Facing financial hurdles with your home or property? There’s an option many Calgarians explore to avoid lengthy legal processes. This strategy allows homeowners to transfer ownership directly to their lender, offering a smoother exit than traditional methods.

Facing financial hurdles with your home or property? There’s an option many Calgarians explore to avoid lengthy legal processes. This strategy allows homeowners to transfer ownership directly to their lender, offering a smoother exit than traditional methods.

Unlike foreclosure, which involves court proceedings and credit damage, this approach prioritizes mutual agreement. Lenders often prefer it because it reduces costs, while homeowners gain control over the outcome. Terms like mortgage obligations and loan agreements play a central role here, shaping how these decisions unfold.

This guide breaks down the essentials, helping you understand your options during tough financial times. Whether you’re a first-time buyer or an investor, clarity empowers smarter real estate choices. Local experts like The Second Mortgage Store in Calgary, AB, Canada, offer tailored advice for these situations—reach them at +1 403-827-6630.

Below, we’ll explore how this process works, its benefits, and steps to take. Knowledge is your strongest tool when navigating complex property matters.

Key Takeaways

- Transferring ownership voluntarily can prevent foreclosure’s credit impact.

- Lenders and homeowners benefit from reduced costs and faster resolutions.

- Mortgage terms directly influence eligibility for this option.

- Local professionals provide critical guidance for Calgary residents.

- Understanding rights and obligations leads to better financial outcomes.

What is a Deed in Lieu of Foreclosure Calgary?

