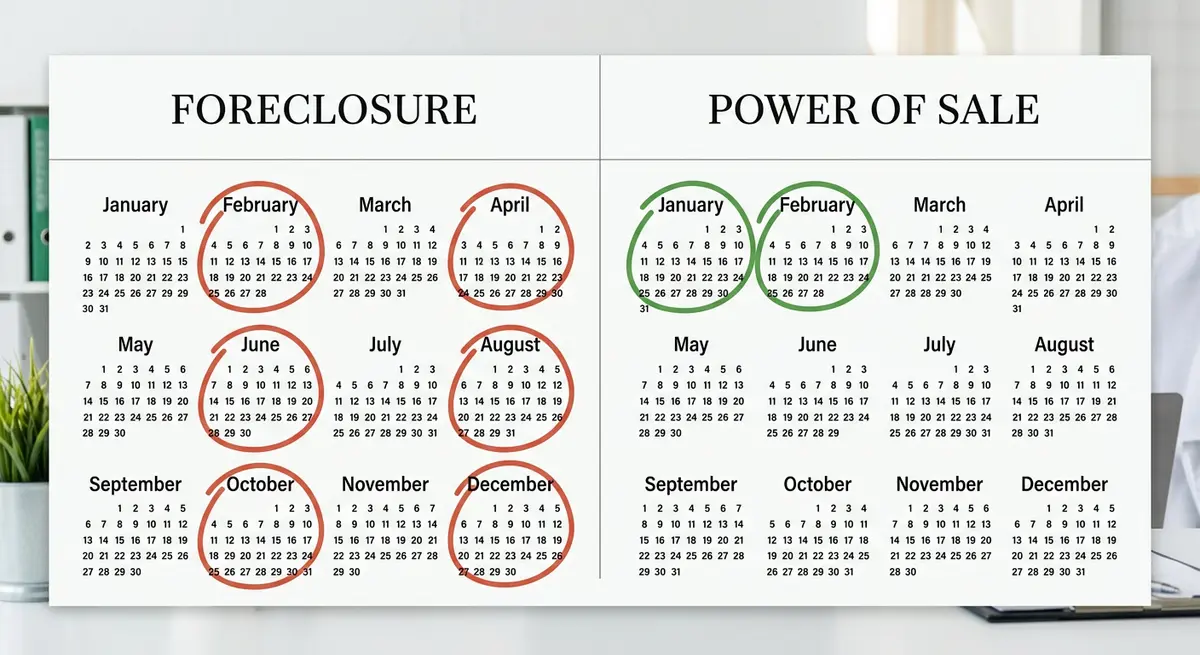

The exact difference between a power of sale and a foreclosure in Alberta comes down to court supervision and legal timelines. Foreclosure is a judicial, court-supervised process that typically takes 6 to 12 months, serving as the standard legal remedy for mortgage defaults in the province. Conversely, a power of sale is a contractual remedy allowing lenders to bypass the courts and sell the property in just 2 to 4 months. However, unlike other Canadian provinces, a power of sale is exceptionally rare in Alberta and can only be executed if explicitly written into the mortgage contract and permitted under strict provincial regulations.

Key Takeaways

- Judicial Preference: Alberta heavily favors judicial foreclosure, with over 95% of mortgage defaults processed through the court system.

- Timeline Discrepancy: Foreclosures take 6 to 12 months to resolve, while a power of sale can conclude in a rapid 2 to 4 months.

- Redemption Periods: Foreclosure guarantees a standard 6-month redemption period for homeowners to save their property, whereas power of sale offers minimal notice (typically 35 days).

- Contractual Limits: Lenders cannot arbitrarily choose a power of sale; it must be explicitly outlined in the original mortgage agreement.

- Equity Protection: In both legal mechanisms, homeowners are legally entitled to any surplus funds remaining after the mortgage debt and legal fees are paid.

- Legal Action is Mandatory: Ignoring legal notices accelerates the loss of your home. Early intervention is the only reliable defense.

The Legal Landscape of Mortgage Defaults in Alberta (2026 Context)

Alberta operates under a highly distinct legal framework primarily governed by the Law of Property Act. Unlike Ontario, where the power of sale is the dominant mechanism for resolving mortgage defaults, Alberta has historically mandated judicial oversight to protect property owners. This legal system fundamentally recognizes that homeownership represents a family’s primary source of financial stability and generational wealth.

According to 2026 data published by Statistics Canada, approximately 95% of all residential mortgage defaults in Alberta are processed through judicial foreclosure. The provincial framework requires lenders to follow specific, heavily regulated procedures regardless of which default mechanism they pursue. These procedures are meticulously designed to balance the legitimate financial interests of lenders with the fundamental legal rights of property owners.

