A second mortgage in Calgary is an additional secured loan taken against the accumulated equity of your property, positioned in a subordinate legal status to your primary mortgage. This financial instrument allows homeowners to borrow up to 80% of their home’s appraised value without altering the interest rate, terms, or amortization schedule of their original mortgage contract. Because the primary lender retains the first right to repayment in the event of a default, secondary lenders assume higher risk, which is reflected in slightly higher interest rates compared to first mortgages.

Key Takeaways

- Equity Limits: Calgary homeowners can access up to 80% of their property’s appraised value, minus the outstanding balance of their primary mortgage.

- Preserved Terms: Secondary financing allows you to extract cash without breaking your existing first mortgage, avoiding costly prepayment penalties.

- Two Main Structures: Borrowers can choose between a lump-sum home equity loan (fixed rate) or a revolving Home Equity Line of Credit (variable rate).

- Interest Rates: Rates typically range from 6% to 12%, which is substantially lower than unsecured credit cards or personal loans.

- Primary Uses: The most common applications in 2026 include high-interest debt consolidation, property renovations, and funding business ventures.

- Approval Timeline: The standard funding process takes between 7 and 21 days, depending on appraisal scheduling and document verification.

The Mechanics of Secondary Financing in Alberta

Understanding the fundamental mechanics of property equity is the first step toward leveraging your real estate assets. Equity represents the portion of your property that you truly “own” free and clear of debt. According to recent 2026 data from the Statistics Canada, over 60% of property owners in the Calgary metropolitan area possess more than $100,000 in available home equity. This wealth accumulation is driven by a combination of regular principal paydowns and regional property value appreciation.

Financial institutions calculate your borrowing power using a metric known as the Loan-to-Value (LTV) ratio. The Canada Mortgage and Housing Corporation (CMHC) mandates that federally regulated lenders cap total borrowing at 80% of a home’s appraised value. For example, if your Calgary home is valued at $650,000, 80% of that value is $520,000. If your primary mortgage balance is $350,000, you have $170,000 in accessible equity available for secondary financing.

“Secondary financing is no longer just a safety net; in the 2026 economic landscape, it has evolved into a primary wealth-building tool for Alberta families looking to optimize their debt structures,” says Sarah Jenkins, Senior Economist at the Alberta Real Estate Board.

Unlike cash-out refinancing, which replaces your entire existing loan with a new one at current market rates, secondary financing creates a completely separate loan agreement. This distinction is critical for homeowners who secured ultra-low fixed rates on their primary mortgages in previous years and wish to preserve those favorable terms.

The Step-by-Step Approval Process for Calgary Homeowners

Securing additional financing against your property involves a structured evaluation process. Lenders must verify both the collateral’s value and the borrower’s capacity to manage additional debt obligations. The standard timeline from application to funding typically spans 7 to 21 days.

- Initial Consultation and Application: The process begins by submitting an application detailing your requested loan amount and intended use of funds. Lenders will perform a preliminary credit check to assess your financial health.

- Professional Property Appraisal: A licensed appraiser evaluates your home to determine its current market value. They analyze recent comparable sales in your specific Calgary neighborhood, property condition, and recent upgrades.

- Document Verification: Borrowers must provide comprehensive income and tax documentation. To streamline this phase, it is highly recommended to review a comprehensive document checklist prior to applying.

- Underwriting and Approval: The lender’s underwriting team calculates your Debt-to-Income (DTI) ratio, ensuring your total monthly debt obligations do not exceed 43% of your gross monthly income.

- Legal Registration and Funding: Once approved, you will sign the final loan agreements with a real estate lawyer. The lender registers a subordinate lien on your property title, and the funds are disbursed to your account.

