When you’re facing mortgage arrears in Alberta, time becomes your most critical resource. Private lenders can typically fund arrears resolution within 3 to 14 business days—significantly faster than traditional banks, which often take 30 to 90 days for similar arrangements. This accelerated timeline can mean the difference between saving your home and losing it to foreclosure proceedings.

- Private lenders in Alberta can resolve mortgage arrears within 3-14 business days

- Speed depends on property equity, documentation readiness, and lender workload

- Private financing can stop foreclosure proceedings faster than traditional refinancing

- Interest rates are higher but the trade-off is speed and accessibility

- Working with a licensed mortgage broker improves access to multiple private lenders

- Legal advice is strongly recommended before signing any private lending agreement

- Alberta’s foreclosure timeline typically runs 6-12 months, giving homeowners a window for action

Understanding Mortgage Arrears in Alberta

Mortgage arrears occur when a homeowner fails to make their scheduled mortgage payments. According to the Financial Consumer Agency of Canada, missing even one payment can trigger a cascade of consequences that escalate quickly. In Alberta, once a borrower falls behind by more than three payments, lenders can legally initiate foreclosure proceedings.

The Alberta Residential Mortgage Practices Act provides specific protections for borrowers, but these protections have time limits. Research from Canada Mortgage and Housing Corporation (CMHC) indicates that Alberta homeowners have approximately 6 to 12 months from the first missed payment before a property reaches the final foreclosure order stage. This window represents your opportunity to secure alternative financing and resolve the arrears.

Common causes of mortgage arrears include job loss, reduced work hours in cyclical industries like energy and construction, unexpected medical expenses, divorce or separation, and variable rate increases. Understanding why you fell behind helps determine the best resolution strategy.

What Are Private Lenders and How Do They Operate?

Private lenders are individuals, investor groups, or companies that provide mortgage financing outside the traditional banking system. Unlike chartered banks, private lenders aren’t subject to the same regulatory requirements that slow down approval processes. This flexibility allows them to make lending decisions based primarily on property equity rather than strict credit score requirements.

As the Canadian Bankers Association notes, traditional lenders must follow stringent underwriting guidelines that often disqualify borrowers with recent financial difficulties. Private lenders fill this gap by assessing risk differently—they look at the collateral value, the borrower’s equity position, and the exit strategy rather than focusing primarily on credit history.

Private lending in Alberta operates under provincial regulations, and reputable private lenders must be licensed through the Alberta Real Estate Association or similar bodies. Always verify a lender’s licensing status before entering any agreement. The Financial Consumer Agency of Canada provides resources for verifying consumer protection standards.

