When securing secondary financing in Alberta, borrowers can expect to pay between $2,200 and $4,500 in upfront fees. These typically include appraisal costs ($300–$800) to verify current property value, legal fees ($1,500–$3,000) for title searches and registration, administrative processing charges ($150–$500), and title insurance ($250–$500). Unlike primary home loans where costs are often absorbed by the lender or minimized through promotions, secondary financing requires homeowners to budget carefully for these out-of-pocket expenses or roll them into the total loan amount, which directly impacts the effective annual percentage rate (APR).

Key Takeaways

- Upfront Costs Are Mandatory: Expect to pay between $2,200 and $4,500 in total upfront fees for appraisals, legal work, and administration.

- Effective APR Increases: Rolling fees into your loan balance can increase your effective interest rate by 1.5% to 2.0% over the term.

- LTV Limits Are Strict: In 2026, most regulated Canadian lenders cap your combined loan-to-value (CLTV) ratio at 80%.

- Documentation is Critical: Missing paperwork can delay funding by weeks; prepared borrowers average an 11-day closing timeline.

- Negotiation is Possible: Borrowers can often save up to $1,000 by bundling legal and appraisal services through preferred lender networks.

Understanding the True Cost of Secondary Financing in Alberta

Borrowing against your property’s accumulated equity involves several hard costs beyond the advertised interest rate. These expenses shape your total repayment plan and vary significantly depending on the lending institution. Whether you are working with an A-lender, a B-lender, or a private mortgage investment corporation (MIC), understanding the fee structure is the first step toward responsible borrowing.

Breakdown of Common Upfront Expenses

To accurately assess your financial strategy, you must account for four primary fee categories. These are one-time payments required to process, secure, and register the new lien against your property.

| Fee Type | Estimated Cost (2026) | Description & Purpose |

|---|---|---|

| Appraisal Fees | $300 – $800 | Paid to a certified appraiser to determine the current fair market value of your home. |

| Legal Costs | $1,500 – $3,000 | Covers the lawyer’s time for document preparation, title searches, and registering the secondary lien. |

| Administrative Charges | $150 – $500 | Lender processing fees for underwriting the application and reviewing financial documents. |

| Title Services | $250 – $500 | Includes title insurance policies and obtaining updated Real Property Reports (RPR). |

According to guidelines published by the Financial Consumer Agency of Canada (FCAC), lenders are required to disclose all associated costs in the initial borrowing agreement. However, borrowers must actively request itemized estimates to avoid surprises.

“Transparency in fee structures separates trustworthy lenders from those hiding costs in the fine print,” says Dr. Elena Rostova, Senior Financial Analyst at the Canadian Mortgage Brokers Association. “In 2026, we are seeing a trend where informed borrowers successfully negotiate bundled administrative fees, saving hundreds of dollars before the ink dries.”

How Additional Lender Fees Impact Your Borrowing Power

Many homeowners make the mistake of focusing solely on the nominal interest rate, ignoring how upfront fees affect long-term affordability. When you add thousands of dollars in closing costs to your loan principal, your effective Annual Percentage Rate (APR) increases.

Calculating the Effective Annual Percentage Rate (APR)

Consider a practical scenario: A homeowner takes out a $100,000 equity loan at an 8.0% nominal interest rate amortized over 20 years. The standard monthly payment is approximately $836. However, if the borrower incurs $3,500 in upfront fees and rolls them into the loan balance, the new principal becomes $103,500. This increases the monthly payment to $865, effectively raising the APR to roughly 8.45%.

Over the life of the loan, that seemingly small $3,500 fee generates an additional $3,460 in interest charges. This highlights exactly how compounding frequency impacts your debt over time. To mitigate this, financial experts recommend paying upfront fees out-of-pocket whenever possible, rather than capitalizing them into the loan.

Comparing Primary and Secondary Loan Structures

Understanding the fundamental differences between your initial home loan and subsequent financing helps clarify why fee structures differ. While both use your real estate as collateral, their risk profiles dictate their costs.

| Aspect | Primary Mortgage | Secondary Financing |

|---|---|---|

| Lien Priority | First claim in event of default | Subordinate claim (higher risk) |

| Typical Rates (2026) | 4.5% – 6.0% | 7.5% – 14.0% |

| Borrowing Limits | Up to 95% LTV (with insurance) | Strictly capped at 80% CLTV |

| Fee Structure | Often subsidized by lender | Paid entirely by the borrower |

The higher interest rates associated with secondary loans directly reflect the increased risk to the lender. If a property goes into foreclosure, the primary lienholder is paid out first. The secondary lender only recovers funds if there is equity remaining. The Bank of Canada closely monitors these lending practices to ensure systemic stability in the housing market.

