To determine the exact financial stake you hold in your property, subtract your current outstanding mortgage balance from the present fair market value of your residence. For example, if your Calgary house is professionally appraised at $650,000 and your remaining mortgage principal is $400,000, your total ownership stake is $250,000. This figure represents your accessible wealth, serving as the foundation for refinancing, securing secondary financing, or funding major renovations.

Key Takeaways

- The Core Formula: Fair Market Value (FMV) minus Outstanding Mortgage Balance equals Total Ownership Stake.

- Borrowing Limits: Canadian financial regulations typically restrict homeowners to borrowing up to 80% of their property’s appraised value.

- Valuation Accuracy: Professional appraisals provide the definitive metric for lenders, whereas online automated valuation models (AVMs) only offer preliminary estimates.

- Market Influence: Calgary’s 2026 real estate market, driven by interprovincial migration and energy sector stability, directly impacts daily property valuations.

- Strategic Leverage: Accessible funds can be optimized through fixed-term loans or revolving credit lines to consolidate debt or increase property value.

Understanding Property Ownership Value in the 2026 Market

Owning residential real estate in Alberta is a dynamic financial journey. Your property is not merely a dwelling; it is an active financial asset that fluctuates in value based on broader economic conditions and your personal repayment habits. As you make consistent mortgage payments, you reduce the principal loan amount, thereby increasing your ownership stake. Simultaneously, if local market conditions drive property prices upward, your financial position strengthens without any additional capital injection on your part.

According to recent data from the Canadian Real Estate Association, the benchmark price for detached homes in Calgary has seen steady stabilization throughout early 2026. This stability provides a predictable environment for homeowners looking to assess their financial standing. However, understanding the exact numbers requires moving beyond broad market trends and looking at the specific metrics of your individual property.

The Step-by-Step Formula for 2026

Accurately assessing your financial position requires a systematic approach. Guesswork can lead to rejected loan applications or over-leveraging. Follow these definitive steps to calculate your exact standing:

- Determine Fair Market Value (FMV): This is the price your property would sell for in the current open market. While recent neighborhood sales provide a baseline, a certified appraisal is required for formal financial transactions.

- Verify Outstanding Principal: Check your most recent mortgage statement or online banking portal. You need the exact principal balance, excluding future interest.

- Calculate Total Stake: Subtract the principal from the FMV. (e.g., $700,000 FMV – $450,000 Mortgage = $250,000).

- Determine Accessible Borrowing Limit: Multiply your FMV by 0.80 (80%), then subtract your outstanding mortgage. This reveals the actual liquid capital you can access through lenders.

Factors Influencing Calgary Real Estate Valuations

The local real estate landscape is uniquely sensitive to specific macroeconomic drivers. Understanding these factors helps you anticipate shifts in your property’s worth before you apply for financing.

As Marcus Chen, Senior Valuation Analyst at Alberta Property Metrics, explains: “Calgary’s housing market in 2026 is highly localized. We are seeing distinct valuation divergences between established inner-city neighborhoods like Bridgeland and rapidly expanding suburban corridors like Livingston. Homeowners must look at hyper-local data, not just city-wide averages.”

| Economic Factor | Impact on Property Value | 2026 Calgary Context |

|---|---|---|

| Interprovincial Migration | Increases housing demand, driving up FMV. | Continued influx from Ontario and BC sustains high demand for detached homes. |

| Interest Rate Adjustments | Lower rates increase buyer purchasing power, elevating prices. | Stabilized rates by the Bank of Canada have created a balanced seller’s market. |

| Infrastructure Development | Proximity to new transit or amenities boosts neighborhood appeal. | Green Line LRT progress is positively impacting valuations in adjacent southern communities. |

Professional Appraisals vs. Online Estimators

In the digital age, it is tempting to rely on automated valuation models (AVMs) found on real estate portals. While these tools use algorithms to analyze public registry data and recent sales, they possess a critical blind spot: they cannot assess the interior condition, custom upgrades, or specific structural nuances of your home.

The Appraisal Institute of Canada mandates strict standards for certified evaluations. A professional appraiser conducts a comprehensive site visit, analyzing square footage, material quality, basement finishing, and immediate neighborhood comparables. If you are planning to leverage your property for substantial financing, lenders will universally require a certified appraisal to mitigate their risk.

