If you’re facing mortgage difficulties with Bridgehouse in Alberta, you have legal options to prevent foreclosure and keep your home. Alberta’s civil justice system provides homeowners with multiple avenues to delay, negotiate, or halt foreclosure proceedings entirely—but you must act quickly and understand the deadlines involved. This guide covers everything Alberta homeowners need to know about responding to foreclosure when Bridgehouse is your lender.

- Alberta homeowners have legal rights that require lenders to negotiate in good faith before proceeding to court

- The Statement of Claim initiates formal foreclosure proceedings—timing is critical once you receive this document

- Second mortgages can provide rescue financing to pay arrears and reinstate your primary mortgage

- Consumer proposals and bankruptcy offer formal debt relief as alternatives to losing your property

- Early intervention dramatically improves outcomes—delays significantly reduce your options

- Bridgehouse, like all federally regulated lenders, must comply with Alberta’s civil procedures and FCAC guidelines

- Independent legal advice is strongly recommended before signing any agreement with your lender

Understanding How Foreclosure Works in Alberta

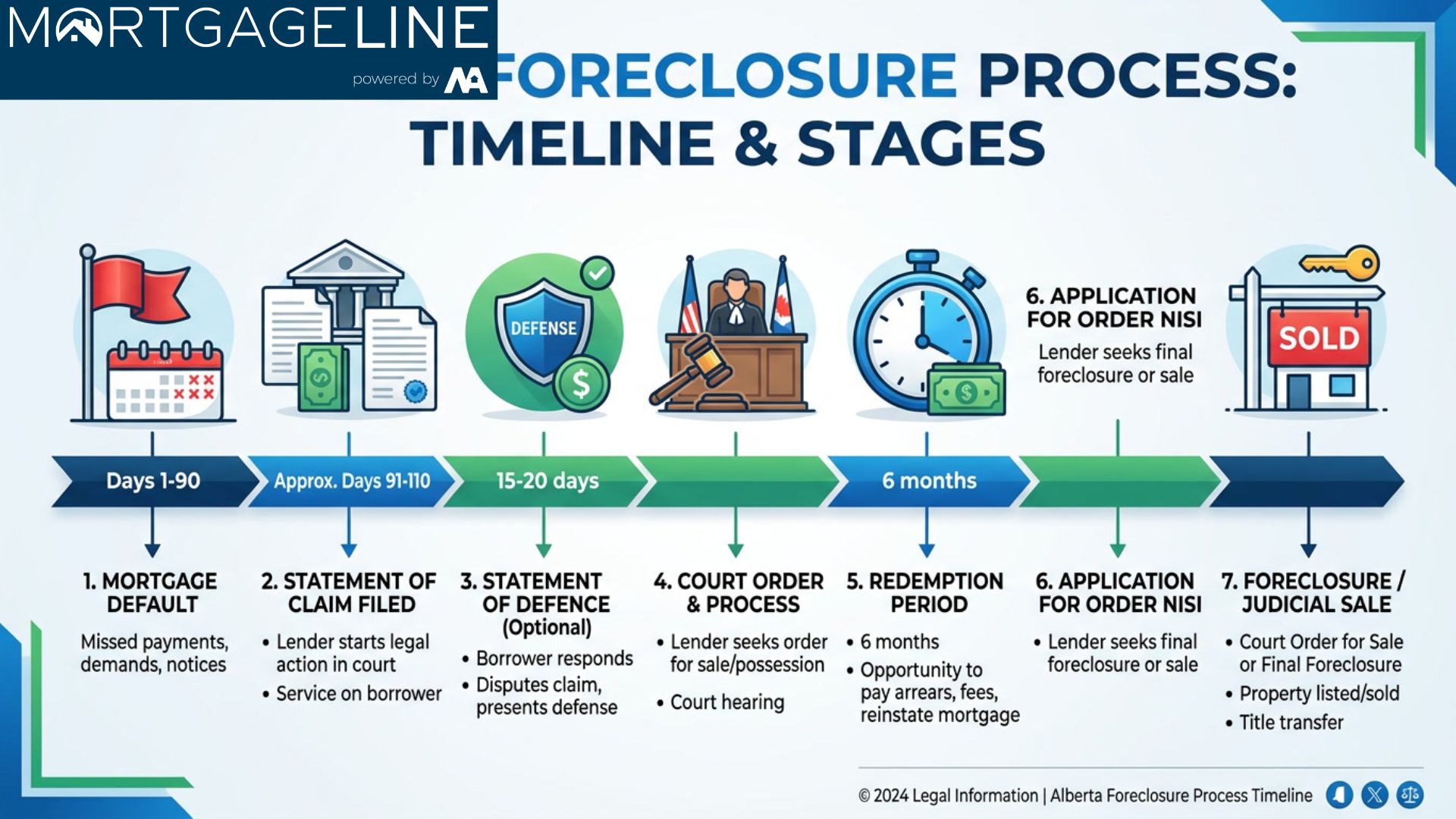

Foreclosure is a legal process that allows a lender to sell a property when the borrower defaults on mortgage payments. Unlike some provinces that use power of sale or strict foreclosure, Alberta follows a court-based redemption period model. According to the Alberta Department of Justice, the process involves multiple stages where homeowners retain the right to catch up on missed payments until the property is sold at auction.

The process typically begins when a homeowner misses several mortgage payments. The lender sends default notices, and if payments remain outstanding, they file a Statement of Claim for foreclosure with the Alberta Court of King’s Bench. This legal document officially starts the foreclosure timeline. From this point, homeowners have a defined redemption period—typically six months to one year—to either catch up on arrears, negotiate a new payment arrangement, or find alternative financing.

Research from the Financial Consumer Agency of Canada indicates that approximately 12% of Canadian homeowners experienced significant mortgage stress in 2025, with Alberta’s energy sector fluctuations contributing to elevated delinquency rates in Calgary and surrounding communities. Understanding this process before you receive legal documents gives you a significant advantage.

Who Is Bridgehouse and What Are Your Options

Bridgehouse is a Canadian mortgage lender specializing in residential lending across multiple provinces, including Alberta. As a federally regulated financial institution, Bridgehouse operates under the Bank Act and must adhere to guidelines established by the Office of the Superintendent of Financial Institutions (OSFI). This regulatory framework means they must follow specific procedures before and during foreclosure proceedings.

