Buying a home in Calgary is an exciting milestone, but navigating financing options can feel overwhelming. For those with a down payment below 20%, securing mortgage default insurance is often essential. This protection allows lenders to offer loans to buyers who might otherwise struggle to qualify, making homeownership more accessible.

Buying a home in Calgary is an exciting milestone, but navigating financing options can feel overwhelming. For those with a down payment below 20%, securing mortgage default insurance is often essential. This protection allows lenders to offer loans to buyers who might otherwise struggle to qualify, making homeownership more accessible.

As a trusted provider in Calgary, AB, The Second Mortgage Store specializes in guiding clients through this process. Their team at +1 403-827-6630 combines local market expertise with personalized solutions, ensuring buyers understand their options. Default insurance isn’t just about lender security—it’s a tool that unlocks opportunities for aspiring homeowners.

Why is this coverage so critical? Without it, many lenders cannot approve loans for smaller down payments. This insurance acts as a safety net, reducing risk while helping buyers enter the housing market sooner. For Calgary residents, working with professionals who know the area’s trends ensures tailored advice for every situation.

Key Takeaways

- Mortgage default insurance protects lenders when down payments are under 20%.

- It enables buyers to purchase a home with as little as 5% down.

- Calgary-based experts like The Second Mortgage Store simplify the process.

- Local insights ensure strategies align with market conditions.

- This coverage expands access to financing for qualified buyers.

Introduction to Mortgage Default Insurance

For many aspiring homeowners, securing financing hinges on understanding protective measures like mortgage default insurance. This coverage bridges the gap for buyers with limited savings, enabling them to enter the market confidently.

What Is Mortgage Default Insurance?

