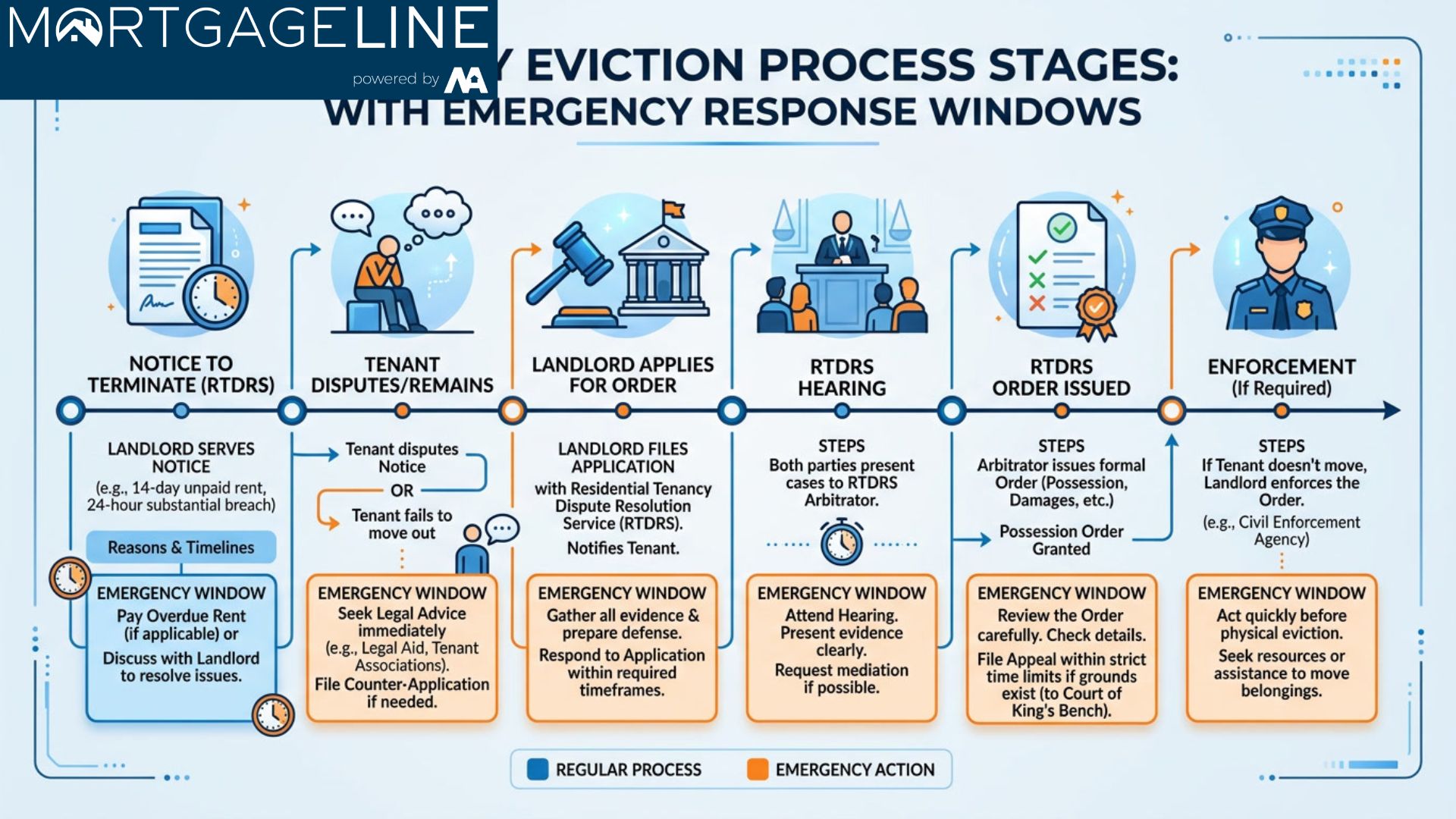

Understanding Calgary’s Eviction Process and Your Legal Rights

Before exploring emergency funding options, homeowners must understand Alberta’s specific eviction regulations. Under the Residential Tenancy Act, landlords must provide written notice with specific timeframes depending on the cause. For non-payment of rent, a 14-day notice is standard, while end of lease or landlord’s own use requires 90 days notice. According to the Government of Alberta’s official housing resources, tenants have the right to dispute any eviction notice through the Residential Tenancy Dispute Resolution Service (RTDRS).

