Purchasing a home in Calgary after experiencing a foreclosure is entirely possible, typically requiring a strategic waiting period of two to three years. By actively rebuilding your credit score, maintaining stable employment, and saving a substantial down payment, you can successfully transition from a past financial setback to securing a new mortgage. Lenders in 2026 are increasingly willing to approve applicants who demonstrate documented financial recovery and responsible debt management.

Key Takeaways

- Recovery Timeline: Most Canadians can qualify for a new mortgage 24 to 36 months after a foreclosure is finalized.

- Credit Impact: A foreclosure typically drops your credit score by 100 to 150 points, but strategic rebuilding can restore it within two years.

- Down Payment Requirements: Expect to need a larger down payment (often 15% to 20%) when applying through alternative lenders post-foreclosure.

- Documentation is Crucial: Lenders require extensive proof of income stability and a detailed letter explaining the past foreclosure.

- Alternative Lenders: B-lenders and private mortgage providers offer the most viable pathways back into the Calgary housing market.

The Reality of Purchasing Real Estate Post-Foreclosure in Alberta

Losing a property to foreclosure is a deeply stressful experience, but it does not permanently revoke your ability to own real estate. The Calgary housing market in 2026 is dynamic, and financial institutions have adapted their risk assessment models to account for economic fluctuations. According to data from the Financial Consumer Agency of Canada (FCAC), approximately 75% of Canadians who experience a foreclosure are able to re-enter the housing market within three to five years, provided they follow a strict financial rehabilitation plan.

Understanding the timeline is your first step. In Alberta, the clock on your recovery begins the moment the final order of foreclosure timeline concludes and the property title is officially transferred. From this date, traditional A-lenders (major banks) typically enforce a strict seven-year waiting period. However, the mortgage landscape is vast, and alternative lending solutions provide much faster routes to homeownership.

“Re-entering the housing market after a foreclosure isn’t about erasing the past; it’s about demonstrating financial evolution,” explains Dr. Sarah Jenkins, Senior Economist at the Canadian Real Estate Research Institute. “Lenders want to see a clear demarcation between the financial distress that caused the foreclosure and the applicant’s current economic stability.”

How a Foreclosure Impacts Your Credit Profile

To navigate your return to homeownership, you must understand exactly how a foreclosure affects your financial footprint. When a lender initiates legal action after consecutive missed payments, the impact on your credit report is immediate and severe.

Research from Equifax Canada indicates that a single foreclosure can plummet a healthy credit score by 100 to 150 points. This derogatory mark remains visible on your credit bureau report for six to seven years from the date of the first missed payment. However, the weight of this mark diminishes significantly over time. A foreclosure that occurred three years ago carries far less negative impact than one that occurred six months ago, especially if subsequent credit behavior has been flawless.

5 Strategic Steps to Rebuild Your Credit for a New Mortgage

Passive waiting will not repair your credit. To qualify for a new mortgage in Calgary, you must take proactive, documented steps to rebuild your financial reputation. Follow these five essential steps to accelerate your credit recovery:

- Automate All Current Payments: Your payment history accounts for 35% of your total credit score. Set up automatic withdrawals for utilities, cell phones, and existing credit lines to ensure you never miss a due date.

- Optimize Credit Utilization: Keep your credit card balances below 30% of their total limits. High utilization signals financial distress to future mortgage lenders.

- Secure a Credit-Builder Product: If traditional credit cards are unavailable, apply for a secured credit card. By placing a $500 to $1,000 deposit, you can establish a new, positive reporting history.

- Monitor Your Bureau Reports: Request free annual reports from both Equifax and TransUnion. Ensure the foreclosure is reported accurately and dispute any lingering errors or duplicate derogatory marks.

- Draft a Comprehensive Letter of Explanation: When you eventually apply for a mortgage, you will need a letter of explanation (LOE). Document the exact circumstances of the foreclosure (e.g., job loss, medical emergency) and detail the specific steps you have taken to ensure it will never happen again.