When you work with Bridgehouse, your mortgage agreement outlines specific default provisions. Typically, these include failure to make regular payments, breach of insurance requirements, or failure to maintain property taxes. Understanding which provision triggered your default is essential because it determines what you must cure to reinstate your loan.

As experts at the Final Order of Foreclosure Timeline for Calgary Homeowners explain, lenders like Bridgehouse prefer to avoid the costly foreclosure process whenever possible. Legal proceedings are expensive, time-consuming, and often result in below-market sales. This gives homeowners leverage—Bridgehouse has financial incentive to negotiate alternatives that allow them to recover their investment while keeping you in your home.

Your Right to Request a Workout Arrangement

Under federal guidelines, federally regulated lenders must make reasonable attempts to contact borrowers and offer workout options before initiating foreclosure. According to the Government of Canada, these options may include payment deferrals, loan modifications, partial payments, or refinancing arrangements. Request these options in writing and document all communications with Bridgehouse.

The Critical Timeline: Responding to a Statement of Claim

Receiving a Statement of Claim for foreclosure is a serious matter that requires immediate action. This legal document means Bridgehouse has filed suit in Alberta court, and you have a limited time to respond. The Complete 2026 Guide to Responding to a Foreclosure Statement of Claim in Calgary emphasizes that missing your response deadline results in a default judgment, allowing Bridgehouse to proceed directly to obtaining a foreclosure order without further input from you.

You typically have 15 days to file a Statement of Defence if you’re served in Alberta. This deadline is firm—courts rarely grant extensions. Your defence can include various arguments: the amount claimed is incorrect, you’ve already cured the default, the lender failed to follow required procedures, or you have a counterclaim. Even if you believe you cannot win, filing a defence triggers settlement conferences where most cases resolve.

As Sarah Mitchell, a Calgary real estate lawyer with over 15 years of foreclosure experience, explains: “The moment you receive legal papers, your negotiating position changes dramatically. Lenders know that a defended file costs them thousands in legal fees and months of delays. This is when they become genuinely willing to negotiate terms they would never offer before litigation.”

Prevention Strategies: How to Stop Bridgehouse Foreclosure

Successfully preventing foreclosure requires understanding your options and acting on multiple fronts simultaneously. Here are the primary strategies Alberta homeowners use to stop Bridgehouse foreclosure proceedings:

1. Reinstatement: Catching Up on Missed Payments

The simplest solution is paying everything you owe—principal, interest, late fees, and legal costs. If you have access to funds through savings, family loans, or emergency credit, reinstatement immediately ends the foreclosure. Calculate your total arrears by contacting Bridgehouse directly and requesting a reinstatement quote in writing.