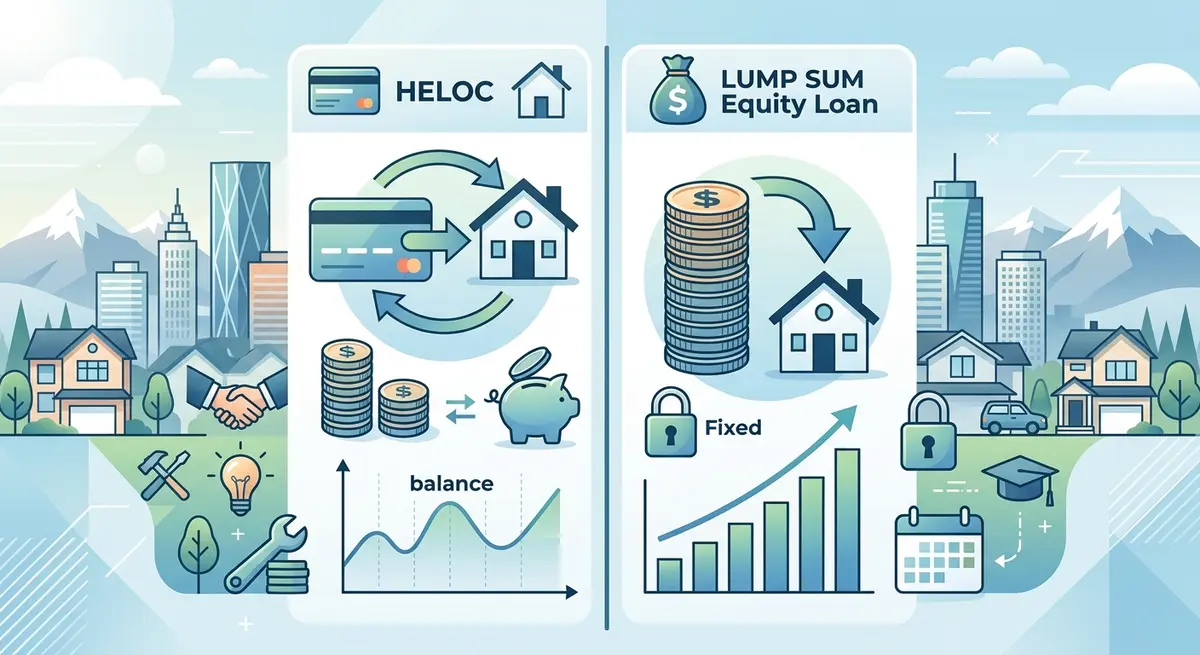

Home Equity Loans vs. HELOCs: Which Makes Financial Sense?

Property owners looking to access their home’s value generally choose between two distinct products: a lump-sum home equity loan or a Home Equity Line of Credit (HELOC). Each serves a different financial purpose and carries a unique fee structure.

A standard equity loan provides a single, lump-sum payment with a fixed interest rate and predictable monthly installments. This structure is ideal for defined expenses, such as a major roof replacement or consolidating a specific amount of high-interest credit card debt. In contrast, a HELOC functions like a revolving credit card secured by your home. You can draw funds as needed up to a predetermined limit (typically 65% of the home’s value), and you only pay interest on the amount you actively borrow.

When evaluating cash-out refinancing alternatives, consider that HELOCs often feature lower upfront legal fees but come with variable interest rates tied to the prime rate. Lump-sum loans offer rate stability but may incur higher initial appraisal and registration costs.

Step-by-Step Guide to Applying for Additional Property Financing

Navigating the application process requires meticulous organization. In 2026, lenders have tightened their underwriting standards, making preparation more critical than ever. Follow these steps to streamline your approval process and minimize unnecessary administrative fees.

- Calculate Your Available Equity: Determine your home’s current market value and subtract your existing mortgage balance. You can typically borrow up to 80% of the total value minus your current debt.

- Check Your Credit Profile: Prime lenders generally require a minimum credit score of 650. While private lenders may accept scores as low as 550, this will result in significantly higher interest rates and lender fees.

- Gather Financial Documentation: Success hinges on organizing your mortgage paperwork. Prepare two years of tax returns, recent pay stubs, and current mortgage statements.

- Verify Non-Traditional Income: If you are an entrepreneur, you must understand the specific requirements for verifying self-employed income, which often involves providing Notice of Assessments (NOAs) and business bank statements.

- Order an Independent Appraisal: While some lenders mandate using their specific appraisers, getting an independent valuation first can give you leverage during negotiations.

- Compare Multiple Offers: Never accept the first term sheet. Compare the APR, not just the nominal rate, across at least three different lending institutions.

Data from Statistics Canada indicates that household debt remains a primary concern for economic regulators. Consequently, lenders are meticulously verifying income stability before approving secondary liens. Borrowers who submit complete, well-organized applications typically see funding within 11 business days, avoiding costly processing delays.