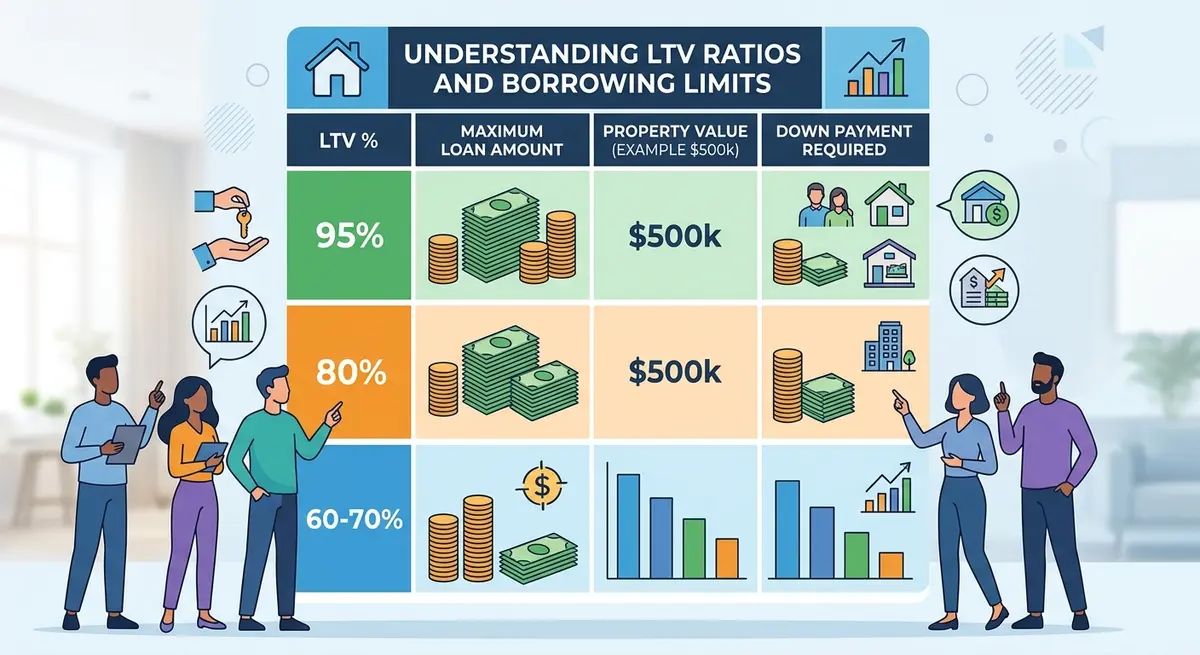

Navigating Loan-to-Value (LTV) Ratios

The Loan-to-Value (LTV) ratio is the most critical metric lenders use to assess risk. It represents the percentage of your property’s value that is currently financed by debt. The Canada Mortgage and Housing Corporation (CMHC) and federal banking regulators stipulate that homeowners can typically only refinance or borrow up to an 80% LTV ratio.

To calculate your LTV, divide your current mortgage balance by the appraised value of the home, then multiply by 100. For instance, a $400,000 mortgage on a $500,000 home results in an 80% LTV. In this scenario, you have “maxed out” your accessible borrowing limit through traditional prime lenders, even though you technically hold $100,000 in ownership stake.

Strategic Ways to Leverage Your Accessible Funds

Once you have accurately calculated your available capital, the next step is determining the most efficient way to deploy it. Transforming dormant property wealth into active financial tools requires strategic planning.

Many homeowners choose between revolving credit lines (HELOCs) and fixed-term lump-sum loans. HELOCs offer variable rates and the flexibility to draw funds as needed, making them ideal for phased renovation projects. Conversely, fixed-term loans provide a single disbursement with predictable monthly payments, which is often preferable for debt consolidation.

When deciding how to structure your borrowing, it is crucial to compare cash-out refinancing vs second mortgages. Refinancing breaks your current mortgage term—potentially triggering severe prepayment penalties if you have a low fixed rate—whereas secondary financing leaves your primary mortgage untouched.

Debt Consolidation and Financial Restructuring

One of the most mathematically sound uses of property wealth is consolidating high-interest unsecured debt. Credit cards and personal loans often carry interest rates exceeding 19%. By leveraging equity over unsecured credit, homeowners can blend these debts into a single, much lower interest rate, drastically reducing their monthly cash outflow and accelerating their path to being debt-free.