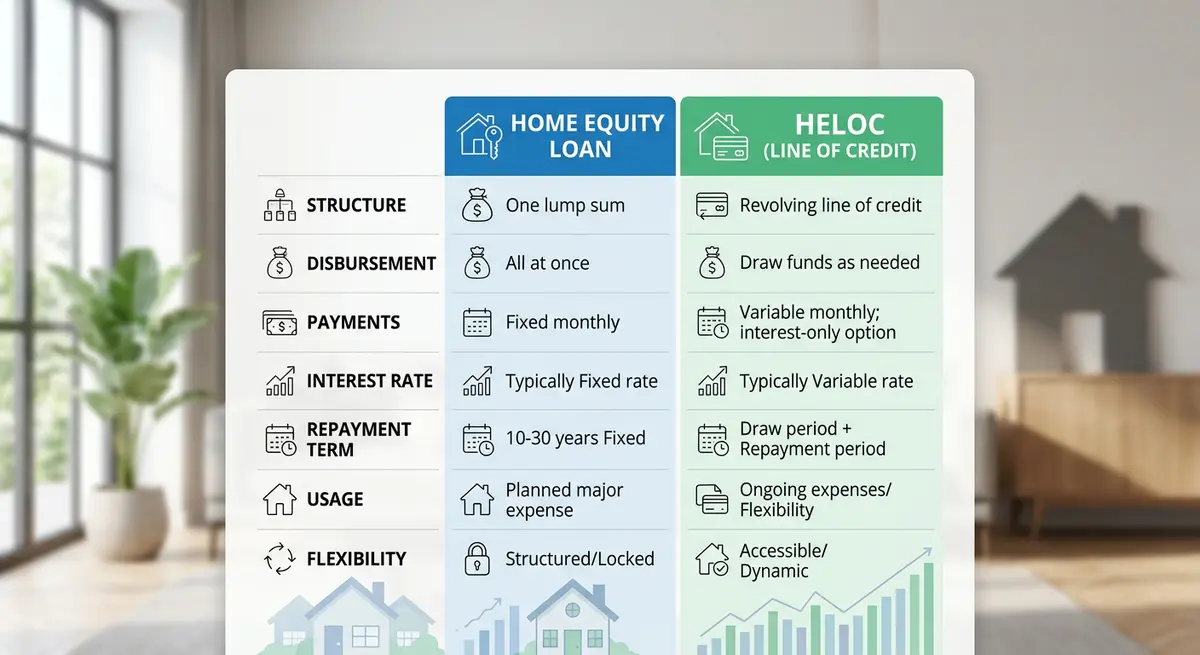

Home Equity Loans vs. HELOCs: Choosing the Right Structure

Homeowners must choose between two primary structures when accessing their equity: a traditional Home Equity Loan or a Home Equity Line of Credit (HELOC). Each product serves distinct financial strategies and comes with different repayment expectations.

A Home Equity Loan provides a single, lump-sum payout with a fixed interest rate and a set amortization schedule (typically 5 to 25 years). This structure offers predictable monthly payments, making it ideal for one-time, large-scale expenses like a major roof replacement or consolidating a specific amount of consumer debt.

Conversely, a HELOC functions as revolving credit. You are approved for a maximum limit and can draw funds as needed, repay them, and borrow again during the draw period (usually 5 to 10 years). HELOCs feature variable interest rates tied to the Bank of Canada prime rate. This flexibility is perfect for ongoing projects with staggered costs, such as a multi-phase home renovation.

| Feature | Home Equity Loan | HELOC |

|---|---|---|

| Fund Disbursement | Single lump sum at closing | Revolving access as needed |

| Interest Rate Type | Fixed rate | Variable rate (Prime + margin) |

| Payment Structure | Predictable, fixed monthly payments | Fluctuating payments based on usage |

| Best Used For | Debt consolidation, single large purchases | Ongoing renovations, emergency funds |

Strategic Uses for Your Property’s Hidden Value

Accessing property wealth is only half the equation; deploying those funds strategically dictates your long-term financial success. In 2026, Calgary residents are utilizing secondary financing for highly specific, value-generating purposes rather than discretionary consumer spending.

Debt Consolidation and Cash Flow Management

The most impactful use of property equity is restructuring high-interest liabilities. According to the Financial Consumer Agency of Canada (FCAC), the average credit card interest rate hovers between 18% and 24%. By contrast, secured secondary financing typically ranges from 6% to 12%. Using equity to pay off unsecured debts can reduce total monthly payment obligations by up to 40%.

“Homeowners often overlook the compounding effects of unsecured debt. Consolidating high-interest credit cards into a secured equity loan can literally salvage a family’s financial future by stopping the bleed of compound interest,” notes David Chen, Lead Financial Advisor at Prairie Wealth Management.

When consolidating debt, it is crucial to understand compounding frequency and how it impacts your total cost of borrowing. Secured loans generally compound semi-annually, whereas credit cards compound daily, making the transition to secured debt mathematically advantageous.

High-ROI Home Renovations in the 2026 Market

Reinvesting equity back into the property is another dominant strategy. In Calgary’s competitive real estate market, strategic renovations—such as legal basement suites, kitchen modernizations, and energy-efficient HVAC upgrades—frequently yield a 60% to 75% return on investment (ROI). Furthermore, creating a secondary suite can generate rental income that offsets the new loan payments entirely.

