Calculating your available home equity requires subtracting your outstanding mortgage balance from your property’s current market value. In Calgary’s 2026 real estate market, financial institutions typically allow homeowners to borrow up to 80% of this appraised value, a metric known as your accessible equity. By multiplying your home’s value by 0.80 and deducting any existing secured debt, you can determine exactly how much capital is available for secondary financing, renovations, or debt consolidation.

Key Takeaways

- Core Formula: Accessible equity equals 80% of your property’s current market value minus your existing mortgage balance.

- Valuation Matters: Professional appraisals provide the most accurate baseline for calculations, superseding automated online estimates.

- LTV Limits: Prime lending institutions strictly enforce an 80% Loan-to-Value (LTV) maximum for combined mortgages.

- Qualification Ratios: Lenders evaluate Gross Debt Service (GDS) and Total Debt Service (TDS) ratios alongside your equity position.

- Market Dynamics: Calgary’s 2026 economic indicators directly influence local property appraisals and subsequent borrowing power.

Understanding Property Equity in Calgary’s 2026 Market

Your property represents a dynamic financial asset, not just a physical residence. As you make regular mortgage payments and as local real estate values fluctuate, your ownership stake—your equity—changes. Research from the Canada Mortgage and Housing Corporation (CMHC) indicates that 63% of homeowners underestimate their property’s financial potential, often confusing gross equity with accessible equity.

Gross equity is simply the market value minus your mortgage. Accessible equity, however, is the portion a lender will actually let you borrow against. Because institutions must mitigate risk, they rarely allow you to leverage 100% of your home’s value.

As Dr. Elena Rostova, Senior Economist at the Alberta Real Estate Research Institute, explains: “In 2026, accurate property valuation is the cornerstone of sustainable household leverage. Calgary homeowners must differentiate between what their home is worth on paper and what financial institutions consider usable collateral under current federal stress test regulations.”

Step-by-Step: How to Calculate Your Available Equity

Determining your borrowing capacity requires a systematic approach. Follow these steps to calculate your precise financial position before applying for secondary financing.

- Determine Current Market Value: Obtain a realistic estimate of your home’s worth. For initial calculations, recent comparable sales in your specific Calgary neighborhood provide a solid baseline.

- Calculate the 80% Threshold: Multiply your estimated market value by 0.80. This represents the maximum total debt most prime lenders will allow secured against the property.

- Verify Outstanding Balances: Check your most recent mortgage statement to find the exact principal amount remaining on your primary loan, plus any existing lines of credit secured by the house.

- Subtract to Find Accessible Funds: Deduct your outstanding balance from the 80% threshold calculated in step two. The resulting number is your maximum available borrowing power.

For example, if your Calgary home is valued at $800,000, the 80% maximum allowable debt is $640,000. If your current mortgage balance is $350,000, you have $290,000 in accessible equity available for strategic use.

The Loan-to-Value (LTV) Ratio Explained

The Loan-to-Value (LTV) ratio is the most critical metric in real estate financing. It represents the percentage of your property’s value that is mortgaged. The formula is straightforward: (Total Secured Debt ÷ Property Value) × 100.

According to Marcus Thorne, Chief Underwriter at Calgary Financial Trust: “Borrowers frequently confuse gross equity with accessible equity. Your LTV ratio dictates not only your approval odds but also the interest rate tier you qualify for. In 2026, maintaining an LTV below 65% often unlocks the most competitive prime rates available.”

Different lending institutions have varying risk tolerances, which reflect in their maximum allowable LTV ratios. Understanding these tiers helps you target the right financial products.

| Lender Category | Maximum LTV Limit | Typical Interest Rate Profile | Ideal Borrower Profile |

|---|---|---|---|

| Prime Institutions (Banks/Credit Unions) | 80% | Highly Competitive (Prime + 0.5% to 2%) | Excellent credit (680+), verifiable standard income |

| Alternative (B-Lenders) | 80% – 85% | Moderate (Prime + 2% to 4%) | Self-employed, minor credit blemishes, non-traditional income |

| Private Lenders | Up to 95% (Location dependent) | Higher Yield (8% to 14%+) | Short-term needs, heavy debt consolidation, poor credit |

Methods for Determining Current Market Value

Accurate valuation prevents the risks associated with over-leveraging. While online automated valuation models (AVMs) offer quick estimates based on algorithmic data, they often fail to account for unique structural improvements or hyper-local neighborhood trends in Calgary.

Sarah Jenkins, Director of Mortgage Compliance at the Canadian Lending Standards Board, notes: “The shift toward automated valuation models in 2026 requires homeowners to be vigilant. An AVM cannot see your newly renovated kitchen or finished basement, potentially undervaluing your equity by tens of thousands of dollars.”

