Rising interest rates directly increase the cost of borrowing against your home equity, squeezing monthly cash flow for variable-rate loan holders and tightening qualification metrics for new applicants. In 2026, Calgary homeowners must navigate stricter federal stress tests, fluctuating local property valuations, and elevated baseline borrowing costs to secure favorable secondary financing. Successfully managing a second mortgage in this economic climate requires proactive refinancing strategies, a deep understanding of loan-to-value ratios, and careful monitoring of central bank monetary policies.

Key Takeaways

- Variable-rate secondary loans adjust immediately with central bank policy shifts, requiring larger monthly budget allocations.

- Fixed-rate agreements provide payment certainty but currently carry higher initial premiums in the 2026 financial market.

- Accessible home equity is heavily dependent on recent property appraisals, which fluctuate based on Calgary’s unique housing demand.

- Federal stress tests now require borrowers to qualify at rates significantly higher than their contract rate, reducing maximum loan amounts.

- Strategic debt consolidation using home equity can still yield net savings, provided the blended interest rate is lower than unsecured debt rates.

- Proactive repayment strategies, such as accelerated bi-weekly payments, mitigate the long-term impact of elevated borrowing costs.

The 2026 Economic Landscape: Why Borrowing Costs Are Shifting

Central banks utilize monetary policy as a primary mechanism to regulate economic activity and curb inflation. When consumer prices escalate beyond target thresholds, institutions like the Bank of Canada incrementally raise the overnight target rate to cool domestic spending. These macroeconomic decisions ripple instantly through global financial markets, directly dictating the prime lending rates offered by retail banks and alternative lenders across Alberta.

According to recent data from Statistics Canada, the national inflation rate has experienced significant volatility over the past three years, prompting a series of aggressive rate adjustments. By early 2026, the baseline borrowing cost stabilized at a higher plateau compared to the historic lows of the early pandemic era. This paradigm shift fundamentally alters the mathematics of home equity lending. For every 100 basis point (1%) increase in the central bank’s policy rate, consumer mortgage rates typically adjust by 0.75% to 1.25% within a single fiscal quarter.

As Dr. Sarah Jenkins, Chief Economist at the Canadian Housing Research Institute, explains: “Calgary’s dual-engine economy, driven by both energy sector revenues and record interprovincial migration, creates a unique micro-economy. While national rate hikes aim to suppress demand, Calgary’s localized population boom continues to support high property valuations, creating a complex environment for equity borrowing.”

How Rate Hikes Directly Impact Your Existing Secondary Financing

Homeowners who secured additional financing against their properties prior to the recent rate hike cycles are experiencing varying degrees of financial friction, depending entirely on their specific loan structure. The distinction between variable and fixed-rate agreements has never been more critical than in the current 2026 fiscal environment.

Variable-rate agreements are intrinsically linked to the lender’s prime rate. When the central bank announces a rate increase, variable payments adjust almost immediately. For a homeowner carrying a $100,000 secondary loan, a cumulative 2.5% rate increase translates to an additional $200 to $250 in monthly interest obligations. This payment shock can severely strain household budgets if not anticipated. Furthermore, it is crucial to understand how compounding frequency impacts your debt, as higher rates combined with frequent compounding periods exponentially accelerate interest accumulation.

Conversely, fixed-rate options shield borrowers from immediate market volatility. By locking in a specific rate for a predetermined term (typically one to five years), homeowners guarantee payment stability. However, this security comes at a premium. Lenders price fixed rates based on anticipated future bond yields, meaning borrowers often pay a higher initial rate for the privilege of certainty. When these fixed terms mature in 2026, many Calgary residents face significant renewal shocks as they transition from historically low rates to current market realities.

Assessing Your Home Equity in a Fluctuating Calgary Market

The foundation of any secondary financing strategy is the accurate assessment of available home equity. Canadian financial regulations generally permit homeowners to borrow up to 80% of their property’s appraised value, encompassing both the primary and secondary mortgages. This metric is known as the Loan-to-Value (LTV) ratio.

To calculate your accessible equity, you must subtract your outstanding primary mortgage balance from 80% of your home’s current market value. For example, if your Calgary home is appraised at $600,000, the maximum allowable debt secured against the property is $480,000. If your primary mortgage balance is $350,000, you theoretically have $130,000 in accessible equity.

However, property valuations are not static. The Alberta Real Estate Association notes that while Calgary has seen robust price appreciation due to housing supply constraints, neighborhood-specific valuations can vary wildly. A professional, localized appraisal is mandatory. If local market conditions soften and property values decline, your equity cushion shrinks proportionally, potentially pushing your LTV ratio above acceptable lending thresholds and limiting your refinancing options.