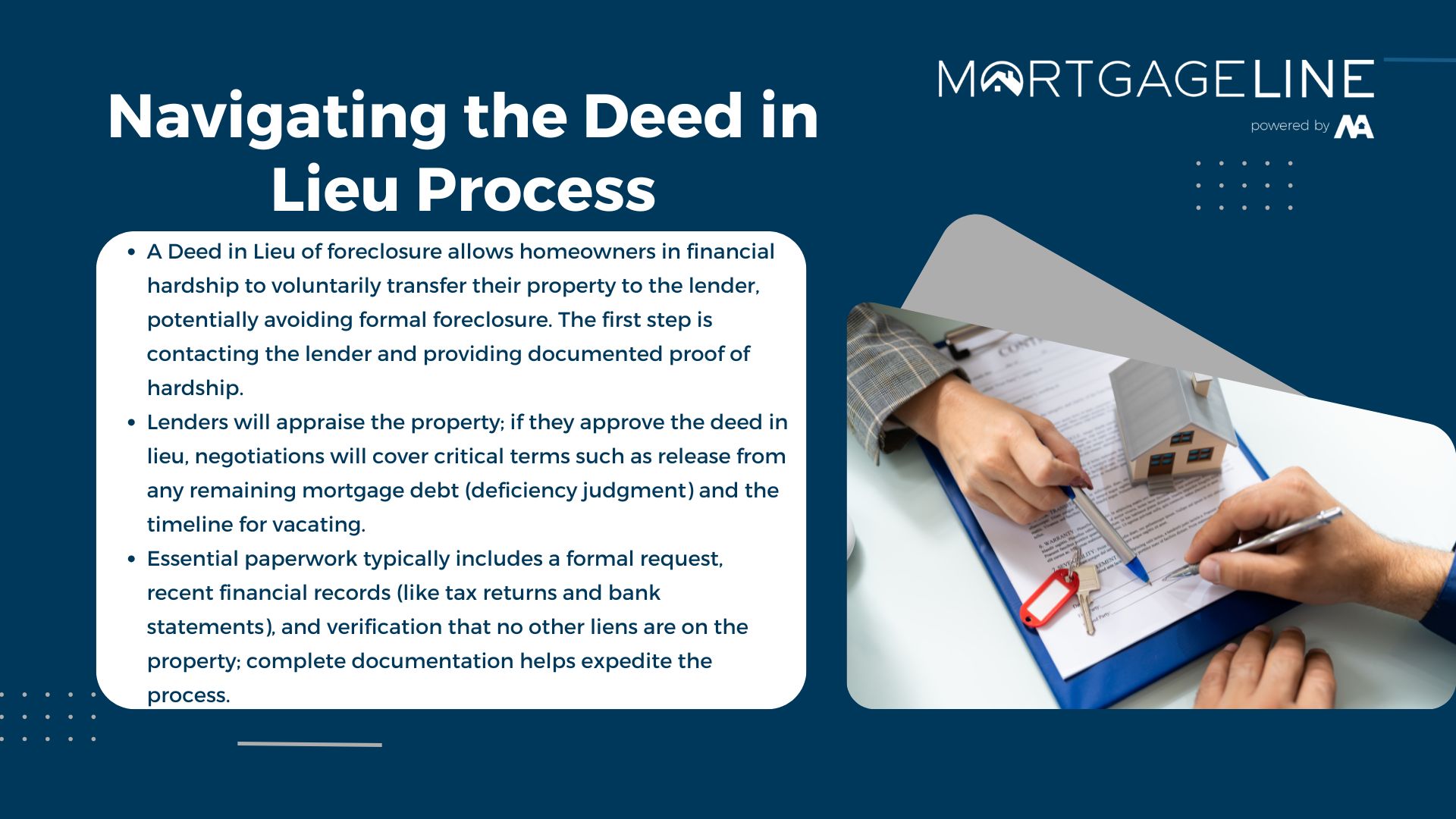

When mortgage payments become unsustainable, homeowners in Calgary may explore alternatives to avoid prolonged legal battles. A deed in lieu of foreclosure allows property owners to voluntarily transfer ownership to their financial institution. This mutual agreement streamlines resolution while minimizing stress for both parties.

Defining the Process and Legal Implications

Under this arrangement, lenders accept full property rights instead of pursuing repayment through courts. Homeowners must prove they can’t meet obligations and surrender the estate free of liens. Legal documentation ensures all claims are settled, though tax implications or deficiency judgments may apply in some cases.

How It Differs from Traditional Foreclosure

Traditional foreclosure involves public auctions and court oversight, often lasting months. A deed in lieu skips these steps, creating a faster exit strategy. Credit reports reflect these events differently—foreclosures typically lower scores by 100-150 points, while voluntary transfers show less severe impacts.

| Factor | Deed in Lieu | Foreclosure |

|---|---|---|

| Timeline | 4-8 weeks | 6-18 months |

| Credit Impact | Moderate | Severe |

| Legal Costs | Low | High |

Calgary’s real estate professionals, like The Second Mortgage Store, often recommend this path when clients face irreversible financial strain. Their team at +1 403-827-6630 helps navigate lender requirements and local market nuances.

Navigating the Deed in Lieu Process in Calgary

Managing overwhelming mortgage obligations requires a clear roadmap. Calgary homeowners can navigate this path efficiently by following structured steps and gathering essential records. Local experts like The Second Mortgage Store emphasize preparation to streamline interactions with financial institutions.

Step-by-Step Process Overview

Begin by contacting your bank to discuss eligibility. Most lenders require proof of financial hardship, such as income statements or job loss documentation. You’ll need to submit 3–6 months of payment records to demonstrate consistent struggles.

Next, lenders assess the property’s value through an appraisal. If equity aligns with outstanding balances, they may approve the transfer. Negotiations often involve clarifying terms like release from deficiency judgments or timelines for vacating the property.

Key Documentation and Lender Requirements

Essential paperwork includes a formal request letter, recent tax returns, and bank statements. Lenders also verify that no secondary liens exist on the home. Missing documents delay the process—organize files early to save time.

Timing matters. Banks typically resolve these cases faster than foreclosures, but deadlines vary. For example, one major Calgary lender finalizes agreements within 45 days if paperwork is complete. Always review money-related clauses, such as waived fees or repayment plans for residual debts.

| Requirement | Purpose | Timeframe |

|---|---|---|

| Payment History | Prove financial hardship | 3–6 months |

| Property Appraisal | Assess market value | 1–2 weeks |

| Debt Clearance | Confirm no other liens | 7–10 days |

The Second Mortgage Store advises clients to “approach negotiations transparently—banks prefer solutions that minimize losses.” Their team helps homeowners present cases persuasively, balancing legal obligations with practical outcomes.

Benefits and Considerations for Homeowners

Exploring alternatives to foreclosure can lead to unexpected financial advantages. While transferring ownership to a lender isn’t ideal, it offers structured solutions for those facing unsustainable obligations. Below, we break down key factors influencing this decision.

