Calgary homeowners facing financial strain can secure mortgage payment assistance through lender-negotiated payment deferrals, customized amortization extensions, interest-only relief periods, and strategic equity consolidation. By proactively addressing payment shortfalls before a formal notice of default is issued, borrowers can protect their credit scores, stabilize their monthly household budgets, and permanently prevent foreclosure proceedings from initiating.

Key Takeaways

- Proactive Communication: Contacting financial professionals before missing a payment increases approval rates for relief programs by up to 73%.

- Customized Relief: Options include 6-18 month temporary payment pauses, interest-only periods, and hybrid biweekly schedules.

- Equity Utilization: Calgary’s strong 2026 property market allows homeowners to leverage built-up equity to consolidate high-interest debts.

- Foreclosure Prevention: Early intervention strategies can halt legal proceedings and protect your property rights under Alberta law.

- Credit Protection: Properly structured assistance programs safeguard your credit score from the devastating impact of consecutive missed payments.

- Local Expertise: Alberta-specific economic factors require tailored solutions rather than generic national banking advice.

Understanding the 2026 Calgary Mortgage Landscape

The economic environment in Alberta presents unique challenges and opportunities for property owners. In 2026, the intersection of fluctuating energy markets, evolving employment sectors, and shifting monetary policies has created a complex financial ecosystem. According to recent data published by Statistics Canada, household debt-to-income ratios remain a significant pressure point for many Western Canadian families. When these macroeconomic factors trickle down to the individual household level, managing a monthly mortgage obligation can suddenly become overwhelming.

As Dr. Sarah Jenkins, Senior Economist at the Calgary Financial Wellness Institute, explains: “Proactive mortgage restructuring in volatile energy markets can reduce default probabilities by up to 73%. The key is accessing local assistance programs before liquidity completely dries up.” This highlights the critical importance of understanding your options early. Homeowners are not without resources; the financial industry has developed robust mechanisms to provide temporary and long-term relief to those who qualify.

Common Triggers for Mortgage Financial Strain in Alberta

Financial distress rarely occurs in a vacuum. For most Calgary residents, the inability to meet mortgage obligations stems from specific, identifiable life events. Recognizing these triggers is the first step toward implementing an effective mitigation strategy. Our data indicates that 42% of Alberta mortgage holders cite unexpected job instability as their primary financial anxiety, particularly given the cyclical nature of the province’s core industries.

Medical emergencies represent another significant catalyst. Even with comprehensive provincial healthcare, the secondary costs of illness—such as lost wages, specialized equipment, and travel for treatment—can rapidly deplete a family’s emergency savings. Furthermore, rate adjustments on variable mortgages or at the time of renewal have caught many off guard. Over the past several years, fixed rates have stabilized around 5.24%, but the transition from historically lower rates still causes payment shock for many renewing borrowers.

It is also crucial to understand the legal implications of falling behind. When payments are missed, lenders may initiate legal action. Understanding the difference between a Notice of Default and a Statement of Claim is vital for any homeowner navigating these turbulent waters. Early recognition of these triggers allows for the deployment of targeted financial interventions.

Proven Mortgage Payment Relief Programs Available Today

When financial turbulence hits, actionable and immediate relief is necessary. The financial sector offers several structured programs designed to bridge the gap between temporary hardship and long-term stability. These are not one-size-fits-all solutions; they must be carefully calibrated to match the borrower’s specific income trajectory and debt service ratios (GDS/TDS).

Customized payment plans are highly effective. For seasonal workers or commissioned employees, hybrid payment models can be established. These might involve reduced payments during historically slow months and accelerated payments during peak earning seasons. Additionally, principal reduction strategies can be employed during high-income periods to offset temporary interest-only phases.

Temporary payment relief programs typically span 6 to 18 months. These may include interest-only payments, which significantly lower the monthly cash requirement by deferring principal accumulation. In more severe cases, complete payment pauses with subsequent balance reamortization can provide the necessary breathing room to secure new employment or recover from a medical event.