For official lending purposes, a full professional appraisal is mandatory. Certified appraisers, regulated by organizations like the Appraisal Institute of Canada, evaluate recent comparable sales, zoning regulations, lot size, and interior condition. David Chen, Lead Appraiser at Western Canada Valuations, states: “A professional appraisal does more than satisfy lender requirements; it protects the homeowner from over-leveraging by providing an objective, data-driven assessment of the asset’s true market position.”

Types of Secondary Financing Options

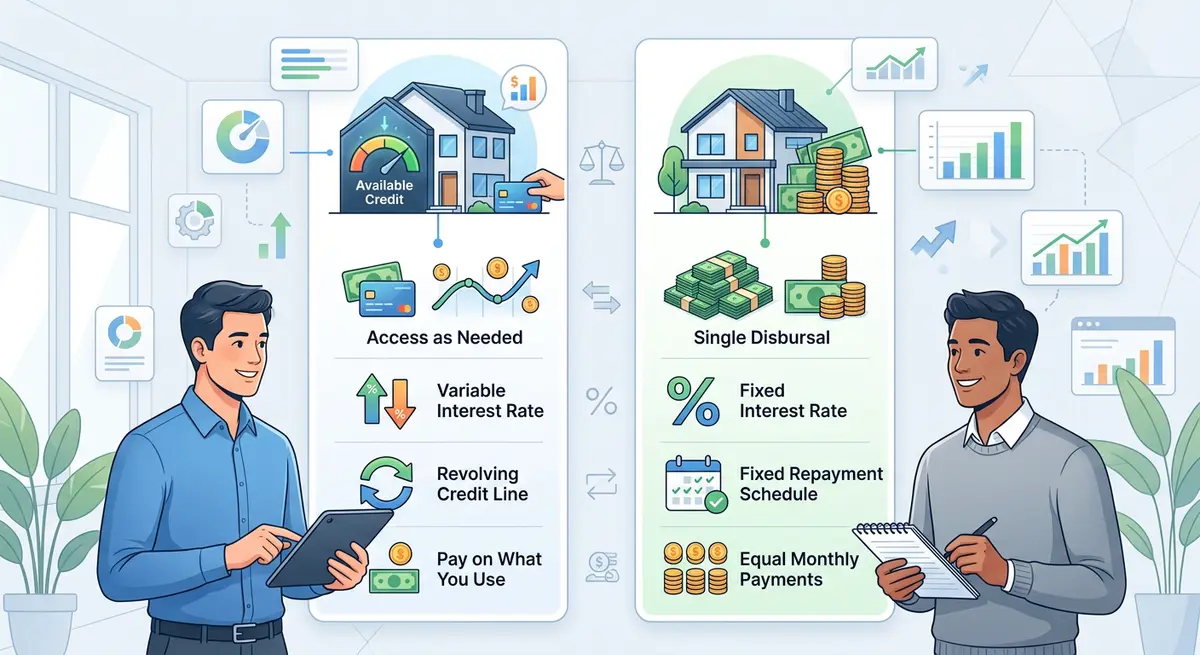

Once you have calculated your accessible funds, you must choose the appropriate vehicle to access them. The two primary structures are revolving credit facilities and lump-sum loans. Your choice should align with your specific capital requirements and repayment capabilities.

Home Equity Line of Credit (HELOC)

A HELOC functions similarly to a secured credit card. You are approved for a maximum limit based on your equity calculations, but you only draw funds as needed. Interest is charged exclusively on the drawn balance. According to the Financial Consumer Agency of Canada (FCAC), HELOCs typically feature variable interest rates tied to the lender’s prime rate and require interest-only minimum payments during the draw period. This flexibility makes them ideal for ongoing projects like phased home renovations or funding a child’s university education.

Traditional Lump-Sum Loans

Conversely, a traditional equity loan provides the entire approved amount upfront. These products generally feature fixed interest rates and amortized repayment schedules, meaning your monthly payment includes both principal and interest. This structure offers absolute budgeting certainty, making it the preferred choice for one-time expenses such as consolidating high-interest credit card debt or executing a managing spousal buyouts during a separation.

Qualification Requirements for Equity Borrowing

Having sufficient equity is only the first hurdle; lenders must also verify your ability to service the new debt. In 2026, financial institutions scrutinize three primary pillars during the underwriting process: credit history, income stability, and debt service ratios.

Credit Score Thresholds

Your credit score dictates your risk profile. Prime lenders typically require a minimum beacon score of 680 to access the best rates. If your score falls below this threshold due to past financial challenges, you may need to explore alternative documentation financing or consider using a parent as a guarantor to strengthen your application.

