When facing imminent property loss in Calgary, an equity sharing agreement allows a homeowner to sell a percentage of their property’s future appreciation and current equity to an investor in exchange for immediate capital to cure mortgage arrears. This collaborative ownership model halts legal proceedings, reduces monthly debt obligations, and keeps the homeowner in their primary residence without triggering a forced sale. By legally restructuring the property title into a tenancy in common, homeowners can leverage their built-up equity to satisfy lender demands while maintaining housing stability during financial hardship.

Key Takeaways

- Immediate Arrears Resolution: Investor capital is used directly to pay off missed mortgage payments, instantly halting judicial foreclosure proceedings.

- Reduced Monthly Burden: Co-owners share ongoing mortgage, tax, and insurance costs, lowering the primary resident’s debt-to-income ratio.

- Credit Preservation: Curing the default prevents a final foreclosure judgment, protecting the homeowner’s credit score from catastrophic damage.

- Flexible Exit Strategies: Agreements typically last 3 to 5 years and include buyout clauses, allowing the original owner to reclaim full title once financially stable.

- Legal Safeguards: Alberta law requires strict documentation, including defined profit splits and maintenance responsibilities, to protect all parties.

- Market Viability: With Calgary’s average home prices reaching $615,000 in 2026, shared equity models offer a practical alternative to high-interest refinancing.

Understanding the 2026 Foreclosure Landscape in Calgary

The economic environment in 2026 has placed unprecedented pressure on Alberta homeowners. With the Bank of Canada maintaining elevated baseline interest rates, over 18% of mortgage holders are experiencing severe payment shock upon renewal. When household budgets fracture under the weight of inflation, sudden job loss, or medical emergencies, falling behind on mortgage payments becomes a stark reality. However, unlike regions that utilize rapid power-of-sale mechanisms, Alberta employs a judicial foreclosure process. This legal framework requires lenders to petition the Court of King’s Bench to seize a property, a procedure that typically spans 12 to 18 months.

This extended timeline is a critical advantage for distressed borrowers. It provides a vital window to explore alternative solutions before a judge issues a final ruling. Understanding the difference between a notice of default and a statement of claim is the first step in navigating this crisis. Once a statement of claim is filed, the clock begins ticking on the redemption period—usually set between 35 and 180 days by the courts. During this phase, homeowners must either pay the arrears in full, sell the property, or find an innovative financing solution like collaborative ownership to satisfy the debt.

