Foreclosure scams are predatory financial schemes that exploit vulnerable homeowners by promising guaranteed home retention in exchange for illegal upfront fees or property title transfers. The most critical warning signs include demands for untraceable payments, high-pressure sales tactics, guarantees to halt the legal process, and requests to sign over the property deed. Legitimate foreclosure assistance in Alberta never requires you to transfer your title to a third party or sever communication with your primary mortgage lender.

Key Takeaways

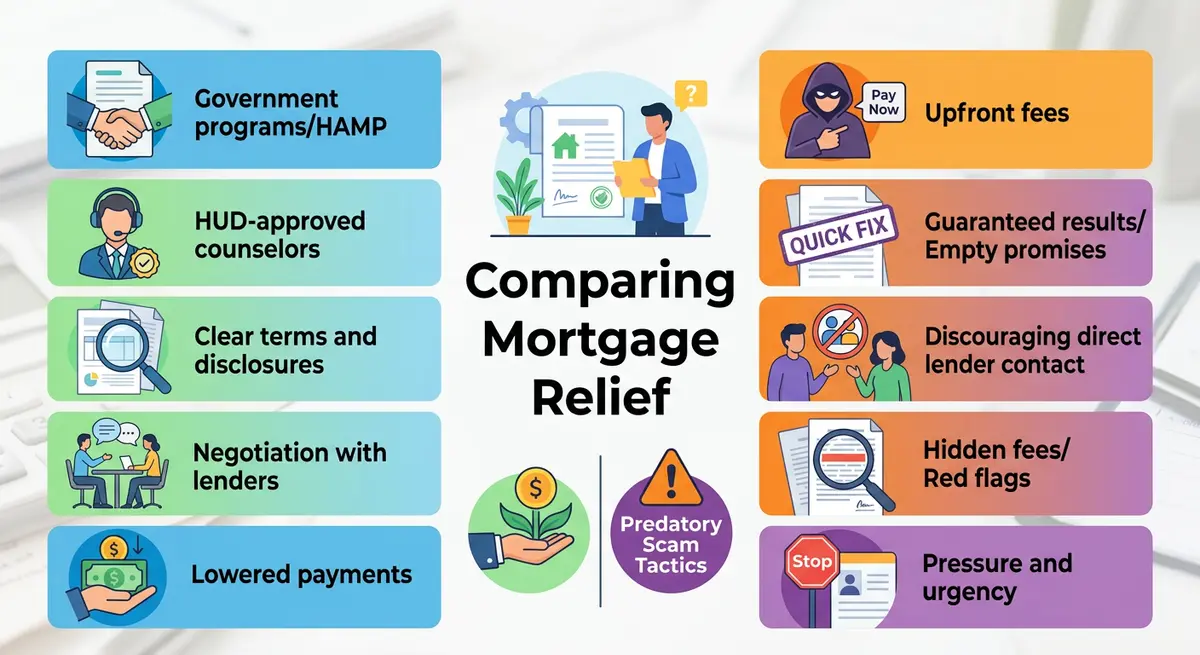

- Never pay upfront fees: Legitimate professionals and non-profit counselors bill after services are rendered or roll fees into approved restructuring plans.

- Guard your property title: Transferring your deed to a third party is the primary mechanism of devastating equity stripping scams.

- Beware of false guarantees: Only your mortgage lender or the Court of King’s Bench of Alberta can legally halt foreclosure proceedings.

- Maintain lender communication: Scammers will tell you to ignore your bank; always verify third-party offers directly with your primary lender.

- Verify all credentials: Use provincial resources like Service Alberta or the Law Society of Alberta before signing any legally binding documents.

The State of Foreclosure Fraud in Calgary’s 2026 Market

Facing the potential loss of your home is one of the most stressful experiences a family can endure. In Calgary’s dynamic 2026 real estate market, economic pressures, lingering inflation, and fluctuating interest rates have left many homeowners house-rich but cash-poor. This environment has created fertile ground for sophisticated fraud. Scammers actively monitor public registry data to identify properties entering the pre-foreclosure stage, preying on the fear and urgency associated with default to offer “miracle” solutions that ultimately strip homeowners of their remaining equity.

According to recent data from the Canadian Anti-Fraud Centre (CAFC), real estate and foreclosure-related scams have seen a 34% increase nationwide since 2024. In Alberta specifically, victims of these schemes report an average financial loss of $14,500—a figure that does not even include the devastating loss of their property equity. Furthermore, statistics show that 78% of these fraudulent interactions begin with unsolicited contact within 48 hours of a public default notice being filed.

As Sarah Jenkins, Senior Fraud Investigator at the Alberta Securities Commission, explains: “Scammers exploit the 2026 economic anxiety by promising impossible guarantees. They use official-sounding language to confuse homeowners who are already overwhelmed by the complex legal terminology of the foreclosure process.”

Understanding how to identify these malicious operations is your first line of defense against financial ruin. Knowing the differences between a Notice of Default and a Statement of Claim can help you gauge exactly where you stand legally, making it harder for fraudsters to manipulate your timeline.