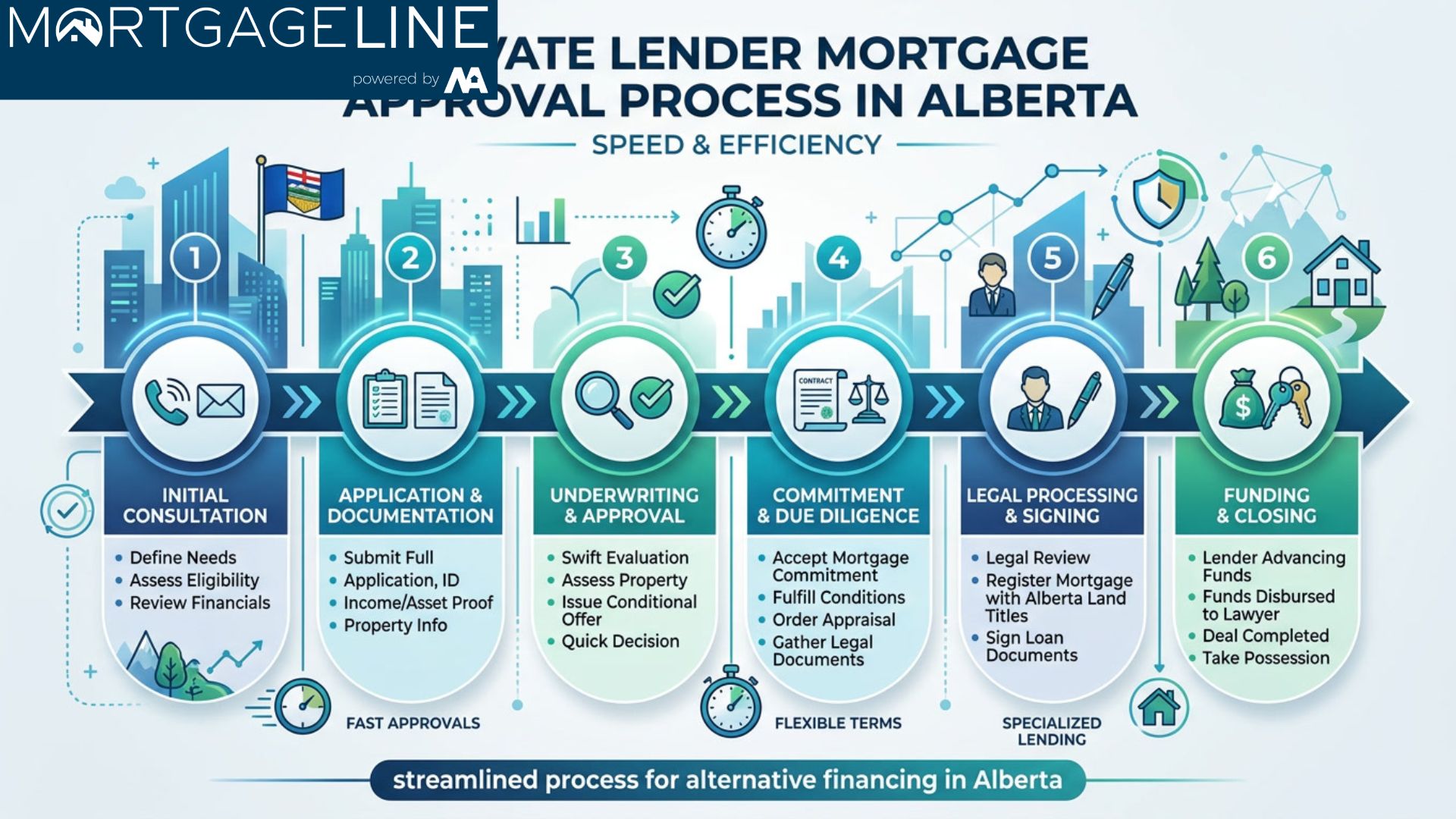

The Private Lender Arrears Resolution Timeline

One of the primary advantages of working with private lenders is the speed of funding. Here’s a realistic breakdown of how quickly a private lender can help resolve your mortgage arrears in Alberta:

Initial Consultation and Application (Days 1-2)

The process begins when you contact a private lender or mortgage broker specializing in private financing. During this phase, you’ll provide basic information about your property, current mortgage balance, and arrears amount. Most private lenders can provide a preliminary indication of approval within 24 hours based on preliminary information.

Property Appraisal and Due Diligence (Days 2-5)

After initial approval, the lender orders a property appraisal to confirm current market value. In Alberta’s major urban centres like Calgary and Edmonton, appraisers typically complete assessments within 2-3 business days. Rural properties may require additional time. The lender also reviews title, existing encumbrances, and any legal concerns during this phase.

Underwriting and Final Approval (Days 5-8)

Private lenders maintain more streamlined underwriting processes than traditional institutions. According to industry data from Real Estate Weekly, private mortgage underwriting typically takes 2-3 business days compared to 2-4 weeks for bank financing. The lender assesses your equity position, exit strategy, and ability to service the new debt.

Funding and Arrears Payoff (Days 8-14)

Once approved, funding can occur within 24-72 hours for standard transactions. More complex arrangements involving multiple lenders or legal complications may extend to 14 business days. The new private mortgage funds are used to pay off the existing lender’s arrears, bringing your mortgage current and stopping any foreclosure proceedings.

Factors That Affect Private Lender Processing Speed

While private lenders are faster than traditional banks, several variables influence exactly how quickly your arrears can be resolved:

| Factor | Impact on Timeline | Typical Adjustment |

|---|---|---|

| Property equity position | Higher equity = faster approval | Reduces processing by 2-3 days |

| Documentation readiness | Complete docs = faster processing | Reduces processing by 3-5 days |

| Property location | Urban = faster than rural | Adds 2-5 days for rural properties |

| Existing legal proceedings | Active foreclosure = urgent processing | May accelerate approval |

| Borrower exit strategy | Clear plan = faster approval | Reduces processing by 1-2 days |

| Lender current workload | Varies by lender | Adds 0-5 days depending on demand |

Working with an experienced mortgage broker can significantly reduce delays by matching your situation with lenders known for quick turnaround times. Brokers maintain relationships with multiple private lenders and understand which lenders specialize in urgent arrears situations.