Impact on Credit and Financial Health

Opting for this route typically lowers credit scores by 50–100 points—less severe than the 100–150-point drop from foreclosure. While both stay on reports for seven years, lenders view voluntary transfers as more responsible. This distinction helps rebuild financial stability faster.

Loan Forgiveness and Debt Relief Opportunities

Some institutions waive portions of unpaid balances, reducing overall debt. For example, a homeowner owing $300k might negotiate $275k as final settlement. However, tax implications could apply to forgiven amounts. Always consult professionals to clarify obligations.

Cost, Time Savings, and Long-Term Effects

Completing the process in 4–8 weeks saves months compared to foreclosure. Homeowners often avoid court fees, auction costs, and prolonged stress. Long-term benefits include:

- Faster eligibility for future loans (3–4 years vs. 5–7)

- Preserved ability to rent or invest elsewhere

- Reduced emotional strain from drawn-out proceedings

| Factor | Short-Term Benefit | Long-Term Advantage |

|---|---|---|

| Credit Recovery | Moderate score drop | Faster rebuilding |

| Financial Flexibility | Immediate debt relief | Improved borrowing power |

| Time Investment | Weeks, not months | Earlier financial reset |

The Second Mortgage Store notes, “Transparency with lenders often yields better terms—many prioritize minimizing losses over punitive measures.” Their team helps clients present cases strategically, balancing immediate needs with future goals.

Alternatives and Additional Options to Foreclosure

When mortgage struggles arise, exploring alternatives can provide financial breathing room. Loan adjustments and negotiated sales often help homeowners regain stability while minimizing long-term consequences. Let’s examine two practical paths forward.

