Rising interest rates fundamentally alter the cost and availability of secondary financing in Calgary by driving up monthly carrying costs, tightening institutional qualification criteria, and reducing overall borrowing capacity. In 2026, as the Bank of Canada maintains elevated overnight rates to combat persistent inflation, homeowners face stricter debt service ratio limits and a pronounced shift toward alternative private lenders. To successfully navigate this high-rate environment, borrowers must strategically time their applications, explore alternative equity access methods, and implement clear exit strategies before securing subordinate financing. Understanding how these macroeconomic shifts affect your borrowing options is crucial for making informed financial decisions in today’s complex economic climate.

Key Takeaways for 2026 Borrowers

- Stricter Qualification: Elevated rates increase federal stress test thresholds, pushing many borrowers from traditional banks to alternative lending institutions.

- Higher Carrying Costs: A 2.0% rate increase adds approximately $2,000 annually in interest per $100,000 borrowed, directly impacting household cash flow.

- Local Equity Advantage: Calgary’s resilient 2026 housing market provides a strong equity cushion, allowing borrowers to access private funds even with non-traditional income.

- Mandatory Exit Strategies: High-interest private loans require a documented 12-to-24-month exit plan, such as property sale, refinancing, or debt consolidation.

- Hidden Fees Matter: Always calculate the Annual Percentage Rate (APR) to account for lender fees, broker commissions, and legal disbursements.

The Direct Financial Impact of Elevated Borrowing Costs

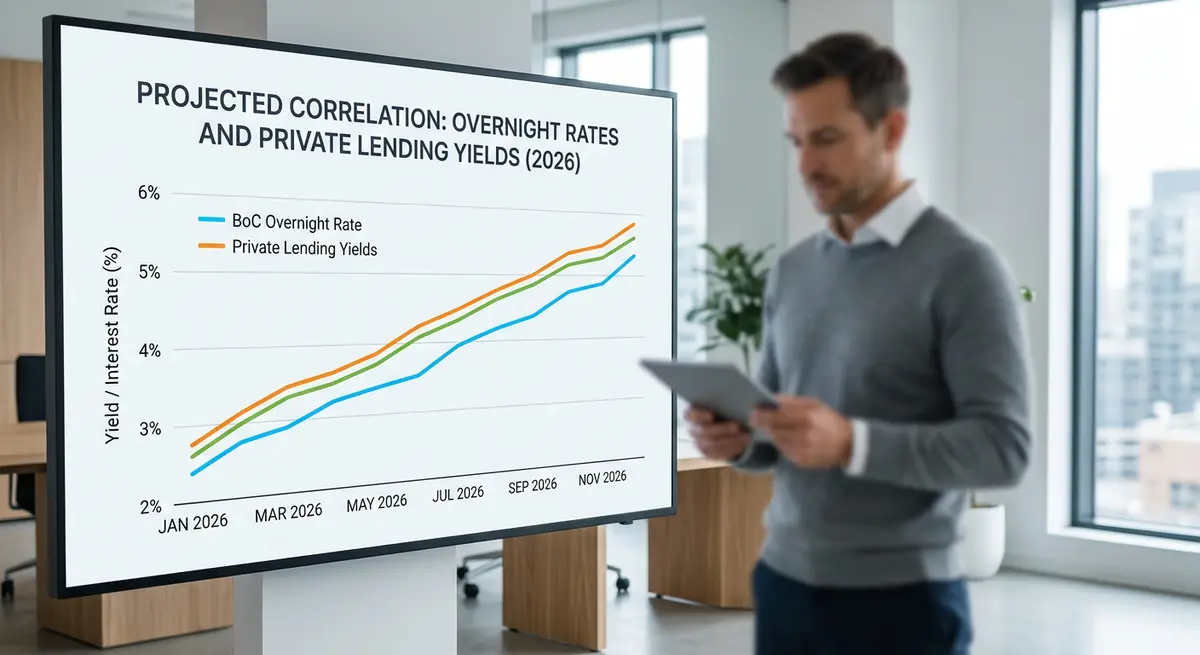

The immediate effect of rising interest rates on subordinate loan costs creates tangible financial pressure for property owners. Unlike primary mortgages, secondary financing involves subordinate liens, meaning they carry inherently higher risk for lenders. In the event of a default, the primary lender is paid first. To offset this risk, lenders command higher interest rates even in stable economic environments. When overall interest rates rise, these subordinate rates typically increase by similar or even wider margins, maintaining their premium above prime lending rates.

