Aluminum wiring, prevalent in Calgary homes built between 1965 and 1978, poses significant hurdles for securing primary mortgages and standard homeowner’s insurance. A secondary lending facility provides the necessary capital to either purchase an un-remediated property or fund essential electrical safety upgrades like pigtailing or a full house rewire. By leveraging existing home equity, property owners can bypass the rigid underwriting constraints of traditional A-lenders, ensure code compliance, and ultimately maximize their asset’s market value in the 2026 real estate landscape.

Key Takeaways

- A-Lender Restrictions: Major banks often decline primary mortgages or require exorbitant insurance premiums for homes with un-remediated solid aluminum branch wiring.

- Equity Leverage: Secondary mortgage options allow Calgary homeowners to access up to 80% Loan-to-Value (LTV) to finance immediate electrical remediation.

- Remediation Costs: Standard upgrades range from $3,500 for ESA-approved pigtailing to over $15,000 for a comprehensive copper rewire.

- Insurance Savings: Monthly insurance premiums can decrease by up to 40% once a certified master electrician verifies the completed upgrades.

- Processing Speed: Alternative lending approvals typically process within 3 to 7 business days, preventing delays in real estate transactions.

The Real Estate Challenge in Mature Calgary Neighborhoods

Calgary experienced a massive residential construction boom during the late 1960s and 1970s. Neighborhoods such as Brentwood, Dalhousie, Acadia, and Marlborough rapidly expanded to accommodate a growing workforce. During this era, copper shortages led developers to utilize solid aluminum wiring for branch circuits. While legal and compliant at the time of installation, decades of use have revealed structural flaws in the material.

Aluminum exhibits a property known as “thermal creep.” When electrical current flows, the wire heats up and expands. When the current stops, it cools and contracts. Over time, this constant expansion and contraction causes connections at outlets, switches, and breaker panels to loosen. Furthermore, exposed aluminum oxidizes rapidly, and unlike copper oxide, aluminum oxide is an electrical insulator. This combination of loose connections and high resistance increases the risk of arcing and localized overheating, which is a recognized fire hazard.

According to market data provided by the Canadian Real Estate Association, approximately 18% to 22% of the housing inventory in these established Calgary quadrants still contains partial or complete aluminum electrical systems. For buyers and current owners, this material defect complicates financing. Just as buyers face hurdles financing historic properties, older electrical infrastructure demands immediate capital intervention.

Bridging the Financial Gap with Alternative Lending

When a homebuyer puts an offer on a 1970s bungalow, standard procedure dictates a home inspection. Once the inspector identifies aluminum wiring, traditional lenders (A-lenders like major national banks) typically halt the underwriting process. They will either deny the mortgage outright or stipulate that the wiring must be professionally remediated before the funds are released. This creates a severe catch-22: the buyer cannot get the mortgage without fixing the wiring, but cannot fix the wiring without owning the house.

This is where alternative financing steps in. Utilizing a secondary lending facility allows a buyer or current owner to secure the necessary funds based on the property’s intrinsic equity rather than strict traditional banking metrics. Private lenders and secondary mortgage institutions are primarily concerned with the Loan-to-Value (LTV) ratio and the property’s marketability post-renovation. By bridging this gap, homeowners can secure the capital required to hire a certified master electrician, complete the necessary upgrades, and subsequently satisfy the conditions of A-lenders and insurance providers.

As Sarah Jenkins, Senior Underwriter at Alberta Mortgage Solutions, explains: “In 2026, we are seeing a massive shift. A-lenders are becoming hyper-conservative with older housing stock. A secondary loan acts as a strategic bridge, allowing homeowners to resolve structural or electrical deficits quickly so they can eventually transition back to prime lending rates.”