Mortgage Options and Lender Requirements in 2026

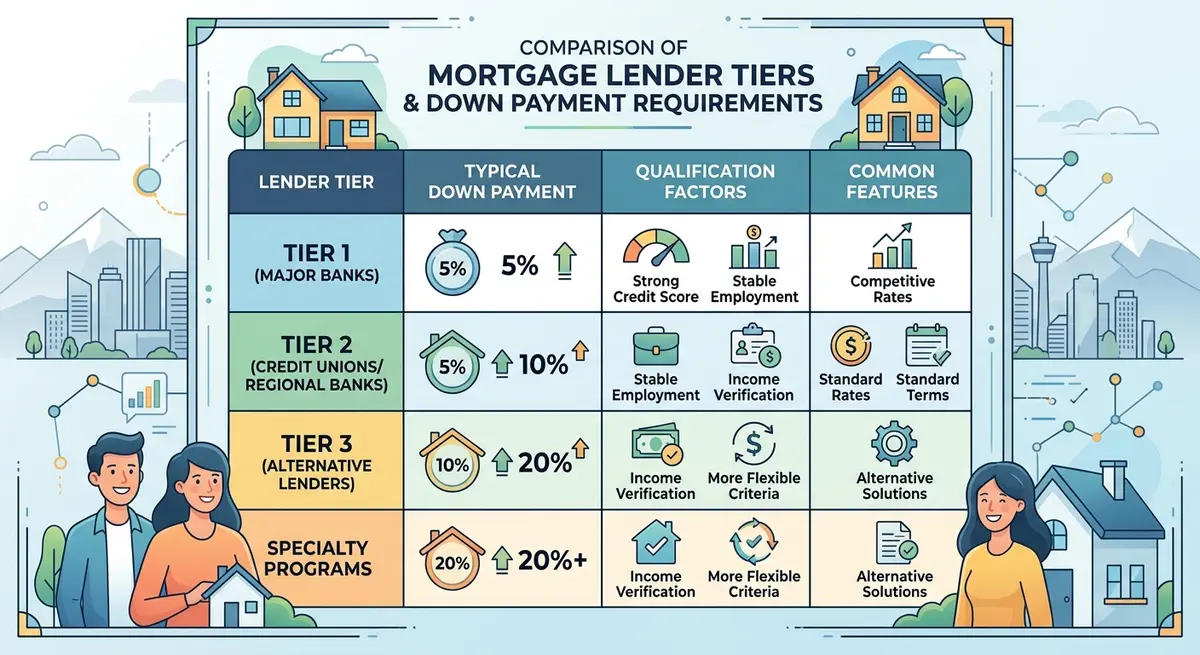

Because traditional banks are bound by strict federal stress tests mandated by the Bank of Canada, post-foreclosure buyers usually turn to alternative lending markets. Understanding the tiers of lending is crucial for setting realistic expectations regarding interest rates and down payments.

| Lender Tier | Waiting Period | Typical Down Payment | Interest Rate Impact |

|---|---|---|---|

| A-Lenders (Major Banks) | 7 Years | 5% – 20% | Standard Market Rates |

| B-Lenders (Trust Companies) | 2 – 3 Years | 15% – 20% | +1.0% to +2.5% above standard |

| Private Lenders | No strict minimum | 20% – 35% | Significantly higher premiums |

For self-employed individuals or those with complex income structures, exploring stated income mortgage options through B-lenders can be a viable workaround when traditional T4 slips do not tell the whole financial story.

Navigating the Calgary Market: Timing and Financial Preparation

Calgary’s real estate market requires strategic timing. Whether you are looking at townhomes in McKenzie Towne or detached properties in the deep south, you must approach the market with absolute financial readiness. Sellers and their agents will scrutinize your financing conditions; having a rock-solid pre-approval from an alternative lender gives you a competitive edge.

Marcus Thorne, a senior underwriter specializing in post-foreclosure recovery, notes: “In 2026, the biggest hurdle for previous foreclosure clients isn’t their credit score—it’s liquidity. Lenders want to see that you have not only securing your down payment, but also a healthy emergency fund of at least three to six months of mortgage payments in reserve.”