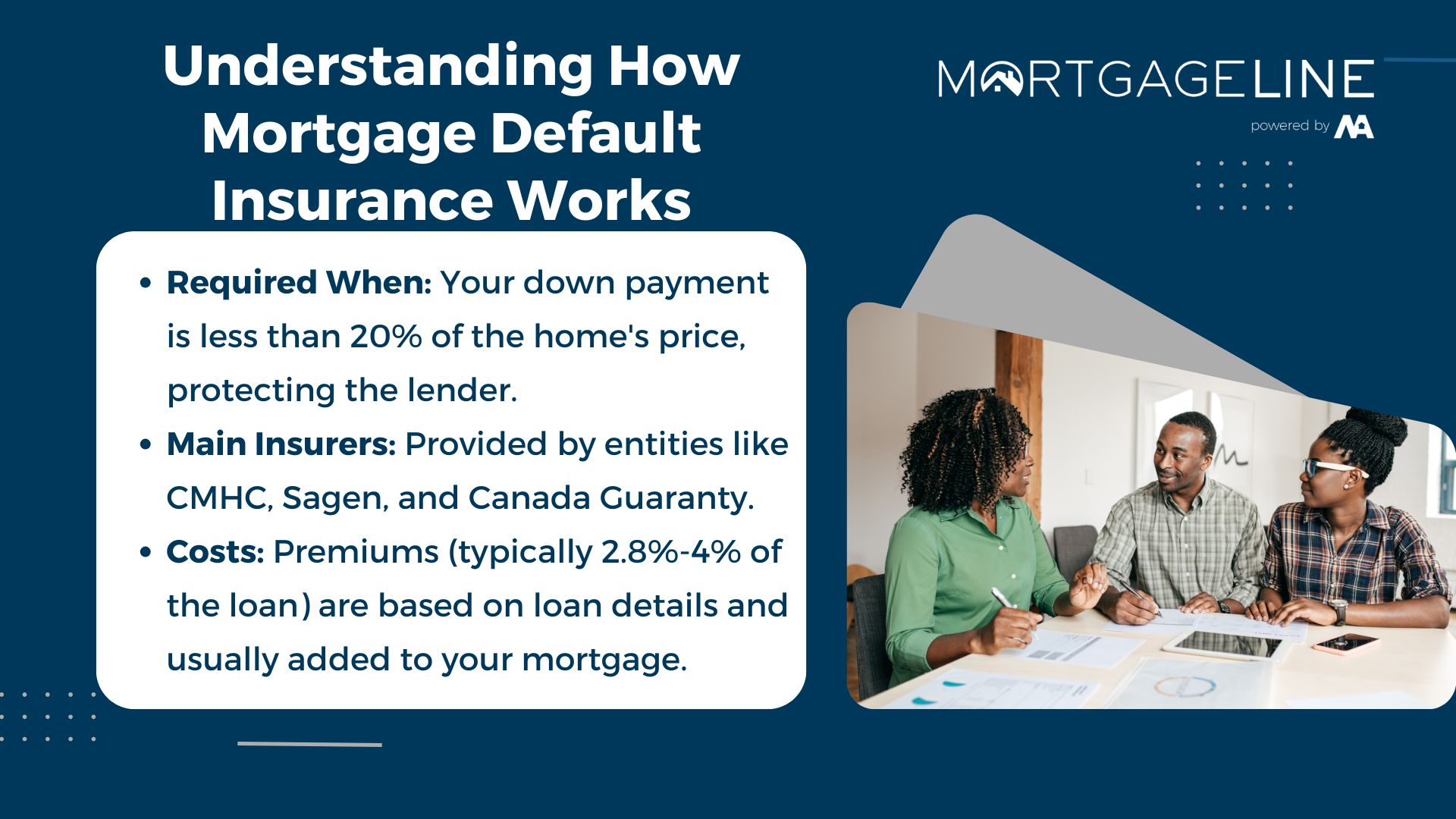

Mortgage default insurance protects lenders if a borrower fails to make payments. Unlike mortgage protection insurance (which covers personal circumstances like job loss), this policy focuses on lender security. It’s mandatory for high-ratio loans where the down payment is below 20% of the purchase price.

| Down Payment Range | Loan-to-Value Ratio | Premium Rate |

|---|---|---|

| 5% – 9.99% | 90% – 95% | 4.00% |

| 10% – 14.99% | 85% – 89.99% | 3.10% |

| 15% – 19.99% | 80% – 84.99% | 2.80% |

Why It Matters for Calgary Homebuyers

In competitive markets like Calgary, smaller down payments help buyers act quickly. Default insurance makes this possible by reducing lender risk. For example, a $400,000 home with a 10% down payment requires coverage, ensuring approval despite lower upfront funds.

The insurance premium is added to the mortgage at closing. This spreads costs over time while keeping initial expenses manageable. Local experts emphasize its role in balancing affordability with lender requirements.

Understanding How Mortgage Default Insurance Works Calgary

Securing a home often starts with understanding financial safeguards. When a down payment represents less than 20% of a property’s value, lenders require protective coverage. This rule applies nationwide, including in dynamic markets like Alberta.

When Is Coverage Required?

A high-ratio loan occurs when the loan-to-value ratio exceeds 80%. For example, a $500,000 purchase with 10% down leaves 90% financed. In such cases, coverage becomes mandatory to protect lenders from potential defaults.

“High-ratio loans account for nearly 40% of first-time buyer transactions in Canada,” notes a CMHC housing report.

Leading Providers in the Industry

Three organizations dominate this sector:

| Provider | Founded | Maximum Coverage |

|---|---|---|

| Canada Mortgage Housing Corporation (CMHC) | 1946 | 95% LTV |

| Sagen | 1995 | 95% LTV |

| Canada Guaranty | 2010 | 95% LTV |

The Canada Mortgage Housing Corporation, a federal crown corporation, sets industry standards. Private firms like Sagen and Canada Guaranty offer competitive premium structures. All providers use similar criteria when calculating costs:

- Purchase price

- Loan-to-value ratio

- Property type

Premiums typically range from 2.8% to 4% of the loan amount. These fees get added to the principal balance, allowing gradual repayment. Working with knowledgeable professionals helps buyers navigate these requirements efficiently.