2. Refinancing with Your Current Lender

Bridgehouse may agree to refinance your loan, extending the amortization, adjusting the interest rate, or capitalizing arrears into a new mortgage. This requires demonstrating you can afford the modified payments going forward. Provide updated income documentation, employment verification, and a letter explaining the circumstances that caused your default.

3. Second Mortgage Rescue Financing

If your home has sufficient equity, a second mortgage can provide the funds needed to pay off Bridgehouse and reinstate your primary loan. According to industry data, approximately 67% of Alberta homeowners with mortgages have at least 20% equity in their properties, making them candidates for secondary financing. The Pros and Cons of Second Mortgages in Calgary provides detailed analysis of when this strategy makes sense.

Second mortgages for foreclosure prevention typically come from private lenders who can close quickly—often within 5-10 business days. While interest rates are higher than primary mortgages, the alternative is losing your home entirely. A $300,000 home with a $200,000 first mortgage could support a $50,000-$75,000 second mortgage to clear arrears and stop proceedings.

4. Consumer Proposal: A Formal Debt Alternative

A consumer proposal under the Bankruptcy and Insolvency Act allows you to negotiate with Bridgehouse and other creditors to pay a portion of what you owe over time. This legally binding arrangement stops all collection proceedings, including foreclosure. The Early Consumer Proposal Discharge and Home Equity in Calgary guide explains how homeowners can use this option while preserving their property.

5. Selling Your Property

If other options aren’t viable, selling before the foreclosure completes gives you control over the process and potentially preserves equity. Even in a market downturn, most Alberta properties have sufficient equity to allow sales that satisfy the first mortgage. The Second Mortgage Bridge Financing for Calgary House Flips demonstrates how strategic financing can facilitate timely sales.

Comparing Your Foreclosure Prevention Options

| Option | Speed | Cost | Impact on Credit | Best For |

|---|---|---|---|---|

| Reinstatement | Immediate | Arrears + fees | Minimal additional | Short-term cash flow issues |

| Lender Refinance | 30-60 days | Standard closing costs | Minimal | Stable income, equity available |

| Second Mortgage | 5-14 days | Higher interest rates | Moderate | Quick action needed, good equity |

| Consumer Proposal | 30-90 days | Administration fees | Significant | Overwhelmed by total debt |

| Property Sale | 60-120 days | Real estate commissions | Moderate | Unaffordable mortgage, equity exists |

| Bankruptcy | Immediate stay | Court fees, trustee costs | Severe | No equity, no income |

Common Mistakes to Avoid During Foreclosure

Alberta homeowners facing foreclosure frequently make errors that cost them their homes. Avoiding these pitfalls can mean the difference between keeping your property and losing it:

Ignoring Legal Documents: Many homeowners throw away certified mail or avoid answering the door because they’re embarrassed or overwhelmed. Every document you receive is legally significant. Open and read everything, then contact a lawyer immediately.

Believing the Lender Will Wait: Bridgehouse has a fiduciary duty to their investors to pursue defaulted loans. Waiting for them to “forget about it” or hoping for a callback that never comes wastes your redemption period. As noted in Managing a BMO Foreclosure in Alberta, lenders follow systematic escalation procedures—delay only makes things worse.

Signing Agreements Without Legal Review: Lenders may offer what sounds like a helpful workout agreement that actually accelerates your default or waives important rights. Have any proposed agreement reviewed by an independent lawyer before signing. The Independent Legal Advice for Alberta Second Mortgages guide explains why this review is essential.

Paying Legal Fees Without Negotiating: If Bridgehouse has already incurred legal costs, these are added to your mortgage balance. However, these fees are often negotiable. Lenders frequently reduce or waive legal fees to facilitate a resolution that avoids continued court costs.

Assuming You Have No Options: Even homeowners with poor credit, recent bankruptcies, or self-employed income challenges have options. Private second mortgages, consumer proposals, and creative financing arrangements help people in situations that seem hopeless. The Home Equity Financing for Calgary Energy Workers guide shows how workers in volatile industries have successfully prevented foreclosure.

Getting Professional Help: Who to Contact

Foreclosure prevention requires expertise in real estate law, mortgage financing, and debt management. Building a professional team early gives you the best chance of keeping your home:

Real Estate Lawyer: Essential for reviewing legal documents, filing your defence, and negotiating with Bridgehouse’s legal team. The Law Society of Alberta maintains a referral service to help you find qualified real estate lawyers in your area.

