Adding a non-residing individual with strong income and credit to your property title and mortgage application instantly lowers your Total Debt Service (TDS) ratio, allowing you to bypass strict 2026 banking stress tests. This strategic financing solution enables Alberta homeowners to access locked home equity for debt consolidation, renovations, or investments when their solo income falls short of traditional lending requirements.

Key Takeaways

- Income Combination: Merging incomes drastically lowers your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios, turning bank rejections into alternative lender approvals.

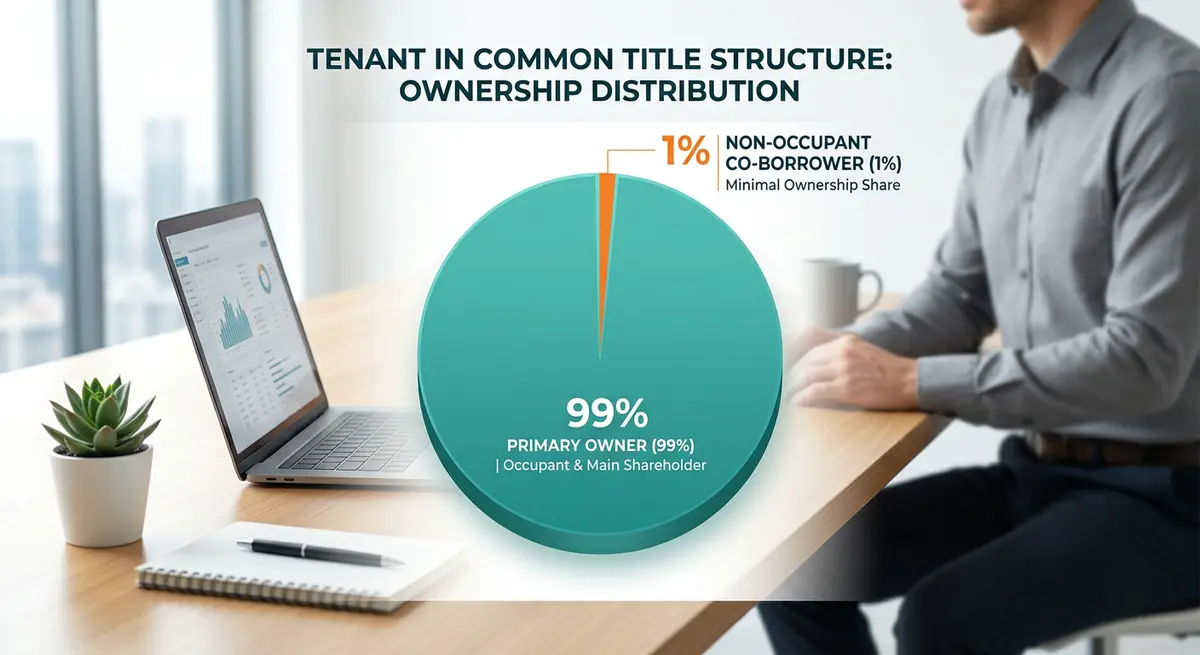

- The 1% Rule: Structuring ownership as 99% primary owner and 1% co-borrower minimizes the co-borrower’s capital gains tax exposure.

- Legal Safeguards: Independent Legal Advice (ILA) is a mandatory requirement in Alberta to ensure the co-borrower fully understands their liability.

- Lender Preferences: Alternative lenders prioritize Loan-to-Value (LTV) and combined household income over the rigid stress tests used by prime banks.

- Exit Planning: Always establish a documented 12 to 24-month strategy to refinance the property and release the co-borrower from the financial encumbrance.

The Financial Mechanics of Co-Borrowing in 2026

Navigating the real estate financing landscape has become increasingly difficult, particularly for those looking to access the equity in their homes. In 2026, Alberta property values have surged by an average of 8.4%, creating a perfect storm where many homeowners find themselves “house rich but cash poor.” You might have substantial equity built up in your property, but when you apply for a loan, your income alone does not meet the bank’s strict debt-service ratios.

When you apply for financing on your own, lenders evaluate your income, your debts, and your credit score. According to guidelines from the Canada Mortgage and Housing Corporation (CMHC), traditional lenders typically cap your Gross Debt Service (GDS) ratio at 39% and your Total Debt Service (TDS) ratio at 44%. If your monthly debt payments consume too much of your gross income, the lender classifies you as a high-risk applicant.

Bringing a non-residing partner onto the application fundamentally changes this mathematical equation. By adding a co-borrower, you are legally combining their income with yours for the purpose of the application. For example, if you earn $60,000 annually and your co-borrower earns $80,000, the underwriter evaluates the application based on a robust household income of $140,000.

