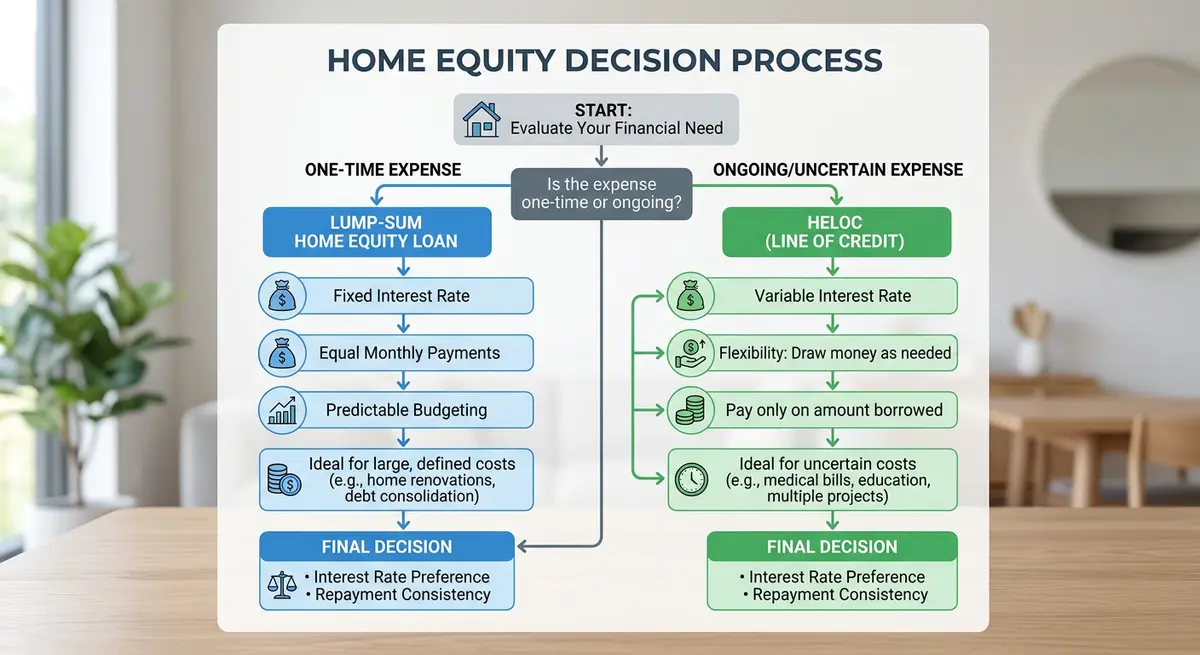

A Home Equity Line of Credit (HELOC) provides revolving, flexible access to funds with variable interest rates, while a second mortgage delivers a one-time lump sum with fixed repayment terms. Both financial instruments allow Calgary homeowners to borrow against their property’s built-up equity without altering their primary mortgage, but they serve entirely different financial strategies. Choosing the wrong product can lead to unnecessary interest costs or restricted cash flow, making it critical to align your loan structure with your specific capital requirements.

Key Takeaways

- HELOCs function like high-limit credit cards secured by your home, ideal for ongoing, unpredictable expenses.

- Second mortgages provide a single lump-sum disbursement, making them perfect for fixed-cost projects or debt consolidation.

- Canadian lending guidelines in 2026 permit homeowners to borrow up to 80% of their property’s appraised value across all mortgages combined.

- Interest rates on HELOCs are typically variable and tied to the prime rate, whereas second mortgages usually offer fixed rates for predictable budgeting.

- Both options place a subordinate lien on your property, meaning failure to maintain payments can trigger foreclosure proceedings.

- Qualifying for either product requires passing the federal mortgage stress test, proving you can afford payments at a rate 2% higher than your contract rate.

Understanding Home Equity in Calgary’s 2026 Market

Calgary’s real estate landscape has evolved significantly, and local homeowners collectively hold over $1.2 billion in untapped home equity. This wealth accumulation happens silently as you pay down your principal balance and as neighborhood property values appreciate. According to recent data from Statistics Canada, the average Canadian homeowner has seen their equity position strengthen, providing a robust financial safety net.

Equity is simply the current market value of your home minus any outstanding loan balances. For example, if your property in Evanston is appraised at $600,000 and your primary mortgage balance is $350,000, you possess $250,000 in raw equity. However, lenders will not let you access 100% of this amount. Regulatory frameworks cap total borrowing at 80% of the home’s value, known as the Loan-to-Value (LTV) ratio. In this scenario, your maximum allowable debt is $480,000, leaving you with $130,000 in accessible capital.

As Marcus Thorne, a Senior Financial Analyst at the Alberta Lending Institute, explains: “Home equity is the most powerful wealth-building tool available to the middle class. But extracting it requires strategic foresight. Treating your home like an ATM without a clear repayment plan is a recipe for financial disaster.”

