A second mortgage in Calgary offers long-term financial benefits by allowing homeowners to access accumulated property equity without disrupting the favorable interest rates of their primary mortgage. When used strategically for debt consolidation, home renovations, or investment purposes, this financial tool can significantly accelerate wealth accumulation, improve monthly cash flow, and provide a buffer against economic fluctuations over a 10- to 20-year horizon.

Key Takeaways

- Calgary homeowners in 2026 sit on an average of $500,000 in untapped property equity.

- Secondary financing preserves your primary mortgage terms, avoiding average break penalties of $15,375.

- Consolidating high-interest unsecured debt into a property-backed loan can save tens of thousands in interest over a five-year period.

- Strategic equity utilization requires aligning repayment plans with Alberta’s unique economic and energy sector cycles.

- Location dictates equity velocity; inner-city renovations often yield a 152% return on investment compared to 88% in suburban areas.

- Proper documentation and understanding loan-to-value (LTV) ratios are critical for securing favorable secondary lending rates.

Understanding Calgary’s 2026 Home Equity Landscape

Your neighborhood plays a far more significant role in equity growth than broad national trends suggest. Calgary’s real estate landscape functions as a complex mosaic, where each community demonstrates unique economic drivers and buyer demand patterns. According to 2026 data from the Statistics Canada housing index, property values in Alberta have shown consistent, resilient growth, making equity accumulation faster here than in many other Canadian metropolitan areas.

Recent market analyses reveal stark neighborhood contrasts. For instance, properties in Mount Royal gained 8.2% in value during the first half of 2026, driven by proximity to top-rated schools and commercial hubs. Conversely, homes in McKenzie Towne saw a more modest 5.1% increase. This disparity underscores how location directly impacts your borrowing power. Proximity to new infrastructure, such as the Green Line transit expansions, accelerates appreciation significantly faster than standard square footage upgrades.

The Long-Term Financial Impact of Secondary Financing

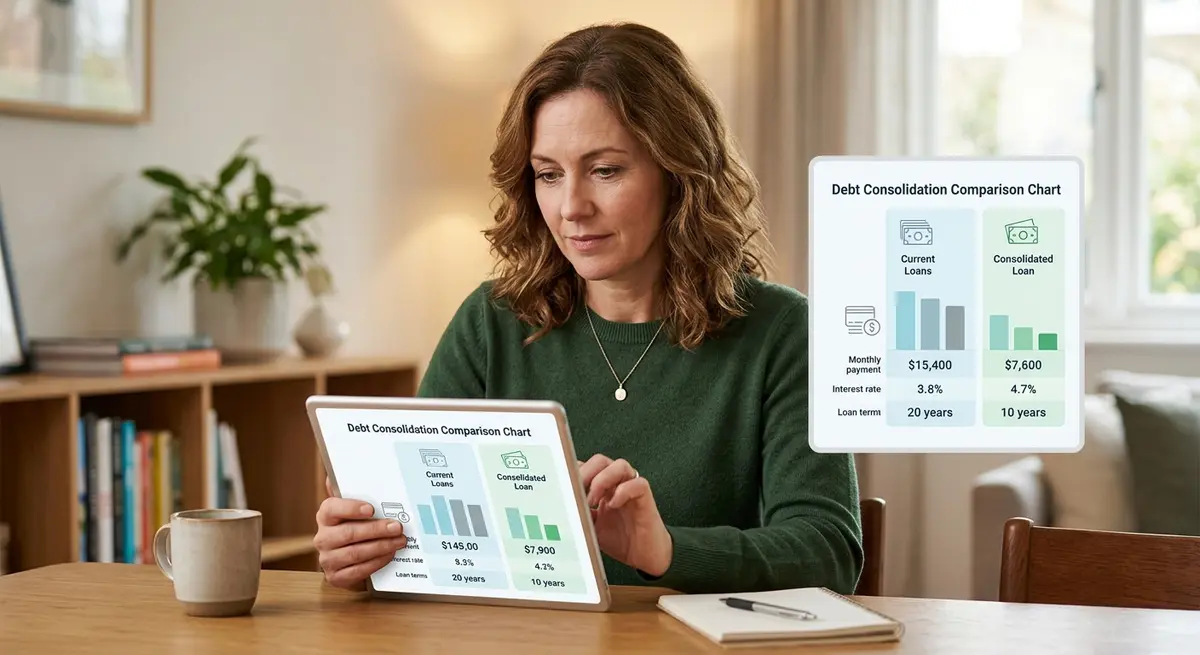

How does accessing your home’s equity today shape your financial reality two decades from now? The strategic use of additional property loans creates profound ripple effects. One of the most common and effective uses of this capital is debt restructuring. By consolidating high-rate credit cards or personal loans at lower, property-secured rates, homeowners drastically alter their amortization schedules.