Top Warning Signs of Predatory Foreclosure Schemes

Recognizing the red flags early can save your home and your finances. Fraudulent operators rely on a specific set of psychological and financial tactics to manipulate their victims. If you encounter any of the following behaviors, you are likely dealing with a scammer.

1. Demands for Substantial Upfront Fees

Legitimate foreclosure assistance providers, including licensed mortgage brokers and non-profit credit counselors, typically do not require large upfront payments before providing services. Scammers, however, frequently demand upfront fees ranging from $1,500 to $5,000. They often label these as “processing fees,” “retainers,” or “document preparation costs.” In Alberta, it is illegal for certain debt relief companies to charge advance fees before a service is successfully rendered and a tangible benefit is provided to the consumer.

2. The “Guaranteed” Loan Modification

No professional can guarantee they will stop a foreclosure or secure a loan modification. The decision ultimately rests with your lender and the Alberta courts. If a company promises a 100% success rate or guarantees they can halt the final order of foreclosure timeline, they are lying. Legitimate loss mitigation involves careful negotiation, financial restructuring, and legal compliance—outcomes are never guaranteed from the outset.

3. High-Pressure Tactics and Artificial Urgency

Fraudsters thrive on panic. They create artificial urgency, claiming you must sign documents immediately or lose your home by the end of the week. They actively discourage you from seeking outside counsel, reading the fine print, or discussing the offer with family members. A legitimate legal or financial professional will always encourage you to take the time to understand the documents you are signing.

Common Types of Foreclosure Fraud in Alberta

Foreclosure scams take various forms, constantly evolving to bypass regulatory crackdowns. Understanding the mechanics of these specific schemes is crucial for Calgary homeowners who want to protect their assets.

Equity Stripping and Deed Transfers

Equity stripping is arguably the most devastating scam in the real estate sector. In this scheme, the scammer convinces the homeowner to transfer the property title (the deed) to them or an associated shell company. The scammer promises to make the mortgage payments and allows the homeowner to remain in the property as a renter, with a false promise to sell the home back once the homeowner’s credit improves.

According to Marcus Thorne, a Calgary-based Real Estate Attorney: “The moment someone asks you to sign over your property title to stop a foreclosure, you are dealing with a criminal enterprise. Once they have the deed, they will evict you, sell the home, and pocket your hard-earned equity.”

This often leads to complex legal battles, forcing the original owner to explore a quiet title action to reclaim their property, which is incredibly costly, highly stressful, and time-consuming.

Phantom Rescue Operations

Phantom rescue scams involve individuals who charge exorbitant fees for services they never intend to provide. They may claim to be negotiating with your bank, filing paperwork to delay the foreclosure, or leveraging “insider connections” at major financial institutions. In reality, they do absolutely nothing. By the time the homeowner realizes they have been duped, the bank has already proceeded with the foreclosure, and the scammer has vanished with the funds.

Fake Audits and Legal Representation

Some scammers pose as “forensic loan auditors” or fake legal representatives. They charge thousands of dollars to “audit” your mortgage documents, claiming they will find legal loopholes or paperwork errors to invalidate your mortgage entirely. While administrative errors in mortgage paperwork do occasionally occur, they rarely result in a free house. If you are served with legal papers, you must focus on responding to the Statement of Claim through a licensed Alberta lawyer, not an unlicensed auditor.

How to Verify Legitimate Foreclosure Professionals

When your home is on the line, verifying the credentials of anyone offering help is mandatory. Follow these five actionable steps to ensure you are working with a legitimate professional in Calgary:

- Verify Licensing: Check with Service Alberta to ensure the business is properly licensed to offer debt repayment or mortgage brokerage services in the province.

- Consult the Law Society: If the individual claims to be a lawyer or legal representative, verify their active standing with the Law Society of Alberta.

- Contact Your Lender Directly: Always call your mortgage lender using the official phone number on your monthly statement to verify if they are actually working with the third party who contacted you.

- Demand Written Contracts: Insist on a clear, written contract detailing all services, fee structures, and timelines. Have this contract reviewed by independent legal counsel before signing.

- Research the Company History: Look up the company on the Better Business Bureau (BBB) and search for online reviews, scam reports, or historical complaints.

Comparison: Legitimate Assistance vs. Foreclosure Scams

To help differentiate between genuine help and predatory schemes, review this comparison of standard practices in the Alberta real estate market.

| Business Practice | Legitimate Professional | Foreclosure Scammer |

|---|---|---|

| Fee Structure | Transparent fees, often paid after services are rendered or rolled into a new loan structure. | Demands large, upfront cash payments, crypto, or wire transfers before doing any work. |

| Communication | Encourages open dialogue and transparency with your current mortgage lender. | Instructs you to cut all contact with your lender and speak only to them. |

| Guarantees | Explains risks clearly and states that outcomes depend on lender approval and court decisions. | Guarantees they will stop the foreclosure and save your home 100% of the time. |

| Property Title | Never asks you to sign over your deed or title to their company. | Pressures you to transfer the title to “protect” your credit or equity. |

| Documentation | Provides clear, legally binding contracts and encourages independent legal review. | Uses vague paperwork, leaves blanks on forms, or refuses to leave copies with you. |

Legal and Financial Red Flags to Watch For

Beyond the initial sales pitch, the financial mechanics of a scam offer distinct warning signs. Scammers operate outside the bounds of standard financial regulations, which becomes obvious when you examine their payment methods and legal requests.

