A second mortgage is a subordinate loan secured against your property’s built-up equity that exists alongside your primary mortgage. It allows homeowners to borrow up to 80% of their home’s appraised value without altering the interest rate, amortization, or terms of their original loan. Because the primary mortgage remains untouched, this financial tool provides a strategic way to access large sums of capital for debt consolidation, renovations, or investments while maintaining your initial borrowing conditions.

Key Takeaways

- Preserve Primary Terms: Access up to 80% of your property’s equity without refinancing or losing your original mortgage rate.

- Subordinate Structure: Secondary financing sits behind your first mortgage on the property title, which influences lender risk and interest rates.

- Flexible Formats: Choose between a lump-sum home equity loan for fixed expenses or a revolving Home Equity Line of Credit (HELOC) for ongoing projects.

- Cost Efficiency: Secured borrowing typically offers significantly lower interest rates compared to unsecured personal loans or credit cards.

- Strategic Utility: Ideal for high-interest debt consolidation, funding major renovations, or providing capital for business ventures.

Understanding the Mechanics of Secondary Home Financing

Your home’s equity acts as a powerful, yet often overlooked, financial asset. Equity represents the portion of your property that you fully own—calculated by subtracting all secured debts from the current appraised market value of the home. As you pay down your principal balance and as local real estate markets appreciate, this financial resource naturally expands.

In Canada, lending regulations typically allow property owners to borrow up to 80% of their home’s appraised value, minus any outstanding mortgage balances. This metric is known as the Loan-to-Value (LTV) ratio. For example, if your home is appraised at $500,000 in 2026, 80% of that value equals $400,000. If your remaining primary mortgage balance is $250,000, you have $150,000 in accessible equity available for secondary financing.

According to the Canada Mortgage and Housing Corporation (CMHC), understanding your exact LTV is the critical first step before applying for any additional property-secured debt. Lenders view this equity as collateral, which mitigates their risk and allows them to offer more favorable terms than unsecured lending options.

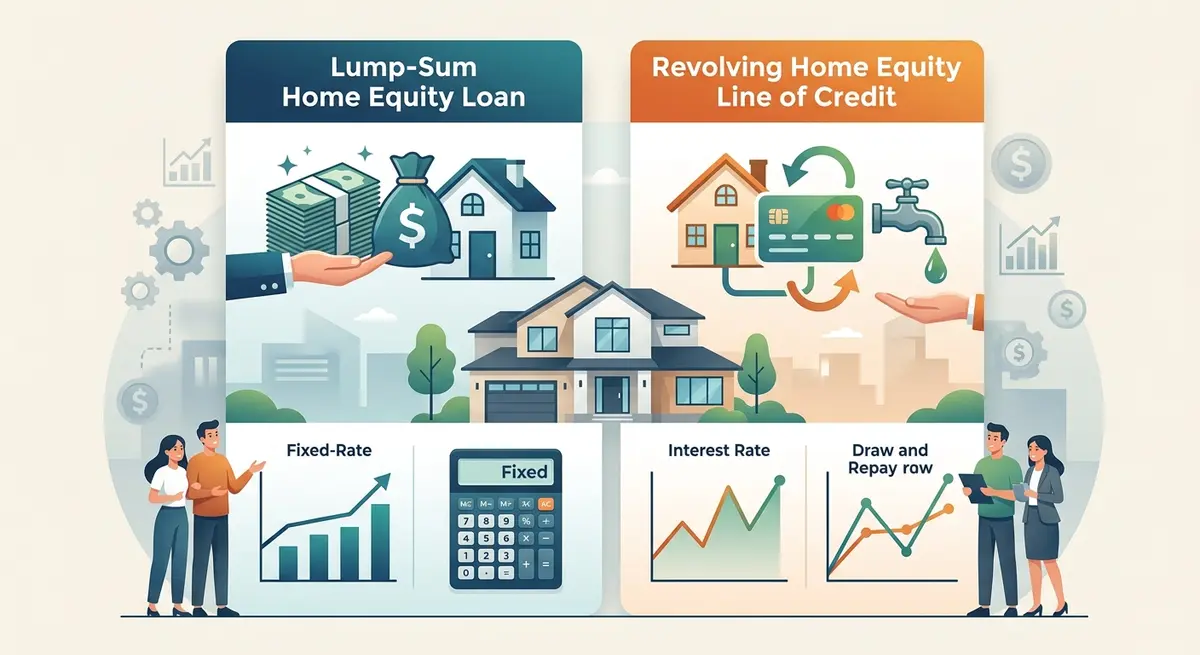

Home Equity Loans vs. HELOCs: Which is Right for You?

