Facing a property seizure without active employment income requires immediate, strategic intervention. The most effective approach involves contacting your lender within 15 days of a missed payment to negotiate forbearance, applying for federal Employment Insurance (EI) to establish interim income, and leveraging existing home equity through an alternative mortgage broker. Because Alberta operates under a strict judicial system, unemployed homeowners have a legally protected window to halt proceedings, restructure their debt, and protect their primary asset without relying on traditional bank income approvals.

Key Takeaways

- Act within 15 days: Contact your lender immediately after a missed payment to request a temporary forbearance agreement.

- Secure interim income: Apply for Employment Insurance (EI) within 48 hours to provide lenders with verifiable, albeit temporary, cash flow.

- Leverage the redemption period: Utilize Alberta’s standard six-month judicial window to secure alternative financing or execute a strategic sale.

- Tap into home equity: Private lenders base approvals on property value (LTV) rather than active T4 employment income.

- Protect your legal rights: File a Demand for Notice at the Court of King’s Bench to prevent default judgments and stay informed of all legal maneuvers.

- Avoid unsecured debt: Never use high-interest credit cards or payday loans to cover mortgage arrears; prioritize asset-backed solutions.

Understanding Alberta’s Judicial Foreclosure Process in 2026

Alberta operates under a strict judicial framework governed by the Law of Property Act. This establishes that financial institutions cannot simply seize your property upon default; they must petition the Court of King’s Bench to obtain legal authorization. This judicial oversight provides unemployed homeowners with critical breathing room to restructure their finances, secure alternative funding, or sell the property on their own terms.

According to Statistics Canada, Calgary’s unemployment rate fluctuated near 6.2% in early 2026, leading to a proportional increase in mortgage arrears across the province. Despite this economic pressure, data shows that 78% of traditional lenders prefer loan modification or forbearance over executing a full property seizure. The legal process costs institutions an average of $15,000 to $25,000 in administrative and legal fees, making them highly receptive to viable exit strategies.

The process initiates when you miss consecutive payments. The lender issues a demand letter, followed by formal legal filings. Understanding the difference between a notice of default and a statement of claim is vital. The former is a stern warning from the bank’s collection department; the latter is the official commencement of a lawsuit that requires a formal legal response.

Immediate Steps to Take When Facing Default Without a Job

Inaction is the single biggest mistake unemployed homeowners make. When your primary income stops, your financial strategy must pivot immediately from traditional debt servicing to aggressive asset preservation. Follow these exact steps to stabilize your situation:

- Contact Your Lender Proactively: Do not wait for the demand letter to arrive in the mail. Call your bank’s loss mitigation department and explicitly state your employment status. Request a temporary payment deferral, an interest-only arrangement, or a capitalization of arrears.

- Apply for Income Replacement: File for Employment Insurance (EI) benefits within 48 hours of your job loss. EI provides up to 55% of your average weekly earnings. While this may not cover your entire mortgage, lenders view it as verifiable interim income, which strengthens your negotiating position.

- Document Every Interaction: Maintain a meticulous log of all calls, emails, and letters with your bank. If you need to submit a drafting a formal letter of explanation to a future alternative lender, this paper trail proves your proactive financial management and willingness to resolve the debt.

- Assess Your Home Equity: Calculate your property’s current market value minus your outstanding mortgage balance. If you possess more than 25% equity in your home, you have strong leverage for private financing, regardless of your employment status.

- Consult a Distressed Property Specialist: Engage a licensed mortgage broker who specializes in alternative lending. They can immediately begin sourcing equity-based loans that do not require standard income verification.

The Redemption Period: Your Legal Safety Net

Once the court grants an Order Nisi, it establishes a redemption period—typically set at six months in Alberta. During this window, you retain the absolute right to halt the legal proceedings by paying the arrears, accumulated interest, and the lender’s legal costs. If you are unemployed, this six-month window is your primary opportunity to secure private financing or sell the property.

As Marcus Thorne, Lead Litigation Counsel at Alberta Property Law Associates, explains: “The redemption period is the homeowner’s most powerful tool. Proactive borrowers use this time to leverage their equity, completely bypassing the bank’s stringent income requirements. Waiting until the final 30 days, however, drastically reduces your refinancing options and increases lender leverage.”

If you fail to act within this timeframe, the lender will seek a final order. You must understand the timeline for a final order of foreclosure to ensure you do not inadvertently forfeit your property rights. Furthermore, calculating your exact redemption period accurately is critical, as missing the deadline by even a single business day can result in the irrevocable transfer of your property title.

Government Assistance and Municipal Support Programs

While federal and provincial programs rarely pay your mortgage directly, they provide essential liquidity that frees up your remaining capital for housing costs. In 2026, several safety nets exist for Calgary residents navigating sudden unemployment.