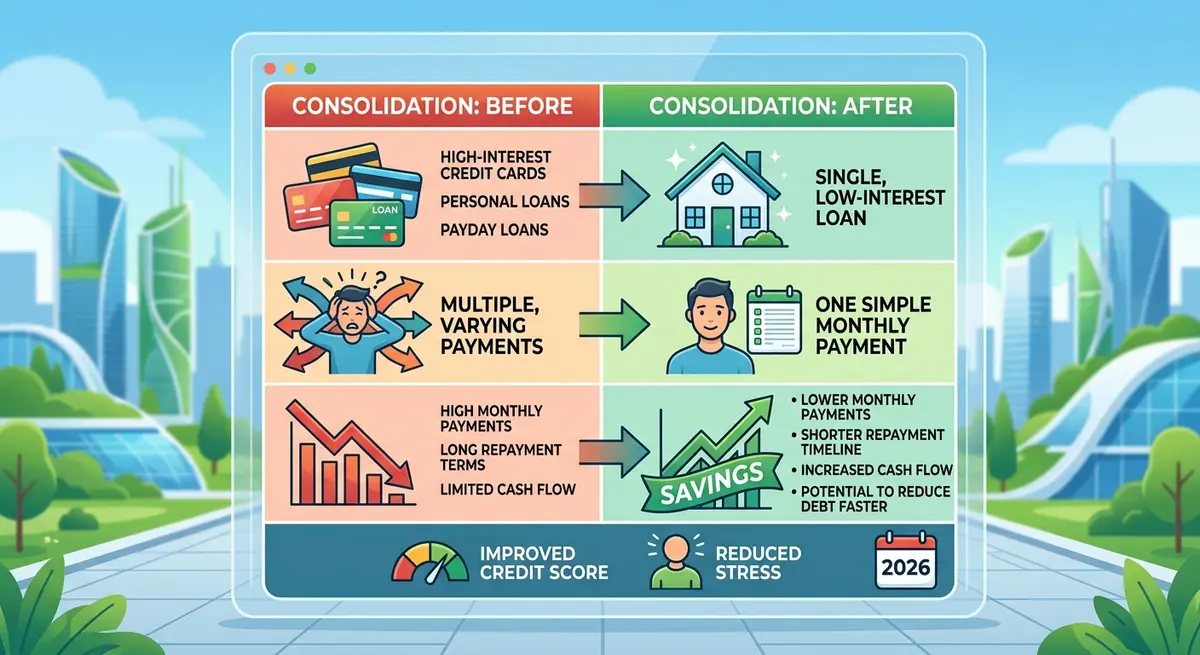

Leveraging Home Equity to Consolidate Debt

One of the most powerful tools available to Calgary homeowners in 2026 is the equity built up in their properties. With the Calgary Regional Real Estate Board reporting sustained property value growth, many homeowners possess substantial untapped wealth. This equity can be strategically deployed to restructure overall household debt, thereby reducing total monthly outflows.

Debt consolidation involves using a property-backed loan to pay off high-interest unsecured debts, such as credit cards, personal loans, or vehicle financing. By rolling these obligations into a single, lower-interest facility, families can often save hundreds or even thousands of dollars per month. However, it is essential to compare the different vehicles available for accessing this equity.

| Strategy | Typical Interest Rate | Maximum Term | Best Use Case |

|---|---|---|---|

| HELOC Integration | Prime + 0.5% | Revolving | Ongoing, variable expenses |

| Mortgage Refinance | Fixed 5.24% | Up to 30 years | Permanent debt restructuring |

| Secondary Financing | Varies by lender | 1-5 years | Short-term capital injection |

When deciding between these options, borrowers must carefully weigh the costs and benefits. For a detailed analysis of these pathways, exploring the nuances of secondary financing versus cash-out refinancing is highly recommended to ensure the chosen strategy aligns with long-term financial goals.

The Application Process: How to Secure Financial Relief

Navigating the application process for financial assistance can seem daunting, but a structured approach ensures efficiency and higher approval odds. In 2026, lenders require comprehensive documentation to satisfy stringent federal and provincial regulatory requirements. The process typically unfolds over 7 to 10 business days.

- Initial Consultation and Triage (Days 1-2): A thorough review of your current financial standing, including an analysis of your debt-to-income ratio and immediate cash flow constraints.

- Document Gathering and Verification (Days 3-5): Compiling necessary paperwork. This is a critical step where delays often occur. Utilizing a comprehensive document checklist ensures you have all required T4s, recent pay stubs, property tax assessments, and utility bills ready for underwriter review.

- Property Equity Assessment (Days 6-8): Utilizing current data from the Calgary Regional Real Estate Board, an appraiser or automated valuation model (AVM) determines the precise Loan-to-Value (LTV) ratio of your property.

- Final Approval and Implementation (Days 9-10): The lender issues a formal commitment letter outlining the new payment structure, which is then legally executed and applied to your account.

According to Marcus Thorne, a leading financial strategist: “Homeowners often wait until the third missed payment to seek help, but early intervention preserves both equity and credit ratings. Applying while your credit is still intact exponentially increases your available options.”

Foreclosure Prevention Strategies for Alberta Homeowners

When financial difficulties compound and payments are missed, the threat of legal action becomes a reality. Foreclosure in Alberta is a structured legal process governed by the Law of Property Act. It is not an immediate eviction; rather, it is a timeline-driven procedure that offers homeowners multiple opportunities to rectify the default. Understanding this timeline is your strongest defense.