Debt Service Ratios

Lenders calculate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios to ensure your housing costs and total debt obligations do not consume an unsafe percentage of your income. Typically, your GDS (housing costs including the new loan, property taxes, and heating) should not exceed 39% of your gross income. Your TDS (housing costs plus all other debt payments) is generally capped at 44%. If you have unique income structures, such as self-employment dividends, proper documentation is vital. In some cases, drafting a letter of explanation can help underwriters understand complex financial histories or recent credit inquiries.

Real-World Equity Calculation Scenarios

To illustrate how these calculations apply in practice, consider these common scenarios faced by Calgary homeowners in 2026.

Scenario A: Debt Consolidation

The Thompson family owns a property valued at $650,000. Their primary mortgage balance is $400,000. They have accumulated $45,000 in high-interest credit card debt and personal loans.

- Maximum Allowable Debt (80% of $650,000): $520,000

- Current Mortgage: $400,000

- Accessible Equity: $120,000

Scenario B: Business Investment

Sarah, a local entrepreneur, wants to leverage her home to expand her retail business. Her property appraises at $900,000, and she owes $600,000.

- Maximum Allowable Debt (80% of $900,000): $720,000

- Current Mortgage: $600,000

- Accessible Equity: $120,000

Common Pitfalls and Edge Cases

While leveraging property wealth is a powerful financial tool, it carries inherent risks. The most significant danger is over-leveraging—borrowing to the absolute maximum limit without a clear repayment strategy. If Calgary property values experience a localized correction, homeowners heavily leveraged at 80% or 85% LTV could find themselves in a negative equity position, complicating future renewals or sales.

Furthermore, borrowers must understand the implications of variable interest rates. Data from the Bank of Canada highlights how sudden policy rate adjustments directly impact HELOC carrying costs. A 1% increase in the prime rate on a $100,000 balance adds $1,000 annually in interest expenses. Homeowners utilizing variable products must stress-test their budgets to ensure they can absorb potential rate hikes.

Finally, administrative details matter. Ensure you are properly retaining your mortgage documents, as future refinancing or discharging of liens requires a clear paper trail. If your goal is to eventually clear the debt entirely, implementing aggressive principal reduction strategies early in the loan term will save thousands in compounding interest.

Conclusion

Calculating your available home equity is a foundational step in effective wealth management. By accurately assessing your property’s 2026 market value, understanding the strict 80% Loan-to-Value limits enforced by prime lenders, and carefully evaluating your debt service ratios, you can unlock substantial capital. Whether you are funding a major renovation, consolidating high-interest debt, or investing in a business, leveraging your property’s value requires strategic planning and professional guidance. If you are ready to explore your financing options and want a precise calculation of your accessible funds, contact us today to speak with a qualified advisor.

Frequently Asked Questions

How is accessible home equity calculated in Alberta?

Accessible home equity is calculated by determining the current market value of your property, calculating 80% of that value, and then subtracting your outstanding mortgage balance. This formula reveals the maximum amount most prime lenders will allow you to borrow against the home.

What is the maximum Loan-to-Value (LTV) ratio allowed in 2026?

For prime lending institutions like major banks and credit unions, the maximum combined LTV ratio is strictly capped at 80%. However, certain alternative or private lenders may allow LTV ratios up to 85% or even 95%, though these come with significantly higher interest rates and fees.

Do I need a new appraisal to calculate my equity?

While you can estimate your equity using online tools or recent property tax assessments, lenders require a formal, professional appraisal to approve secondary financing. This ensures the valuation reflects current 2026 market conditions and accounts for any specific property improvements.

How do Gross Debt Service (GDS) ratios affect my borrowing power?

Even if you have substantial equity, lenders use your GDS ratio to ensure you can afford the monthly payments. Your total housing costs, including the new loan payment, property taxes, and heating, typically cannot exceed 39% of your gross household income.

Can I add a co-borrower to increase my borrowing capacity?

Yes, adding a spouse to your application or bringing on a co-signer can significantly improve your debt service ratios. By combining incomes, you may qualify for a larger loan amount or secure a more favorable interest rate tier.

What is the difference between a HELOC and a traditional equity loan?

A HELOC is a revolving line of credit with variable rates where you only pay interest on the funds you actively draw. A traditional equity loan provides a lump sum upfront, usually with a fixed interest rate and a set amortized repayment schedule covering both principal and interest.

How do interest rates compare to cash-out refinancing?

Secondary financing rates are generally higher than primary mortgage rates because the lender takes a subordinate position on the property title. However, depending on your current primary mortgage rate and penalty fees, exploring cash-out refinancing options might be more cost-effective than taking out a separate secondary loan.

Will my credit score impact how much equity I can access?

Yes. While your equity determines the maximum theoretical loan amount, your credit score determines the lender’s risk appetite. A score below 680 may result in the lender capping your LTV at 65% or 75% instead of the standard 80%, reducing your accessible funds.