In Alberta, a private mortgage is legally classified as a “high-cost credit” product if its Annual Percentage Rate (APR) reaches or exceeds 32%. Under the provincial Consumer Protection Act, lenders offering these specific financial products must hold a specialized government license, provide a mandatory disclosure statement at least two days before signing, and offer a statutory four-day cancellation window. These strict 2026 regulations are designed to protect homeowners from predatory lending practices and hidden administrative fees that can drastically inflate the true cost of borrowing against their home equity.

Key Takeaways for Alberta Borrowers

- The 32% APR Threshold: Any loan with an Annual Percentage Rate of 32% or higher is legally defined as “High-Cost Credit” in Alberta.

- APR Includes All Fees: The APR is not just your face interest rate; it legally must include brokerage fees, administrative costs, and legal charges.

- Mandatory 2-Day Cooling-Off: Lenders must provide a comprehensive disclosure document at least two business days before you sign any legally binding agreement.

- The 4-Day Right to Cancel: Borrowers have a statutory right to cancel a high-cost credit agreement within four days of signing, without penalty.

- Strict Licensing Requirements: High-cost lenders and brokers must hold a specific, verifiable license from Service Alberta to operate legally.

Understanding Alberta’s 32% APR Threshold for Private Mortgages

Entering the private lending market can feel like stepping into a completely different financial ecosystem compared to the highly regulated environment of major Canadian banks. For many homeowners facing strict stress tests, private lenders are a vital lifeline, providing access to home equity when traditional institutions decline their applications. However, because these loans carry higher risks for the lender, they inherently come with higher interest rates and setup fees. This is where the legal line between a standard private loan and a high-cost credit product becomes critical.

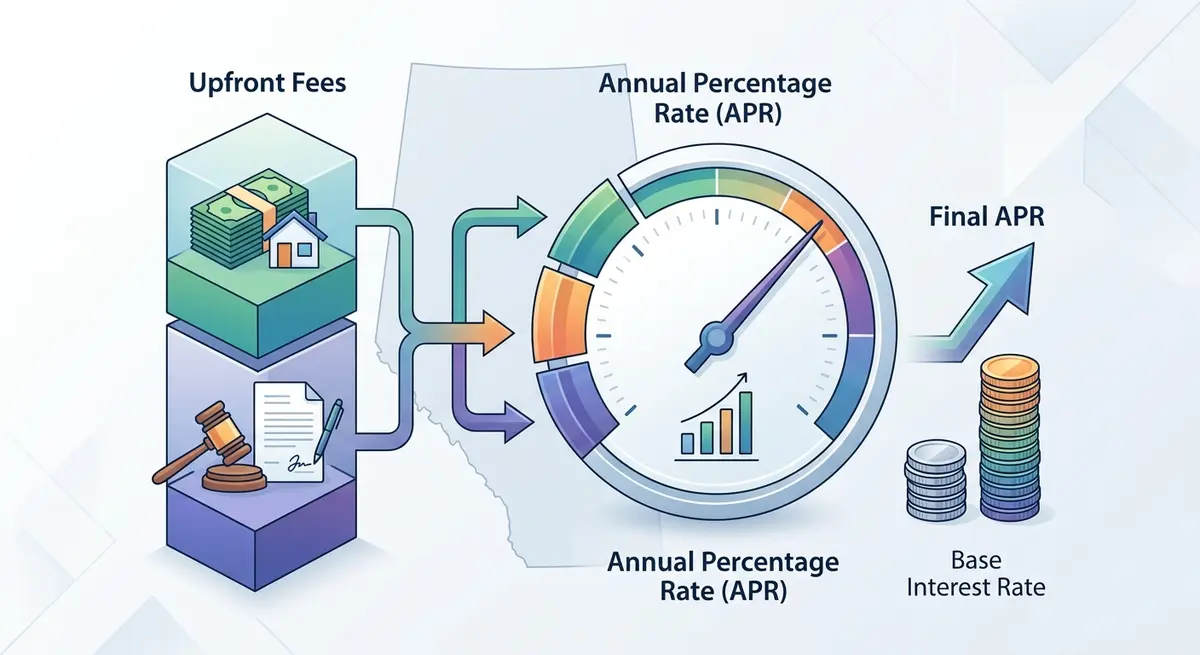

In 2019, and with subsequent updates leading into 2026, the provincial government established a clear boundary to protect consumers. Under provincial law, a credit agreement is officially designated as a high-cost credit product if it carries an Annual Percentage Rate (APR) of 32% or higher. It is absolutely critical to understand that this threshold is based on the APR, not the simple contract interest rate.

As Sarah Jenkins, Senior Policy Analyst at the Canadian Financial Protection Bureau, explains: “The APR is the only true equalizer in lending. A borrower might be offered a 15% interest rate, which sounds reasonable, but once you factor in $10,000 in upfront lender and brokerage fees on a short-term loan, the APR can easily eclipse the 32% legal threshold, triggering strict regulatory oversight.”