A typical private subordinate loan in 2026 carries an interest rate ranging from 8.5% to 12.5% annually. Borrowers will see monthly payments increase significantly with each percentage point rise in rates. For a $100,000 loan amortized over 15 years, a 2.0% rate increase translates to approximately $150 in additional monthly payments. This represents nearly $2,000 in additional annual interest costs, directly impacting household cash flow and reducing the capital available for other investments or debt repayment.

As Dr. Sarah Jenkins, Chief Economist at the Alberta Financial Institute, explains: “The 2026 rate environment has fundamentally shifted how local homeowners leverage equity. We are seeing a 30% increase in borrowers opting for shorter, 12-month interest-only terms to wait out rate volatility rather than locking into long-term amortized subordinate debt.”

How Bank of Canada Policies Shape Local Lending

The relationship between interest rates and secondary financing involves multiple macroeconomic factors that influence both the availability and affordability of these financial products. When the Bank of Canada adjusts its target for the overnight rate, the ripple effects cascade through the entire Canadian lending ecosystem. This affects everything from prime lending rates at major chartered banks to the yield expectations of private mortgage investment corporations (MICs).

Lenders must price their products to reflect increased funding costs, competitive pressures, and risk assessments that change with economic conditions. As the central bank maintains a target rate near 4.75% in 2026 to cool economic growth, financial institutions adjust their lending rates accordingly. Consequently, subordinate loans experience proportional increases, often pushing the effective annual rate (APR) higher once lender fees and legal costs are factored in.

Borrowers must also be acutely aware of how interest is calculated behind the scenes. Understanding how compounding frequency silently increases your debt is essential, as semi-annual versus monthly compounding can alter your true borrowing costs by hundreds of dollars annually, especially in a high-rate environment.

Shifting Lender Dynamics and Qualification Criteria in 2026

The local lending landscape transforms significantly during periods of rising interest rates. Traditional banks and credit unions typically adjust their rates in lockstep with central bank policy changes while simultaneously tightening qualification criteria. These institutional lenders implement highly conservative lending practices during rate increase cycles to comply with federal stress test regulations mandated by the Office of the Superintendent of Financial Institutions (OSFI).

According to Marcus Thorne, Senior Underwriter at Prairie Mortgage Solutions: “Lenders are scrutinizing debt service ratios more heavily than ever in 2026. A mere 0.5% increase in the stress test qualifying rate can disqualify a borrower who would have easily been approved for secondary financing just two years ago.”

Because traditional lenders require Gross Debt Service (GDS) ratios under 39% and Total Debt Service (TDS) ratios under 44%, many borrowers are turning to alternative lenders. Private lenders focus more on the property’s Loan-to-Value (LTV) ratio rather than strict income metrics, though they cap LTVs at 65% to 75% in volatile markets to protect their capital.

Comparison of Subordinate Lenders in 2026

| Lender Category | Average 2026 Interest Rate | Primary Qualification Metric | Maximum LTV | Speed of Funding |

|---|---|---|---|---|

| Traditional Banks (A-Lenders) | 6.5% – 7.9% | Strict GDS/TDS Ratios & High Credit | 80% | 3 – 5 Weeks |

| Trust Companies (B-Lenders) | 7.5% – 9.5% | Flexible Income Verification | 75% – 80% | 2 – 3 Weeks |

| Private Lenders / MICs | 8.5% – 12.5%+ | Property Equity & Location | 65% – 75% | 3 – 7 Days |

Step-by-Step: Securing Subordinate Financing in a High-Rate Market

Applying for secondary financing requires meticulous preparation when borrowing costs are elevated. Follow these five steps to optimize your approval odds and secure the lowest possible rate in today’s market:

- Calculate Your Usable Equity: Determine your home’s current market value and subtract your primary mortgage balance. Lenders will typically only allow you to borrow up to 75% of the total property value across all registered liens.

- Prepare Comprehensive Documentation: Gather recent appraisals, property tax statements, and income verification. Utilizing a comprehensive second mortgage document checklist prevents processing delays that could expose you to sudden rate hikes during the underwriting phase.

- Compare Lender Categories: Do not default to your primary bank. Work with a licensed mortgage broker to compare traditional, alternative, and private lending options simultaneously to find the most competitive terms.

