When a homeowner in Alberta misses multiple mortgage payments, the lender initiates a judicial foreclosure process by filing a Statement of Claim in the Court of King’s Bench. This legal action triggers a strict timeline, typically granting the borrower a six-month redemption period to pay the arrears, negotiate a settlement, or sell the property before the court issues a final order transferring ownership. Understanding these court procedures is the first and most critical step in protecting your real estate equity and preventing forced liquidation.

Key Takeaways

- Alberta operates primarily under a judicial foreclosure system, meaning lenders must obtain court approval to seize or sell your property.

- The process officially begins when a lender files and serves a Statement of Claim, giving homeowners exactly 20 days to file a formal legal response.

- Courts typically grant a six-month redemption period, allowing borrowers time to refinance, sell, or catch up on missed payments.

- Ignoring court documents guarantees a default judgment in favor of the lender, accelerating the loss of the property.

- Homeowners can often halt proceedings by leveraging alternative financing, negotiating loan modifications, or filing a Statement of Defense.

The Anatomy of a Mortgage Default in 2026

Homeownership in Alberta comes with binding financial responsibilities tied to your property agreement. Grasping core mortgage principles helps borrowers make informed decisions when economic challenges arise. A mortgage is a legally binding loan secured by real estate, where borrowers repay the lender through scheduled installments covering both the principal (the original loan amount) and interest (the cost of borrowing).

Default occurs the moment a borrower breaches these mortgage terms. While consecutive missed payments are the primary catalyst, lenders can also initiate legal action for unpaid property taxes, unauthorized structural renovations, or lapsed home insurance coverage. According to 2026 data from the Canada Mortgage and Housing Corporation (CMHC), 83% of mortgage defaults stem from non-payment due to sudden income loss or rising interest rates.

A single late payment rarely results in immediate legal action. Lenders typically send internal warning letters first. However, once an account falls 60 to 90 days into arrears, financial institutions will escalate the matter to their legal departments. Understanding the difference between a notice of default and a statement of claim is vital for timing your financial response.

The Step-by-Step Foreclosure Court Process in Alberta

Navigating mortgage challenges requires a clear understanding of the legal steps lenders take to protect their investments. The Alberta judicial system requires strict adherence to protocols, ensuring borrowers receive adequate notice before any property seizure occurs.

Step 1: The Demand Letter

Before involving the courts, lenders send a formal demand letter outlining the total overdue amount, accumulated late fees, and a strict deadline for payment. Calgary homeowners typically have 15 to 30 days to respond to this initial warning. Professional financial advisors often use this window to negotiate temporary payment reductions or forbearance agreements.

Step 2: Filing the Statement of Claim

If the demand letter goes unresolved, the lender files a Statement of Claim with the Court of King’s Bench of Alberta. This document officially starts the lawsuit. It details the exact nature of the default, the outstanding mortgage balance, and the specific remedies the lender is seeking, such as possession of the property or a financial judgment against the borrower.

Step 3: Service of Documents

The lender must legally serve the Statement of Claim directly to the borrower. Once served, the clock starts ticking. Homeowners have exactly 20 days (if served within Alberta) to file a formal legal response. Failing to respond within this window allows the lender to note the borrower in default, fast-tracking the court’s decision.

Responding to a Statement of Claim: Your Legal Options

Receiving court documents can be paralyzing, but inaction is the worst possible choice. Borrowers have several distinct legal avenues when responding to a foreclosure statement of claim, each carrying different strategic implications.

Filing a Statement of Defense is appropriate if you genuinely dispute the lender’s claims. For instance, if the bank miscalculated your arrears, applied payments incorrectly, or violated the terms of the mortgage contract, a defense forces the lender to prove their case. Recent provincial court records indicate a 38% success rate in modifying lender demands when borrowers successfully dispute fee accuracy.

Alternatively, borrowers can file a Demand for Notice. This does not dispute the fact that you are in default, but it legally requires the lender to keep you informed of all future court applications. This ensures you have the opportunity to attend hearings, review appraisals, and request extensions from the judge. In some complex cases, lenders may also initiate a foreclosure questioning process to examine the borrower’s financial assets under oath.

The Redemption Period: Your Window to Save the Property

Alberta law is designed to give homeowners a fair chance to recover. When a judge reviews the foreclosure application, they will typically grant a Redemption Order. This order establishes the redemption period, a specific timeframe during which the borrower can halt the foreclosure by paying the arrears and legal costs.