The eviction timeline in Calgary typically follows a predictable sequence: written notice, opportunity to remedy (for curable breaches like late rent), potential application to RTDRS if unresolved, and finally a court order for enforcement. Research from the Canada Mortgage and Housing Corporation indicates that Calgary’s rental market saw a 12% increase in formal eviction applications between 2024 and 2025, highlighting the importance of knowing your options before proceedings advance.

Statistics Canada data shows that Alberta homeowners experiencing mortgage stress (spending more than 30% of income on housing) increased to approximately 18% of the provincial population in recent years. This economic pressure translates directly into eviction risk, making emergency cash solutions increasingly vital for Calgary residents.

The Importance of Acting Immediately When You Receive an Eviction Notice

Time is your most valuable resource when facing eviction. Most notice periods provide only 10-14 days to respond, and court proceedings can move quickly once initiated. Financial experts at the Financial Consumer Agency of Canada recommend that homeowners immediately assess their total debt, contact their lender, and explore all available funding options within the first 48 hours of receiving notice.

Delays in responding to eviction notices can result in sheriff enforcement, which removes belongings and changes locks within hours. Once a court order is obtained, options become severely limited and significantly more expensive to reverse. This makes early intervention the single most important factor in successfully stopping an eviction.

Emergency Funding Options for Calgary Homeowners

Calgary homeowners facing eviction have several emergency cash sources available, each with distinct advantages, requirements, and processing timelines. Understanding these options allows you to select the most appropriate solution for your specific financial situation.

