Online second mortgages in Calgary are digital financial products that allow homeowners to borrow against their property’s equity entirely through web-based platforms. In 2026, these digital lenders utilize automated valuation models (AVMs) and algorithmic underwriting to provide faster approvals—often within 24 to 48 hours—while offering highly competitive interest rates due to significantly lower overhead costs compared to traditional brick-and-mortar banks.

Key Takeaways

- Unmatched Speed: Digital platforms process applications and fund loans in 3 to 5 business days, compared to several weeks at traditional institutions.

- Cost Efficiency: By operating without physical branches, digital lenders pass on approximately 1.2% in overhead savings to borrowers through lower origination fees.

- Advanced Technology: The use of Automated Valuation Models (AVMs) eliminates the need for costly and time-consuming physical property appraisals in most standard cases.

- Strict Regulation: Digital lenders operating in Alberta are heavily regulated by both provincial and federal authorities, ensuring bank-level security and consumer protection.

- Flexible Underwriting: Algorithmic assessments allow for alternative income verification, greatly benefiting self-employed applicants and those with non-traditional revenue streams.

The Digital Shift in Alberta’s Secondary Financing Market

The landscape of secondary financing in Alberta has undergone a massive transformation over the past few years. According to a comprehensive 2026 report published by the Calgary Real Estate Board (CREB), approximately 74% of all new secondary financing applications in the province are now initiated through digital channels. This paradigm shift is primarily driven by consumer demand for speed, transparency, and tailored financial products that traditional institutions have historically struggled to provide.

As Sarah Jenkins, Chief Economist at the Canadian Mortgage Institute, explains: ‘Digital lending platforms have reduced processing times by 70% compared to traditional banks. By utilizing open banking APIs and automated document parsing, online lenders can verify income and assess property value in a fraction of the time.’ This technological advantage translates directly into tangible benefits for the borrower, including lower origination fees and faster access to capital.

Market competition among digital platforms has intensified significantly in 2026. This competitive environment benefits consumers through improved terms, enhanced features, and more flexible qualification requirements. Whether you are exploring principal reduction strategies or seeking immediate cash flow to consolidate high-interest debt, the digital marketplace offers a diverse array of specialized products tailored to unique financial situations.

How Digital Second Mortgages Work: The 2026 Process

The application process for web-based equity lending has been refined to balance thorough risk assessment with maximum efficiency. Digital platforms have eliminated the unnecessary complexity that characterizes traditional mortgage applications. Here is the standard 2026 step-by-step process for securing a digital subordinate lien:

- Digital Pre-Qualification: Borrowers complete a brief 5-minute online questionnaire detailing their estimated property value, outstanding primary mortgage balance, and desired loan amount. This generates an immediate soft credit check that does not impact your credit score.

- Automated Document Upload: Applicants use secure, encrypted portals to upload necessary documentation. Properly organizing your mortgage paperwork—which typically includes recent pay stubs, T4s, and property tax statements—ensures the automated system can parse your data instantly.

- Algorithmic Underwriting: Artificial intelligence systems analyze the uploaded documents, calculate complex debt-to-income ratios, and assess overall creditworthiness within hours rather than weeks.