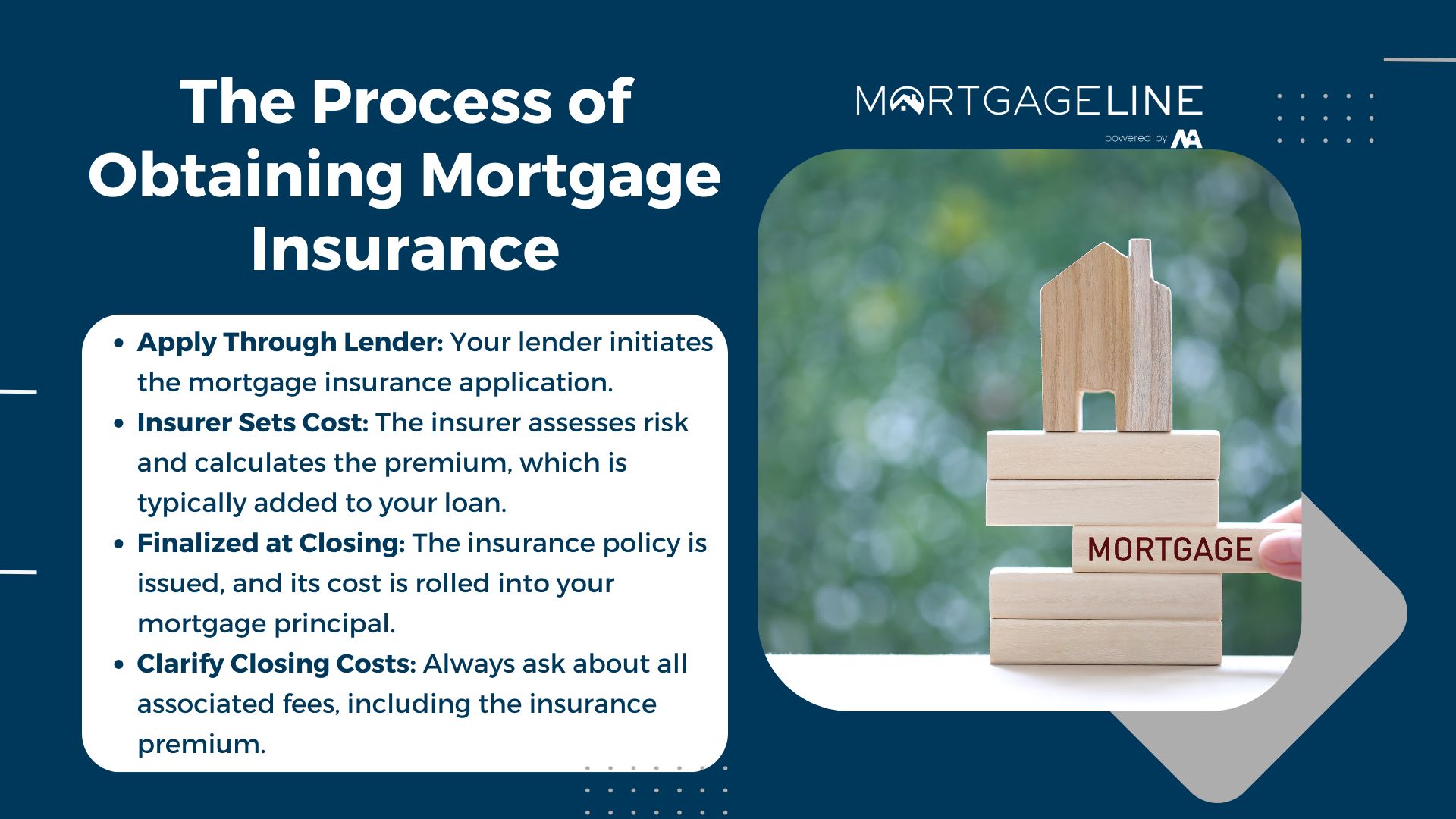

The Process of Obtaining Mortgage Insurance

Navigating the path to homeownership involves several key steps, one of which is securing the necessary protection for your loan. This process requires collaboration between borrowers, lenders, and insurers to ensure smooth transactions.

Steps to Secure Your Coverage

To get mortgage protection, follow these steps:

- Apply Through Your Lender: Most financial institutions handle insurance requests directly. Submit income verification, credit reports, and property details.

- Review Premium Calculations: Insurers determine costs based on loan-to-value ratios. A 10% down payment typically results in a 3.1% premium.

- Finalize at Closing: The premium gets added to your principal balance, spreading payments over the loan term.

“Lenders act as intermediaries, streamlining approvals while insurers assess risk profiles,” explains a senior advisor at Sagen.

Roles of Lenders and Insurers

Lenders initiate coverage requests and verify borrower eligibility. Insurers evaluate applications and set rates. Both parties ensure compliance with federal guidelines.

| Stage | Lender Responsibility | Insurer Responsibility |

|---|---|---|

| Application | Collect documents | Review credit history |

| Approval | Confirm down payment | Calculate premium |

| Closing | Add costs to loan | Issue policy |

If payments stop, default insurance protects lenders by covering losses. Legal proceedings may follow, but this safeguard minimizes financial exposure. Always ask about closing costs upfront—they often include appraisal fees and legal expenses.