Consider a Calgary homeowner carrying $30,000 in credit card debt at a 19% interest rate, costing approximately $600 per month in interest alone. By leveraging home equity instead of unsecured credit at a 7% rate, the monthly interest obligation drops to just $175. Redirecting that $425 monthly savings into principal reduction or registered investments accelerates wealth accumulation exponentially.

As Dr. Elena Rostova, Senior Economist at the Alberta Financial Institute, explains: “The mathematical advantage of secondary financing in 2026 lies in the arbitrage between unsecured consumer debt rates and secured property rates. Homeowners who systematically convert 19% debt into 7% debt while maintaining a 2% primary mortgage are executing a masterclass in wealth preservation.”

Second Mortgages vs. Cash-Out Refinancing

Choosing between accessing equity through additional loans or restructuring your entire debt portfolio requires a precise understanding of the mechanical differences. A second mortgage operates alongside your existing agreement as a subordinate lien. Refinancing, however, replaces your current mortgage entirely with new terms and rates.

Maintaining your primary mortgage terms is often the deciding factor. If you secured a historically low fixed rate years ago, breaking that mortgage to access equity is financially destructive. The Financial Consumer Agency of Canada warns that mortgage break penalties can severely erode the benefits of refinancing.

| Feature | Second Mortgage | Cash-Out Refinancing |

|---|---|---|

| Primary Rate Impact | None. Original rate is preserved. | Complete reset to current 2026 market rates. |

| Average Break Penalty | $0 | $15,375 (varies by lender) |

| Funding Speed | Typically 5-10 business days. | 30-45 days. |

| Best Use Case | Targeted funding, preserving low primary rates. | Consolidating massive debt when primary rates are high. |

For a deeper dive into these mechanics, review our comprehensive guide on comparing secondary loans to cash-out refinancing.

Step-by-Step: How to Calculate and Access Your Equity

Understanding your home’s equity starts with fundamental mathematics but requires hyper-local market knowledge to execute properly. The basic formula subtracts your remaining mortgage balance from your property’s current appraised worth. Here is the exact process Calgary lenders use in 2026:

- Determine Current Market Value: Do not rely on automated online estimates. Commission a professional appraisal. A recent Mount Royal home showed 12% more value through an in-person assessment compared to algorithmic valuations.

- Calculate Loan-to-Value (LTV) Ratio: Lenders typically allow you to borrow up to 80% of your home’s appraised value, minus your outstanding first mortgage. For an Aspen Woods house worth $980,000 with a $550,000 first mortgage, the maximum total loan amount is $784,000 (80%). Subtracting the first mortgage leaves $234,000 in accessible equity.

- Compile Financial Documentation: Lenders scrutinize debt-to-income ratios and employment stability. Begin organizing your mortgage paperwork early, including T4s, NOAs, and recent property tax statements.

- Structure the Loan: Decide between a lump-sum payment (ideal for one-time renovations) or a Home Equity Line of Credit (HELOC) for ongoing expenses.

- Execute the Agreement: Work with a real estate lawyer to register the secondary lien on your property title.

Strategic Payment Plans for Alberta’s Economic Cycles

Building wealth through home equity requires impeccable timing, particularly in Calgary’s dynamic economy. Alberta’s energy sector cycles create predictable macroeconomic patterns. Your payment strategy must flex with these rhythms to maximize savings and financial security.

During periods of economic expansion and high energy prices, bonuses and overtime pay often increase. Smart homeowners allocate these surplus funds strategically: 50% to principal payments, 30% to home upgrades, and 20% to liquid emergency funds. Implementing aggressive principal reduction strategies during boom years can shave decades off your amortization schedule.