Other common uses include funding a child’s university education, providing a down payment for an investment property, or injecting capital into a small business. When multiple parties are involved in the home’s ownership, such as when adding a spouse to the title, the combined income can often qualify the household for larger loan amounts and superior rates.

Understanding Subordinate Lien Risks and Interest Rates

It is essential to approach secondary financing with a clear understanding of the risks involved. The term “second” refers strictly to the legal hierarchy of the loan on your property’s title. If a borrower defaults and the property enters foreclosure, the primary lender is guaranteed to recoup their funds first from the sale proceeds. The secondary lender only receives compensation from whatever funds remain.

“The subordinate position of a secondary loan means lenders take on exponentially more risk, which is directly reflected in the interest rate spread. If property values dip, the secondary lender’s collateral is the first to evaporate,” explains Dr. Marcus Thorne, Professor of Finance at the University of Calgary.

Because of this elevated risk profile, interest rates for these products will always be higher than those of primary mortgages. However, they remain significantly cheaper than unsecured credit alternatives. To mitigate the total interest paid over the life of the loan, savvy borrowers implement aggressive principal reduction strategies, such as making bi-weekly accelerated payments or applying annual lump-sum prepayments allowed by their contract.

Essential Documentation and Credit Requirements

While secondary lenders are often more flexible than primary banking institutions, they still enforce strict qualification criteria to ensure responsible lending. In 2026, most traditional lenders require a minimum credit score of 620 for approval, though private lenders may accept scores as low as 600 if the property boasts substantial equity.

Income stability is paramount. Borrowers must provide two to three years of verifiable income history via Notice of Assessment (NOA) documents, T4 slips, or recent pay stubs. Self-employed individuals may face additional scrutiny and are often required to provide comprehensive business financial statements to prove consistent cash flow.

Furthermore, maintaining a healthy equity buffer is non-negotiable. “In Calgary’s fluctuating 2026 housing market, maintaining a 20% equity buffer isn’t just a lender requirement—it’s essential financial hygiene to protect against localized market corrections,” states Elena Rostova, Director of Lending at Western Canada Credit Union.

Frequently Asked Questions

What is the maximum amount I can borrow against my home in Calgary?

Federally regulated lenders allow you to borrow up to 80% of your home’s current appraised value, minus the outstanding balance of your primary mortgage. Private lenders may occasionally lend up to 85%, though this comes with significantly higher interest rates and fees.

Do I have to use my current mortgage provider for a second mortgage?

No. You are free to shop around and secure secondary financing from any bank, credit union, or private lender. In fact, comparing offers from multiple institutions is the best way to ensure you receive the most competitive interest rate and terms.

How does a second mortgage affect my primary mortgage?

It does not affect your primary mortgage at all. Your original interest rate, amortization schedule, and monthly payments remain exactly the same. The secondary loan is a completely separate contract with its own distinct payment schedule.

Can I pay off my home equity loan early?

Yes, but you must review your specific contract for prepayment penalties. Many fixed-rate equity loans charge a fee (often three months of interest) if you pay off the entire balance before the term ends. HELOCs, being revolving credit, can generally be paid down to zero at any time without penalty.

What happens if I sell my house while having a second mortgage?

When you sell your property, the proceeds from the sale are used to pay off all liens on the title in their legal order. Your primary mortgage is paid first, followed immediately by the secondary loan. Any remaining profit is then transferred to you.

Are the interest payments on a second mortgage tax-deductible in Canada?

Interest payments are only tax-deductible if the borrowed funds are used specifically for investment purposes that generate income, such as buying dividend-paying stocks or funding a business. Funds used for personal debt consolidation or personal home renovations are not tax-deductible.

Conclusion

Leveraging the equity in your property through secondary financing is a powerful financial strategy when executed correctly. Whether you are looking to consolidate high-interest consumer debt, fund a major home renovation, or access capital for business investments, understanding the mechanics of Loan-to-Value ratios, interest rate structures, and lender requirements is crucial. By carefully weighing the benefits of lump-sum loans against revolving credit lines, Calgary homeowners can unlock their property’s hidden wealth without jeopardizing the favorable terms of their primary mortgage.

If you are ready to explore your equity options or need professional guidance navigating Alberta’s lending landscape, our team of local experts is here to help. Contact us today to schedule a free consultation and discover the best financing solutions tailored to your unique financial goals.