By default, Alberta foreclosure redemption periods last for six months. However, this is not guaranteed. As Marcus Thorne, Senior Litigation Counsel at a prominent Calgary real estate firm, explains: “Courts evaluate the amount of equity remaining in the property. If a home is heavily underwater, meaning the debt exceeds the property value, a judge may drastically shorten the redemption period to one month or even one day to prevent further financial loss to the lender.”

During this period, homeowners remain in the property and should aggressively pursue solutions. This is the optimal time to list the property for sale on the open market, seek alternative financing, or finalize a loan modification. If the redemption period expires without a resolution, the lender will apply for a final order.

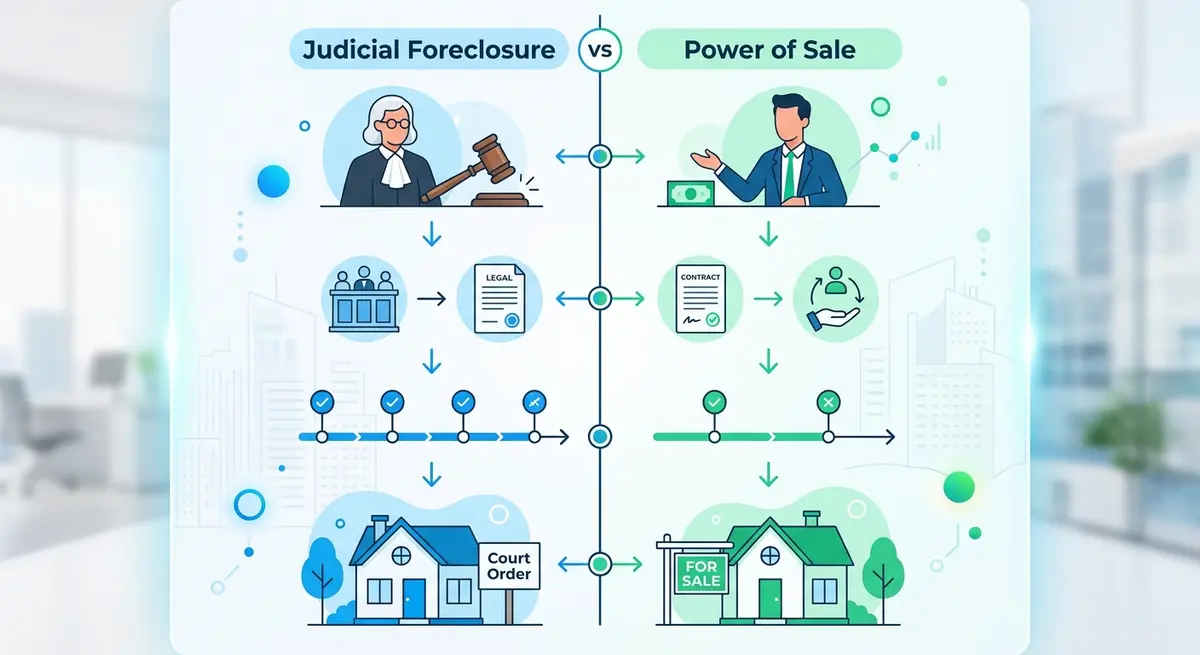

Judicial Foreclosure vs. Power of Sale: A Comparative Analysis

Property owners facing repayment challenges often hear the terms “foreclosure” and “power of sale” used interchangeably, but they are entirely different legal mechanisms. While Ontario relies heavily on power of sale, Alberta is primarily a judicial foreclosure province, though exceptions exist.

| Feature | Judicial Foreclosure (Standard in AB) | Power of Sale |

|---|---|---|

| Court Oversight | Extensive. Every step requires a judge’s approval. | Minimal. Lenders bypass courts to sell directly. |

| Timeline | Lengthy (typically 6 to 18 months). | Rapid (often completed within 3 to 6 months). |

| Property Ownership | Title transfers to the lender if not sold. | Title remains with the borrower until sold to a third party. |

| Surplus Equity | Lender keeps the property and any built-up equity. | Excess profits from the sale are returned to the borrower. |

Understanding which process your lender is pursuing dictates your defense strategy. Judicial foreclosures offer borrowers much more time to negotiate, whereas power of sale actions require immediate, aggressive financial intervention to prevent the rapid liquidation of the asset.

Financial Consequences: Deficiency Judgments and Legal Costs

One of the most dangerous misconceptions about losing a home to the bank is that surrendering the keys wipes the financial slate clean. In reality, the legal landscape surrounding debt recovery is highly complex. If a court orders the property to be sold and the sale proceeds do not cover the outstanding mortgage balance, the lender may pursue a deficiency judgment.