Cost vs. Equity: Analyzing Remediation Strategies

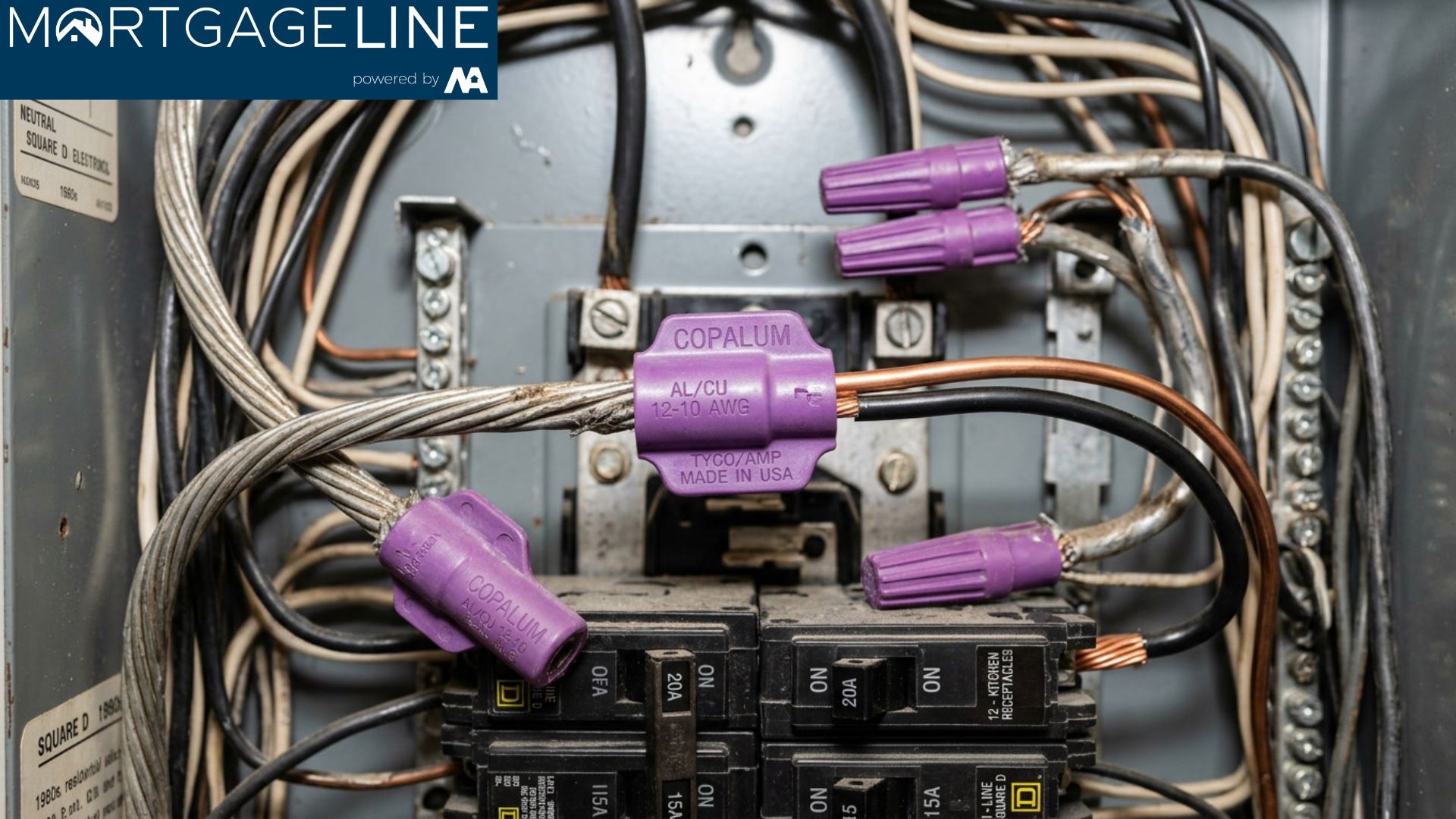

Once you secure the capital, you must choose a remediation path. The electrical code recognizes specific, permanent solutions for aluminum wiring. Attempting DIY fixes with standard wire nuts is illegal and highly dangerous due to galvanic corrosion between mismatched metals.

The two primary accepted methods are Pigtailing and a Full Rewire. Pigtailing involves splicing a short piece of copper wire to the end of the aluminum wire using specialized, approved connectors (such as COPALUM crimps or AlumiConn lugs) at every single receptacle, switch, and junction box in the home. A full rewire involves tearing out the drywall and replacing all aluminum cables with modern copper NM-B cabling.

| Remediation Method | Estimated Cost (Calgary 2026) | Project Timeline | Insurance Acceptance |

|---|---|---|---|

| Approved Pigtailing (COPALUM/AlumiConn) | $3,500 – $6,500 | 2 to 4 Days | Accepted by most carriers with ESA certificate |

| Panel Upgrade + AFCI Breakers | $2,000 – $4,000 | 1 Day | Highly Recommended supplementary step |

| Full Copper Rewire | $15,000 – $30,000+ | 2 to 4 Weeks | Universally Accepted (Premium standard) |

Choosing the right method often depends on the homeowner’s long-term goals. If you are already tearing down walls for a major renovation, a full rewire is logical. However, if the home is fully finished, pigtailing funded through a secondary loan is the most cost-effective path to compliance. Much like managing Poly-B plumbing issues, addressing the wiring head-on preserves the home’s value.

Step-by-Step Guide: Leveraging Home Equity for Upgrades

The process of utilizing your home’s equity to update aging electrical infrastructure is straightforward, provided you follow a structured approach. Understanding how long alternative approvals take will help you align your contractor’s schedule with your funding availability.