How Non-Interest Finance Charges Inflate Your APR

To fully grasp how a standard-looking loan transforms into high-cost credit, you must understand how the APR is calculated. The APR represents the total cost of borrowing expressed as an annual percentage. It legally includes all “non-interest finance charges” that are mandatory to secure the loan.

These non-interest finance charges typically include:

- Brokerage fees: Commissions paid to the mortgage broker arranging the deal.

- Lender setup fees: Administrative costs charged directly by the private lender.

- Legal fees: Costs paid to the lender’s legal representation (though your own independent legal advice is usually separate).

- Appraisal and inspection costs: Any property valuation fees mandated by the lender to approve the funding.

Consider a scenario where you borrow $50,000 on a one-year term with a face interest rate of 15%. If you are required to pay $6,000 in upfront fees, the cost of borrowing skyrockets. When those fees are amortized over a short 12-month period, the effective APR easily surpasses 32%. Understanding this math is crucial, especially when evaluating how compounding frequency silently increases your debt.

The Mandatory 2-Day Disclosure Rule

Transparency is the foundational core of modern consumer protection. Lenders cannot legally hide the true cost of a loan in dense fine print that you only discover after the funds have been dispersed. The Cost of Credit Disclosure Regulation requires all lenders to provide a clear, standardized written disclosure statement.

This document must prominently summarize the “Total Cost of Credit.” This figure is the exact sum of all interest and non-interest charges you will pay over the entire term of the loan, presented in a hard dollar amount rather than just a percentage. Seeing this number is often a wake-up call for borrowers, allowing them to evaluate if the immediate cash infusion is truly worth the long-term financial burden.

By law, you must receive this disclosure statement at least two business days before you incur any obligation to the lender. This mandatory review period ensures you have adequate time to consult with a financial advisor or lawyer. While borrowers can voluntarily waive this timeline in writing to expedite funding, consumer protection advocates strongly advise against doing so unless you have extensive experience in private finance. For more information on standardized disclosures, borrowers can consult the Financial Consumer Agency of Canada (FCAC).

Step-by-Step: How to Review Your High-Cost Credit Agreement

When you receive a disclosure document from a private lender, you must review it methodically. Rushing through this paperwork can lead to devastating financial consequences. Follow these steps to ensure the agreement is compliant and fair:

- Locate the APR: Verify that the Annual Percentage Rate is clearly stated on the first page. If it is missing, the document is non-compliant.

- Check the Total Cost of Credit: Look for the exact dollar amount that represents the total cost of borrowing over the term.

- Itemize the Fees: Review the breakdown of all non-interest finance charges. Ensure there are no unexplained “administrative” or “processing” fees.

- Verify the Term Length: Confirm the exact maturity date of the loan and the conditions for renewal.

- Review Default Penalties: Understand exactly what financial penalties apply if you miss a payment. Alberta law strictly limits these to reasonable cost-recovery amounts.

Properly managing these documents is essential for your financial security. We highly recommend following a structured approach to organizing your mortgage paperwork to ensure you have a clear paper trail if a dispute arises.

Licensing Requirements for Alberta Private Lenders

Not everyone with capital is legally permitted to offer high-cost credit in Alberta. If a business offers, arranges, or provides high-cost credit products, they must hold a valid, active license from Service Alberta. This strict requirement applies equally to the mortgage brokers who arrange these deals and the private lenders who fund them.

According to 2026 data from the Canadian Mortgage and Housing Corporation (CMHC), alternative lending accounts for roughly 12% of the national mortgage market, making regulatory oversight more important than ever. Dealing with a licensed lender ensures that the business is subject to provincial audits and must adhere to strict rules regarding collection practices and advertising.

Marcus Thorne, Director of Compliance at Alternative Lending Canada, notes: “The 2026 regulatory updates have made it virtually impossible for unlicensed entities to legally enforce high-cost debt in Alberta. If a borrower discovers their lender is unlicensed, the courts frequently rule the interest and fees entirely void.”

Your Legal Right to Cancel: The 4-Day Cooling-Off Period

One of the most powerful protections afforded to Alberta borrowers is the statutory right to cancel a high-cost credit agreement. Once you sign the final paperwork, the law provides a mandatory cooling-off period. You have the absolute right to cancel the agreement within four days of signing, without needing to provide any justification to the lender.

If you exercise this right within the four-day window, you must return the principal loan amount, but the lender is legally prohibited from charging you any interest, setup fees, or cancellation penalties. Furthermore, if the lender failed to provide the mandatory disclosures, or if the disclosure statement was missing critical information like the APR, your cancellation rights may extend for months or even up to a year.

Understanding the exact mechanics of this process is vital. For a deep dive into how and when you can exercise this right, read our comprehensive guide on when you can legally rescind a high-interest private mortgage.

Comparing High-Cost Private Mortgages vs. Traditional Bank Loans

It is important to recognize that while consumer protection laws apply to all lenders, the practical reality differs vastly between major banks (A-lenders) and private lending institutions. Banks rarely, if ever, issue high-cost credit. Their interest rates are heavily influenced by the Bank of Canada overnight rate, keeping their APRs well below the 32% threshold.