Gathering Your Documentation

Alternative lenders require meticulous paperwork. You must be prepared to provide extensive proof of income, bank statements, and tax returns. Properly organizing your financial paperwork well in advance prevents delays during the underwriting process. Ensure you have at least two years of Notice of Assessment (NOA) documents from the Canada Revenue Agency to prove you have no outstanding tax arrears, which is a massive red flag for lenders assessing post-foreclosure applicants.

Alternative Financing and Co-Borrower Strategies

If your individual financial profile is not yet strong enough to secure a mortgage independently, you may need to leverage external support. Bringing on a co-signer or guarantor can significantly strengthen your application. A guarantor provides a safety net for the lender, promising to cover the mortgage if you default.

However, this is a serious legal commitment. Both parties must fully understand guarantor liability considerations before signing. If you are considering using a parent as a guarantor, ensure they seek independent legal advice to protect their own retirement assets and home equity.

Legal Considerations for Your Next Property Purchase

When you are ready to purchase again, it is vital to understand the legal frameworks governing real estate transactions in Alberta. The Canada Mortgage and Housing Corporation (CMHC) outlines strict guidelines for property acquisitions, especially if you are looking at purchasing a distressed property yourself.

Interestingly, some buyers who have experienced foreclosure look to buy bank-owned (REO) properties or homes in the pre-foreclosure stage to find a deal. If you choose this route, be aware of the differences between a Judicial Sale and a Power of Sale. Judicial sales in Alberta involve court oversight, meaning the timeline can stretch from 6 to 18 months, and the property is sold “as-is, where-is.” You must budget for potential hidden costs, including immediate structural repairs or clearing municipal liens that may not have been fully disclosed.

Frequently Asked Questions (FAQ)

How long does a foreclosure stay on my credit report in Alberta?

A foreclosure remains on your Equifax and TransUnion credit reports for six to seven years from the date of the first missed payment that led to the default. However, its negative impact on your credit score decreases significantly after the first 24 months if you maintain perfect payment habits on your other accounts.

Can I buy a house 2 years after foreclosure in Calgary?

Yes, purchasing a home two years post-foreclosure is possible through B-lenders or private mortgage providers. You will need to demonstrate fully re-established credit, stable income, and typically provide a down payment of 15% to 20% to offset the lender’s perceived risk.

Will I have to pay a higher interest rate on my new mortgage?

Yes, because you will likely need to use an alternative lender rather than a major bank, you should expect to pay an interest rate premium. This premium usually ranges from 1.0% to 2.5% above standard A-lender market rates, plus potential lender fees at closing.

Do I need to disclose my past foreclosure to my new lender?

Absolutely. Failing to disclose a past foreclosure constitutes mortgage fraud. Lenders will see the public record or credit bureau mark regardless, so it is always best to be upfront and provide a detailed letter of explanation regarding the circumstances.

Can I use CMHC insurance on a home purchase after a foreclosure?

CMHC and other default insurers (like Sagen or Canada Guaranty) have very strict guidelines regarding past foreclosures. Generally, they require a minimum waiting period of five to seven years before they will insure a new mortgage for a borrower with a prior foreclosure.

How large of a down payment do I need post-foreclosure?

Because you will likely not qualify for default insurance, you cannot utilize the standard 5% down payment program. You should prepare to save a minimum of 20% for your down payment to access B-lender and private mortgage products in Calgary.

Conclusion

Experiencing a foreclosure is a major financial hurdle, but it is not the end of your homeownership journey in Calgary. By understanding the 2026 lending landscape, taking aggressive steps to rebuild your credit profile, and saving a robust down payment, you can successfully navigate your way back into the real estate market. Patience, meticulous documentation, and partnering with the right financial professionals are the keys to unlocking your second chance at property ownership.

If you are ready to explore your mortgage options and need expert guidance tailored to your unique financial history, we are here to help. Get in touch with our team today to start building your customized path back to homeownership.