Comparing Private Lenders to Traditional Banks for Arrears Resolution

When facing mortgage arrears, homeowners often wonder whether to approach their existing bank or seek private financing. Here’s how these options compare:

Traditional Bank Financing: Banks typically require excellent credit, consistent income verification, and extensive documentation. Their approval processes involve committee review, which adds time. According to the Bank of Canada, traditional mortgage refinancing can take 45-90 days from application to funding. Additionally, banks may be reluctant to refinance properties already in arrears, viewing them as elevated risk.

Private Lender Financing: Private lenders focus on property equity and exit strategy rather than credit history. This approach allows approval even when credit scores have been damaged by the financial difficulties that caused the arrears. The streamlined process typically results in funding within 2 weeks versus 2-3 months for traditional refinancing.

As Sarah Mitchell, a licensed mortgage broker with over 15 years of experience in Alberta’s private lending market, explains: “In urgent situations where foreclosure is imminent, private financing often becomes the only viable option. The speed advantage alone can save homeowners tens of thousands of dollars in legal fees and foreclosure costs.”

The Arrears Resolution Process: Step by Step

Understanding the complete process helps you prepare and respond quickly when engaging private lenders:

- Assess your situation: Calculate total arrears amount, current property value, and remaining equity. You need equity of at least 10-15% above the existing mortgage to qualify for most private financing.

- Gather documentation: Prepare property documents, existing mortgage statements, proof of income, and identification. Having these ready accelerates the process significantly.

- Contact multiple lenders or a broker: Getting quotes from 2-3 private lenders ensures competitive rates and terms. A broker can often secure better rates through established lender relationships.

- Review and compare offers: Private lender terms vary in interest rate, fees, and repayment schedule. Compare the annual percentage rate (APR) including all charges to get the true cost of financing.

- Obtain independent legal advice: Before signing any mortgage documents, consult a lawyer familiar with Alberta’s independent legal advice for second mortgages. This typically costs $500-1,000 but protects your interests.

- Sign and fund: Once legal review is complete, sign the mortgage documents and receive funding. The lender typically pays out the existing mortgage directly.

- Begin new payment schedule: Your new private mortgage has its own payment schedule. Consistent payments prevent future arrears and protect your equity.

Cost Considerations: What Faster Financing Really Means

Private lender financing typically carries higher interest rates than traditional mortgages—often 8% to 15% annually compared to 4% to 7% for bank financing. However, when evaluated against the costs of prolonged foreclosure proceedings, the premium often makes financial sense.

Consider this example: A homeowner with $50,000 in arrears faces a traditional bank refinancing timeline of 60 days. During those 60 days, the lender may continue accumulating interest on the arrears, legal fees mount, and the homeowner experiences stress-related costs. If the property enters foreclosure, additional legal costs of $15,000 to $30,000 are common in Alberta.

By securing private financing in 10 days and paying $5,000 in higher interest costs over six months, the homeowner avoids thousands in legal fees and potentially saves their home. The pros and cons of second mortgages in Calgary guide provides detailed cost comparisons.

Common Mistakes to Avoid When Seeking Private Financing

Homeowners in distress sometimes make decisions that worsen their situation. Avoid these common pitfalls:

- Waiting too long: The longer you wait, the fewer options become available. Once a foreclosure order is granted, private lenders may still help, but options narrow significantly.

- Not verifying lender credentials: Unscrupulous private lenders occasionally target desperate homeowners. Always verify licensing through Alberta Real Estate Association.

- Skipping legal review: Private mortgages are complex legal documents. Failing to get independent legal advice can result in unfavorable terms or predatory clauses.

- Borrowing from family without proper documentation: Informal family loans may seem easier but can create relationship problems and tax complications.

- Ignoring the exit strategy: Private financing is typically a bridge solution. You need a clear plan for eventual repayment or refinancing to avoid repeating the arrears cycle.

When Private Lenders Cannot Help

Despite their flexibility, private lenders cannot help every situation. Understanding when private financing isn’t viable saves time and frustration:

Insufficient equity: If your property value has declined such that you owe more than 85-90% of current value, private lenders may decline financing or charge prohibitively high rates.

