When deciding between a second mortgage and refinancing in Calgary, the optimal choice depends entirely on your current primary mortgage rate and the penalty required to break it. A second mortgage allows you to access up to 80% of your home’s equity without touching your low-interest primary loan, making it ideal if you secured a highly favorable rate in previous years. Conversely, refinancing replaces your entire mortgage with a new one at current 2026 market rates, which is typically the superior option if your current rate is high or you need to consolidate massive debts over a longer amortization period.

Key Takeaways

- Preservation of Rates: Second mortgages protect your existing primary mortgage terms, shielding you from higher 2026 base rates on your principal balance.

- Penalty Avoidance: Refinancing often triggers prepayment penalties, such as the Interest Rate Differential (IRD), which must be weighed against long-term interest savings.

- Borrowing Limits: Alberta lenders strictly cap total equity access at 80% Loan-to-Value (LTV) across all combined mortgage products.

- Cost of Capital: While second mortgages carry higher interest rates on the borrowed amount, the blended overall cost may still be lower than refinancing your entire home.

- Speed of Access: Supplemental financing typically closes within days, whereas a full mortgage replacement can take several weeks of underwriting.

Understanding Home Equity Access in Calgary’s 2026 Market

Calgary’s real estate landscape has evolved significantly, transforming how homeowners leverage their property wealth. In 2026, the average detached home price in Calgary surpassed $715,000, creating substantial untapped equity for long-term residents. As property values appreciate, homeowners increasingly view their residences not just as shelter, but as dynamic financial instruments capable of funding business ventures, renovations, or debt consolidation.

According to recent data from the Canadian Real Estate Association (CREA), over 34% of Alberta property owners explored equity extraction methods in the past twelve months. This surge is driven by a combination of rising living costs and the desire to optimize household cash flow. However, accessing this capital requires navigating complex financial products, each with distinct regulatory frameworks and cost structures.

The fundamental metric governing your borrowing power is the Loan-to-Value (LTV) ratio. As defined by financial authorities like Investopedia, LTV compares your total mortgage debt to your property’s appraised value. Canadian federal regulations mandate that homeowners must retain at least 20% equity in their property, meaning your maximum borrowing capacity is capped at 80% LTV, regardless of whether you choose supplemental financing or a complete mortgage overhaul.

What is a Second Mortgage?

A second mortgage is a subordinate lien placed on your property that operates entirely independently of your primary mortgage. This financial instrument allows you to borrow against your accumulated equity while leaving your original loan agreement, including its interest rate and amortization schedule, completely untouched. It is a targeted injection of capital designed for specific financial goals.

These supplemental loans typically take two forms: a fixed-rate home equity loan, which provides a lump sum with predictable monthly payments, or a Home Equity Line of Credit (HELOC), which functions as revolving credit. “In a fluctuating rate environment, the ability to isolate new borrowing from your primary principal is a massive strategic advantage,” explains Dr. Michael Chen, Professor of Finance at the University of Calgary. “It prevents homeowners from unnecessarily exposing their largest debt pool to current market premiums.”

Advantages of Supplemental Financing

The primary benefit of this approach is rate preservation. If you secured a primary mortgage at 2.5% several years ago, breaking that term to access $50,000 in equity would force your entire $400,000 balance into a higher 2026 rate. By utilizing a subordinate loan, only the new $50,000 is subject to current pricing. Furthermore, these products offer exceptional speed; alternative lenders can often fund these requests in a matter of days, providing crucial liquidity for time-sensitive investments.

Drawbacks and Risks

Because the lender holds a secondary position on the property title, they assume higher risk. If the property goes into foreclosure, the primary lender is paid first. To compensate for this risk, interest rates on subordinate financing are inherently higher than primary mortgage rates. Additionally, borrowers must manage two separate monthly payments, which requires disciplined cash flow management. If you are exploring stated income options, expect slightly higher premiums due to the alternative documentation.

What is Mortgage Refinancing?

Refinancing is the process of completely dissolving your existing mortgage contract and replacing it with a new agreement. The new lender pays off your original debt and establishes fresh terms, a new interest rate, and a revised amortization period based on your current financial profile and the 2026 market conditions. When you borrow more than your current outstanding balance to extract cash, it is known as a cash-out refinance.

This strategy is highly effective for structural debt reorganization. If you have accumulated $80,000 in high-interest credit card debt, rolling that balance into a new primary mortgage can drastically reduce your monthly obligations. By spreading the repayment over 25 or 30 years at a mortgage interest rate, your immediate cash flow improves significantly, even though the total interest paid over the life of the loan will increase.

The Cost of Breaking Your Term

The most critical factor in refinancing is the prepayment penalty. According to the Financial Consumer Agency of Canada (FCAC), breaking a fixed-rate mortgage typically incurs a penalty equal to the greater of three months’ interest or the Interest Rate Differential (IRD). In 2026, IRD penalties can easily exceed $10,000 to $15,000, depending on your remaining balance and the gap between your contract rate and current rates.

Before proceeding, you must calculate your “break-even point”—the number of months it will take for your new, lower monthly payments to offset the upfront penalty and legal fees. If you plan to sell the home before reaching this break-even point, refinancing is mathematically disadvantageous. For a deeper dive into how these structures compare, review our cash-out refinancing comparison.