- Initial Electrical Assessment: Hire a certified master electrician to perform a comprehensive audit of all branch circuits, receptacles, and the main breaker panel. Ensure they provide a detailed written quote for ESA-approved remediation.

- Equity Evaluation: Determine your available equity by subtracting your current primary mortgage balance from the property’s estimated 2026 market value. Most secondary lenders will finance up to 80% LTV.

- Consult a Mortgage Broker: Work with an alternative lending specialist. Unlike traditional banks, private lenders prioritize the asset’s equity over stringent Debt-to-Income (DTI) ratios. Evaluating the pros and cons of secondary financing at this stage ensures you secure the best possible term.

- Appraisal and Funding: A licensed appraiser will verify the home’s current condition. Once approved, the funds are deposited directly into your account, typically within a week.

- Execution and Certification: The electrician completes the pigtailing or rewiring. Crucially, they must pull the proper municipal permits and provide a final certificate of inspection upon completion.

Navigating Home Insurance Complexities in Alberta

The intersection of property insurance and outdated building materials is a significant pain point for homeowners. According to the Insurance Bureau of Canada, electrical fires account for roughly 20% of all residential fires in Canada, with un-remediated vintage wiring acting as a leading catalyst. Consequently, insurance carriers have adopted aggressive risk mitigation policies.

If you purchase a home with solid aluminum branch circuits, standard insurance companies will typically offer a temporary 30-to-60-day policy at a highly inflated premium. This grace period is strictly to allow the new owner time to remediate the hazard. Failure to provide a certificate of electrical compliance before the deadline results in immediate policy cancellation, which in turn triggers a default on the primary mortgage.

Using a secondary loan allows homeowners to aggressively meet these tight deadlines. Mark Davies, an underwriting specialist in Calgary, notes: “We see homeowners panic when they receive a 30-day remediation notice from their insurer. Traditional bank loans simply do not close fast enough. Alternative equity financing is often the only mechanism agile enough to fund a $6,000 pigtailing job before the insurance policy is revoked.”

Maximizing Property Value Through Modernization

Beyond basic safety and insurance compliance, modernizing a home’s electrical system drastically improves its marketability. In 2026, prospective buyers in Calgary’s competitive real estate market are highly educated about material defects. A property with a clean, certified electrical bill of health will sell faster and command a higher premium than a comparable home with outstanding electrical liabilities.

Many homeowners choose to roll multiple upgrades into a single financing package. For example, while securing funds for electrical remediation, a property owner might also secure capital for energy-efficient solar panel upgrades or repairing critical foundation issues. By consolidating these renovations under one equity-backed facility, you minimize administrative fees and streamline your modernization efforts. The key is finding a competitive variable or fixed-rate secondary loan that aligns with your timeline to either sell the property or refinance it back to an A-lender.

Frequently Asked Questions

Can I get a traditional mortgage on a house with aluminum wiring?

It is very difficult. Most A-lenders will either deny the application or require an enormous down payment and proof of high-risk insurance until the wiring is professionally upgraded and certified.

Is pigtailing a permanent solution for aluminum wiring?

Yes, when performed by a certified electrician using approved connectors like COPALUM crimps or AlumiConn lugs, pigtailing is considered a permanent, code-compliant solution by the Electrical Safety Authority and major insurers.

How much equity do I need to qualify for secondary financing?

In the Calgary market, most alternative lenders require you to have at least 20% to 25% equity remaining in the property after the new loan is applied. They typically lend up to a maximum of 75% or 80% Loan-to-Value (LTV).

Do I need a new electrical panel as well?

Not always, but it is highly recommended. Upgrading to a modern panel with Arc Fault Circuit Interrupters (AFCI) adds a significant layer of safety and is viewed favorably by home insurance underwriters.

Will my insurance premiums drop after the electrical remediation?

Yes. Once you provide your insurance broker with the final electrical inspection certificate, the high-risk surcharge is removed, often reducing monthly premiums by 20% to 40%.

How fast can alternative lending funds be disbursed?

Because secondary lenders focus on property equity rather than prolonged income verification, funds can often be appraised, approved, and disbursed within 3 to 7 business days.

Conclusion

Navigating the purchase or renovation of a vintage Calgary home requires strategic financial planning, especially when confronting the strict lender and insurance policies surrounding 1970s electrical systems. Relying solely on prime banks can lead to unnecessary delays or outright denials. By leveraging a secondary mortgage, property owners unlock the agility required to fund essential upgrades, secure comprehensive insurance, and restore the home’s fundamental safety and market value. If you are facing tight deadlines from an insurance provider or need fast capital to close on a mature property, alternative equity solutions are an indispensable tool in the 2026 real estate landscape.

Are you ready to explore your equity financing options for essential home upgrades? Contact our team today to discuss how we can secure the capital you need to modernize your Calgary property securely and efficiently.