As Sarah Jenkins, Senior Underwriter at Alberta Alternative Lending, explains: “Adding a non-occupant co-borrower fundamentally shifts the risk profile. We are no longer looking at a single strained income, but a diversified household balance sheet that provides a much wider safety net for repayment.”

Guarantor vs. Non-Occupant Co-Borrower: Understanding the Difference

It is critical to distinguish between a guarantor and a co-borrower. In the prime banking world, a guarantor might support the loan without going on the property title. However, in the private and alternative lending space—where most equity loans originate in 2026—lenders almost exclusively require a formal co-borrower.

A co-borrower must be registered on the property title. This provides the lender with cleaner legal recourse. If the loan defaults, they can initiate foreclosure on the property without having to sue a separate party first. For a deeper dive into the risks involved, it is vital to understand guarantor responsibilities and liabilities and how they differ from direct co-borrowing.

| Feature | Guarantor | Non-Occupant Co-Borrower |

|---|---|---|

| Title Ownership | Not on title | Must be registered on title |

| Income Usage | Used to back up the loan | Directly combined with primary borrower |

| Lender Preference | Rarely accepted by private lenders | Highly preferred by alternative lenders |

| Legal Liability | Secondary liability | 100% joint and several liability |

Who Makes the Ideal Co-Borrower in 2026?

Not everyone is a suitable candidate for this financial strategy. The ideal co-borrower is someone with strong, verifiable income that is sufficient to cover their own existing debts plus a portion of your new loan. If they are already heavily leveraged with their own properties and vehicle loans, adding them will not improve your TDS ratio.

Furthermore, a solid credit history is mandatory. A co-borrower with a 700+ credit score adds significant strength to the file, potentially unlocking lower interest rates. According to data from Equifax Canada, files with a combined average credit score above 720 receive approval rates 40% higher in the alternative lending sector. Conversely, if their credit is bruised, they may drag your application down.

Lenders strongly prefer immediate family members due to the presumed moral obligation to assist. For instance, adding an adult child to your application is a highly successful strategy for overcoming pension income shortfalls. Alternatively, relying on a parent to back your financing provides lenders with the stability of long-term employment or guaranteed retirement income.

Structuring Ownership: The 1% Tenant in Common Strategy

Since the co-borrower must be registered on the property title, you must decide how much of the title they will hold. You do not have to split ownership 50/50. The most effective strategy in Alberta is to add the non-occupant co-borrower to the title with a 1% interest as a “Tenant in Common.”

Structuring the ownership as 99% for you and 1% for the co-borrower satisfies the lender’s requirement for the co-borrower to be an owner, while clarifying that you retain the vast majority of the equity. Using “Tenants in Common” rather than “Joint Tenancy” ensures that if the co-borrower passes away, their 1% share goes to their estate, not automatically to you. This keeps estate planning secure and prevents unintended wealth transfers.

Navigating Tax Implications and Capital Gains

This is a critical consideration that many homeowners overlook. In Canada, your primary residence is exempt from capital gains tax. However, for a non-occupant co-borrower, your home is classified as an investment property by the Canada Revenue Agency (CRA).

If the property increases in value, the non-occupant co-borrower may be liable for capital gains tax on their share of the appreciation when the property is sold or when they are removed from the title. Under the 2026 tax rules, the capital gains inclusion rate is 66.67% for gains over $250,000.

By limiting their ownership share to just 1%, you drastically minimize this potential tax burden. Their taxable gain is calculated only on 1% of the property’s total appreciation, making the eventual tax liability negligible compared to the immediate financing benefits.

Mandatory Legal Safeguards: Independent Legal Advice (ILA)

To protect all parties involved, alternative lenders in Alberta strictly require Independent Legal Advice (ILA). This means the co-borrower must meet with a separate lawyer from the one representing the primary borrower. According to the Law Society of Alberta, this ensures the co-borrower fully understands the legal encumbrances they are accepting.

David Chen, a prominent Alberta Real Estate Lawyer, notes: “ILA is not just a rubber stamp. It is a vital session where we bluntly ask the co-borrower if they understand that they could lose their own personal assets if the primary borrower defaults. It prevents coercion and validates the enforceability of the contract.”

While this adds a nominal cost to the transaction—usually between $300 and $600—it is a non-negotiable safeguard that protects both the lender and the co-borrower from future disputes.

The Application Process: Step-by-Step Guide

Securing financing with a non-occupant co-borrower requires meticulous preparation. Both parties must be fully transparent and ready to provide comprehensive documentation. Reviewing a comprehensive document checklist ensures nothing is missed during the initial stages.

- Income Verification: Gather the last two years of T4s, recent pay stubs, and employment letters for both applicants. Self-employed individuals will need T1 Generals and Notices of Assessment (NOAs).