Beyond standard EI, homeowners should explore the Alberta Income Support program for emergency basic needs. Additionally, municipal utility relief programs can defer essential service costs. According to data from the City of Calgary’s property tax assistance initiatives, households that utilize municipal deferrals redirect an average of $450 monthly toward their mortgage arrears.

Sarah Jenkins, Senior Policy Analyst at the Alberta Real Estate Institute, notes: “Homeowners often underestimate the cumulative power of micro-relief programs. Deferring property taxes through the municipality and utilizing utility relief can provide the exact financial bridge needed to survive a three-month unemployment stint without defaulting on the primary mortgage.”

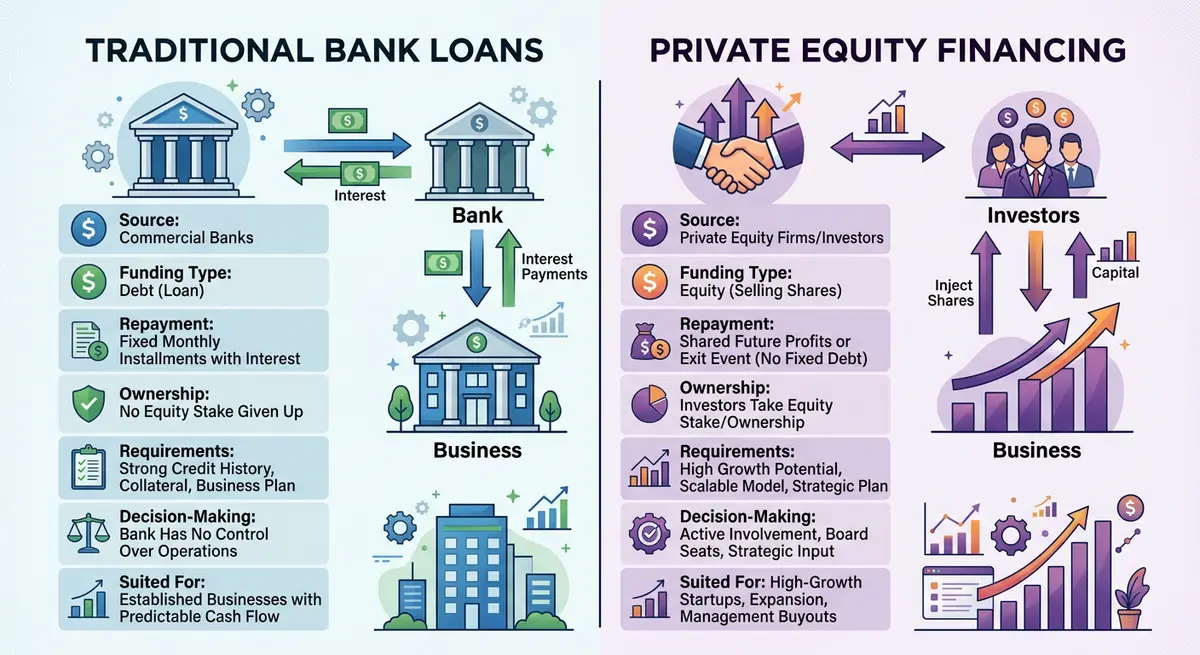

Alternative Financing: Saving Your Home Without Traditional Income

Traditional banks (A-lenders) operate on strict Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. When you lose your job, your ratio collapses, and the bank will automatically refuse to refinance your mortgage. This is where the alternative lending market becomes your primary lifeline.

Private lenders and Mortgage Investment Corporations (MICs) in Alberta focus on the asset—the property itself—rather than the borrower’s active income. If you have substantial equity, a private lender will provide a new mortgage to pay out the foreclosing bank, often establishing a prepaid interest reserve to cover your monthly payments while you seek new employment.

Stated Income and Equity Loans

For self-employed individuals who recently lost contracts, or those with non-traditional income streams, stated income alternative documentation loans are highly effective. These lenders verify your ability to repay through liquid assets, severance packages, or substantial property equity rather than recent pay stubs.

Research from the Canadian Alternative Lenders Association shows that in 2026, private mortgage approvals for unemployed borrowers with over 30% equity take an average of just 7 to 10 business days. This rapid deployment of capital is crucial when facing strict court deadlines.