Decoding Equity Sharing Agreements

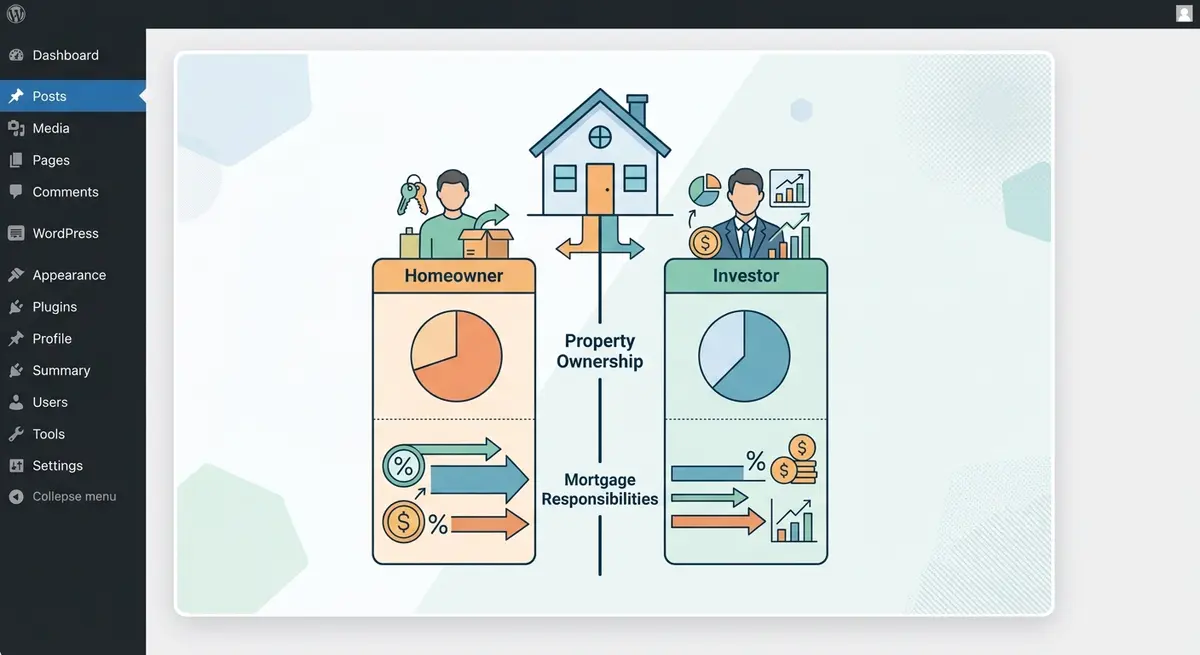

An equity sharing agreement is a legally binding contract where an investor or partner purchases a minority or majority stake in a residential property. Instead of a traditional loan, the investor provides a lump sum of cash that is immediately applied to the mortgage arrears and legal fees. In return, they receive a proportional share of the property’s title, usually structured as a tenancy in common. This means both parties own distinct, transferable shares of the real estate, and both share in the property’s future appreciation or depreciation.

For example, if a homeowner owes $40,000 in arrears on a property valued at $600,000, an investor might contribute $60,000 (covering the arrears plus a reserve fund) in exchange for a 20% equity stake. The homeowner continues to live in the property, paying a proportionally reduced share of the monthly mortgage, while the investor covers the rest.

As Dr. Elena Rostova, Senior Housing Economist at the University of Calgary, explains: “Equity sharing transforms a distressed asset into a collaborative investment. It provides immediate liquidity to cure defaults without displacing the homeowner, creating a symbiotic relationship between private capital and housing preservation.”

How Co-Ownership Halts Foreclosure Proceedings

The primary mechanism by which equity sharing stops foreclosure is the immediate injection of capital to cure the default. In Alberta, lenders are legally obligated to halt foreclosure actions if the borrower pays the outstanding arrears, accumulated interest, and associated legal costs before the redemption period expires. By partnering with an equity investor, the homeowner secures the exact funds required to reinstate the mortgage in good standing.

Once the arrears are cleared, the lender’s legal standing to pursue the property dissolves. The final order of foreclosure timeline is permanently interrupted. Furthermore, the addition of a financially stable co-borrower to the property title often satisfies the lender’s risk management criteria. Because the investor typically possesses a strong credit profile (usually a minimum credit score of 680) and verifiable income, the overall risk profile of the mortgage improves, making lenders more amenable to restructuring the ongoing payment terms.

Core Components of a Shared Equity Contract

A successful collaborative ownership model relies on meticulous legal documentation. Because multiple parties hold a vested interest in a single asset, the contract must anticipate various future scenarios, from market downturns to unexpected maintenance costs. According to Alberta Courts guidelines regarding joint property disputes, poorly drafted co-ownership agreements frequently lead to costly litigation. Therefore, a robust contract must include several non-negotiable elements.

First, the agreement must clearly define the ownership percentages and how monthly obligations (principal, interest, property taxes, and insurance) are divided. Second, it must establish a profit distribution formula. If the property is sold in the future, how is the initial investment returned, and how is the subsequent profit split? Finally, the contract must detail maintenance responsibilities. Typically, the occupying homeowner handles day-to-day upkeep, while major capital expenditures (like a new roof) are split according to ownership shares.

Comparison: Equity Sharing vs. Traditional Refinancing

| Feature | Equity Sharing Agreement | Traditional Refinancing |

|---|---|---|

| Credit Requirements | Flexible; relies heavily on partner’s credit | Strict; requires high personal credit score |

| Monthly Payments | Reduced (shared with investor) | Often increased due to higher 2026 rates |

| Debt-to-Income Impact | Lowers DTI ratio | Increases overall debt load |

| Future Appreciation | Shared proportionally with investor | 100% retained by homeowner |

