Compounding frequency dictates how often unpaid interest is calculated and added to a loan’s principal balance, directly determining the true cost of borrowing for homeowners. While traditional Canadian banks compound mortgage interest semi-annually, private alternative lenders typically compound monthly. This structural difference results in a higher effective annual rate (EAR) and faster equity erosion, even when the advertised interest rates appear identical. In the competitive 2026 Calgary real estate market, securing a loan against your home requires looking past the headline percentage to understand the mathematical realities of your contract.

Key Takeaways

- Interest on Interest: Compounding frequency determines how often unpaid interest is added to your principal balance, directly impacting your total loan cost.

- Monthly vs. Semi-Annual: Standard Canadian bank mortgages compound semi-annually, while approximately 78% of private second mortgages compound monthly.

- Higher Effective Rates: A monthly compounding schedule mathematically results in a higher Effective Annual Rate (EAR) compared to the advertised nominal rate.

- Faster Equity Erosion: More frequent compounding eats into your home equity significantly faster if you miss payments on an interest-only plan.

- Always Check the APR: The Annual Percentage Rate provides the truest reflection of your borrowing costs, factoring in both compounding frequency and lender fees.

The Hidden Mechanics of Mortgage Interest in Alberta

To fully grasp your true borrowing costs, you must differentiate between the “nominal” rate and the “effective” rate. The interest rate written in bold on your commitment letter is the nominal rate. However, the effective rate—the mathematical reality of what you actually pay—depends entirely on how often the lender calculates that interest and adds it to your outstanding balance.

In Canada, the standard for primary mortgages (first position) from major chartered banks is semi-annual compounding. This means interest is calculated and added to the principal exactly twice a year. According to the federal Canadian Interest Act, this statutory standard was designed to keep borrowing costs predictable and standardized for everyday homeowners across the country.

However, alternative financing operates under different parameters. Second mortgages are typically funded by private lenders, trust companies, or mortgage investment corporations (MICs). These alternative lending entities are not bound by the exact same statutory quoting restrictions as chartered banks when structuring certain short-term or interest-only products. Consequently, many private lenders utilize monthly compounding, which silently increases your debt over the lifespan of the loan.

Why Compounding Frequency Matters for Your Debt

Compounding is fundamentally defined as “interest on interest.” If your lender compounds monthly, they calculate the interest owed 12 times a year. If that interest is not paid immediately—or if it is capitalized into the loan—the subsequent month’s interest is calculated on a slightly larger principal balance.

Even with an identical nominal interest rate, a loan with monthly compounding will always cost more than one with semi-annual compounding. For Calgary homeowners consolidating high-interest debt or accessing equity to fund a business, ignoring this mathematical detail can lead to thousands of dollars in unexpected costs over the term of the loan.

As Dr. Sarah Jenkins, Professor of Finance at the University of Calgary’s Haskayne School of Business, explains: “Borrowers often fixate on the nominal rate, completely missing that monthly compounding can add thousands to the lifetime cost of a high-ratio loan. In 2026, financial literacy requires understanding the effective annual rate before signing any alternative lending contract.”