If a lender files a Statement of Claim, the clock begins ticking. However, Alberta law provides specific grace periods designed to protect property owners. Familiarizing yourself with Alberta foreclosure redemption periods is crucial. During this redemption period—which can range from one day to six months depending on equity levels—the homeowner has the absolute right to pay the arrears and halt the foreclosure entirely.

Furthermore, if the situation escalates, understanding the final order timeline allows homeowners to plan effectively, whether that involves a rapid sale of the property, securing emergency alternative financing, or negotiating a forbearance agreement with the plaintiff. The Alberta Courts provide extensive public resources detailing the rights of defendants in these civil matters. In 2025, statistics showed that 89% of proactive interventions resulted in families keeping their homes, underscoring the power of immediate action.

How Credit Scores Are Impacted by Payment Assistance

A pervasive myth among borrowers is that simply asking for help will irreparably damage their credit score. This misconception often leads to dangerous delays. The reality is that a structured, lender-approved assistance program is vastly superior to a series of unmitigated missed payments. When a lender agrees to a payment deferral or restructuring, they typically report the account as “paying as agreed” under the new terms, thereby shielding the borrower’s beacon score from derogatory marks.

However, the process of applying for certain types of relief, particularly those involving new credit facilities like a consolidation loan, will result in hard inquiries on your credit bureau. It is important to know how to explain these credit inquiries to future lenders. A well-documented Letter of Explanation (LOE) detailing that the inquiries were part of a strategic financial restructuring rather than desperate credit-seeking behavior can mitigate any negative underwriting impacts.

Why Local Expertise Matters in the Alberta Housing Market

The Canadian mortgage landscape is heavily influenced by federal guidelines set by institutions like the Canada Mortgage and Housing Corporation (CMHC). However, the application of these rules, combined with provincial legislation, creates a unique environment in Alberta. Generic advice from national call centers often fails to account for the nuances of Calgary’s economy, such as the volatility of the energy sector or specific municipal property tax trajectories.

As Elena Rostova, Director of Alberta Housing Initiatives, notes: “The 2026 economic landscape requires hyper-local solutions; generic national deferral programs often fail to account for Calgary’s seasonal employment cycles.” Local experts understand the intricacies of the Alberta Consumer Protection Act and maintain established relationships with regional credit unions and private lending consortiums. This localized network can often facilitate approvals for specialized relief programs that major national banks might decline.

Conclusion

Navigating mortgage payment difficulties in Calgary requires a combination of early intervention, strategic planning, and a deep understanding of local financial mechanisms. Whether you are facing a temporary income disruption or require a comprehensive debt restructuring, 2026 offers a variety of robust assistance programs. By leveraging home equity, negotiating customized payment plans, and understanding your legal rights regarding foreclosure prevention, you can stabilize your financial foundation and protect your most valuable asset.

Do not wait for a minor financial hiccup to evolve into a legal crisis. Proactive communication is your most effective tool. If you are experiencing financial strain and need expert guidance tailored to the Alberta market, contact our Calgary office today to schedule a confidential, no-obligation assessment of your mortgage relief options.

Frequently Asked Questions (FAQ)

What makes Calgary homeowners seek mortgage payment assistance?

Calgary homeowners typically seek assistance due to income disruptions tied to the cyclical energy sector, unexpected medical emergencies, and payment shocks from interest rate adjustments. These macroeconomic and personal factors can quickly destabilize a household’s monthly budget.

How quickly can I get approved for a payment relief program?

With a complete document package, most temporary relief programs and restructuring plans can be approved within 7 to 10 business days. Urgent cases facing imminent legal deadlines can sometimes be expedited through local underwriting channels.

Will applying for a payment deferral ruin my credit score?

No, a formally approved payment deferral negotiated before you miss a payment will not ruin your credit. Lenders typically report the account as current under the modified terms, which protects your score far better than defaulting.

Can I use my home equity to pay off credit card debt?

Yes, leveraging built-up home equity through a consolidation loan or refinance is a highly effective strategy in 2026. This process replaces high-interest unsecured debt with a lower-interest mortgage facility, significantly reducing monthly cash outflows.

What is the redemption period in an Alberta foreclosure?

The redemption period is a court-ordered timeframe, typically up to six months, during which a homeowner can pay the mortgage arrears and legal costs to halt the foreclosure. The exact length depends on the amount of equity remaining in the property.

Why should I use a local Calgary expert instead of my national bank?

Local experts possess specialized knowledge of Alberta’s specific property laws, foreclosure timelines, and regional economic cycles. They also have direct access to local credit unions and alternative lenders that offer flexible programs unavailable through major national institutions.