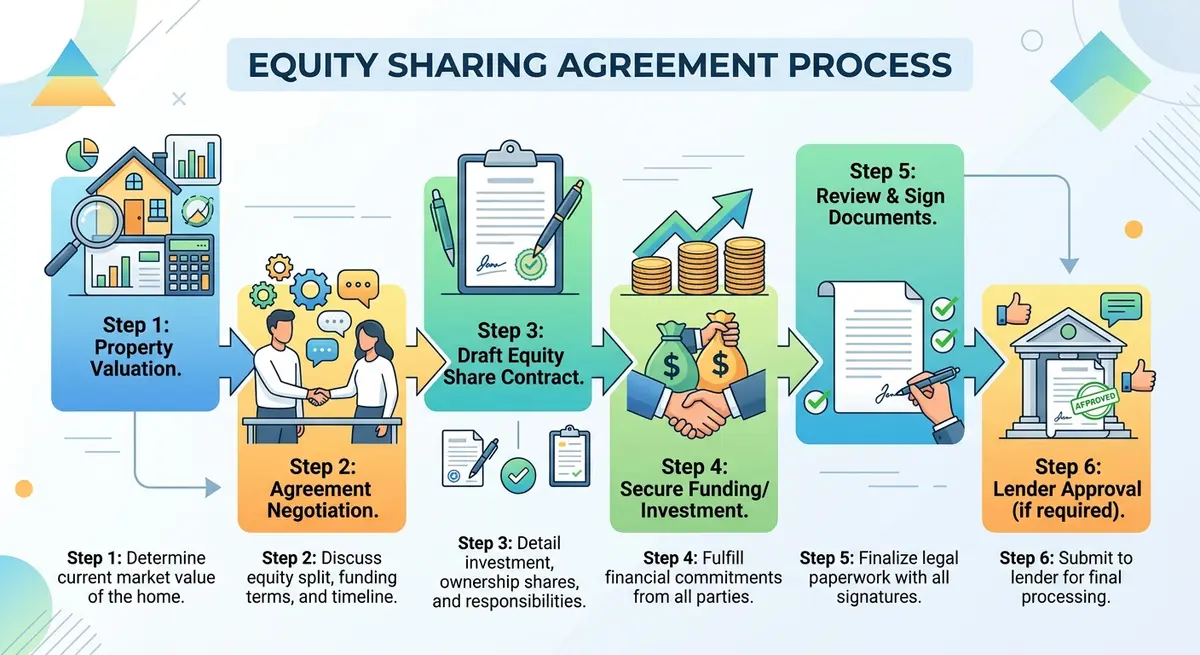

Step-by-Step: Structuring a Shared Equity Deal in Alberta

Transitioning from a distressed mortgage to a stable co-ownership arrangement requires a methodical approach. Rushing the process can lead to unfavorable terms or regulatory violations. Here is the standard procedure for executing these agreements in the Calgary market:

- Assess Property Equity: Order an independent appraisal to determine the current fair market value. You must have sufficient equity (typically at least 25%) to make the deal attractive to an investor.

- Vetting Potential Partners: Whether partnering with a family member, a private investor, or an institutional fund, verify their financial capacity. They should possess a debt-to-income ratio below 42% and liquid capital ready for deployment.

- Drafting the Legal Framework: Retain a real estate attorney to draft the tenancy in common agreement. This document must include a “right of first refusal,” ensuring you have the first opportunity to buy back the investor’s share before they can sell it to a third party.

- Navigating Spousal Rights: Ensure compliance with provincial family law. Understanding Dower Act requirements is essential, as a non-titled spouse must consent to any disposition of the homestead, including selling a partial equity stake.

- Lender Notification and Approval: Present the restructured ownership and cured arrears to your existing mortgage lender. Most institutions require an updated application when adding a party to the title.

Mitigating Legal and Financial Risks

While collaborative ownership offers a lifeline, it is not without inherent risks. The most significant vulnerability is joint and several liability. In the eyes of the mortgage lender, all parties on the title are 100% responsible for the debt. If your investor partner suddenly stops contributing their share of the monthly payment, the lender will look to you to cover the shortfall. If the payment is missed, both of your credit scores will suffer equally.

According to Marcus Thorne, Lead Real Estate Attorney at Alberta Legal Advocates: “The judicial nature of Alberta foreclosures gives homeowners a critical 6-to-12-month window to execute co-ownership agreements before the Court of King’s Bench issues a final order. However, borrowers must ensure their exit strategies are airtight. A poorly defined buyout clause can trap a homeowner in a perpetual partnership.”

To protect yourself, establish a joint escrow account funded with a three-month reserve to cover unexpected shortfalls. Additionally, outline a clear path for buying out a co-owner. Most agreements span 3 to 5 years, after which the original homeowner refinances the property under their own name to purchase the investor’s shares at the current market value.