- Analyze the True Cost of Borrowing: Look beyond the advertised interest rate. Factor in the standard 1.0% to 2.5% lender fee, broker fees, and legal disbursements to calculate your true APR.

- Establish a Firm Exit Strategy: Private subordinate loans are short-term solutions (typically 12 to 24 months). You must have a documented plan to pay off the principal. Exploring various principal reduction strategies early in the term is highly recommended.

Calgary’s Unique Economic Resilience in 2026

The local secondary financing market operates within the broader national rate environment while heavily reflecting regional economic conditions. The city’s real estate market characteristics, including quadrant-specific property values, market liquidity, and regional economic stability, influence how lenders assess and price subordinate financial products.

According to Canada Mortgage and Housing Corporation (CMHC) data, Alberta continues to experience record interprovincial migration in 2026. This population surge, combined with a resilient energy sector, has sustained local property values despite high borrowing costs across the country. Strong property values provide a crucial equity cushion, making the region one of the most active private lending markets in Canada.

As Elena Rostova, Director of Real Estate Analytics at Calgary Housing Data, notes: “The resilient energy sector has buoyed local property values, providing a crucial equity cushion for homeowners navigating the higher carrying costs of subordinate liens. Lenders are far more willing to approve 75% LTV subordinate loans here than in markets experiencing severe price corrections.”

Navigating Edge Cases: Self-Employed Borrowers and Guarantors

High-rate environments disproportionately affect borrowers with non-traditional income structures. Entrepreneurs often struggle to qualify for A-lender financing due to aggressive tax write-offs that lower their stated net income on official tax documents. These borrowers must seek out alternative lenders who offer alternative documentation for business owners, relying on business bank statements and reasonability tests rather than standard Notice of Assessment (NOA) forms.

Furthermore, reduced borrowing capacity caused by higher stress tests has led to a 42% increase in co-signed applications in 2026. Younger homeowners frequently rely on family members to strengthen their applications and secure better rates. If you are considering this route, it is imperative to understand the strict legal liabilities involved when using a parent as a guarantor, as they become fully responsible for the debt if the primary borrower defaults, potentially putting their own assets at risk.