When exploring secondary financing, homeowners generally choose between two primary structures: a traditional lump-sum loan or a Home Equity Line of Credit (HELOC). While both utilize your property as collateral, their disbursement methods and repayment structures differ significantly.

A traditional home equity loan provides immediate funds through a single, upfront disbursement. You receive the full approved amount immediately, making it ideal for predictable, one-time expenses like a major kitchen upgrade, medical bills, or consolidating a specific amount of high-interest debt. Repayment involves fixed monthly installments over a set term (often 5 to 25 years), providing absolute payment stability.

Conversely, a HELOC functions as revolving credit. You are approved for a maximum limit and can draw funds as needed, paying interest only on the amount you actively use. This flexibility is perfect for phased construction projects or ongoing educational costs. As you repay the borrowed principal, your available credit replenishes.

Comparison of Secondary Financing Options

| Feature | Home Equity Loan | HELOC |

|---|---|---|

| Disbursement | Single lump sum upfront | Revolving access as needed |

| Interest Rates | Typically fixed, providing predictable payments | Usually variable, tied to the prime rate |

| Repayment Structure | Fixed monthly principal and interest payments | Interest-only minimums during the draw period |

| Best Used For | Debt consolidation, one-time major purchases | Ongoing renovations, emergency safety nets |

Current Interest Rates and Administrative Costs in 2026

Navigating the costs associated with secondary borrowing requires a clear understanding of both interest rates and upfront administrative fees. Because these loans are registered as subordinate debt, the secondary lender takes a backseat to the primary mortgage holder. If a default occurs, the first lender is paid entirely before the secondary lender receives any funds. To compensate for this elevated risk, secondary financing rates are inherently higher than primary mortgage rates.

In the 2026 financial landscape, rates are heavily influenced by the Bank of Canada policy decisions. Fixed-rate equity loans offer protection against market volatility, while variable-rate HELOCs fluctuate with the prime lending rate. When evaluating these options, borrowers must also consider the impact of compounding frequency on their total cost of borrowing over time.

Beyond interest, securing additional financing involves several upfront administrative costs. Borrowers should budget for an independent property appraisal ($300 to $600) to confirm current market value. Legal fees for document processing and title registration typically range from $800 to $1,500. Additionally, lenders may require title insurance, which generally costs between 0.5% and 1% of the total loan amount. Proper planning ensures these fees do not unexpectedly diminish your usable capital.

Strategic Uses for Your Property’s Equity

Transforming illiquid property value into accessible cash opens numerous avenues for wealth building and financial stabilization. The most common and mathematically advantageous use of secondary financing is debt consolidation. By replacing multiple high-interest credit card balances (often carrying rates of 19% to 25%) with a single, lower-rate secured loan, homeowners can drastically reduce their monthly obligations.

Data from the Financial Consumer Agency of Canada indicates that strategic debt consolidation can reduce monthly debt servicing costs by up to 40% for the average household. This approach not only simplifies budgeting but also accelerates the timeline to becoming debt-free.

Property upgrades represent another highly effective use of funds. Investing in modernizing kitchens, developing basements, or improving energy efficiency often yields a high return on investment (ROI), simultaneously increasing your living standard and boosting the home’s resale value. For self-employed individuals, leveraging equity can provide crucial alternative financing for business owners who need capital for inventory, equipment, or expansion but face strict criteria from traditional commercial lenders.

Furthermore, equity can be utilized to navigate complex life transitions, such as managing spousal buyouts during a separation, allowing one party to retain the family home while fairly compensating the other.

Step-by-Step: How to Apply for Additional Property Financing

Securing a subordinate loan involves a structured evaluation process. Lenders will scrutinize your financial health using the ‘Five Cs of Credit’: Character, Capacity, Capital, Collateral, and Conditions. Here is the standard process for 2026:

- Assess Your Equity Position: Calculate your estimated LTV. Ensure you have at least 20% equity remaining in the property after accounting for the new loan.