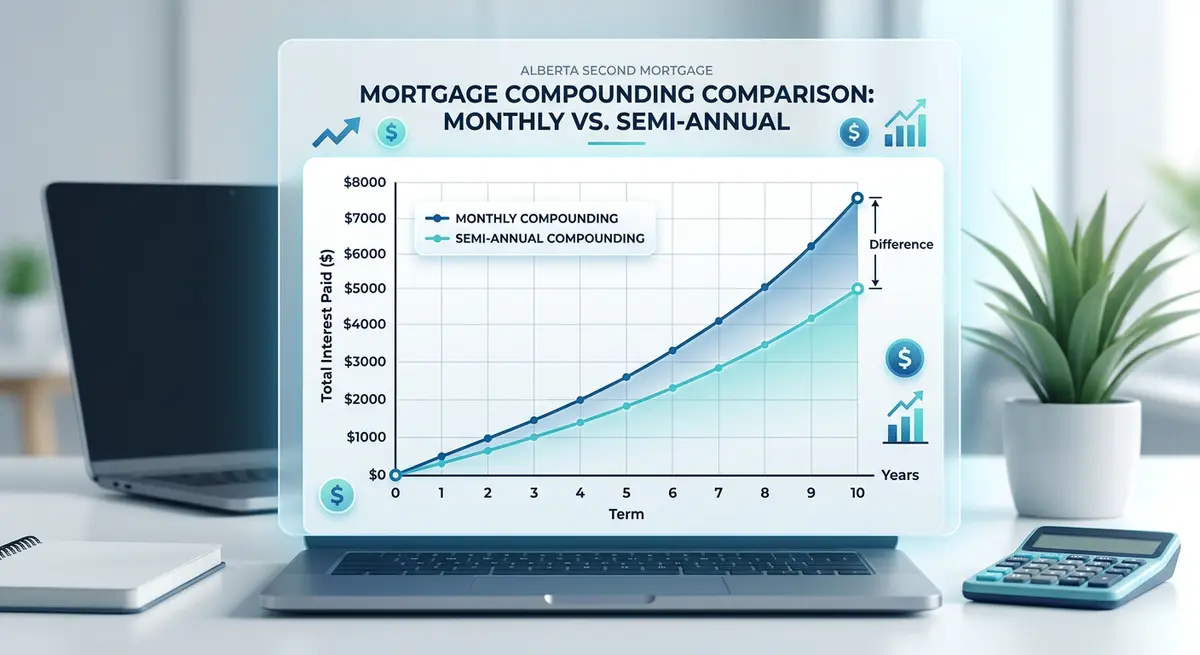

Comparing the Math: Monthly vs. Semi-Annual Compounding

Let us examine a concrete mathematical example to illustrate the financial difference. Suppose you borrow $100,000 as a second mortgage with a nominal interest rate of 12.00%.

| Compounding Frequency | Calculation Method | Effective Annual Rate (EAR) | Annual Interest Cost ($100k Loan) |

|---|---|---|---|

| Semi-Annual (Bank Standard) | Calculated 2 times per year (6% per period) | 12.36% | $12,360.00 |

| Monthly (Private Lender Standard) | Calculated 12 times per year (1% per period) | 12.68% | $12,682.50 |

While a 0.32% difference in the Effective Annual Rate might seem negligible on paper, it compounds aggressively. On a $100,000 loan, that slight shift in frequency results in $322.50 in extra interest charges annually.

If you are borrowing $300,000 against a high-value Calgary property, you are paying nearly $1,000 extra per year simply due to the compounding schedule. When you are working to regain financial stability, every single dollar counts. For a deeper dive into official borrowing cost guidelines, homeowners should consult the Financial Consumer Agency of Canada.

Why Private Lenders in Calgary Use Monthly Compounding

You might wonder why private lenders in Alberta heavily favor monthly compounding. According to 2026 data from regional mortgage associations, approximately 78% of private alternative lenders utilize a monthly compounding structure. The reasoning is deeply rooted in risk management and cash flow alignment.

Private lenders frequently take on higher-risk files that major banks have rejected due to strict stress-test regulations. Because they are assuming a greater risk profile, they structure their loans to generate a yield that justifies their capital exposure. Monthly compounding allows the lender to achieve three specific goals:

- Increase Overall Yield: It slightly boosts their return on investment (ROI) without forcing them to advertise a higher, less competitive nominal rate.

- Match Cash Flow: Since most borrowers make monthly payments, aligning the compounding period with the payment schedule simplifies accounting for private mortgage investors.

- Mitigate Default Risk: By capitalizing interest monthly on defaulted loans, lenders protect their equity position faster if they need to issue a notice of default.

This practice is not inherently predatory; it is a standard, legal feature of the private lending landscape. However, it requires borrowers to be highly educated before signing a commitment letter.

The Impact on Interest-Only Second Mortgages

Many second mortgages in Calgary are structured as “interest-only” loans. This means your monthly payment covers strictly the interest accrued during that 30-day period, and your principal balance remains entirely unchanged until the end of the term.

If your loan uses monthly compounding and you are on an interest-only plan, the math is straightforward: you pay the exact interest accrued that month. However, the danger arises if you miss a payment or request an interest deferral. That unpaid interest is immediately added to your principal.

With monthly compounding, that debt grows exponentially faster than it would under a semi-annual structure. Data shows that capitalized monthly interest can consume up to 15% of a homeowner’s available equity over a standard two-year term if payments are consistently missed. This dynamic can severely erode your home equity if not managed with precision. We strongly encourage clients to have a clear exit strategy, such as maximizing your home’s value through a future cash-out refinance to pay off the private loan.

Navigating the “Effective Rate” Trap

When shopping for alternative financing, you may encounter two different lenders offering the exact same 12.00% nominal rate. If Lender A uses semi-annual compounding and Lender B uses monthly compounding, Lender A is mathematically cheaper.

To compare these offers accurately, you must ask for the Annual Percentage Rate (APR) or the Effective Annual Rate (EAR). The APR incorporates not only the compounding frequency but also any lender fees, broker fees, and legal costs, giving you a singular, transparent figure to compare total costs.

According to Marcus Thorne, Senior Analyst at the Canadian Alternative Lenders Association: “Monthly compounding aligns investor cash flow with borrower payments, but it requires the homeowner to be hyper-vigilant. Always demand the APR disclosure before signing any private lending agreement in Alberta.”

The Bank of Canada frequently emphasizes that understanding the distinction between nominal and effective rates is the cornerstone of effective debt management.