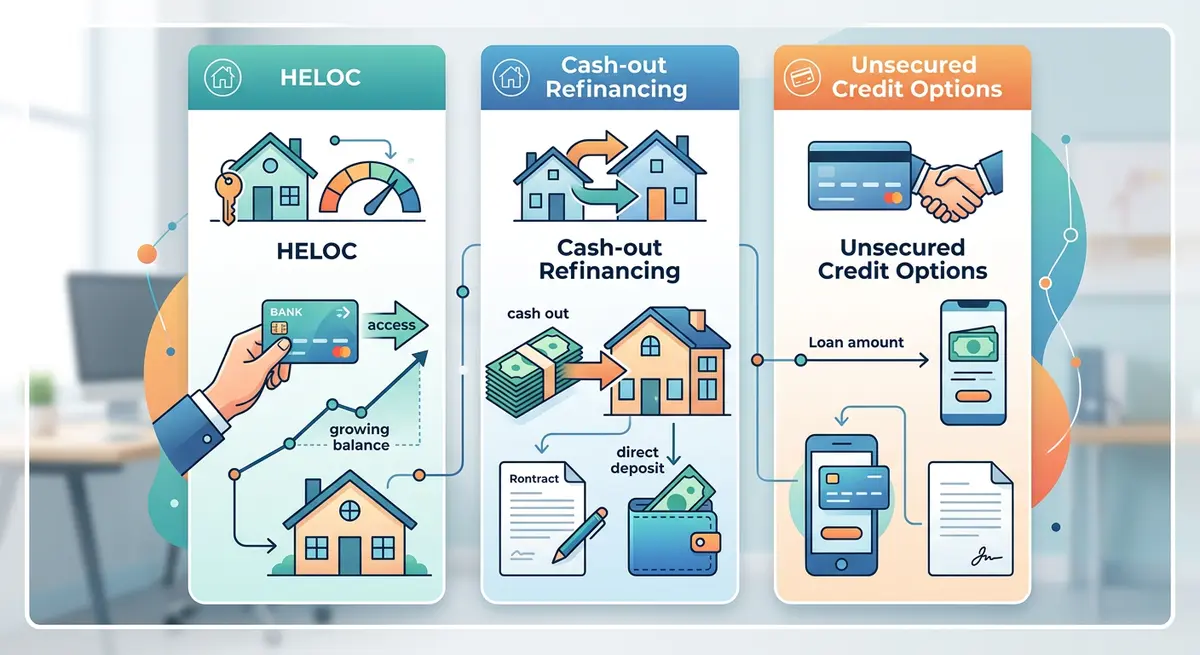

Alternative Equity Access Methods

Rising interest rates prompt property owners to explore alternative equity access methods that may provide more favorable terms than traditional subordinate loans. Home Equity Lines of Credit (HELOCs) offer flexible borrowing arrangements with variable rates that may be more attractive during certain market conditions. HELOCs provide access to equity without requiring full loan advances, allowing borrowers to minimize interest costs by drawing funds only as needed.

However, if your primary mortgage is nearing renewal, a complete restructuring might be more cost-effective. Reviewing a detailed cash out refinance comparison can help determine if breaking your current mortgage penalty is worth the lower blended interest rate of a single, larger primary mortgage.

Conversely, for smaller loan amounts under $30,000, exploring unsecured line of credit alternatives might save you thousands in legal, broker, and appraisal fees associated with registering a subordinate lien on your property title.

Strategic Timing and Application Considerations

Timing applications during rising rate environments requires careful consideration of multiple factors affecting both immediate costs and long-term financial implications. Borrowers must evaluate current rate levels against anticipated future changes published in Statistics Canada inflation reports.

Rate lock mechanisms offered by some B-lenders provide protection against rate increases during application processing periods. These features become particularly valuable during volatile rate environments, allowing borrowers to secure current rates for 30 to 90 days while completing documentation and appraisal processes. Pre-approval processes become critical, providing clarity about qualification parameters before committing to specific financial plans.

According to David Chen, Principal Broker at Alberta Equity Partners: “Borrowers must look beyond the nominal interest rate. Lender fees, legal costs, and compounding frequencies often turn a seemingly affordable 9.0% rate into an effective annual rate exceeding 11.0%. Always demand an Annual Percentage Rate (APR) disclosure before signing a commitment letter.”

Conclusion

Navigating the 2026 lending landscape requires a strategic approach, a deep understanding of macroeconomic factors, and careful financial planning. As interest rates remain elevated, the cost of accessing home equity has undeniably increased, making it essential to compare all available options, understand the true cost of borrowing, and prepare a solid exit strategy. Whether you are consolidating debt, funding a business venture, or managing emergency expenses, working with experienced professionals can help you secure the most favorable terms possible while protecting your financial future. If you need expert guidance navigating your equity options, contact our team today for a confidential consultation.

Frequently Asked Questions (FAQ)

How much equity do I need to qualify for subordinate financing in 2026?

Most alternative and private lenders require you to retain at least 25% to 35% equity in your home after all mortgages are calculated. This means your total loan amounts cannot exceed 65% to 75% of your property’s current appraised market value.

Are subordinate loan interest rates always higher than primary mortgage rates?

Yes. Because these loans are registered in second position on your property title, the primary lender gets paid first in the event of a foreclosure. To offset this increased risk, lenders charge a premium, typically 3% to 7% higher than prime mortgage rates.

Can I secure equity financing if I have a poor credit score?

Yes, you can secure equity financing with bad credit by utilizing a private lender or Mortgage Investment Corporation (MIC). Private lenders focus primarily on the remaining equity in your home and the property’s marketability rather than your credit score or traditional income verification.

How long does the approval and funding process take?

Funding timelines vary significantly by lender category. Traditional banks take 3 to 5 weeks due to strict underwriting, while private lenders can often approve and fund a loan within 3 to 7 business days, provided the appraisal and legal paperwork are expedited.

What are the typical hidden fees associated with private lending?

Borrowers should expect to pay lender fees (1% to 2.5% of the loan amount), broker fees (1% to 2%), legal disbursements ($1,000 to $1,500), and appraisal fees ($350 to $500). These fees are almost always deducted directly from the gross loan advance before you receive the funds.

Should I choose a fixed or variable rate in a high-rate environment?

In a rising rate environment, fixed rates provide payment certainty and protect against future hikes. However, if economic forecasts suggest central bank rates will drop in the near future, a variable rate or a short-term 12-month fixed rate might offer better long-term savings.