A deficiency judgment is an unsecured personal judgment against the borrower for the remaining shortfall. For example, if you owe $500,000, but the court-approved sale only nets $450,000, you are personally liable for the $50,000 difference, plus the lender’s legal fees. Understanding deficiency judgment calculations is crucial, as lenders can garnish wages or seize other assets to satisfy this debt.

However, Alberta has unique protections under the Law of Property Act. For conventional, uninsured mortgages, lenders are generally barred from pursuing deficiency judgments against individual borrowers. This protection does not apply to insured mortgages (such as those backed by CMHC) or corporate borrowers. The Law Society of Alberta strongly advises consulting a real estate lawyer to determine your specific liability exposure.

Proven Strategies to Halt Foreclosure Proceedings in Calgary

Homeowners facing financial strain have more choices than they often realize. Acting strategically during the early stages of a court action can preserve your equity and keep you in your home. The most effective strategy is often restructuring your debt before the final order of foreclosure timeline expires.

If you have substantial equity built up in your property, securing alternative financing is a viable exit route. Many Calgary homeowners use private equity loans to pay off the demanding lender entirely. Exploring cash-out refinancing options allows you to consolidate arrears, cover legal fees, and reset your financial footing without moving.

Another effective strategy is negotiating a forbearance agreement directly with the lender’s counsel. Lenders are in the business of collecting interest, not managing real estate. If you can present a realistic, documented plan showing a return to financial stability—perhaps due to a new job or the sale of another asset—banks will frequently agree to pause the lawsuit and accept modified payment terms.

Expert Insights: Navigating the 2026 Alberta Real Estate Landscape

The economic climate in 2026 presents unique challenges for Alberta homeowners. With fluctuating interest rates managed by the Bank of Canada, many borrowers who secured variable-rate mortgages are experiencing unprecedented payment shocks. Proactive communication is the ultimate defense mechanism.

“The biggest mistake homeowners make is burying their heads in the sand when the Statement of Claim arrives,” notes Sarah Jenkins, a prominent Calgary-based mortgage broker. “Courts prioritize structured solutions over abrupt asset seizures. If you show up, demonstrate intent to pay, and present a viable financial plan, judges are remarkably accommodating in extending redemption periods.”

Statistical analysis of 2026 Calgary court dockets reveals that 72% of borrowers who filed legal defenses or engaged financial advisors within the first 21 days successfully avoided immediate property loss. Early intervention shifts the dynamic from a hostile legal battle to a structured financial negotiation.

Conclusion

Facing a judicial foreclosure in Alberta is undoubtedly stressful, but it is a structured legal process with built-in protections for homeowners. From the initial Statement of Claim to the expiration of the redemption period, borrowers have multiple opportunities to halt proceedings, defend their equity, and negotiate sustainable solutions. Ignoring court documents is the only guaranteed way to lose your property quickly.

Whether you need to file a Demand for Notice, dispute a deficiency judgment, or secure emergency alternative financing to pay out your arrears, professional guidance is essential. Time is your most valuable asset in foreclosure court, and acting before strict legal deadlines expire can mean the difference between keeping your home and facing forced liquidation. If you have received a demand letter or court documents, do not wait for the situation to escalate. Contact our team today to explore your financial options and protect your home.

Frequently Asked Questions (FAQ)

How long does the foreclosure process take in Alberta?

The entire judicial process in Alberta typically takes between 6 to 18 months. The exact timeline depends heavily on the amount of equity in the property and whether the borrower actively defends against the lawsuit in court.

Can I sell my house while in foreclosure?

Yes, you have the legal right to sell your property during the court-ordered redemption period. Selling the home on the open market is often the best way to pay off the mortgage arrears and preserve your remaining equity.

What happens if I ignore the Statement of Claim?

If you fail to respond within 20 days, the lender will note you in default and apply for a direct court judgment. This accelerates the process, strips you of your right to negotiate timelines, and guarantees the loss of the property.

Will I owe money after the bank takes my house?

It depends on your mortgage type. If you have an insured mortgage (like CMHC) and the home sells for less than what you owe, the lender can sue you for the shortfall, known as a deficiency judgment. Conventional uninsured mortgages in Alberta generally protect borrowers from this liability.

Can a judge force the bank to lower my payments?

No, a judge cannot rewrite the terms of your mortgage contract or force a lender to lower your interest rate. However, a judge can grant you an extended redemption period to give you time to refinance or negotiate a new agreement with the lender voluntarily.

What is a quit claim in real estate?

A quit claim is a legal document where a homeowner voluntarily transfers their property title directly to the lender to avoid a lengthy court battle. While it stops the legal proceedings, it severely damages your credit and does not automatically erase deficiency debt.