Navigating Combined Loan-to-Value (CLTV) Ratios

Your property’s equity potential hinges on a critical financial metric known as the Combined Loan-to-Value (CLTV) ratio. This percentage compares your total loan balances (both primary and proposed secondary) against the property’s current market value.

To calculate your CLTV, add your first mortgage balance to your desired secondary loan amount, then divide that sum by your home’s appraised value. For example, if your home is worth $600,000, your first mortgage is $300,000, and you want to borrow $150,000, your total debt is $450,000. Dividing $450,000 by $600,000 yields a CLTV of 75%.

“Smart borrowers treat LTV like a speed limit – exceeding it invites financial turbulence,” explains Marcus Thorne, Director of Lending at the Alberta Financial Institute. “We strongly advise clients to keep their CLTV below 75% to secure the most favorable interest rates and avoid premium risk fees charged by private lenders.”

Higher ratios mean less equity cushion. If housing prices experience a localized correction, borrowers with an 85% or 90% CLTV risk falling into negative equity, where they owe more than the property is worth.

Strategic Benefits and Hidden Risks of Tapping Home Equity

Accessing your property’s hidden value opens doors to strategic financial moves, provided the funds are deployed intelligently. Home equity solutions allow you to tap into accumulated wealth without selling your primary residence, maintaining your position in the real estate market.

One of the most common strategic uses is debt consolidation. By paying off high-interest credit cards (often carrying rates of 19.99% or higher) with a 8.5% equity loan, borrowers can save thousands in interest. In fact, aggressive principal reduction strategies combined with consolidation can save the average household up to $18,000 in interest over a five-year period. This makes leveraging home equity versus unsecured credit a mathematically sound decision for disciplined borrowers.

Furthermore, using funds for major property renovations can yield substantial returns. According to the Alberta Real Estate Association, strategic upgrades like kitchen remodels or adding secondary basement suites can increase a property’s resale value by an average of 18% in competitive urban markets.

However, the risks are equally significant. Defaulting on a secondary loan can trigger foreclosure proceedings, jeopardizing your primary residence. Additionally, life changes such as divorce or separation can complicate repayment, making it crucial to understand the legal implications of adding a spouse to your home equity loan.

“Leveraging property wealth should always be tied to an asset-building strategy, not just consumption,” notes Sarah Jenkins, a Calgary-based certified financial planner. “Using equity to fund a business expansion or a revenue-generating suite is smart; using it to finance a depreciating asset like a luxury vehicle is a recipe for financial strain.”

Frequently Asked Questions About Home Equity Fees

Can upfront mortgage fees be rolled into the loan balance?

Yes, most lenders allow you to capitalize upfront costs like appraisal and legal fees into the total loan amount. However, doing so means you will pay interest on those fees for the entire duration of the loan, which increases your overall cost of borrowing.

Why are legal fees for secondary financing so high?

Legal fees range from $1,500 to $3,000 because the lawyer must perform extensive due diligence. This includes conducting fresh title searches, verifying the primary lender’s priority, drafting new lien documents, and registering the charge with the provincial land titles office.

Do I have to use the lender’s appraiser?

In most cases, yes. Lenders require appraisals from certified professionals on their approved vendor list to prevent fraud and ensure accurate valuations. If you order your own appraisal beforehand, the lender may still require a secondary review at your expense.

Are there penalties for paying off a secondary loan early?

It depends on the loan structure. Fixed-rate equity loans often carry prepayment penalties, typically calculated as three months of interest or an Interest Rate Differential (IRD). HELOCs, being revolving credit, usually allow penalty-free principal payments at any time.

How does my credit score affect the fees I pay?

Your credit score heavily influences both your interest rate and lender fees. Borrowers with scores below 600 are often pushed toward private lenders, who may charge “lender fees” or “brokerage fees” ranging from 1% to 3% of the total loan amount, in addition to standard legal and appraisal costs.

What is a broker fee and when is it charged?

If you use a mortgage broker to secure financing through a B-lender or private institution, the broker may charge a fee for their services (usually 1% to 2% of the loan). For A-lender prime mortgages, brokers are typically compensated directly by the bank, meaning no direct fee to the borrower.

Conclusion

Securing secondary financing is a powerful tool for homeowners looking to consolidate debt, fund renovations, or invest in new opportunities. However, the true cost of borrowing extends far beyond the advertised interest rate. By understanding the mandatory appraisal, legal, and administrative fees—and how they impact your effective APR—you can make strategic, informed decisions that protect your financial future. Always calculate your Combined Loan-to-Value (CLTV) ratio carefully, compare multiple lender offers, and ensure your borrowing aligns with a long-term wealth-building strategy.

If you are ready to explore your equity options or need help navigating the complex fee structures of Alberta’s lending market, expert guidance is just a click away. Get in touch with our team today to schedule a personalized consultation and secure the most competitive rates available in 2026.