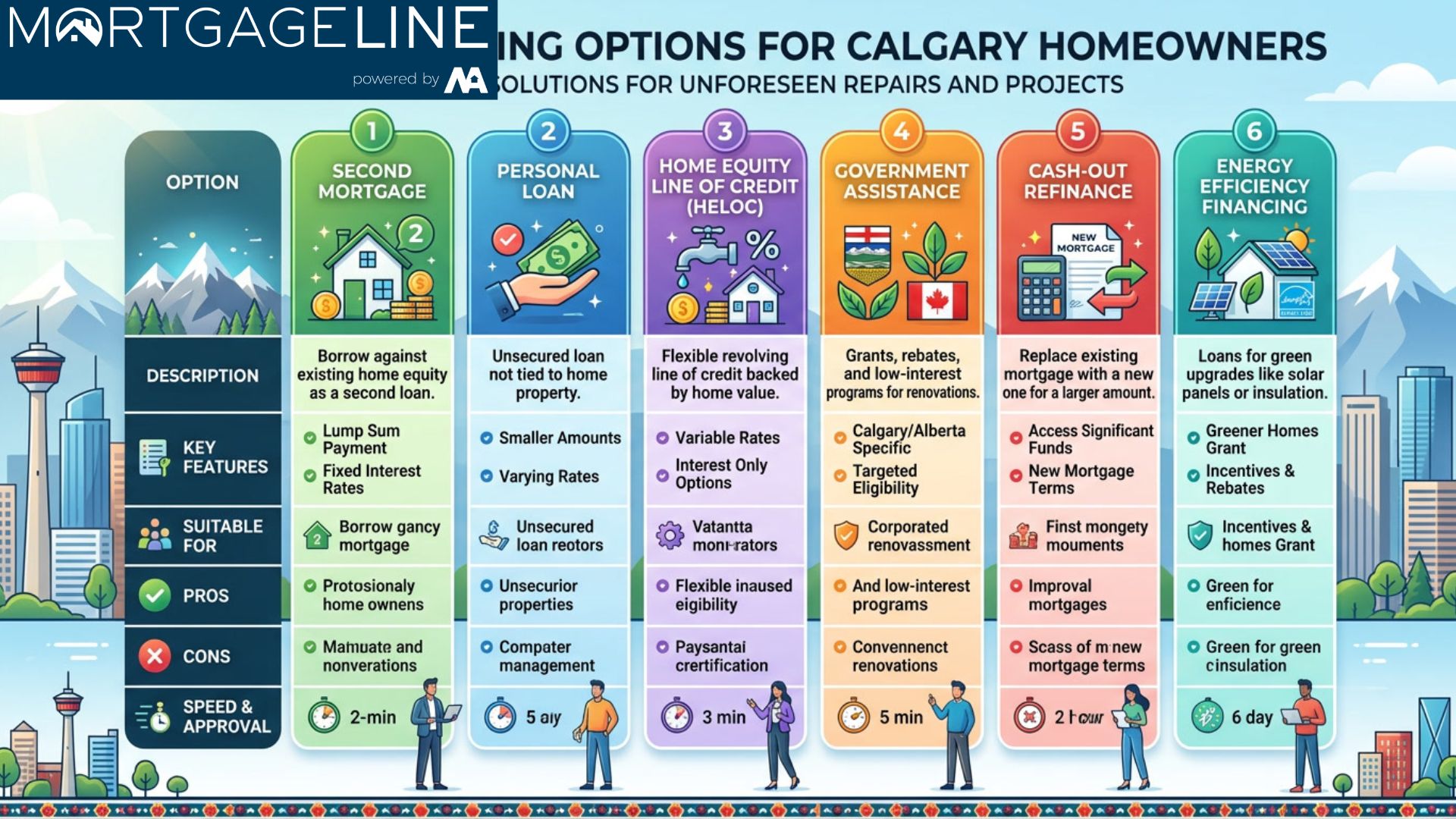

Second Mortgages: Fast Access to Home Equity

A second mortgage represents one of the fastest legitimate pathways to emergency cash for homeowners with substantial equity in their Calgary property. Unlike traditional bank mortgages, second mortgage lenders focus primarily on property value rather than credit scores, making approval more accessible for those with recent financial difficulties.

According to mortgage industry data, second mortgages in Calgary typically process within 7-14 days for qualified applicants, significantly faster than traditional refinancing which can take 45-90 days. These loans use your home as collateral, with the second mortgage sitting behind your existing first mortgage in the repayment hierarchy.

As Sarah Mitchell, a licensed mortgage specialist with extensive experience in Alberta’s housing market, explains: “Second mortgages can be an effective solution for homeowners facing urgent financial crises, but borrowers must understand the increased interest rates and potential consequences of default. The equity in your home is a powerful tool, but it should be used strategically under professional guidance.”

For homeowners dealing with mortgage arrears from major banks, exploring second mortgage options can provide the bridge funding needed to bring first mortgages current and stop foreclosure proceedings. Our guide on stopping RBC foreclosure in Alberta provides detailed strategies that apply similarly to eviction situations.

Emergency Personal Loans and Lines of Credit

Traditional financial institutions offer emergency personal loans that can provide funds within days of approval. Calgary’s major banks and credit unions assess these loans based on income verification, debt-to-income ratios, and credit history. While approval standards are strict, those with stable employment and reasonable credit can access competitive rates.

The Canada Emergency Business Account (CEBA) and similar programs have demonstrated the government’s willingness to provide low-interest emergency financing for Canadians facing economic hardship. While CEBA has concluded, similar programs may emerge based on economic conditions, making it worth checking current government offerings through the Government of Canada homepage.