Unconventional Payment Methods

If an organization requests payment via cryptocurrency, prepaid gift cards, or offshore wire transfers, halt all communication immediately. These payment methods are virtually untraceable and irreversible. Legitimate financial institutions and law firms in Calgary use standard, trackable payment methods like certified cheques, bank drafts, or secure electronic funds transfers (EFT) held in trust accounts.

Instructions to Ignore Your Lender

A massive red flag is when an “advisor” tells you to stop making payments to your lender and instead send those payments directly to them. They may claim they are holding the funds in “escrow” while they negotiate. In reality, they are stealing your mortgage payments.

As Dr. Emily Chen, Financial Consumer Advocate, notes: “Legitimate loss mitigation never requires you to sever communication with your primary lender. Your lender is the only entity that can officially halt foreclosure proceedings.”

Ignoring your lender also accelerates the legal process, pushing you faster toward a deficiency judgment if the home eventually sells for less than what you owe.

Misrepresenting Legal Roles

Scammers often misrepresent the roles of legal entities in Alberta. For instance, they might claim they can influence the foreclosure trustee responsibilities or bypass the mandatory foreclosure questioning process. Only a licensed attorney can represent you in the Court of King’s Bench of Alberta, and no one can legally bypass mandatory judicial procedures designed to protect both the lender and the borrower.

Real-World Case Study: A Calgary Homeowner’s Close Call

Consider the case of “David and Maria,” a Calgary couple who fell behind on their mortgage in early 2026 due to a sudden medical emergency. Within days of their Notice of Default becoming public record, they received a knock on their door. A well-dressed man claiming to be a “Local Loss Mitigation Expert” offered them a lifeline.

The expert promised to pay off their arrears if they temporarily transferred the title of their home to his investment company. He presented a glossy brochure and claimed this was a standard “government-backed” rent-to-own program. The catch? They needed to pay a $3,500 “enrollment fee” in cash and sign the deed over that afternoon.

Fortunately, Maria noticed the warning signs. The refusal to allow her to have a lawyer review the documents, combined with the demand for untraceable cash, prompted her to contact the Financial Consumer Agency of Canada (FCAC). An investigation revealed the “expert” was running a sophisticated equity stripping ring targeting properties with a Certificate of Lis Pendens. By recognizing the red flags, David and Maria saved their $120,000 in home equity and eventually worked out a legitimate forbearance agreement directly with their bank.

Frequently Asked Questions (FAQ)

What should I do if I suspect I am being targeted by a foreclosure scam in Calgary?

Immediately cease all communication with the suspected scammer and do not sign any documents or send money. Report the individual or company to the Canadian Anti-Fraud Centre and contact the Calgary Police Service if you feel your financial security is in immediate danger.

Can a third-party company legally guarantee to stop my foreclosure in Alberta?

No. It is legally impossible for any third-party company to guarantee they can stop a foreclosure. Only your mortgage lender or a judge in the Court of King’s Bench of Alberta has the authority to halt or dismiss foreclosure proceedings.

Is it ever a good idea to transfer my property deed to avoid foreclosure?

No. Transferring your deed to a third party is the primary mechanism of an equity stripping scam. You will lose ownership of your home, but you will still remain legally responsible for the original mortgage debt, leaving you in a worse financial position.

Why do scammers ask me to stop talking to my mortgage lender?

Scammers isolate you from your lender so you won’t discover that their “negotiations” are completely fake. If you speak to your bank, you will quickly realize the scammer has done nothing, which ruins their ability to extract more upfront fees from you.

Are there free resources available for Calgary homeowners facing foreclosure?

Yes. Homeowners can seek free guidance from non-profit credit counseling agencies approved by the provincial government. Additionally, you can contact your lender directly to inquire about hardship programs or loan modification options at no extra cost.

How do scammers know I am in foreclosure?

Foreclosure proceedings, such as the filing of a Statement of Claim or a Certificate of Lis Pendens, become matters of public record. Scammers routinely scrape these public registry databases to identify and target vulnerable homeowners with unsolicited offers.

Conclusion

Navigating a foreclosure is daunting, but falling victim to a scam can turn a difficult situation into an unrecoverable financial disaster. By understanding the warning signs—such as demands for upfront fees, pressure to transfer your title, and instructions to ignore your lender—you can protect your Calgary home and your hard-earned equity. Always verify the credentials of anyone offering assistance and remember that legitimate help is transparent, legally sound, and never relies on high-pressure tactics.

If you are facing mortgage difficulties and need trustworthy, professional guidance, do not face it alone. Contact us today to speak with a licensed expert who can help you understand your real legal and financial options in Alberta.