Fixed Loans vs. Home Equity Lines of Credit (HELOCs): A 2026 Comparison

When accessing home equity, Calgary homeowners typically choose between a traditional structured loan and a revolving credit facility. Understanding the mechanical differences between these products is essential for optimizing your financial strategy in a high-rate environment.

| Feature | Traditional Second Mortgage | HELOC (Home Equity Line of Credit) |

|---|---|---|

| Fund Disbursement | Single, upfront lump sum. | Revolving access up to a predetermined credit limit. |

| Interest Rate Structure | Typically fixed for the duration of the term. | Almost exclusively variable, tied to the prime rate. |

| Repayment Schedule | Predictable, blended payments of principal and interest. | Flexible; often allows interest-only payments during the draw period. |

| Best Use Case | Debt consolidation, single large purchases, budget certainty. | Ongoing renovation projects, emergency funds, fluctuating expenses. |

In 2026, the preference between these two instruments has shifted. With variable rates remaining elevated, many conservative borrowers are opting for fixed-term secondary mortgages to guarantee their monthly obligations. However, for those who require funds incrementally and possess the cash flow to absorb potential rate fluctuations, a HELOC remains a highly flexible financial tool.

Step-by-Step: Navigating the Application Process in a Strict Lending Climate

The underwriting process for secondary financing has become markedly more rigorous. Lenders are acutely aware of the macroeconomic pressures facing consumers and have adjusted their risk tolerance accordingly. To successfully secure funding, applicants must present a flawless financial profile.

- Calculate Your Debt-to-Income (DTI) Ratio: Lenders scrutinize your Total Debt Service (TDS) ratio, which should ideally remain below 42% of your gross household income. This calculation must include the proposed new loan payments at the current stress-tested rate.

- Compile Comprehensive Documentation: The days of stated-income leniency are largely behind us for prime lending. You must gather recent T4s, Notices of Assessment (NOAs), consecutive pay stubs, and detailed property tax statements. Reviewing a comprehensive secondary mortgage document checklist ensures you do not delay the underwriting process.

- Address Credit Report Anomalies: Obtain a copy of your Equifax or TransUnion report before applying. Dispute any inaccuracies and be prepared to explain credit inquiries to lenders, as multiple recent credit checks can signal financial distress to an underwriter.

- Prepare for the Stress Test: The Financial Consumer Agency of Canada mandates that federally regulated lenders qualify borrowers at a rate 2% higher than the contracted rate, or 5.25%, whichever is greater. This ensures you can sustain payments if rates climb further.

- Secure a Professional Appraisal: Engage a certified appraiser familiar with your specific Calgary quadrant to provide an accurate, defensible valuation of your property.

Debt Consolidation: Weighing the Benefits and Foreclosure Risks

One of the most prevalent uses for secondary financing in Calgary is debt consolidation. As the cost of living increases, many households accumulate high-interest unsecured debt, such as credit card balances and personal loans. Leveraging home equity to pay off these obligations can dramatically improve monthly cash flow.

Consider a scenario where a homeowner holds $40,000 in credit card debt at an average interest rate of 21.99%. The monthly interest alone exceeds $730. By consolidating this debt into a secondary mortgage at 8.5%, the annual interest burden drops significantly, allowing the borrower to allocate funds toward principal reduction rather than merely servicing interest.

However, this strategy carries profound risks. By converting unsecured consumer debt into secured mortgage debt, you are collateralizing your home. If you fail to maintain the new mortgage payments, the lender possesses the legal right to initiate foreclosure proceedings. Understanding the notice of default and statement of claim process is vital; in Alberta, missing payments for as little as 90 days can trigger legal action. Borrowers must be acutely aware of the foreclosure timeline in Calgary to comprehend the severity of defaulting on secured debt.

As Marcus Thorne, Senior Risk Analyst at Prairie Financial Group, warns: “Consolidation is a financial reset, not a cure. If the underlying spending habits that created the unsecured debt are not addressed, homeowners risk depleting their equity and ultimately losing their property to foreclosure.”

Effective Repayment Strategies to Protect Your Equity

Securing the loan is only the first step; executing a disciplined repayment strategy is what ultimately protects your wealth. In a high-interest environment, passive repayment schedules result in massive total interest costs over the life of the loan. Proactive management is essential.