Home Equity Lines of Credit (HELOCs)

A HELOC allows homeowners to borrow against accumulated equity as needed, providing flexible access to funds during financial emergencies. Unlike term loans that provide a lump sum, HELOCs function like credit cards with a set maximum, allowing you to draw only what you need and pay interest only on used amounts.

Calgary homeowners with existing mortgages may already have partial equity available for HELOC access. Financial advisors at the Financial Planning Standards Council note that HELOCs can be particularly useful when the exact amount needed is uncertain, as they provide ongoing access without requiring reapplication.

Private and Alternative Lenders

Private lenders and alternative financing companies offer emergency cash options with more flexible approval criteria than traditional banks. These lenders typically focus on property value and equity rather than credit scores, making them accessible to homeowners with recent bankruptcy, consumer proposals, or credit difficulties.

However, private financing often comes with higher interest rates and fees. The Alberta Securities Commission warns homeowners to carefully verify lender credentials and understand all terms before signing. Working with a licensed mortgage broker helps ensure you’re dealing with reputable lenders and getting competitive terms.

Government and Community Assistance Programs

Beyond traditional financing, Calgary homeowners should explore government assistance programs designed to prevent homelessness and housing instability. These programs often provide grants, low-interest loans, or rental assistance that can stop eviction proceedings.

Canada-Alberta Housing Benefit

The Canada-Alberta Housing Benefit provides monthly financial assistance to eligible renters and homeowners facing housing instability. According to the Canada Mortgage and Housing Corporation, this program has helped thousands of Alberta households maintain housing stability during financial crises. Applications can be submitted through Alberta’s Supports for Financial Need programs.

Eligibility typically considers household income, current housing costs, and evidence of housing instability or eviction risk. While processing times vary, emergency circumstances can sometimes accelerate applications for immediate assistance.

Emergency Shelter Assistance

Calgary’s Emergency Shelter Assistance program provides short-term funding for individuals and families facing immediate housing loss. Administered through Calgary’s Family and Community Support Services, this program prioritizes cases involving children, seniors, or individuals with health vulnerabilities.

Research from the Calgary Homeless Foundation indicates that rapid rehousing programs, which provide emergency financial assistance followed by ongoing support, achieve significantly better outcomes than emergency shelter placement alone. This approach helps families avoid the trauma and expense of eviction while addressing underlying financial issues.

Legal Aid Alberta

Legal Aid Alberta provides free or low-cost legal representation for qualifying individuals facing eviction. Their services include advice on rights, representation at RTDRS hearings, and assistance with documentation required for various defense strategies.

As tenant rights advocate Jennifer Wong notes: “Many homeowners don’t realize they have legal options to challenge evictions, especially when proper procedures weren’t followed or when circumstances beyond their control contributed to the breach. Legal Aid can help identify these defenses and present them effectively.”

Step-by-Step: How to Stop an Eviction with Emergency Cash

Following this structured approach maximizes your chances of successfully stopping eviction proceedings while minimizing costs and stress.

Step 1: Verify the Eviction Notice (Days 1-2)

Review your eviction notice carefully to confirm it meets Alberta legal requirements. Valid notices must include the reason for eviction, the date the tenancy ends, and information about dispute rights. According to the Residential Tenancy Act requirements, notices must be served personally or via registered mail with specific delivery timeframes.

If the notice contains procedural errors, this may provide grounds to challenge it through RTDRS before addressing the underlying financial issue. Document all communication with your landlord and keep copies of everything.

Step 2: Calculate Total Amount Needed (Days 1-2)

Determine exactly how much money you need to resolve the situation. This includes unpaid rent or mortgage payments, late fees, legal costs, and any amounts required to bring accounts current. Add a buffer for moving costs and first month’s rent at a new location in case resolution fails.

Contact your landlord or mortgage lender to get exact payoff figures. Many will provide written statements showing exact amounts due, which is essential for comparison shopping emergency funding options.

Step 3: Explore All Funding Sources Simultaneously (Days 2-5)

Apply to multiple funding sources at once to maximize approval chances and access the best terms. Prioritize sources based on processing speed and your eligibility profile. Second mortgages and private lenders typically process fastest, while government programs offer better terms but longer timelines.