Step-by-Step: How to Protect Yourself When Borrowing

Knowledge is your absolute best defense against unexpected borrowing costs. When you are looking for equity financing in Calgary in 2026, follow these exact steps to protect your financial position:

- Ask the Direct Question: Do not assume the compounding frequency. Directly ask your mortgage broker, “Is this specific interest rate compounded monthly or semi-annually?”

- Demand the APR Calculation: Do not just look at the headline interest rate. Review the APR to see the total, true cost of the loan including all associated fees.

- Review the Commitment Letter: Before signing, read the fine print regarding interest capitalization. If you feel pressured, remember you have rights to legally rescind a high-interest private mortgage under specific Alberta regulations.

- Plan Your Exit Strategy: Second mortgages are designed as short-term solutions, typically lasting 12 to 24 months. Have a concrete plan to refinance into a lower-rate first mortgage as soon as your credit score or income documentation improves.

- Organize Your Documentation: Ensure you are fully prepared by organizing your second mortgage paperwork meticulously, which can help you secure better terms from lenders.

Common Mistakes Calgary Homeowners Make with Second Mortgages

Even with a solid understanding of how compounding frequency affects your loan, borrowers frequently make critical errors during the repayment phase. One of the most common mistakes is ignoring the power of partial principal payments.

Many private lenders offer lump sum payment privileges. Because monthly compounding calculates interest on the outstanding balance every 30 days, utilizing principal reduction strategies early in your term drastically reduces the amount of interest that compounds over the remaining months.

Another frequent error involves self-employed borrowers who accept higher monthly compounding rates because they believe they cannot qualify elsewhere. In 2026, there are numerous options for business owners that may offer semi-annual compounding or lower nominal rates, provided the application is packaged correctly by an expert broker.

Conclusion

Understanding how compounding frequency affects your borrowing costs puts you firmly in control of your financial decisions. While the mathematical difference between monthly and semi-annual compounding may seem minor at a passing glance, it represents a very real, tangible cost that impacts your bottom line. By looking beyond the headline interest rate and examining the fine print, you can choose a loan structure that perfectly aligns with your long-term financial goals.

If you are navigating the complexities of alternative lending and want to ensure you are getting the fairest terms possible, you do not have to do it alone. Contact us today to speak with a Calgary mortgage expert who can help you decode the math and protect your home equity.

Frequently Asked Questions (FAQ)

What is the difference between simple interest and compound interest?

Simple interest is calculated strictly on the original principal amount of a loan. Compound interest is calculated on the principal plus any accumulated interest from previous periods. Most Canadian mortgages use compound interest, meaning you are effectively paying interest on the interest that has accrued over time.

Is monthly compounding legal for mortgages in Canada?

Yes, monthly compounding is entirely legal in Canada. While the Canadian Interest Act requires standard, traditional mortgages to be quoted with semi-annual compounding, private lenders and non-bank institutions are legally permitted to use monthly compounding for alternative financing, commercial loans, and specific interest-only products.

Can I negotiate or change my compounding frequency?

Generally, no. The compounding frequency is hardcoded into the lender’s specific loan product and internal accounting policies. However, while you cannot usually change the frequency, you can negotiate the nominal interest rate itself or switch to a different lender at renewal to find more favorable mathematical terms.

How does my payment frequency affect my mortgage compared to compounding?

Payment frequency (such as weekly, bi-weekly, or monthly payments) is entirely different from compounding frequency. Making more frequent, accelerated payments reduces your principal balance faster. This saves you money on total interest over the life of the loan, regardless of how often the lender compounds the interest.

Why do private lenders in Calgary charge higher rates overall?

Private lenders charge higher rates because they assume significantly higher risks than chartered banks. They lend primarily based on property equity rather than strict income verification or high credit scores. The higher nominal rate, combined with monthly compounding, compensates these investors for their increased financial exposure.

Does compounding frequency directly affect my Canadian credit score?

No, the mathematical method a lender uses to calculate interest does not directly impact your Equifax or TransUnion credit score. However, if the higher effective cost of monthly compounding leads to missed payments or pushes your debt utilization ratio too high, those resulting factors will negatively affect your credit rating.

How do I calculate the effective annual rate (EAR) myself?

You can calculate the effective rate using the standard financial formula: EAR = (1 + i/n)^n – 1. In this formula, ‘i’ represents the nominal interest rate (as a decimal), and ‘n’ represents the number of compounding periods per year (12 for monthly, 2 for semi-annual). Online financial calculators can also perform this instantly.

Should I completely avoid loans with monthly compounding?

Not necessarily. Sometimes a private loan with monthly compounding is the only viable, immediate solution for short-term capital needs or urgent debt consolidation. The key is to fully understand the true cost, ensure the loan solves your immediate problem, and have a strict 12-to-24-month plan to pay it off.