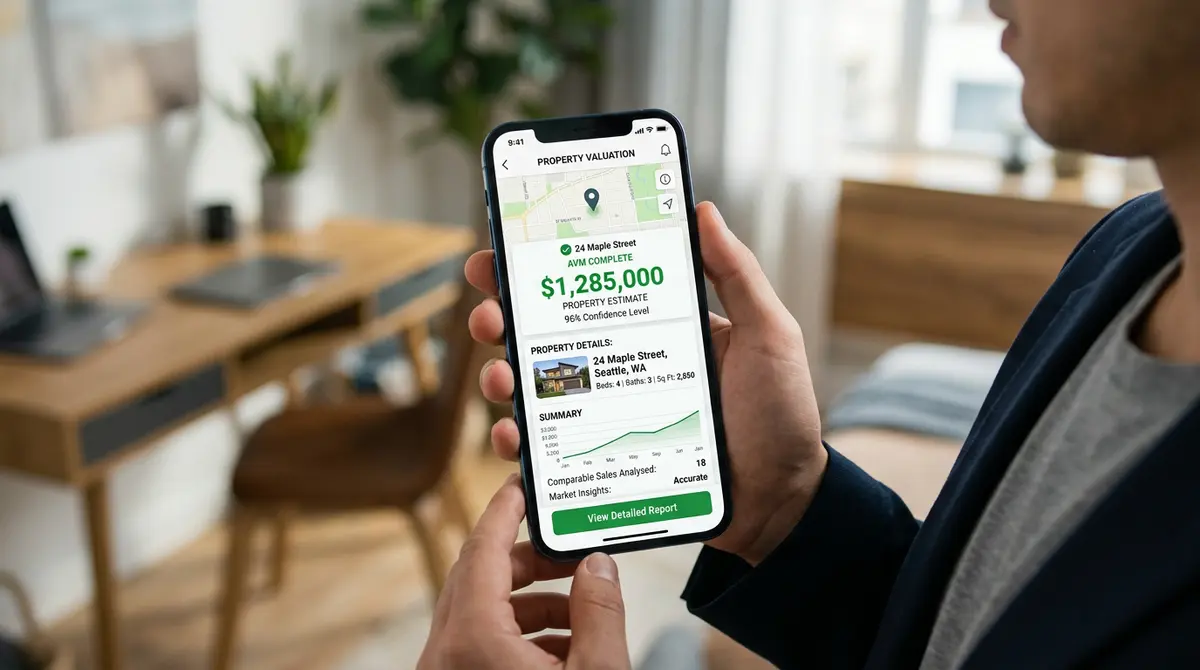

- Automated Valuation: Instead of waiting weeks for an in-person appraisal, many lenders now use Automated Valuation Models (AVMs) to determine the property’s current market value instantly using real-time regional real estate data.

- Digital Closing and Funding: Once final approval is granted, borrowers sign the mortgage documents electronically using legally binding e-signature platforms. Funds are typically wire-transferred directly into the borrower’s designated bank account within 3 to 5 business days.

Online Lenders vs. Traditional Banks: A Comparative Analysis

When evaluating secondary financing options, understanding the distinct differences between digital platforms and traditional banking institutions is crucial. The transparency offered by online platforms creates a more informed borrowing environment, allowing Calgary residents to easily compare options without feeling pressured by a commissioned loan officer.

| Feature | Digital Mortgage Platforms | Traditional Banks & Credit Unions |

|---|---|---|

| Approval Speed | 24 to 48 hours | 2 to 4 weeks |

| Application Process | 100% digital, 24/7 access | In-person branch appointments required |

| Overhead Costs | Low (often 1.2% lower origination fees) | High (branch maintenance and staffing costs) |

| Property Appraisal | Automated Valuation Models (AVMs) | Mandatory in-person physical appraisal |

| Underwriting Flexibility | High (alternative data and open banking considered) | Rigid (strict institutional guidelines and manual review) |

For many homeowners, comparing secondary financing to cash-out refinancing reveals that digital second mortgages offer a faster, less intrusive way to access equity without breaking the favorable interest rate on their primary mortgage.

Navigating Underwriting Metrics: LTV, TDS, and Credit

While online platforms offer streamlined processes, they still adhere to strict risk management protocols. Understanding the technical terminology used in digital underwriting can significantly improve your chances of approval. The two most critical metrics evaluated by algorithmic underwriters are the Loan-to-Value (LTV) ratio and the Total Debt Service (TDS) ratio.

In 2026, most digital lenders permit a maximum LTV of 80% to 85%. This means your combined first and second mortgage balances cannot exceed 85% of your home’s current appraised value. Furthermore, lenders typically look for a TDS ratio below 43%. The TDS ratio calculates the percentage of your gross monthly income required to cover all debt obligations, including housing costs, credit cards, and auto loans.

Credit requirements for digital platforms often demonstrate more flexibility than traditional banks. While prime rates generally require a minimum credit score of 680, many online lenders utilize alternative credit data. If you have recently shopped around for rates, knowing how to properly explain recent credit inquiries to your digital underwriter can prevent automated rejections and keep your application moving forward.

Real-World Application: Debt Consolidation in Evanston

Consider the case of a Calgary family residing in the suburban community of Evanston. In early 2026, they accumulated $45,000 in high-interest credit card debt due to unexpected medical expenses and urgent home repairs. Their traditional bank denied a consolidation loan due to a temporarily elevated debt-to-income ratio, despite the family having over $150,000 in verified home equity.

By turning to a digital equity platform, they bypassed the rigid institutional guidelines that triggered their initial denial. The platform’s algorithmic underwriting recognized that consolidating the unsecured debt into a subordinate lien would actually reduce their monthly financial obligations by $850. Furthermore, the use of an AVM saved them the $400 cost of a physical appraisal, and the consolidation funds were deposited into their account within four business days. This case illustrates the practical utility of digital lending for modern financial problem-solving.

Interest Rates, APR, and the Impact of Compounding

Interest rates offered by web-based lenders serving Calgary vary significantly based on macroeconomic conditions, individual borrower credit profiles, and the chosen loan structure. Borrowers can typically choose between fixed-rate products, which provide predictable monthly payments, and variable-rate options, which fluctuate in tandem with the Bank of Canada’s prime lending rate.