Working with a mortgage broker allows single applications to reach multiple lenders, significantly improving approval odds. Our article on second mortgage approval timelines in Calgary provides detailed processing expectations for various lenders.

Step 4: Review Terms and Sign Quickly (Days 5-10)

Once approved, carefully review all loan terms before signing. Compare interest rates, repayment schedules, prepayment penalties, and total cost of borrowing. Emergency situations create pressure to sign quickly, but understanding terms prevents future problems.

Consider having a lawyer review complex financing agreements. The independent legal advice for second mortgages in Alberta guide explains why this review is particularly important for homeowners in financial distress.

Step 5: Deliver Payment and Document Resolution (Day 10-14)

Arrange payment delivery to your landlord or lender immediately upon signing. Obtain written confirmation that the debt is satisfied and request written acknowledgment that eviction proceedings will be withdrawn. File this documentation immediately with RTDRS if proceedings have been initiated.

Keep copies of all settlement documents for your records. This paper trail protects you if disputes arise later and demonstrates your good faith efforts to resolve the situation.

Comparing Emergency Funding Options

| Funding Source | Processing Time | Interest Rate | Credit Requirements | Best For |

|---|---|---|---|---|

| Second Mortgage | 7-14 days | 8-15% | Flexible | Homeowners with significant equity |

| HELOC | 14-30 days | 5-9% | Moderate | Flexible ongoing access needs |

| Personal Loan | 1-7 days | 7-20% | Strict | Good credit, stable income |

| Private Lender | 3-7 days | 12-25% | Minimal | Credit-challenged borrowers |

| Government Assistance | 14-60 days | 0-3% | Income-based | Low-income households |

Common Mistakes to Avoid When Seeking Emergency Cash

Homeowners in crisis often make decisions that worsen their situations. Understanding common pitfalls helps you avoid them during an already stressful time.

Payday loans and title loans: These predatory lending products charge extremely high interest rates (often 400% APR or more) and short repayment terms that most borrowers cannot meet. The Consumer Financial Protection Bureau warns that these products frequently trap borrowers in cycles of increasing debt. Avoid them entirely, even in emergencies.

Scams targeting distressed homeowners: The Alberta Securities Commission regularly warns about foreclosure rescue scams where fraudulent companies promise to save your home in exchange for upfront fees or deed transfers. Legitimate lenders and assistance programs never require payment before providing services. Our guide on identifying and preventing unregulated lending scams in Calgary provides detailed warning signs.

Ignoring the underlying financial problem: Stopping an eviction without addressing why you fell behind in payments simply delays the inevitable. Use emergency funding as a bridge to stabilize your situation, then develop a sustainable budget and financial plan to prevent recurrence.

Delaying action until the last moment: Court proceedings take time, and lenders need processing time for funding. Waiting until the day before a court-ordered eviction leaves no room for error. Start exploring options immediately upon receiving any eviction notice.

Long-Term Strategies to Prevent Future Eviction Risk

After resolving your immediate crisis, implementing long-term financial strategies prevents future housing instability. This includes building an emergency fund covering 3-6 months of housing costs, reducing other debts to improve cash flow, and exploring mortgage refinancing options if your current terms are unsustainable.

Calgary’s housing market, while experiencing cycles of fluctuation, has historically provided opportunities for homeowners who can maintain payments through downturns. The Canada Mortgage and Housing Corporation’s market analysis indicates that Calgary’s population growth continues to support housing demand, suggesting long-term stability for homeowners who can weather short-term challenges.

For homeowners whose financial challenges stem from unemployment or reduced income, exploring career development opportunities or retraining programs through Alberta’s workforce development resources can address root causes rather than symptoms.