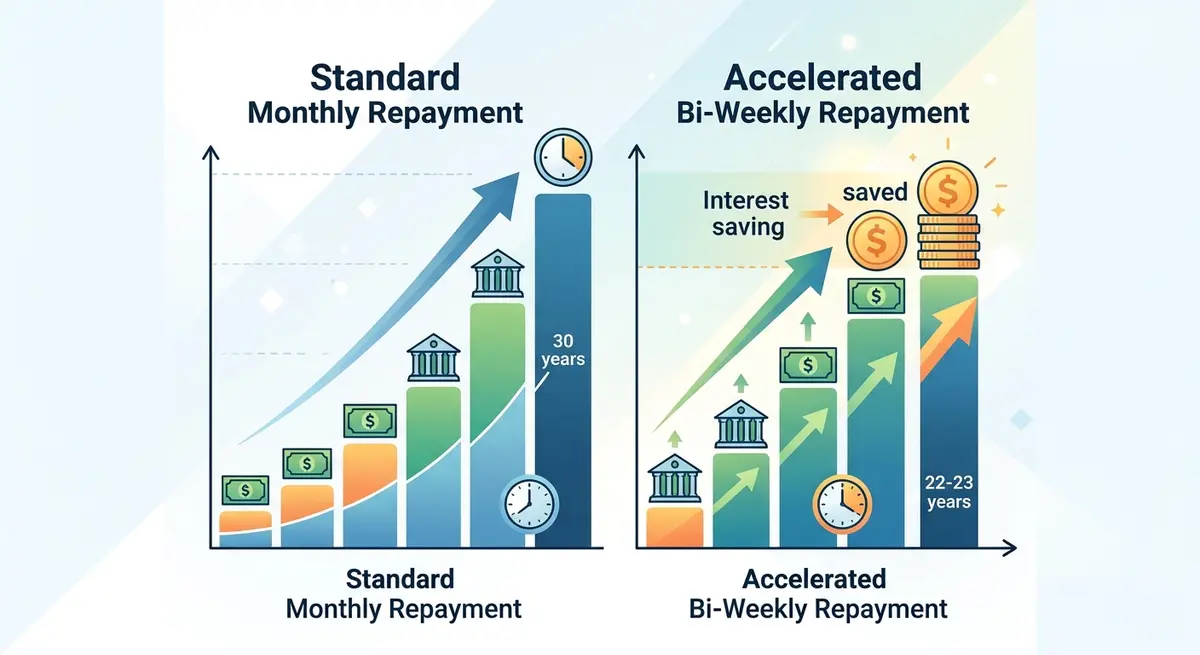

Implementing accelerated principal reduction strategies is the most effective way to combat high borrowing costs. By switching from monthly to accelerated bi-weekly payments, you effectively make one additional full monthly payment per year, applied directly to the principal. On a 20-year amortization schedule, this simple adjustment can shave years off the loan term and save tens of thousands of dollars in interest.

Furthermore, homeowners should capitalize on prepayment privileges. Most closed mortgage contracts allow borrowers to make annual lump-sum payments (typically 10% to 20% of the original principal) without incurring penalties. Directing tax refunds, annual bonuses, or inheritance funds toward the secondary mortgage principal yields a guaranteed, tax-free return on investment equal to the loan’s interest rate.

Finally, continuous market monitoring is required. While rates are elevated in 2026, economic cycles inevitably shift. Homeowners should maintain regular contact with their mortgage broker to assess whether breaking a current contract to refinance at a lower rate is mathematically advantageous, factoring in any associated prepayment penalties. It is also wise to conduct a cash-out refinancing comparison to determine if rolling the primary and secondary loans into a single new facility offers better long-term value.

Conclusion

Navigating the complexities of a Calgary second mortgage in 2026 requires a sophisticated understanding of macroeconomic trends, strict lending regulations, and localized property market dynamics. Rising interest rates have undeniably increased the cost of accessing home equity, making proactive financial management more critical than ever. Whether you are seeking to consolidate high-interest debt, fund a major renovation, or simply restructure your existing obligations, success depends on accurately assessing your equity, choosing the right loan product, and implementing aggressive repayment strategies to protect your most valuable asset.

If you are struggling with rising payments or want to explore your refinancing options in today’s market, professional guidance is invaluable. Get in touch with our team today to schedule a comprehensive review of your home equity position and discover tailored strategies to secure your financial future.

Frequently Asked Questions

How do rising Bank of Canada rates affect my existing fixed-rate second mortgage?

If you have a fixed-rate second mortgage, your interest rate and monthly payments remain completely unchanged for the duration of your current term. However, you will be subject to current, potentially higher market rates when your term expires and you are required to renew the contract.

Can I still qualify for a second mortgage if my property value has decreased?

Yes, but your borrowing capacity will be reduced. Lenders calculate your maximum loan amount based on a percentage (usually up to 80%) of your home’s current appraised value, so a lower valuation directly decreases the amount of accessible equity you can borrow against.

What is the federal mortgage stress test, and does it apply to second mortgages?

The federal stress test requires lenders to prove you can afford mortgage payments at a qualifying rate of 5.25% or your contract rate plus 2%, whichever is higher. This rule applies to all federally regulated financial institutions, making it harder to qualify for secondary financing in a high-rate environment.

Is it better to use a HELOC or a fixed second mortgage for debt consolidation?

A fixed second mortgage is generally superior for debt consolidation because it provides a guaranteed interest rate and a structured repayment schedule, preventing the balance from revolving. A HELOC carries variable rates that can increase your costs if central bank rates rise, and requires strict discipline to pay down the principal.

How quickly can a lender start foreclosure if I miss second mortgage payments in Alberta?

In Alberta, a lender can issue a Notice of Default and begin the legal foreclosure process after you have been in arrears for as little as 60 to 90 days. Because second mortgages are secured against your property, missing payments carries the severe risk of losing your home.

Will multiple credit checks for a second mortgage hurt my credit score?

While hard inquiries do temporarily lower your credit score, credit bureaus typically group multiple mortgage inquiries made within a 14 to 45-day window as a single event. This allows you to shop around for the best secondary financing rates without severely damaging your credit profile.