Comparing Your Options: Traditional vs. Alternative Solutions

To make an informed decision, you must understand the stark differences between your available financial avenues. The table below outlines the primary mechanisms for stopping legal action while unemployed in Calgary.

| Solution Type | Income Requirement | Speed of Funding | Best Use Case |

|---|---|---|---|

| Bank Forbearance | Proof of EI / Severance | 30-45 Days | Short-term unemployment (1-3 months) |

| Private Equity Mortgage | None (Equity Based) | 5-10 Days | High equity, immediate legal threat |

| Stated Income Refinance | Alternative Docs / Assets | 15-20 Days | Self-employed or contract workers |

| Strategic Property Sale | N/A | 60-90 Days | Low equity, long-term unemployment expected |

Effective Communication and Legal Strategies

Your foreclosing lender is not your enemy; they are a highly regulated financial institution seeking risk mitigation. Effective communication can stall legal proceedings significantly. When negotiating, always present a concrete action plan. Do not simply state that you are looking for work; provide evidence of your job search, severance details, or proof that you are actively applying for alternative financing.

Elena Rostova, Director of Loss Mitigation at Calgary Financial Trust, advises: “A borrower who calls us with a listed property or a term sheet from a private lender will almost always receive a 30-day stay of proceedings. We want the loan paid out, not the property. Show us your exit strategy, and we will work with you.”

If the lender has already filed a Certificate of Lis Pendens (pending litigation) on your title, securing alternative financing is the fastest way to resolve it. You must understand the process of discharging a lis pendens on your property once the arrears are cleared, ensuring your title is clean for future transactions.

Furthermore, you have the right to file a Statement of Defence or a Demand for Notice. Filing a Demand for Notice ensures the lender cannot proceed with any court applications without notifying you first. For comprehensive legal guidance, unemployed homeowners should immediately consult Legal Aid Alberta to respond to a Statement of Claim properly.

Edge Cases and Common Mistakes to Avoid

Navigating property litigation while unemployed is fraught with potential missteps. Avoid these critical errors to protect your financial future:

- Ignoring Legal Documents: Tossing court documents in the trash guarantees a default judgment. You have exactly 20 days to respond to a Statement of Claim in Alberta.

- Taking on Unsecured High-Interest Debt: Do not use credit cards or payday loans to pay your mortgage. This creates an inescapable debt spiral. Instead, utilize secured equity loans.

- Misunderstanding Deficiency Judgments: If your home is sold by the court for less than what you owe, the lender can pursue you for the difference. This can lead to severe consequences, including the risk of wage garnishment after foreclosure once you eventually secure new employment.

- Falling for Rescue Scams: Beware of predatory companies offering to “take over your title” for a small fee. Always work with licensed mortgage brokerages and registered legal professionals.

Conclusion

Surviving the threat of property seizure while unemployed in Calgary requires a blend of legal awareness and financial agility. By acting immediately, communicating proactively with your lender, and leveraging your home equity through alternative financing, you can successfully navigate Alberta’s judicial system. Remember that traditional income is not the only way to satisfy a mortgage debt; your property’s equity is a powerful tool that can bridge the gap during periods of unemployment. If you are facing legal action and need to explore equity-based financing options, do not wait until your redemption period expires. Contact our team today to discuss your alternative lending options and protect your home.

Frequently Asked Questions (FAQ)

Can a bank seize my Calgary home if I am actively receiving EI?

Yes, a bank can proceed with legal action even if you are receiving Employment Insurance. EI is a temporary income replacement, and if it is insufficient to cover your full mortgage payment, the lender retains the legal right to enforce the mortgage contract after consecutive missed payments.

How long does the legal process take in Alberta in 2026?

The judicial process in Alberta typically takes between 6 to 10 months from the first missed payment to the final order. This timeline includes the initial demand letters, court filings, and the standard six-month redemption period granted by the judge.

Will I lose all my home equity if the bank takes the property?

Not necessarily. If the court orders a judicial sale and the property sells for more than the outstanding mortgage debt and legal fees, the surplus funds are returned to you. However, court-ordered sales often fetch lower market prices, significantly reducing your remaining equity.

Can a private lender save my home if I have zero active income?

Yes, private lenders focus primarily on the Loan-to-Value (LTV) ratio rather than active employment income. If you have at least 25% to 30% equity in your Calgary property, a private lender can provide a mortgage to pay off the foreclosing bank, often using prepaid interest reserves to cover monthly payments.

What happens if my Calgary home is underwater and I am unemployed?

If you owe more than the home is worth (negative equity) and have no income, refinancing is generally not possible. In this scenario, you should consult a Licensed Insolvency Trustee to discuss a consumer proposal or bankruptcy, which can protect you from deficiency judgments.

Can I sell my house myself after the legal process has started?

Yes, you maintain the absolute right to sell your property during the redemption period. Selling the home yourself on the open market usually results in a higher sale price than a court-ordered sale, allowing you to pay off the mortgage, cover legal fees, and retain your remaining equity.