What is a Home Equity Line of Credit (HELOC)?

A HELOC is a revolving credit facility secured by your property. Investopedia defines a HELOC as a line of credit that allows you to borrow, repay, and borrow again up to a predetermined limit. It operates in two distinct phases: the draw period and the repayment period.

During the draw period, which typically lasts 10 years, you can access funds at your discretion. You are only required to make minimum monthly payments covering the accrued interest on the amount you have actually withdrawn, not the total available limit. This makes HELOCs incredibly flexible for managing cash flow during long-term projects, such as a multi-phase home renovation or funding a child’s university education over four years.

However, this flexibility comes with variable interest rates. HELOC rates are directly tied to the Bank of Canada prime lending rate. If the central bank raises rates to combat inflation, your monthly interest obligations will increase immediately. Once the draw period ends, the HELOC enters the repayment phase (usually 20 years), where you can no longer access funds and must begin paying down both principal and interest.

How Do Second Mortgages Work?

Unlike the revolving nature of a credit line, a second mortgage is a closed-end loan. It provides a one-time, lump-sum disbursement of funds upfront. Because it is registered as a subordinate lien behind your primary mortgage, the lender takes on slightly more risk; if the property is sold or foreclosed upon, the primary lender is paid first. Consequently, interest rates on these products are generally higher than primary mortgage rates but significantly lower than unsecured personal loans or credit cards.

The defining characteristic of this loan type is its predictability. You receive the full amount immediately, and your repayment schedule is fixed from day one. Every monthly payment includes both principal and interest, ensuring that the debt is systematically eliminated over the amortization period. This structure is highly advantageous for borrowers who need a specific amount of money for a defined purpose and want the security of knowing exactly what their monthly obligations will be.

For homeowners looking to aggressively pay down their debt, understanding principal reduction strategies is crucial when managing a fixed-term loan, as early repayment can sometimes trigger prepayment penalties depending on the lender’s terms.

Head-to-Head Comparison: HELOC vs. Fixed-Sum Loans

To make an informed decision, you must evaluate how these two products stack up against each other across several critical financial metrics. The table below outlines the primary distinctions.

| Feature | Home Equity Line of Credit (HELOC) | Second Mortgage |

|---|---|---|

| Disbursement | Revolving access; draw funds as needed | Single lump-sum payment upfront |

| Interest Rate | Variable (fluctuates with prime rate) | Typically fixed for the term |

| Repayment Structure | Interest-only during draw period | Principal + interest from day one |

| Best Used For | Ongoing expenses, emergency funds | Debt consolidation, single large purchases |

| Prepayment Penalties | Rarely applicable; pay down anytime | Often apply if paid off before term ends |

Step-by-Step: How to Choose the Right Equity Product

Selecting the optimal financing route requires a systematic evaluation of your financial health and project goals. Follow these steps to determine which product aligns with your 2026 objectives:

- Calculate Your Available Equity: Determine your home’s current market value and multiply it by 0.80. Subtract your current mortgage balance from that number. This is your maximum borrowing ceiling.

- Define the Project Scope: Are you building a basement suite where contractor costs might fluctuate over six months? A HELOC is likely better. Are you paying off $40,000 in credit card debt today? A fixed lump-sum loan is the superior choice.

- Assess Your Risk Tolerance: Can your monthly budget absorb a sudden $200 increase if the Bank of Canada raises interest rates? If not, prioritize fixed-rate products.

- Review Your Credit Profile: Lenders reserve the best HELOC rates for borrowers with excellent credit (typically 720+). If your score is lower, you might find better approval odds with specialized lump-sum lenders.

- Gather Required Documentation: Prepare your T4s, recent pay stubs, property tax assessments, and existing mortgage statements. Having a complete document checklist ready accelerates the approval process.

Qualification Criteria and the 2026 Stress Test

Accessing your property’s value is not automatic; lenders rigorously evaluate your ability to repay the new debt alongside your existing obligations. The most significant hurdle for Canadian borrowers is the federal mortgage stress test, mandated by the Financial Consumer Agency of Canada (FCAC).

To qualify for a HELOC from a federally regulated institution, you must prove you can afford the payments at a qualifying rate that is typically 2% higher than your contracted rate, or the benchmark rate of 5.25%—whichever is higher. This safety buffer ensures that borrowers will not default if market conditions tighten.

Beyond the stress test, lenders scrutinize your Debt Service Ratios (Gross Debt Service and Total Debt Service). Generally, your total monthly debt obligations should not exceed 42% to 44% of your gross monthly income. For self-employed Calgarians who write off significant expenses, traditional income verification can be challenging. In these cases, exploring stated income options through alternative lenders can provide a viable pathway to approval, though often at a slight premium on the interest rate.