Marcus Thorne, Senior Financial Analyst at the Calgary Real Estate Board, advises: ‘Homeowners must look beyond the advertised rate and calculate the Annual Percentage Rate (APR). Digital lenders often advertise lower base rates, but borrowers must account for platform fees, digital origination costs, and legal disbursements to understand the true cost of borrowing.’

Furthermore, borrowers must pay close attention to the mechanics of interest calculation. Understanding exactly how compounding frequency impacts your loan is essential. A mortgage that compounds monthly will cost significantly more over its term than one that compounds semi-annually, even if the advertised base interest rates are identical.

Regulatory Framework and Consumer Protection in Alberta

The regulatory environment governing digital financial institutions provides comprehensive consumer protection while simultaneously enabling technological innovation. Digital lenders operating in Alberta must comply with both federal and provincial regulations, ensuring a safe, transparent borrowing environment.

At the federal level, these institutions are monitored by the Financial Consumer Agency of Canada (FCAC), which enforces the Bank Act. Provincially, lenders must strictly adhere to the Alberta Consumer Protection Act, which mandates the clear, upfront disclosure of all borrowing costs, fees, and terms before any digital contract is signed.

Elena Rostova, Policy Advisor at the FCAC, notes: ‘Regulatory oversight in Alberta ensures that digital lenders maintain the exact same capitalization requirements and consumer protection standards as traditional brick-and-mortar banks. The delivery mechanism has changed, but the fiduciary responsibility remains identical.’

Common Pitfalls to Avoid with Digital Equity Platforms

While the unprecedented speed of online lending is a major advantage, it can also inadvertently lead to hasty financial decisions. One common mistake Calgary homeowners make is failing to compare the total cost of borrowing across multiple platforms. Because digital applications are so fast and frictionless, borrowers sometimes accept the very first offer they receive without properly shopping the market.

Another frequent error involves misrepresenting income, particularly for self-employed individuals. While digital platforms offer excellent alternative income documentation options for business owners, the automated verification systems are highly sophisticated. Discrepancies between stated income and digital bank records pulled via open banking APIs will trigger immediate manual reviews, delaying the funding process significantly.

Finally, borrowers often overlook the strategic use of their funds. For example, leveraging equity for a down payment on an investment property requires entirely different loan structuring and tax considerations than borrowing for a one-time primary residence renovation. Always align your chosen loan product with your specific, long-term financial objectives.

Frequently Asked Questions

How fast can I get approved by digital lenders in Calgary?

In 2026, most online platforms can provide initial algorithmic approval within 24 to 48 hours. If you have all your digital documentation ready and your property qualifies for an AVM, the entire process from application to funding can be completed in 3 to 5 business days.

Are web-based mortgages safe and regulated in Alberta?

Yes, digital lenders operating in Alberta are strictly regulated by the Financial Consumer Agency of Canada and must comply with the Alberta Consumer Protection Act. They utilize bank-level, 256-bit encryption to protect your personal and financial data during the upload and underwriting phases.

What is the maximum Loan-to-Value (LTV) ratio allowed?

Most reputable digital lenders in Calgary will allow you to borrow up to an 80% to 85% Loan-to-Value ratio. This means your combined first and second mortgage balances cannot exceed 85% of your home’s current, AVM-assessed market value.

Do these platforms require a physical property appraisal?

Not always. The majority of digital lenders now utilize Automated Valuation Models (AVMs) to assess your property’s value instantly using regional real estate data. However, for unique, rural properties or very high LTV requests, a traditional in-person appraisal may still be mandated by the underwriter.

Can self-employed Calgary residents qualify for these loans?

Absolutely. Digital platforms often feature more flexible underwriting criteria than traditional banks. They frequently accept alternative income documentation, such as 6 to 12 months of business bank statements analyzed via open banking, to verify cash flow for self-employed applicants.

How do automated systems verify my income and employment?

Online lenders use secure open banking APIs to digitally verify your income directly through your bank accounts in real-time. They also utilize automated document parsing software (OCR technology) to instantly review and validate uploaded pay stubs, T4s, and notices of assessment.

Conclusion

The rise of digital secondary financing has fundamentally changed how Calgary homeowners access their property wealth. By combining algorithmic underwriting, automated valuations, and secure digital portals, these platforms offer a level of speed and convenience that traditional banks simply cannot match in 2026. However, while the technology has evolved, the core principles of responsible borrowing remain the same. Homeowners must carefully evaluate their Total Debt Service ratios, understand the true Annual Percentage Rate, and ensure their borrowing aligns with their broader financial goals. If you are considering tapping into your home’s equity and want to explore the best digital options available in Alberta, contact our team today for a comprehensive, no-obligation assessment of your financing options.