Mortgage Broker: Can access multiple lenders to find refinancing or second mortgage options. Brokers understand which lenders are active in the Alberta market and can match your situation with appropriate products.

Licensed Insolvency Trustee: Required for consumer proposals and bankruptcies. These professionals provide free initial consultations and can advise whether formal insolvency is appropriate for your situation.

Financial Counsellor: Non-profit credit counselling agencies offer free or low-cost advice on budgeting and debt management. The Government of Canada’s Financial Consumer Agency lists approved credit counselling organizations.

Frequently Asked Questions

How long does the Alberta foreclosure process take with Bridgehouse?

The timeline varies based on court schedules and whether you file a defence. An undefended foreclosure can complete in 6-9 months from the initial Statement of Claim. A defended case where negotiations occur may extend to 12-18 months or longer. Each month of delay costs you additional interest and legal fees, so faster action generally results in better financial outcomes.

Can Bridgehouse foreclose while I’m making partial payments?

Yes, if your payments don’t meet the contractual requirements of your mortgage, Bridgehouse can initiate foreclosure even if you’re sending what you can afford. Partial payments don’t cure the default—they simply delay it. You need either a formal payment arrangement with Bridgehouse or a complete cure of arrears to stop foreclosure proceedings.

What happens to my second mortgage if the first mortgage forecloses?

In a foreclosure, the first mortgage lender receives proceeds from the sale up to their outstanding balance. Second mortgage holders receive anything remaining, which is often nothing. If you have a second mortgage, preventing first mortgage foreclosure also protects that position. Second mortgage holders may even assist in preventing foreclosure to protect their own investment.

Will foreclosure ruin my credit forever?

Foreclosure appears on your credit report for 6-7 years from the date of discharge or settlement. During this period, you’ll face higher interest rates and may need to demonstrate responsible credit behavior before qualifying for traditional mortgages. However, many homeowners who’ve experienced foreclosure purchase new homes within 3-4 years by rebuilding their credit and accumulating down payments.

Can I rent out my home during foreclosure to generate income?

Depending on your mortgage terms, renting the property may be permitted or may constitute a breach that accelerates your default. Some Alberta homeowners successfully negotiate with Bridgehouse to allow temporary rental while they work on their financial situation. This requires explicit written approval from your lender—don’t assume renting is allowed without checking your mortgage agreement.

What is the redemption period in Alberta foreclosure?

After a foreclosure order is granted, Alberta courts typically allow a redemption period of 6-12 months during which you can pay the full amount owed (principal, interest, costs) to keep your property. This period runs from the court order date, not from when you received the Statement of Claim. The Final Order of Foreclosure Timeline guide provides detailed information on this phase.

Is bankruptcy ever the better option than foreclosure?

Bankruptcy may make sense if you have no equity in your home (meaning you’d receive nothing after foreclosure anyway), your mortgage debt exceeds your ability to ever repay, or you have other significant debts that bankruptcy would eliminate. However, bankruptcy has severe long-term credit consequences and doesn’t discharge certain debts like recent income taxes or student loans. A consumer proposal often achieves similar debt relief while preserving your credit rating.

How do I negotiate directly with Bridgehouse?

Contact Bridgehouse’s loss mitigation or workout department in writing, requesting a meeting to discuss alternatives to foreclosure. Include your financial statement, proof of income, explanation of circumstances, and proposed solution. Document every conversation with dates, names, and what was discussed. If negotiations stall, escalate to supervisors and consider involving the Financial Consumer Agency of Canada if you believe your lender isn’t following required procedures.

Conclusion

Facing foreclosure from Bridgehouse in Alberta is serious but not hopeless. The legal process takes time, and every week you use that time strategically improves your options. Whether you secure second mortgage financing to catch up on payments, negotiate a modified loan agreement with Bridgehouse, file a consumer proposal, or sell your property on your own terms, you have more control than it might feel.

The most important thing is to stop ignoring the situation and start taking action today. Contact a real estate lawyer, explore your financing options, and communicate with Bridgehouse in writing. The Second Mortgage Store blog provides additional resources on foreclosure prevention, second mortgage strategies, and Alberta real estate financing.

If you’re ready to explore whether a second mortgage can help you prevent foreclosure and keep your Alberta home, contact our team today for a free consultation. We work with homeowners facing urgent situations and can often arrange financing within days when time is critical.