Private lenders, conversely, take on significantly higher risks by funding clients with poor credit histories or unverifiable income. To offset this risk, their rates and fees are higher. Below is a comparison of how these lending tiers operate in 2026:

| Feature | Traditional Bank (A-Lender) | Standard Private Lender | High-Cost Private Lender |

|---|---|---|---|

| Typical APR | 5% – 8% | 12% – 25% | 32% – 59.9% |

| Special Licensing | Federally Regulated | Standard Provincial License | High-Cost Credit License Required |

| Cooling-Off Period | Standard 2-Day Disclosure | Standard 2-Day Disclosure | Strict 4-Day Cancellation Right |

| Borrower Profile | Excellent Credit, T4 Income | Self-Employed, Minor Credit Issues | Severe Credit Issues, Foreclosure Risk |

Prohibited Practices: What High-Cost Lenders Cannot Do

Alberta’s regulations explicitly outline prohibited behaviors to stop predatory lenders from trapping vulnerable borrowers in endless cycles of debt. One of the most significant prohibitions involves “rollover” fees. A lender cannot legally charge you a fee to refinance or roll over an existing high-cost loan into a new one unless the new agreement significantly changes the terms in your favor.

Additionally, the law strictly limits default charges. If you miss a payment, lenders can only charge reasonable, verifiable costs for the legal steps taken to collect the debt. They cannot invent arbitrary, punitive penalties. For example, charging a $500 “processing fee” for a single missed payment is illegal unless that exact fee reflects actual out-of-pocket costs and was explicitly detailed in the original disclosure statement.

Debt Consolidation and Break-Even Analysis

Many homeowners utilize private mortgages specifically for debt consolidation. While leveraging home equity to pay off high-interest credit cards can be a smart financial maneuver, it requires rigorous mathematical analysis when dealing with high-cost credit. You must ensure the new loan is genuinely cheaper than the debt you are replacing.

If you are consolidating unsecured debt carrying a 19% interest rate, a private mortgage with a 15% face rate might look appealing. However, if upfront fees push the APR to 35%, you are actually losing money. The mandatory disclosure statement is the exact tool you need to calculate your break-even point. By dividing the total upfront fees by your monthly interest savings, you can determine exactly how many months it will take for the consolidation to become profitable. For a broader perspective on this strategy, review our guide on leveraging home equity vs. unsecured credit.

Furthermore, borrowers should actively plan their exit strategy. High-cost credit is designed to be a short-term bridge, not a permanent solution. Implementing aggressive principal reduction strategies is essential to transition back to traditional, lower-cost lending as quickly as possible.

Frequently Asked Questions About Alberta Mortgage Regulations

What is the absolute maximum interest rate a lender can charge in Canada?

Under the Criminal Code of Canada, the maximum legal effective annual rate of interest is 60%. Any rate charged above this threshold is considered criminal usury. However, Alberta’s provincial regulations impose strict licensing and disclosure rules long before that point, specifically targeting any loan with an APR of 32% or higher.

Does the 2-day mandatory review period apply to all mortgages?

Yes, the Cost of Credit Disclosure Regulation requires that a disclosure statement be provided two business days before a borrower incurs any obligation. While this applies to most credit agreements, borrowers can legally waive this timeline in writing if they need immediate emergency funding, though this is generally discouraged.

What should I do if a private lender refuses to show me the APR?

A refusal to disclose the APR is a massive red flag and a direct violation of Alberta’s consumer protection laws. You should immediately halt the transaction and refuse to sign any documents. You can report the unlicensed or non-compliant lender directly to Service Alberta for investigation.

Are mortgage broker fees legally required to be included in the APR?

Yes. Any fee that is mandatory for you to obtain the loan must be included in the APR calculation. This legally includes all broker commissions, lender setup fees, and legal fees paid to the lender’s representation. Excluding these to artificially lower the APR is illegal.

How can I verify if a private lender is properly licensed in Alberta?

Borrowers can easily verify a lender’s legal status by searching the official Service Alberta public registry. You should specifically search the “High-Cost Credit Businesses” database to ensure the lender or brokerage holds a valid, active license for the 2026 calendar year.

How long should I keep my high-cost credit disclosure documents?

You should retain all disclosure statements, contracts, and proof of payments for at least seven years after the loan is fully discharged. For detailed best practices, consult our guide on second mortgage document retention to ensure you are protected against future disputes.

Conclusion

The landscape of private lending offers tremendous opportunities for Alberta homeowners to access trapped equity, consolidate overwhelming debt, and solve immediate financial crises. However, navigating this space requires a significantly higher level of diligence than walking into a traditional bank branch. The consumer protection laws governing high-cost credit are powerful tools designed to ensure transparency, but they only protect you if you actively engage with them. Always insist on receiving your disclosure statement early, meticulously verify the APR, and never let a lender pressure you into waiving your statutory cooling-off periods.

Knowledge is your ultimate defense against predatory lending. By understanding the 32% APR threshold and your legal rights under the Consumer Protection Act, you can secure the funding you need while keeping your long-term financial health intact. If you are looking for transparent, compliant, and fair financing options, our expert team is here to guide you through every line of the agreement. Contact our team today for a secure, no-obligation consultation.