- Gather Documentation: Lenders require proof of income, recent tax assessments, current mortgage statements, and property tax bills. Start gathering your required paperwork early to prevent processing delays.

- Evaluate Debt Service Ratios: Lenders will calculate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios to ensure you can comfortably manage dual mortgage payments.

- Compare Lender Offers: Do not settle for the first offer. Compare rates, terms, and prepayment penalties across traditional banks, credit unions, and alternative lenders.

- Complete the Appraisal: The lender will order an independent appraisal to verify the home’s current market value.

- Finalize Legal Registration: Once approved, a real estate lawyer will register the new mortgage on your property title and disburse the funds.

Navigating the Risks: Protecting Your Financial Future

While leveraging property value presents significant opportunities, it demands rigorous financial discipline. The primary risk of secondary financing is over-leveraging. Because your home secures the debt, failing to meet repayment obligations on either your primary or secondary loan can lead to severe consequences.

As Marcus Thorne, Lead Financial Analyst at the Alberta Real Estate Institute, explains: ‘Leveraging secondary financing in 2026 requires a strategic approach to debt servicing. Homeowners must stress-test their household budgets against potential economic downturns or sudden interest rate hikes, ensuring they maintain a comfortable buffer.’

If a borrower defaults, the lender has the legal right to initiate foreclosure proceedings to recover their funds. Understanding foreclosure timeline risks is essential before pledging your home as collateral. Furthermore, real estate markets are cyclical. If property values decline significantly, homeowners who have borrowed up to the 80% maximum could find themselves in a negative equity position—owing more than the home is worth.

To mitigate these risks, borrowers should implement aggressive principal reduction strategies whenever possible. Aligning payment schedules with income cycles, setting up automatic transfers, and maintaining an emergency fund equivalent to three months of dual mortgage payments are proven methods for safeguarding your financial stability.

Ultimately, when comparing secondary loans to cash-out refinancing, the right choice depends entirely on your current primary mortgage rate, the penalty to break it, and your long-term financial objectives. Consulting with a licensed mortgage professional ensures you structure the debt in a way that builds wealth rather than jeopardizing it.

Frequently Asked Questions (FAQ)

How is available home equity calculated?

Home equity is calculated by taking your property’s current appraised market value and subtracting the outstanding balance of your primary mortgage. In Canada, lenders typically allow you to borrow up to 80% of the home’s total value, minus your existing debt.

Does a second mortgage replace my first mortgage?

No. A second mortgage is a completely separate loan that sits behind your primary mortgage on the property title. Your original mortgage rate, term, and amortization remain entirely unchanged.

Why are interest rates higher for secondary financing?

Rates are higher because these loans are subordinate liens. If a borrower defaults and the home is sold, the primary mortgage lender is paid in full first, meaning the secondary lender takes on significantly more risk.

Can I use a home equity loan to consolidate credit card debt?

Yes, debt consolidation is one of the most common and effective uses for this type of financing. By paying off high-interest credit cards with a lower-rate secured loan, you can drastically reduce your monthly interest costs and simplify your payments.

What is the difference between a HELOC and a traditional equity loan?

A traditional equity loan provides a single lump sum with fixed monthly payments over a set term. A HELOC is a revolving line of credit that allows you to draw funds as needed, paying variable interest only on the amount you actively use.

What happens if I cannot make payments on my second mortgage?

Defaulting on secondary financing carries the same severe consequences as defaulting on a primary mortgage. The lender has the legal right to initiate foreclosure proceedings to force the sale of the property and recover their funds.

Conclusion

Leveraging your home’s equity through secondary financing is a powerful strategy for achieving major financial milestones in 2026. Whether your goal is to consolidate burdensome high-interest debt, fund a property-enhancing renovation, or secure capital for a business venture, these tools offer flexibility and lower borrowing costs compared to unsecured credit. However, because your home serves as the collateral, it is imperative to approach this financial decision with careful planning, a clear understanding of the costs, and a solid repayment strategy. If you are ready to explore how unlocking your property’s potential can serve your specific financial goals, contact our team today for a personalized assessment.