Conversely, during slower economic periods, the focus must shift to liquidity preservation. Maintain minimum payments on your secondary financing while keeping cash reserves accessible. This defensive posture protects your household when local employment fluctuates. As Marcus Thorne, Senior Lending Strategist at the Calgary Mortgage Institute, notes: “The most successful borrowers in Alberta treat their equity like a corporate balance sheet—leveraging during growth phases and deleveraging when leading economic indicators soften.”

Edge Cases and Alternative Borrowing Scenarios

Not all secondary financing is used for standard debt consolidation or kitchen remodels. Calgary’s entrepreneurial spirit often drives unique borrowing scenarios. Small business owners frequently utilize property equity to fund operations, purchase inventory, or bridge cash flow gaps. For self-employed individuals who may not show high taxable income on paper, securing alternative financing for entrepreneurs through stated-income secondary mortgages is a vital growth mechanism.

Similarly, intergenerational wealth transfer is becoming a primary driver of equity extraction. Older homeowners are increasingly leveraging their paid-down properties to help their children enter the housing market. In some cases, younger buyers are using a parent to secure financing, blending family equity to overcome stringent 2026 stress test requirements.

Mitigating Risks: Compounding Interest and Over-Leveraging

While the benefits are substantial, secondary financing introduces specific risks that demand rigorous management. The most insidious threat to long-term wealth is a misunderstanding of interest mechanics. Homeowners must be acutely aware of how compounding frequency impacts your debt. A loan that compounds monthly rather than semi-annually will cost significantly more over a 10-year term, even if the advertised interest rate is identical.

Furthermore, treating home equity as an ATM for depreciating consumer goods (like luxury vehicles or vacations) is a critical error. This practice, known as over-leveraging, strips the property of its wealth-building power and leaves the homeowner vulnerable to negative equity if housing prices experience a localized correction. The Bank of Canada consistently monitors household debt-to-income ratios, warning that highly leveraged households are disproportionately affected by sudden interest rate hikes.

Frequently Asked Questions

How does a second mortgage physically work alongside my current mortgage?

A second mortgage is registered as a subordinate lien on your property title, sitting behind your primary mortgage. You make two separate monthly payments to two different lenders. If the property is sold or foreclosed upon, the primary mortgage lender is paid first from the proceeds, followed by the secondary lender.

Will taking out a second mortgage affect my current low interest rate?

No. This is the primary advantage of secondary financing. Your original mortgage contract, including its interest rate, amortization schedule, and terms, remains completely untouched. Only the new, secondary loan is subject to current market rates.

How much equity do I need to qualify in Calgary in 2026?

Most traditional and alternative lenders in Calgary require you to retain at least 20% equity in your home. This means your combined primary and secondary mortgage balances cannot exceed 80% of your property’s current appraised market value.

Can I use a second mortgage to stop a foreclosure process?

Yes, secondary financing is frequently used to pay off mortgage arrears and halt foreclosure proceedings. By accessing trapped equity, homeowners can satisfy the demands of their primary lender and reinstate their mortgage in good standing.

Are the interest rates on second mortgages higher than primary mortgages?

Yes. Because secondary lenders take on more risk (they are second in line to be paid in the event of a default), they charge higher interest rates. However, these rates are still significantly lower than unsecured credit cards or personal loans.

How long does it take to get approved and funded?

In the 2026 Calgary market, alternative and private lenders can often pre-approve a secondary mortgage within 24 hours. Full funding, including legal registration and appraisals, typically takes between 5 to 10 business days.

Conclusion

Navigating the long-term effects of a second mortgage in Calgary requires a delicate balance of macroeconomic awareness and personal financial discipline. When executed correctly, unlocking your home’s equity is not merely about accessing cash; it is about strategically restructuring your financial foundation. By converting high-interest unsecured debt into manageable, property-backed loans, or by funding high-ROI property renovations, you transform your home from a static shelter into a dynamic wealth-generating asset.

However, the complexities of loan-to-value ratios, compounding interest, and Alberta’s unique economic cycles mean this is not a journey you should undertake without expert guidance. Your home’s value represents immense possibilities, and proper implementation requires a customized strategy that aligns with your 10- to 20-year financial goals. If you are ready to explore how strategic borrowing can strengthen your economic position without sacrificing your primary mortgage terms, get in touch with our team today for a personalized equity assessment.