Funding Property Enhancements

Reinvesting borrowed funds back into the property creates a compounding effect. Strategic renovations—such as legal basement suites, kitchen modernizations, or energy-efficient HVAC upgrades—directly increase the Fair Market Value of the home. This effectively replenishes the ownership stake you just borrowed against, provided the renovations yield a high return on investment (ROI) in the local market.

Common Pitfalls and Edge Cases in Valuation

Navigating property finance is not without its risks. Homeowners must be vigilant about the long-term implications of their borrowing decisions. A primary concern is the amortization schedule and how interest accrues over time. Failing to understand compounding frequency impacts can result in paying thousands of dollars more in interest than initially anticipated.

Furthermore, self-employed individuals often face unique hurdles. Traditional banks rely heavily on Notice of Assessment (NOA) documents to verify income, which can disadvantage business owners who legally minimize their taxable income. In these edge cases, exploring stated income options through alternative lenders provides a viable pathway to access property wealth without standard T4 documentation.

Dealing with Co-Borrowers and Title Changes

Life events such as divorce or separation complicate valuation and borrowing. If two parties are on the title, both must consent to new financing. In situations where one partner wishes to keep the home, they must calculate the exact ownership stake to execute a fair buyout. Paying out a partner requires strict adherence to LTV limits and often necessitates secondary financing to generate the required lump sum without breaking a favorable primary mortgage rate.

Documentation and Preparation for 2026 Applications

Efficiency in securing funds relies entirely on preparation. Lenders in 2026 employ rigorous underwriting standards. Before initiating an application, ensure you have gathered all necessary paperwork. This includes recent mortgage statements, property tax assessments, proof of fire insurance, and income verification. Utilizing a comprehensive required documentation checklist will prevent processing delays and demonstrate to lenders that you are a highly organized, low-risk borrower.

Once your loan is secured, proactive management is essential. Implementing aggressive principal reduction strategies—such as bi-weekly accelerated payments or annual lump-sum contributions—will rapidly rebuild your ownership stake, ensuring long-term financial resilience.

Conclusion

Calculating your property’s financial standing is a fundamental skill for any homeowner in Calgary. By accurately assessing your Fair Market Value, understanding your outstanding principal, and navigating the 80% Loan-to-Value threshold, you unlock powerful tools for wealth generation and debt management. The 2026 economic landscape offers unique opportunities for those who approach their residential assets strategically. Whether you are looking to consolidate high-interest debt, fund a major renovation, or restructure your finances during a life transition, professional guidance ensures you maximize your borrowing power while minimizing risk. Ready to explore your exact borrowing limits and secure the best rates in Alberta? Get in touch with our team today for a personalized valuation and strategy session.

Frequently Asked Questions

What is the fastest way to estimate my property’s current market value?

The fastest preliminary method is combining recent Calgary-area comparable sales data with online automated valuation models (AVMs). However, for precise, actionable figures required by lenders, you must commission a professional appraisal from a certified local expert.

How do rising interest rates affect my ability to borrow against my property?

Higher interest rates reduce your overall borrowing power by increasing the stress-test threshold lenders use to qualify your income. Even if you have substantial ownership stake, elevated rates mean a larger portion of your income must be allocated to servicing the debt, potentially lowering your approved loan amount.

Do all home renovations increase my property’s appraised value?

No. While functional upgrades like kitchen modernizations or adding a legal basement suite typically yield a high return on investment, over-improving for your specific neighborhood or installing highly personalized features (like luxury swimming pools) often results in a low valuation bump compared to the capital spent.

What is the difference between a HELOC and a traditional fixed-term loan?

A Home Equity Line of Credit (HELOC) provides flexible, revolving access to funds with variable interest rates, allowing you to borrow, repay, and borrow again. A traditional fixed-term loan provides a single lump-sum disbursement with a locked-in interest rate and a predictable monthly repayment schedule.

What credit score is required to qualify for equity-based financing in 2026?

Prime lenders and major banks typically require a minimum credit score of 680 to access the best rates. However, alternative lenders focus more on the property’s Loan-to-Value ratio and marketability, often approving borrowers with scores in the 550-650 range, albeit at slightly higher interest rates.

Are there tax implications when using borrowed funds for non-property expenses?

In Canada, interest paid on funds borrowed against your primary residence is generally not tax-deductible if the money is used for personal expenses like vacations or consumer debt consolidation. However, if the funds are directly invested into income-producing assets (like a business or dividend stocks), the interest may be tax-deductible. Always consult a certified accountant.