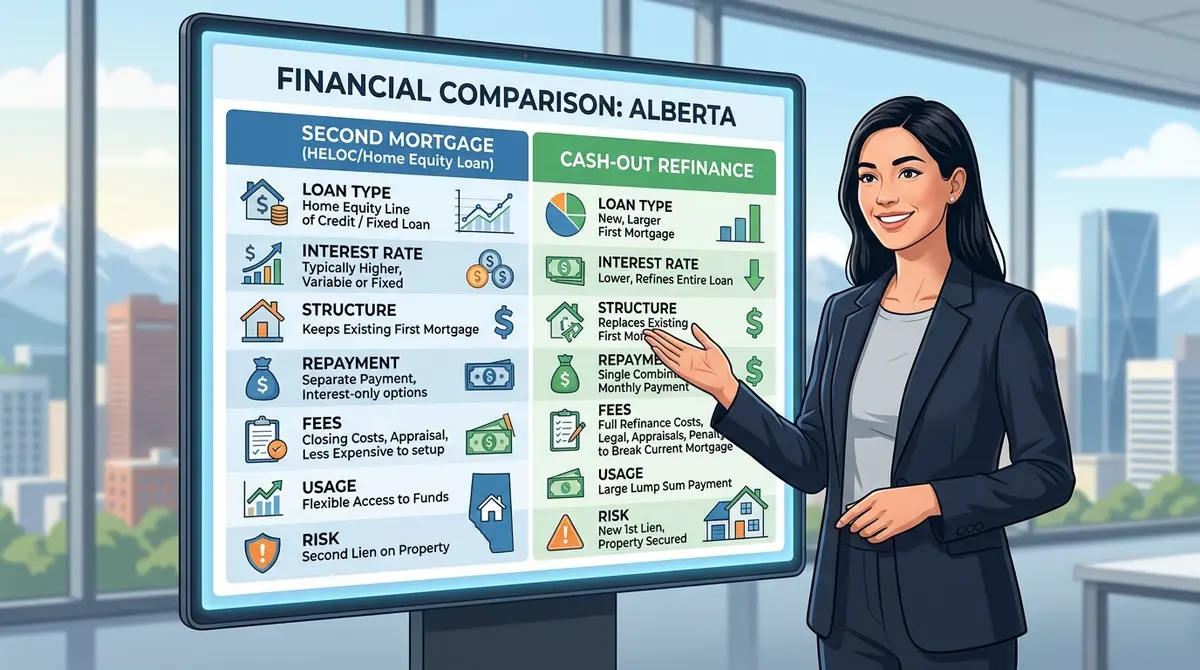

Direct Comparison: Second Mortgage vs. Refinancing

To make an informed decision, homeowners must evaluate how these two distinct paths align with their immediate needs and long-term wealth-building strategies. The table below outlines the core differences between the two approaches in the current Alberta market.

| Feature | Second Mortgage | Refinancing (Cash-Out) |

|---|---|---|

| Impact on Primary Loan | None. Existing rate and terms remain intact. | Replaces entire loan with new 2026 rates. |

| Interest Rates | Higher (reflects secondary lien risk). | Lower (standard primary mortgage rates). |

| Upfront Costs | Lower (appraisal, broker, and legal fees). | Higher (includes massive prepayment penalties). |

| Funding Timeline | Fast (typically 3 to 10 days). | Slow (typically 3 to 6 weeks). |

| Best Used For | Short-term capital, renovations, business funding. | Massive debt consolidation, securing lower overall rates. |

How to Choose the Right Equity Solution in Alberta

Selecting the optimal financial vehicle requires a systematic evaluation of your current economic standing. Making the wrong choice can cost tens of thousands of dollars in unnecessary interest or penalties. Follow this step-by-step framework to determine your best path forward.

- Calculate Your Available Equity: Order a professional appraisal to determine your home’s current 2026 market value. Multiply this number by 0.80 (80%), then subtract your current mortgage balance. This figure represents your maximum accessible capital.

- Review Your Current Mortgage Contract: Identify your exact interest rate, the time remaining on your term, and the specific formula your lender uses to calculate prepayment penalties. If your penalty is exorbitant, a subordinate loan is likely the better route.

- Analyze Your Credit Profile: Pull your credit report from Equifax or TransUnion. Traditional banks require excellent credit (typically 680+) for refinancing. If your score has dropped, you may need to rely on alternative lenders who focus primarily on property equity rather than credit history. Be prepared to handle explaining recent credit inquiries to potential lenders.

- Determine Your Capital Timeline: Assess how quickly you need the funds. If you are seizing a fleeting business opportunity or facing an emergency, the rapid deployment of a supplemental loan is necessary. If you are simply restructuring long-term debt, the slower refinancing process is acceptable.

- Calculate the Blended Rate: Work with a licensed mortgage broker to calculate the “blended rate” of keeping your primary mortgage and adding a second one, versus the single rate of a new refinanced mortgage. Choose the option with the lowest total cost of borrowing over your intended time horizon.