Market Trends: Why Calgary Homeowners Choose Collaborative Ownership

The macroeconomic landscape of 2026 has made traditional debt consolidation exceedingly difficult. Data from Statistics Canada indicates that wage growth has not kept pace with the rising cost of living, leaving many Albertans with maxed-out credit facilities. Concurrently, the Calgary real estate market remains robust. In Q1 2026, Calgary property values increased by 6.4% year-over-year, driven by interprovincial migration and a tight housing inventory with vacancy rates hovering at just 1.8%.

This dynamic—high property values coupled with tight cash flow—creates the perfect environment for equity sharing. Homeowners are sitting on significant wealth trapped in their walls, but lack the monthly income to qualify for traditional refinancing under the stringent federal stress tests.

As Sarah Jenkins, Director of Mortgage Risk at the Canadian Financial Institute, notes: “By distributing the debt burden across multiple parties, equity sharing effectively lowers the primary occupant’s debt service ratios, satisfying stringent 2026 federal stress test requirements while providing investors access to a high-yield, tangible asset.”

Alternative Foreclosure Prevention Strategies

While equity sharing is highly effective, it requires relinquishing a portion of your property’s future wealth. Before committing to a co-ownership model, it is prudent to evaluate all available alternatives for halting foreclosure. For homeowners with substantial equity but temporary cash flow issues, securing a secondary loan might be preferable to giving up ownership shares.

Exploring cash-out refinancing options is the traditional route, though it requires strong credit. If your credit has already been damaged by missed payments, leveraging home equity through a private second mortgage can provide the necessary funds to cure arrears. Private lenders focus primarily on the property’s loan-to-value (LTV) ratio rather than the borrower’s credit score. While these loans carry higher interest rates, they allow you to retain 100% ownership of your home and capture all future market appreciation. Additionally, understanding Alberta’s redemption periods can help you accurately time the deployment of these alternative financing methods before legal costs escalate (which currently average $15,000 in contested foreclosure cases).

Conclusion

Facing foreclosure is a deeply stressful experience, but the judicial process in Alberta provides homeowners with the time needed to implement strategic solutions. Equity sharing agreements represent a powerful, innovative tool for Calgary residents in 2026. By converting trapped home equity into immediate capital and sharing the ongoing financial burden with an investor, you can halt legal proceedings, protect your credit, and most importantly, stay in your home. Success relies on transparent communication, rigorous legal documentation, and a clear exit strategy. If you are struggling with mortgage arrears and want to explore how collaborative ownership or alternative financing can save your property, contact our team today for a confidential consultation.

Frequently Asked Questions (FAQ)

How exactly does equity sharing stop a foreclosure in Alberta?

Equity sharing stops foreclosure by providing the homeowner with an immediate lump sum of cash from an investor. These funds are used to pay off the accumulated mortgage arrears, legal fees, and penalties. Once the default is cured, the lender is legally required to halt the foreclosure process.

Do I have to move out if I sign an equity sharing agreement?

No, you do not have to move out. The primary advantage of this model is that you retain the right to occupy the property as your primary residence. You simply share the ownership title and the monthly financial obligations with your investor partner.

What happens if the Calgary housing market crashes and property values drop?

In an equity sharing agreement, both parties share the financial risk proportionally. If the property value decreases, the investor’s equity stake loses value alongside yours. The specific legal contract will outline how depreciation is handled during a buyout or sale scenario.

Can the investor force me to sell my home?

A properly drafted agreement will include protective clauses, such as a defined term limit (e.g., 5 years) and a right of first refusal. The investor cannot unilaterally force a sale before the term expires, and you will always have the first option to buy out their share at fair market value.

Will my mortgage lender allow me to add an investor to the title?

Most lenders will allow title modifications, but they require the new co-owner to pass a credit and income assessment. Because investors typically have strong financial profiles, lenders often view the addition favorably as it reduces the overall risk of future defaults.

How much does it cost to set up a shared equity contract?

Setting up the agreement involves property appraisal fees, legal drafting costs, and potential lender administration fees. In Calgary, homeowners should budget between $2,500 and $4,000 for the legal and administrative setup, which is often deducted directly from the investor’s initial capital injection.