Conclusion

Stopping an eviction in Calgary requires quick action, thorough understanding of your options, and strategic use of available emergency funding. Whether through second mortgages leveraging your home equity, government assistance programs, or traditional lending sources, multiple pathways exist to resolve eviction situations and maintain housing stability.

The most important steps are acting immediately upon receiving notice, calculating exactly what you need, applying to multiple sources simultaneously, and securing professional guidance throughout the process. Calgary homeowners have legal protections and funding options that, when properly utilized, can stop even advanced eviction proceedings.

If you’re facing eviction in Calgary, don’t wait until it’s too late. Contact our team today to explore your emergency funding options and develop a personalized strategy to protect your home. Visit our blog for ongoing resources about Calgary housing issues, mortgage solutions, and financial planning strategies.

References

- Government of Alberta – Residential Tenancy Act Information

- Canada Mortgage and Housing Corporation – Housing Assistance Programs

- Government of Canada – Financial Consumer Agency

- Statistics Canada – Housing Statistics

- Calgary Homeless Foundation – Research and Reports

Frequently Asked Questions

How quickly can I get emergency cash to stop an eviction in Calgary?

Emergency funding timelines vary by source. Private lenders and second mortgages can provide funds within 3-14 days, while traditional bank loans may take 2-4 weeks. Government assistance programs typically require 2-8 weeks for processing. Acting immediately upon receiving eviction notice is essential to ensure funds arrive before proceedings advance.

Can I challenge an eviction notice in Calgary even if I owe rent?

Yes, you can challenge eviction notices through the Residential Tenancy Dispute Resolution Service (RTDRS). Valid challenges may include improper notice procedures, retaliatory eviction, or demonstrating that you’ve remedied the breach. However, you typically still owe the debt even if the notice is successfully challenged, so addressing the underlying financial issue remains necessary.

What happens if I can’t pay the full amount owed to stop my eviction?

If full payment isn’t possible, you may negotiate a payment arrangement with your landlord, explore partial funding from multiple sources, or consider selling assets to generate cash. In some cases, bankruptcy or consumer proposals can eliminate certain debts, though these have significant long-term consequences and should be considered carefully with professional advice.

Will taking out a second mortgage affect my credit score?

Applying for a second mortgage involves a credit inquiry that may temporarily lower your credit score by a few points. However, making payments on time improves your score over time, and successfully stopping an eviction preserves your housing stability, which has indirect positive effects on your credit profile. The short-term credit impact is typically outweighed by the benefits of avoiding eviction.

Are there free legal resources for Calgary homeowners facing eviction?

Yes, Legal Aid Alberta provides free or low-cost legal services for qualifying individuals. The Calgary Legal Guidance office offers free legal advice clinics, and the Residential Tenancy Dispute Resolution Service provides relatively accessible dispute resolution. Tenant advocacy organizations in Calgary also offer workshops and self-help resources for those representing themselves.

Can government assistance programs help if I own my home and face eviction?

While most government housing assistance programs target renters, some programs support homeowners facing financial hardship. The Canada-Alberta Housing Benefit has limited homeowner eligibility, and emergency assistance programs through Calgary’s Family and Community Support Services may help with mortgage payments in qualifying circumstances. Contact Alberta Supports at 1-877-644-9992 to discuss your specific situation.

What should I do if I receive an eviction notice but don’t have any equity in my home?

If your home has no equity, second mortgages won’t be available, but other options exist. Personal loans from banks or credit unions, borrowing from family or friends, selling personal assets, or accessing RRSPs (with tax implications) may provide necessary funds. Government assistance programs and charitable organizations may also help in specific circumstances. A financial advisor can help identify the best options for your situation.

How can I prevent future eviction risk after resolving my current situation?

Preventing future eviction requires addressing both symptoms and root causes. Build an emergency fund covering 3-6 months of housing costs, reduce other debts to improve cash flow, review your budget for sustainable housing costs, and consider refinancing if your current mortgage terms are unaffordable. Our Calgary home equity guide offers strategies for using property value to improve overall financial health.