Calculating the Mortgage Default Insurance Premium

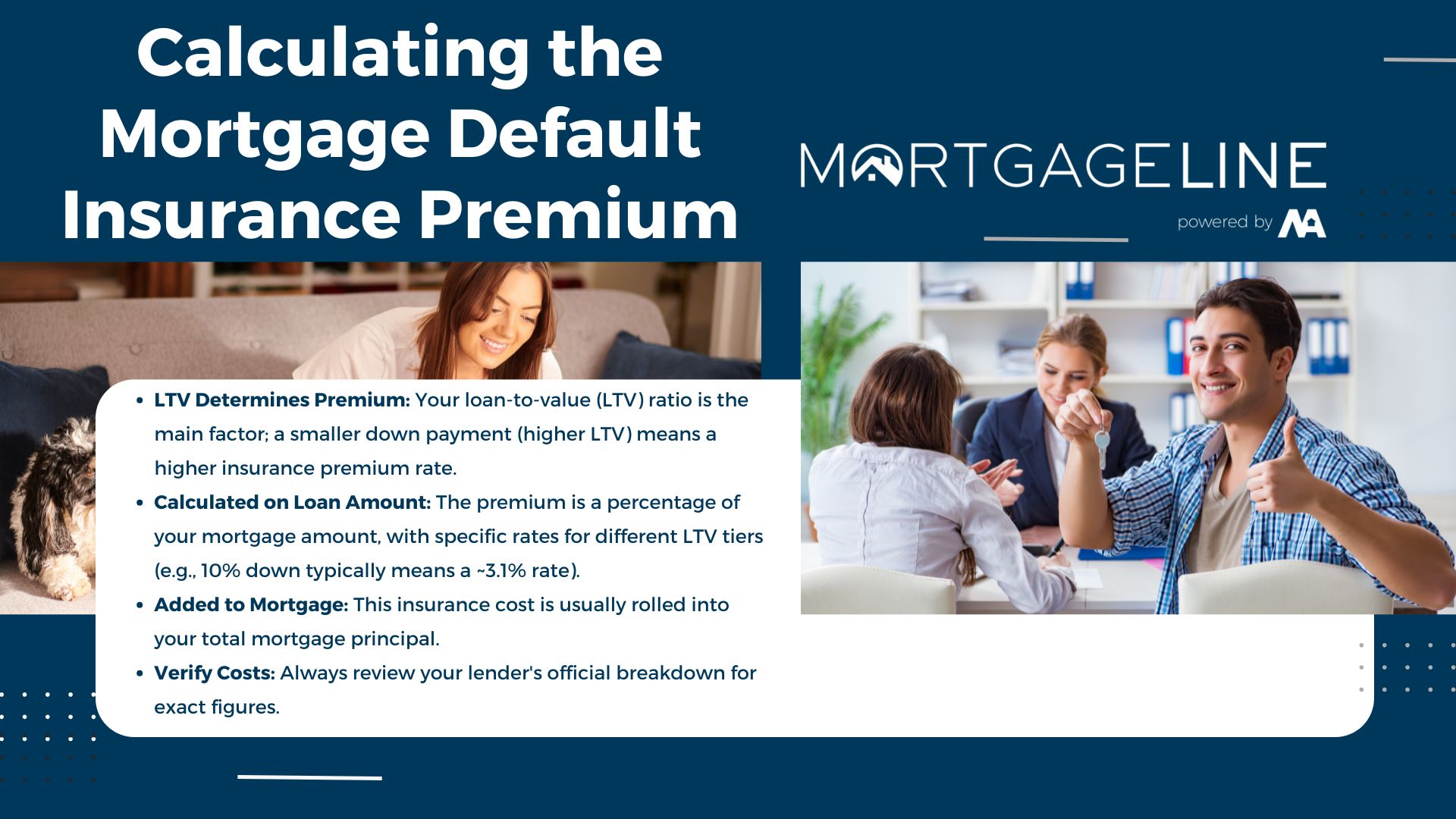

Determining the cost of protective coverage starts with mastering a few key numbers. Premiums depend on your loan’s risk level, which lenders measure using specific financial metrics. Let’s break down the critical components that shape these calculations.

Loan-to-Value Ratio Explained

The loan-to-value (LTV) ratio compares your borrowed amount to the property’s value. A higher ratio means more lender risk, which increases premium rates. For example:

- A $500,000 home with 10% down leaves a $450,000 balance.

- LTV = ($450,000 ÷ $500,000) × 100 = 90%.

Insurers charge higher percentages as LTV rises. This directly impacts your upfront and long-term costs.

A Step-by-Step Calculation Example

Consider a $500,000 purchase with 10% down:

- Down Payment: $50,000 (10% of purchase price).