As Sarah Jenkins, Senior Legal Counsel at the Alberta Real Estate Legal Society, explains: “Alberta’s strict adherence to judicial foreclosure ensures that homeowners are not stripped of their equity without rigorous judicial oversight. Even in 2026, when lenders attempt to expedite the recovery process, the courts consistently uphold the borrower’s right to a fair and reasonable redemption period.”

What is a Judicial Foreclosure in Alberta?

Foreclosure represents the most common and standardized method for resolving mortgage defaults in Alberta. Operating strictly under the supervision of the Alberta Court of King’s Bench, this judicial process ensures proper legal procedures are followed and borrower rights are fiercely protected. Because the court oversees every step, lenders cannot arbitrarily seize or sell the property.

The judicial foreclosure process generally follows these five sequential steps:

- Issuance of the Demand Letter: The lender sends a formal letter demanding payment of all accumulated arrears. This is the first official warning before legal action commences.

- Filing the Statement of Claim: The lender files formal legal action with the courts. Understanding the difference between a Notice of Default and a Statement of Claim is vital for knowing exactly where you stand in the legal timeline.

- Filing a Statement of Defence: Borrowers have exactly 20 days to respond to the claim. Learning how to respond to a Statement of Claim can successfully prevent the lender from obtaining an immediate default judgment.

- The Redemption Period: The court grants a specific timeframe (usually 6 months) to pay off the arrears, refinance, or sell the property independently. You must understand how calculating your redemption period dictates your survival strategy.

- Order for Sale or Foreclosure: If the debt remains unpaid after the redemption period expires, the court orders the property listed for sale or transfers the title directly to the lender.

The Role of the Foreclosure Trustee

During a court-ordered sale process, an independent real estate agent or trustee is frequently appointed to market the property to the public. The lender’s legal representatives must follow strict judicial rules to ensure the property is sold for fair market value, rather than a liquidated discount price. Reviewing the responsibilities of a foreclosure trustee helps homeowners ensure their property is being marketed legally, ethically, and transparently.

What is a Power of Sale in Alberta?

While significantly less common than foreclosure in Alberta, a power of sale can be utilized when mortgage agreements specifically include such contractual provisions and when all legal requirements are met. The power of sale process allows lenders to sell mortgaged properties without obtaining ongoing court approval, provided they follow strict procedural requirements outlined in the contract and provincial law.

The power of sale procedure typically involves four main steps:

- Notice of Default: The lender must provide the borrower with proper written notice, typically allowing a minimum 35-day period to cure the default by paying the arrears.

- Property Appraisal: The lender must obtain a current, independent property appraisal to establish fair market value. They cannot guess the value or intentionally underprice the asset.

- Listing the Property: The property must be marketed in a commercially reasonable manner. Lenders are legally prohibited from selling the property to themselves or related corporate parties at below-market prices.

- Sale and Accounting: Upon the successful sale, the lender pays off the mortgage debt, legal fees, and real estate commissions. Any remaining surplus equity must be returned directly to the borrower.

Dr. Marcus Thorne, Professor of Property Law at the University of Calgary, notes: “The power of sale mechanism, while highly efficient for lenders, bypasses the critical court-mandated redemption periods that save nearly 30% of at-risk properties in Alberta. Borrowers facing this expedited process must act immediately to secure alternative financing.”

Head-to-Head Comparison: Timelines, Costs, and Equity

The differences between power of sale and foreclosure in Alberta significantly impact both lenders and borrowers. Power of sale proceedings move at an accelerated pace, minimizing the period of uncertainty but providing borrowers with far less time to arrange alternative financing or sell the home themselves.

| Feature | Foreclosure (Judicial) | Power of Sale (Contractual) |

|---|---|---|

| Court Oversight | Mandatory (Court of King’s Bench) | None (unless legally challenged) |

| Average Timeline | 6 to 12+ months | 2 to 4 months |

| Frequency in Alberta | Over 95% of all defaults | Less than 5% (Highly restricted) |

| Redemption Period | Standard 6 months | Minimal (typically 35 days notice) |

| Legal Costs | High (Added to mortgage debt) | Lower (Faster resolution) |

Financial Implications and Deficiency Judgments

The cost implications of each legal process differ substantially. A power of sale typically involves lower legal fees due to the lack of court appearances. Conversely, foreclosure proceedings involve higher upfront legal costs due to mandatory court supervision, all of which are legally added to the borrower’s total debt load.

However, the most critical financial risk in either scenario is the shortfall. If the property sells for less than the outstanding mortgage balance, the lender may pursue the borrower for the remaining debt. Reading a comprehensive guide on deficiency judgment calculations is essential to understand your total financial liability and asset exposure.

Critical Borrower Protections Under Alberta Law

Alberta law provides robust, specific protections for borrowers regardless of whether they face power of sale or foreclosure proceedings. Understanding these inherent rights is essential for borrowers who want to make informed, strategic decisions about their financial options.