Strategic Uses for Your Property’s Hidden Value

When deployed responsibly, property-backed financing acts as a financial springboard. The cost of borrowing against your home is substantially lower than unsecured debt, making it an attractive option for several strategic applications.

High-Interest Debt Consolidation

Calgarians carrying balances on credit cards charging 19.99% to 29.99% interest are losing thousands of dollars annually to compounding interest. By using a fixed-sum equity loan to pay off these balances, you can consolidate multiple payments into one manageable monthly obligation at a fraction of the interest rate. When leveraging home equity versus unsecured credit, the monthly cash flow savings can be life-changing, provided you do not rack up new credit card debt afterward.

Value-Add Property Renovations

Using equity to improve your property creates a cyclical benefit: you borrow against the home to increase its ultimate resale value. Kitchen remodels, secondary basement suites, and energy-efficient upgrades often yield high returns on investment. Because renovation costs frequently overrun initial estimates, a HELOC’s revolving nature allows you to draw extra funds only if necessary, preventing you from paying interest on borrowed money sitting idle in a bank account.

Business and Investment Financing

Entrepreneurs often struggle to secure traditional business loans without extensive operating histories. Tapping into residential equity provides immediate capital for inventory, equipment, or expansion. However, business owners must carefully weigh the risks of tying their primary residence to their commercial ventures.

Risks, Edge Cases, and Protecting Your Home

While the benefits are substantial, secured lending carries inherent risks that demand respect. The most critical factor is that your home serves as collateral. If you experience a severe income disruption and default on your payments, the lender possesses the legal right to initiate foreclosure proceedings to recover their funds.

Borrowers must also be hyper-aware of how interest accrues. With a HELOC, making only the minimum interest payments for a decade means your principal balance remains untouched. When the repayment period eventually triggers, the sudden requirement to pay principal plus interest can cause severe payment shock. Understanding how compounding frequency impacts your total debt load is essential for long-term financial health.

Furthermore, life events can complicate equity loans. For instance, if you require a co-signer to qualify, you must understand the legal implications. Using a parent to secure your loan means their credit score and financial assets are equally on the line if you default. Always have a contingency plan, such as a three-month emergency fund, to cover dual mortgage payments in case of job loss or medical emergencies.

Frequently Asked Questions (FAQ)

Can I convert my HELOC into a fixed-rate second mortgage later?

Yes, many financial institutions allow you to lock in a portion or all of your outstanding HELOC balance into a fixed-rate term. This is an excellent strategy if you anticipate rising interest rates or want the predictability of fixed monthly payments. Always check with your lender about potential conversion fees.

Does a low credit score disqualify me from getting a HELOC in Calgary?

Traditional banks typically require a credit score of 680 or higher for a HELOC. If your score is lower, you may be disqualified from prime revolving credit products, but alternative lenders might still approve you for a fixed-sum second mortgage based primarily on your available equity rather than just your credit history.

How does a cash-out refinance differ from these options?

A cash-out refinance replaces your entire existing primary mortgage with a brand new, larger loan, giving you the difference in cash. In contrast, HELOCs and second mortgages leave your original mortgage untouched. Comparing cash-out refinancing to secondary liens is crucial, especially if your current primary mortgage has a very low, locked-in interest rate you don’t want to lose.

Are there restrictions on how I can spend the funds?

Generally, lenders do not restrict how you use the capital extracted from your home equity. Whether you use it for debt consolidation, home renovations, purchasing an investment property, or funding a business, the choice is yours. However, the lender’s primary concern is your ability to repay the loan.

What happens to my HELOC if property values in Calgary drop?

If local real estate values decline significantly, your lender has the right to reduce your HELOC credit limit or freeze the account entirely to protect their LTV ratio. While this is rare for borrowers in good standing, it highlights the risk of relying on a HELOC as your sole emergency fund during an economic downturn.

Do I have to pay legal and appraisal fees for both products?

Yes, setting up either a HELOC or a second mortgage requires registering a new charge on your property title. You should budget for appraisal fees (typically $300-$500) and legal or title fees (ranging from $700 to $1,500) depending on the complexity of the transaction and the lender’s specific requirements.

Conclusion

Unlocking the wealth stored in your Calgary property is a powerful financial maneuver, but it requires selecting the right tool for the job. A HELOC offers unparalleled flexibility for ongoing expenses and variable costs, provided you can manage the discipline of revolving credit and fluctuating interest rates. Conversely, a fixed-sum second mortgage delivers stability, predictability, and forced principal reduction, making it the superior choice for debt consolidation and single-phase projects.

As we navigate the 2026 economic landscape, aligning your borrowing strategy with your long-term wealth goals is more important than ever. Don’t leave your financial future to guesswork. If you need expert guidance to analyze your equity position and find the perfect lending product for your unique situation, contact our team today. We specialize in helping Calgarians secure the optimal financing structures to protect and grow their wealth.