- Borrowed Amount: $450,000.

- Premium Rate: 3.1% for 90% LTV.

- Premium Cost: $450,000 × 3.1% = $13,950.

This $13,950 gets added to your principal, increasing total borrowing to $463,950. Over 25 years at 5% interest, this adds roughly $82 monthly.

| Down Payment | LTV Range | Premium Rate |

|---|---|---|

| 5% – 9.99% | 90% – 95% | 4.00% |

| 10% – 14.99% | 85% – 89.99% | 3.10% |

| 15% – 19.99% | 80% – 84.99% | 2.80% |

Interest rates and tax implications can slightly adjust final costs. Always review your lender’s breakdown to avoid surprises.

Navigating Costs and Payment Options

Understanding where your money goes during a home purchase helps avoid surprises. While protective coverage fees often blend into loan balances, other expenses demand immediate attention. Let’s clarify how these financial pieces fit together.

Integrating Premiums Into Your Mortgage

Protective coverage fees get rolled into your loan balance rather than paid upfront. For example, a $13,950 premium on a $450,000 loan increases the principal to $463,950. This spreads repayment over your term, keeping initial cash requirements lower.

However, provincial sales tax (PST) and closing costs require separate planning. Alberta charges 0% PST on premiums, but provinces like Ontario apply 8%. Legal fees, appraisals, and land transfer taxes also add to upfront expenses.

| Expense Type | Paid Upfront? | Typical Range |

|---|---|---|

| Coverage Premium | No | 2.8% – 4% of loan |

| Provincial Sales Tax | Yes | 0% – 8% of premium |

| Closing Costs | Yes | 1.5% – 4% of price |

Consider these strategies to manage payments:

- Adjust your down payment: A 15% down payment lowers both premiums and monthly payments

- Shorten your amortization: 20-year terms reduce total interest vs. 30-year plans

- Request lender credits: Some institutions offset closing costs

Budgeting for integrated and upfront costs ensures smoother transactions. Always review itemized estimates with your advisor to align expectations with reality.

Tips and Strategies for Calgary Homebuyers

Smart financial planning can turn homeownership dreams into reality, even with limited initial savings. By optimizing your approach to loans and exploring flexible solutions, buyers gain control over long-term costs while meeting lender requirements.

Maximizing Your Down Payment Advantages

Every percentage point saved upfront reduces reliance on protective coverage. For example, increasing a down payment from 10% to 15% on a $400,000 property lowers premiums by 0.3%—saving $3,600 immediately.

- Set up automatic transfers to dedicated savings accounts

- Leverage RRSP withdrawals through the Home Buyers’ Plan

- Explore local grants like Alberta’s Affordable Housing Partnership Program

“A 1% down payment increase often cuts premium rates more than buyers realize,” states a Calgary-based financial planner.

| Down Payment | Premium Rate | Savings vs. 5% Down |

|---|---|---|

| 10% | 3.10% | $5,400 |

| 15% | 2.80% | $9,000 |

| 19% | 2.80% | $9,000 |

Considering Alternative Lending Options

Traditional banks aren’t the only path to financing. Credit unions often provide lower rates for members, while private lenders offer tailored solutions for unique credit situations.

Key alternatives include:

- B-Lenders: Flexible qualifications with slightly higher rates

- Credit Unions: Community-focused rates and terms

- Family Loans: Structured agreements with legal oversight

Improving credit scores by 50 points could qualify you for better terms. Dispute errors on reports and maintain utilization below 30% for optimal results. Shorter loan terms (20 vs. 30 years) also reduce total interest paid, though monthly payments increase slightly.

Conclusion

Strategic financial planning transforms homeownership from aspiration to reality. For buyers with down payments below 20%, mortgage default insurance remains a vital tool, offering lenders security while expanding access to competitive markets. Leading providers like CMHC, Sagen, and Canada Guaranty create stability through standardized policies tailored to diverse needs.

Understanding premium calculations—especially how loan-to-value ratios affect costs—helps optimize upfront investments. Even modest increases in your initial payment can lower long-term expenses. Comparing lenders and exploring regional programs ensures solutions align with your financial goals.

In dynamic markets like Calgary, partnering with local experts provides clarity on tax implications and evolving trends. Their guidance turns complex processes into actionable steps, whether you’re a first-time buyer or seasoned investor. With thorough preparation and informed choices, you’ll navigate financing confidently, turning property dreams into lasting achievements.