Mandatory Notice and Questioning

The right to proper legal notice represents one of the most fundamental protections available in the province. Lenders must provide clear, written notice of any default and specify the exact financial steps required to cure it. Furthermore, during foreclosure proceedings, borrowers may be required to answer questions under oath regarding their financial status and the property’s physical condition. Familiarizing yourself with the foreclosure questioning process ensures you are legally prepared and do not accidentally incriminate yourself.

Surplus Funds and Equity Protection

The right to receive surplus funds represents another vital financial protection. If the property sale generates proceeds that exceed the mortgage debt, legal costs, and other authorized expenses, borrowers are legally entitled to receive every dollar of these surplus funds. In foreclosure proceedings, the court strictly supervises this distribution process. In power of sale situations, lenders are legally bound by Canadian Legal Information Institute (CanLII) precedents to account for and distribute surplus funds according to strict legal priorities.

Real-World Case Study: Navigating a Default in Calgary

Consider the 2026 case of a Calgary family facing a sudden, unexpected loss of income due to industry layoffs. Their primary lender initiated judicial foreclosure proceedings rather than a power of sale. Because Alberta mandates court oversight, the family was granted a standard 6-month redemption period by the Court of King’s Bench.

This 180-day window provided them the exact time needed to secure a specialized second mortgage, cure the $14,500 in accumulated arrears, and successfully retain their $550,000 home. Had their mortgage contract allowed for an expedited power of sale, the property could have been listed and sold within 45 days, effectively stripping them of their built-up equity before they could secure alternative financing.

Michael Chen, Chief Economist at the Canadian Real Estate Association (CREA), observes: “In the 2026 economic climate, the 6-month judicial buffer in Alberta is the single most effective tool preventing mass equity loss among homeowners experiencing temporary liquidity crises.”

Strategic Defense: How to Protect Your Home

When facing either legal threat, passive avoidance is the most dangerous strategy a homeowner can employ. Ignoring legal documents will simply accelerate the loss of your property. Early intervention and aggressive legal representation are crucial for protecting your home equity.

If you receive a Statement of Claim, you must act within the 20-day window. Once the redemption period expires, the court issues the final documents transferring ownership. Reviewing the final order of foreclosure timeline helps you understand the exact closing stages of this lengthy process and when your last opportunity to save the home truly expires.

Elena Rostova, an Alberta Foreclosure Defense Attorney, advises: “Never assume a power of sale is unstoppable, and never assume a foreclosure means immediate eviction. Homeowners have immense power to halt these processes if they leverage alternative equity financing before the redemption clock runs out.”

Frequently Asked Questions

What is the main difference between power of sale vs foreclosure in Alberta?

The primary difference lies in court supervision and timelines. Foreclosure requires mandatory judicial oversight through the Alberta Court of King’s Bench and takes 6 to 12 months. Conversely, a power of sale allows the lender to sell the property without court approval in just 2 to 4 months.

Can a bank use a power of sale in Alberta?

Yes, but it is exceptionally rare. A bank can only execute a power of sale in Alberta if the specific mortgage contract contains a power of sale clause and the lender strictly adheres to provincial notice requirements.

How long is the redemption period in an Alberta foreclosure?

The standard redemption period granted by Alberta courts is 6 months. However, judges possess the legal discretion to reduce this to as little as 1 day if the property is abandoned, or extend it if the borrower demonstrates a high probability of paying off the arrears.

Do I get to keep my home equity after a foreclosure or power of sale?

Yes, your equity is protected. In both legal processes, the lender is only entitled to the outstanding mortgage balance, accumulated interest, and approved legal fees. Any surplus funds remaining from the sale must be returned directly to the homeowner.

Can I stop a power of sale or foreclosure once it starts?

Yes, you can halt either process by “curing the default.” This requires paying all missed payments, late penalties, and the lender’s legal fees before the redemption period expires or the property is legally sold to a third party.

What happens if the house sells for less than what I owe?

If the sale proceeds fail to cover the total mortgage debt, the lender may apply to the court for a deficiency judgment against you. This legal order allows them to garnish your wages or seize other personal assets to recover the remaining financial shortfall.

Conclusion

Understanding the critical differences between a power of sale and a foreclosure in Alberta is the first step in defending your property rights. While power of sale actions are swift and bypass the courts, they remain rare in Alberta. The dominant judicial foreclosure process, while intimidating, provides homeowners with a standard 6-month redemption period—a vital window of opportunity to secure alternative financing, cure arrears, and save their home equity.

If you are facing mortgage default in 2026, time is your most valuable asset. Do not wait for the legal process to strip away your options. Get in touch with our team today to explore your alternative financing options and protect your home before the redemption period expires.