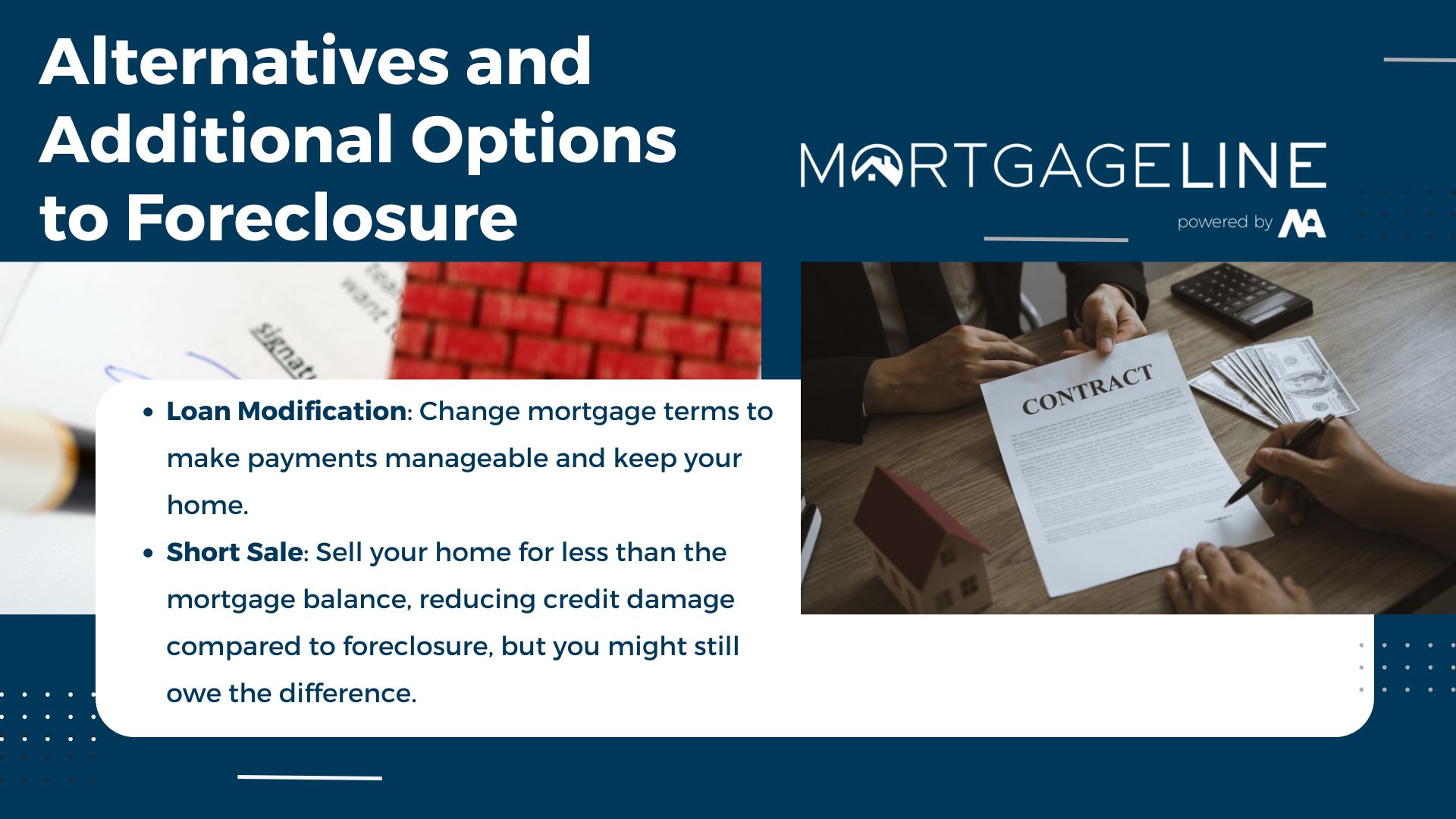

Exploring Loan Modification Options

Restructuring payment terms offers a way to keep your home. Lenders might reduce interest rates, extend loan durations, or adjust monthly amounts owed. For example, a Calgary homeowner reduced payments by $450/month through a 2% rate cut and 10-year term extension.

- Pros: Avoid moving, preserve equity, and stabilize budgets

- Cons: May require upfront fees or extend total debt period

Understanding Short Sale as an Alternative

A short sale occurs when lenders permit selling the property for less than the owed amount. While this requires buyer negotiations, it typically impacts credit scores 30–40 points less than foreclosure. However, deficiency judgments could still apply if sale proceeds don’t cover the full debt.

| Option | Credit Impact | Debt Resolution |

|---|---|---|

| Foreclosure | -150 points | Full balance due |

| Deed in Lieu | -100 points | Partial forgiveness |

| Short Sale | -60 points | Case-dependent |

The Second Mortgage Store advises: “Evaluate court timelines and sale conditions early. A $50k deficiency might be manageable through installment plans, but $200k could warrant different strategies.” Their team helps clients weigh credit recovery timelines against immediate cash needs.

Insights from Lenders and Industry Professionals

Financial institutions evaluate several critical factors when homeowners propose alternative solutions. Understanding these criteria helps streamline negotiations and increases approval chances.