- Credit Consent: Both parties must sign authorizations allowing the broker to pull their Equifax or TransUnion credit bureaus.

- Property Documentation: Provide the current primary loan statement, the latest property tax bill, and proof of home insurance. Organizing your paperwork efficiently speeds up the underwriting process.

- Lender Submission: Your broker will package the combined file, highlighting the strengthened TDS ratio, and submit it to targeted alternative lenders.

- Legal Registration: Once approved, both parties will meet with their respective lawyers (including the ILA requirement) to sign the commitment and register the 1% title transfer.

Crafting a Bulletproof Exit Strategy

A co-borrowing arrangement should never be viewed as a permanent solution. Before signing any documents, you must establish a documented “Exit Strategy.” This outlines exactly how and when the co-borrower will be released from the liability and removed from the property title.

Most private equity loans are structured as interest-only terms lasting 12 to 24 months. The most common exit strategy involves the primary borrower improving their credit score or increasing their income during this period, allowing them to refinance the entire debt back into their name solely. If you are unsure how this works, understanding the process of removing a partner from the title is essential before entering the agreement.

Why Alternative Lenders Outperform Traditional Banks

Traditional “A-tier” banks are notoriously rigid. They often dislike adding non-occupant co-borrowers to a file unless it fits perfectly into a specific “parent helping child” first-time buyer program. If the primary occupant cannot afford the home alone, prime banks view the file as inherently high-risk.

Private and alternative lenders operate differently. They focus primarily on the Loan-to-Value (LTV) ratio and the tangible equity in the home. As long as the property value supports the loan and there is a credible, combined income source to service the monthly payments, they are willing to deploy capital.

This makes leveraging a co-borrower an incredibly viable solution for self-employed individuals or those with bruised credit. However, borrowers must remain aware of how interest is calculated, as compounding frequency can silently increase your overall debt load if not managed properly.

Real-World Case Study: Beating the 2026 Stress Test

Consider the case of an Alberta homeowner who needed $80,000 to consolidate high-interest credit card debt. Despite having over $300,000 in home equity, their solo income resulted in a TDS ratio of 52%—well above the 44% limit. Every traditional bank declined the application.

By bringing in their retired father as a non-occupant co-borrower, they added $45,000 of stable pension income to the application. The father was added to the title as a 1% Tenant in Common. The combined income dropped the TDS ratio to a highly acceptable 38%.

An alternative lender approved the $80,000 loan at a competitive rate. Within 18 months, the primary borrower’s credit score rebounded from 610 to 720, allowing them to refinance with an A-lender and successfully remove the father from the title.

Frequently Asked Questions (FAQ)

Does the co-borrower have to be a family member?

Not necessarily, but alternative lenders strongly prefer immediate family members. Using a friend is possible, but underwriters will heavily scrutinize the relationship and the motivation for co-signing to ensure it is not a fraudulent arrangement.

Can I remove the co-borrower without refinancing?

Rarely. Because the lender approved the loan based on the strength of two incomes, removing one party requires you to prove you can afford the debt alone. This almost always necessitates a completely new application and a full refinance.

Will the co-borrower have to pay the monthly payments?

Legally, they are 100% responsible for the debt if you default. However, in practice, the primary owner makes the monthly payments. It is highly recommended to set up automated withdrawals from the primary borrower’s account to ensure payments are never missed.

How much does it cost to add a co-borrower to the title in Alberta?

You will need a real estate lawyer to register the title change and process the documents. Legal fees for the registration and title transfer typically range from $1,500 to $2,000, plus the $300 to $600 cost for the co-borrower’s Independent Legal Advice (ILA).

Can a retired parent be a non-occupant co-borrower?

Yes. Pension income, CPP, and OAS are all considered valid, highly stable income sources by lenders. If a retired parent has a strong pension and excellent credit, they make an ideal co-borrower for equity financing.

What happens to the debt if the co-borrower dies?

If the property is held as Tenants in Common (e.g., a 99%/1% split), the co-borrower’s 1% share goes to their estate, not automatically to you. The debt remains attached to the property, and you will typically need to refinance to settle the estate and remove the deceased party’s name from the title.

Conclusion

Utilizing a non-occupant co-borrower is a powerful strategy for Alberta homeowners looking to bypass the stringent 2026 banking stress tests. By combining incomes, you can dramatically lower your debt service ratios and unlock the equity trapped in your home. However, it requires careful legal structuring, such as the 1% Tenant in Common rule and mandatory Independent Legal Advice, to protect both parties from unforeseen tax and liability issues. Always ensure you have a clear 12 to 24-month exit strategy to eventually refinance and regain sole ownership of your property. If you are struggling to qualify for financing on your own, contact our team today to explore how a co-borrowing arrangement can work for your specific financial situation.