Properties with significant structural issues: Homes requiring major repairs may not qualify for standard private financing. Specialized hard-money lenders exist but charge even higher rates.

Clear title problems: Properties with title disputes, easements that complicate sale, or other legal clouds may not qualify until issues are resolved.

In these situations, other options like selling the property, negotiating directly with the existing lender, or exploring government assistance programs may be necessary. The final order of foreclosure timeline for Calgary homeowners guide explores alternatives when private financing isn’t available.

Frequently Asked Questions

How quickly can a private lender actually fund my arrears resolution?

Most private lenders in Alberta can complete the entire process from application to funding within 7 to 14 business days. The fastest possible timeline is approximately 3 to 5 days for straightforward transactions with complete documentation and significant equity. Complex situations involving multiple properties, legal complications, or rural properties may require 3 to 4 weeks.

Will using a private lender stop my foreclosure proceedings?

Yes, once your new private mortgage funds and pays out the existing lender, the original lender typically discontinues foreclosure proceedings. However, you should confirm this with both lenders and potentially your lawyer, as some legal steps may need to be formally withdrawn.

What interest rate will I pay with a private lender?

Private lender rates in Alberta typically range from 8% to 15% annually, depending on your equity position, credit situation, and loan-to-value ratio. Higher rates reflect the increased risk private lenders accept and their faster, more flexible approval process. Compare the annual percentage rate (APR) including all fees when comparing offers.

Can I get private financing if I’m already in an active foreclosure?

Yes, private lenders frequently help homeowners in active foreclosure. The key is acting before the final foreclosure order is granted by the court. Once a property reaches the redemption period after a final order, selling or refinancing becomes significantly more difficult. Contacting private lenders as early as possible in the process provides more options.

Do I need a lawyer for private lender financing?

While not legally required in all cases, obtaining independent legal advice is strongly recommended before signing any private mortgage documents. Private mortgages can contain terms that differ significantly from traditional bank financing. A lawyer familiar with Alberta’s mortgage laws can identify unfavorable clauses and ensure your interests are protected.

How much equity do I need to qualify for private financing?

Most private lenders require loan-to-value ratios of 85% or lower, meaning you need at least 15% equity in your property. Some lenders accept higher LTV ratios up to 90% but typically charge higher interest rates. Calculate your equity by subtracting your current mortgage balance(s) from your property’s current market value.

What happens if I can’t qualify for private financing?

If private financing isn’t available, alternatives include selling the property before foreclosure completes, negotiating a repayment arrangement with your current lender, exploring consumer proposal options if debt extends beyond the mortgage, or contacting Alberta’s Service Alberta Consumer Contact Centre for additional resources.

Are private lenders regulated in Alberta?

Yes, private lenders operating in Alberta must comply with provincial regulations. The Alberta Real Estate Association provides licensing for mortgage brokers, and the Land Titles Office maintains records of all registered mortgages. Always verify a lender’s credentials before proceeding.

Conclusion

Private lenders offer Alberta homeowners facing mortgage arrears a significantly faster path to resolution than traditional banking options. With processing timelines of 7 to 14 days compared to 45 to 90 days for conventional refinancing, private financing can literally mean the difference between keeping your home and losing it to foreclosure.

The key to success lies in acting quickly, understanding your equity position, gathering documentation, and working with reputable, licensed professionals. While private financing carries higher interest costs, these premiums are often justified when compared to the alternative: prolonged foreclosure proceedings, mounting legal fees, and the stress of housing insecurity.

If you’re facing mortgage arrears in Alberta, don’t wait until options narrow. Contact a licensed mortgage broker or reputable private lender today to explore your options. The faster you act, the more solutions remain available to you.

Explore our blog for additional resources on foreclosure prevention, mortgage strategies, and Alberta real estate financing. Our team is ready to help you navigate your situation and find the best path forward.

References

- Financial Consumer Agency of Canada – Consumer protection guidelines and mortgage information

- Canada Mortgage and Housing Corporation (CMHC) – Housing market data and foreclosure statistics

- Canadian Bankers Association – Banking industry information and lending practices

- Bank of Canada – Monetary policy and financial system information

- Alberta Real Estate Association – Provincial real estate licensing and standards

- Service Alberta Consumer Contact Centre – Consumer protection resources

- Financial Consumer Agency of Canada (FCAC) – Financial literacy resources