Key Evaluation Metrics for Approval

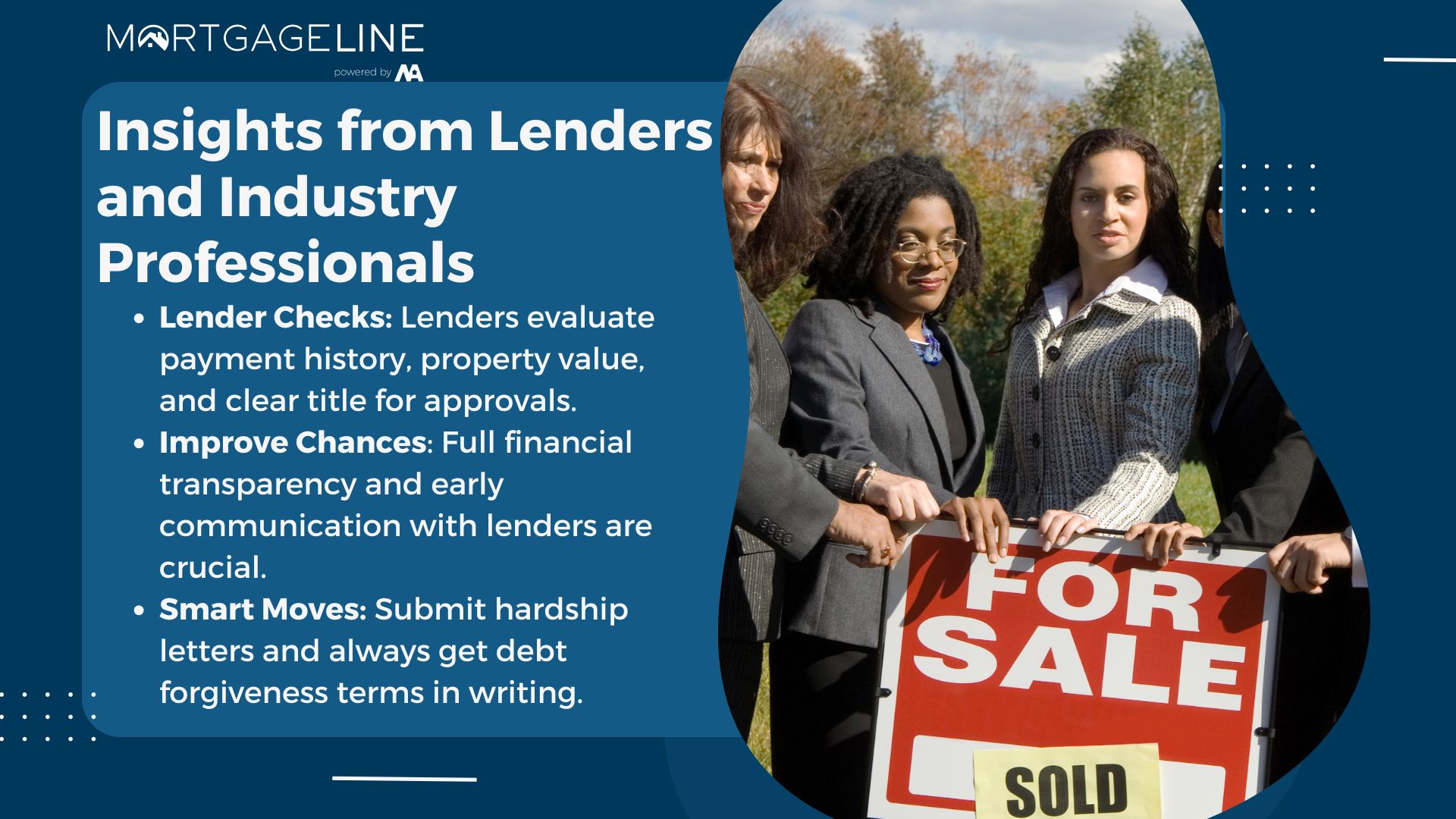

Lenders prioritize three elements when reviewing requests:

- Payment history: Consistent defaults over 3-6 months demonstrate genuine hardship

- Property valuation: Market value must align with outstanding balances

- Clean title: No secondary liens or legal claims on the estate

One major Canadian bank reports approving 68% of cases where homeowners provide complete financial records upfront. “We look for transparency,” explains a mortgage manager. “Missing tax documents or vague explanations often delay proceedings.”

Strategic Guidance for Successful Agreements

The Second Mortgage Store emphasizes proactive communication with lenders. Their experts recommend:

- Preparing a hardship letter detailing income changes

- Calculating residual balances using current appraisal data

- Requesting written confirmation of debt forgiveness terms

“Timing matters. Submitting requests before multiple defaults shows responsibility and improves lender confidence.”

For personalized assistance navigating these requirements, contact their Calgary office at +1 403-827-6630. Their specialists help structure proposals that address both financial realities and lender priorities.

Conclusion

Navigating property challenges requires balancing financial realities with practical solutions. This guide explored how voluntary ownership transfers offer structured exits from unsustainable obligations, contrasting sharply with drawn-out foreclosure processes. Key factors like credit recovery timelines, lender negotiations, and market valuations shape these decisions.

Choosing this alternative often hinges on specific conditions—clear titles, documented hardships, and alignment with lender criteria. Compared to traditional methods, it preserves more financial flexibility while reducing legal costs. Recent market trends show Calgary homeowners increasingly prioritize such agreements to protect long-term stability.

Before proceeding, verify your property’s legal standing and physical condition. Case studies reveal that early expert involvement leads to better outcomes. The Second Mortgage Store specializes in tailoring strategies to local finance landscapes, helping clients navigate complex scenarios efficiently.

Evaluate all options carefully. For personalized guidance on title reviews or debt relief alternatives, contact The Second Mortgage Store at +1 403-827-6630. Their team transforms overwhelming challenges into actionable plans—because informed choices build stronger futures.