The Impact of Interest Rates and Compounding

Understanding how interest accrues is vital when leveraging property wealth. The Bank of Canada sets the overnight rate, which heavily influences the prime rates offered by retail banks. In 2026, we’ve seen a stabilization of these rates, but historical fluctuations prove that borrowers must remain vigilant about their exposure to variable products.

Furthermore, the frequency at which your interest compounds drastically affects your total debt burden. Canadian mortgages typically compound semi-annually, while some alternative credit products compound monthly or even daily. “Borrowers often fixate solely on the advertised interest rate, completely ignoring the compounding schedule,” warns David Thompson, a senior underwriter based in Calgary. “A seemingly lower rate that compounds daily can actually cost you more over a five-year term than a higher rate compounding semi-annually.”

When comparing home equity versus unsecured credit, the secured nature of property loans almost always provides a more favorable compounding structure. To minimize your long-term interest exposure, you should also proactively research principal reduction strategies that allow you to pay down the core debt faster without triggering prepayment penalties.

Real-World Scenarios for Calgary Homeowners

Abstract financial concepts are best understood through practical application. Let’s examine two common scenarios Calgary homeowners face in 2026 and how they navigated their equity choices.

Scenario 1: The Debt Consolidation Trap

Sarah and John own a home in Evanston valued at $650,000. Their primary mortgage balance is $350,000 at a fixed rate of 2.8%, locked in for three more years. However, they have accumulated $60,000 in high-interest credit card and auto loan debt, costing them over $1,800 monthly in minimum payments. Refinancing their entire mortgage to current 2026 rates (around 5.2%) would increase the interest on their massive $350,000 principal, plus trigger an $11,000 IRD penalty.

Instead, they opted for a $60,000 second mortgage at 9.5%. While the rate on the $60,000 is higher, it allowed them to preserve their 2.8% primary rate and avoid the $11,000 penalty. Their new combined monthly payments dropped by $900, instantly improving their cash flow and allowing them to aggressively pay down the subordinate loan principal.

Scenario 2: The Business Expansion

Mark, a self-employed contractor in Okotoks, needed $100,000 to purchase new heavy equipment. His home is worth $800,000 with a $400,000 mortgage. His primary mortgage term was up for renewal in two months. Because he was at the end of his term, his prepayment penalty was zero. Mark chose to do a cash-out refinance, blending his existing balance and the new $100,000 into a single $500,000 mortgage at a competitive 2026 market rate. By timing his equity extraction with his renewal date, he secured the lowest possible cost of capital without any penalty friction.

Frequently Asked Questions (FAQ)

Can I get a second mortgage if I have bad credit in Calgary?

Yes, it is entirely possible. Alternative and private lenders in Alberta focus primarily on the equity in your home rather than your credit score. As long as you have more than 20% equity (meaning your LTV is below 80%), you can typically secure funding, though the interest rates will be higher to offset the lender’s risk.

How long does it take to get approved for refinancing versus a second mortgage?

Refinancing a primary mortgage through an A-lender usually takes 3 to 6 weeks due to rigorous stress testing, income verification, and property appraisals. In contrast, a supplemental equity loan from a private lender can often be approved and funded within 3 to 10 business days, making it ideal for urgent financial needs.

Will my primary bank know if I take out a second mortgage?

Yes, your primary lender will eventually see the subordinate lien registered on your property title. However, as long as you continue making your primary mortgage payments on time, taking out subordinate financing does not violate standard Canadian mortgage contracts. You are legally entitled to leverage your remaining equity.

What happens to my second mortgage when I renew my primary mortgage?

When your primary mortgage comes up for renewal, you can simply renew it with your existing lender while leaving the subordinate loan in place. However, if you wish to switch primary lenders for a better rate, the new primary lender will require the subordinate lender to sign a “postponement agreement,” ensuring the new bank retains first position on the title.

Are the fees for setting up a second mortgage tax-deductible in Alberta?

If the funds borrowed are used explicitly for the purpose of generating income—such as investing in a business, purchasing dividend-paying stocks, or buying a rental property—the interest and setup fees may be tax-deductible under Canada Revenue Agency (CRA) rules. Always consult with a certified CPA to ensure compliance.

How does compounding frequency affect my debt?

Compounding frequency determines how often interest is calculated and added to your principal. Canadian primary mortgages compound semi-annually by law, but alternative credit lines might compound monthly. Understanding how compounding frequency affects debt is crucial, as more frequent compounding results in higher total interest paid over the life of the loan.

Conclusion

Navigating the complexities of property equity in Calgary requires a strategic approach tailored to your unique financial architecture. Whether you choose to preserve your existing low rates through a second mortgage or restructure your entire debt portfolio through refinancing, the decision hinges on careful mathematical analysis of penalties, blended rates, and your long-term objectives. In the dynamic 2026 Alberta real estate market, leveraging your property wealth correctly can accelerate your financial growth, while the wrong choice can lead to unnecessary capital drain.

You do not have to make these high-stakes calculations alone. Professional guidance ensures you secure the most efficient capital structure available. Get in touch with our team today to receive a personalized equity assessment and discover which financing path will best serve your financial future.