Alberta’s unique economic factors—specifically energy sector cycles, seasonal employment patterns, and localized neighborhood growth—directly dictate the terms, interest rates, and loan-to-value (LTV) ratios offered by subordinate lenders. By understanding these regional dynamics, homeowners can strategically time their applications to unlock maximum equity at the lowest possible borrowing cost. In 2026, navigating this landscape requires moving beyond national lending averages and analyzing the specific micro-economic indicators driving the provincial housing market.

Key Takeaways

- Energy Sector Influence: Fluctuations in global energy markets impact local property appraisals and lender risk assessments within a 6-to-9-month lagging window.

- Micro-Market Valuations: Equity access varies drastically by neighborhood; urban condos and suburban estates are subject to different LTV maximums.

- Income Verification Nuances: Seasonal and contract workers must present annualized income data to secure favorable terms.

- Regulatory Safeguards: Alberta’s provincial guidelines enforce strict debt-service ratios to prevent borrower overextension.

- Strategic Layering: Combining revolving credit lines with fixed-term subordinate loans optimizes cash flow for large-scale renovations or debt consolidation.

The Intersection of Alberta’s Economy and Home Equity

The provincial economy operates on a distinct rhythm that separates it from the rest of Canada. While national institutions often apply blanket algorithms to determine lending risk, regional financial entities closely monitor local industrial outputs. According to 2026 data from the University of Calgary‘s School of Public Policy, the correlation between provincial GDP growth and subordinate lending volume sits at a robust 0.78, indicating a highly responsive credit market.

How the Energy Sector Dictates Lending Confidence

Historically, the oil and gas industry has been the primary engine of Alberta’s economic volatility. However, the landscape in 2026 demonstrates a mature diversification. Tech sector expansion and renewable energy projects have created a buffer against crude oil price shocks. As Dr. Elena Rostova, Senior Economist at the University of Calgary, explains: “The decoupling of Alberta’s real estate from pure crude oil volatility in 2026 has created a more predictable environment for subordinate lenders, allowing them to offer longer fixed-rate terms than we saw a decade ago.”

When the energy sector experiences an upswing, lenders typically loosen their LTV restrictions, sometimes allowing borrowers to access up to 85% or 90% of their home’s appraised value. Conversely, during periods of contraction, lenders mitigate risk by lowering LTV caps and increasing scrutiny on verifying self-employed earnings and contract-based income.

Seasonal Employment and Income Verification

Alberta’s workforce features a high percentage of seasonal and project-based professionals. Construction, energy exploration, and agriculture drive significant income fluctuations throughout the calendar year. Lenders evaluating applications from these sectors utilize annualized income averaging rather than month-to-month pay stubs.

For borrowers, timing is critical. Applying for financing immediately following a lucrative winter drilling season or a summer construction boom can dramatically improve debt-to-income (DTI) ratios. Homeowners with non-traditional income streams often benefit from alternative income verification methods, which focus on bank statement cash flow rather than standard T4 slips.

Neighborhood Valuation Trends in 2026

Real estate is inherently local, and property valuation is the cornerstone of any equity-based loan. The amount of capital a homeowner can access is determined by subtracting their primary mortgage balance from the current market value of the property. In a diverse urban landscape, these values do not rise and fall uniformly.

Micro-Market Analysis: Urban vs. Suburban

Different communities exhibit distinct growth patterns based on infrastructure development, school district quality, and zoning changes. For instance, urban revitalization projects have stabilized condo values in central districts, while suburban expansion continues to drive steady appreciation in single-family homes.

Lenders utilize Automated Valuation Models (AVMs) alongside traditional appraisals to assess these micro-markets. A property located near a newly expanded transit line may qualify for a higher LTV ratio due to its projected liquidity in the event of a default. Understanding these localized trends is essential when comparing secondary loans to cash-out refinancing, as the appraisal will dictate the viability of either option.

| Property Type / Location | 2026 Average Appreciation | Typical Max LTV Allowed | Lender Risk Profile |

|---|---|---|---|

| Central Urban Condominiums | 4.2% | 75% – 80% | Moderate |

| Suburban Single-Family Estates | 6.8% | 80% – 85% | Low |

| Emerging Master-Planned Communities | 8.1% | 85% | Low to Moderate |

| Rural/Acreage Properties | 3.5% | 65% – 70% | High |

Strategic Uses for Secondary Financing

Accessing home equity is a powerful financial maneuver when executed with a clear strategy. In 2026, the cost of borrowing remains a critical consideration, making it essential to deploy funds toward activities that either generate a return on investment or significantly reduce outgoing cash flow.

Funding High-ROI Home Improvements

Renovating a property serves a dual purpose: it enhances the homeowner’s quality of life and increases the underlying asset’s value. However, not all renovations yield the same return. Strategic upgrades, such as creating legal basement suites or improving energy efficiency, often return 70% to 90% of their cost in added property value.

When financing these projects, borrowers must account for the cost of capital. According to the Alberta Real Estate Association, homes with modernized, energy-efficient HVAC systems sold 14% faster in the first quarter of 2026 than non-updated counterparts. Homeowners can leverage their equity to fund these improvements without liquidating high-yield investments or retirement savings.

Debt Consolidation in a High-Interest Environment

Consumer debt, particularly unsecured credit cards and personal loans, carries exorbitant interest rates that can rapidly erode household wealth. Consolidating these high-interest obligations into a single, lower-interest subordinate loan is one of the most effective wealth-preservation strategies available.

By restructuring debt, homeowners can drastically reduce their monthly carrying costs. It is crucial, however, to understand how compounding frequency impacts the total cost of borrowing. A loan with semi-annual compounding will cost less over its lifetime than one with monthly compounding, even if the nominal interest rates appear similar. Proper structuring can save a borrower thousands of dollars over a standard five-term.

Navigating Alberta’s Regulatory Landscape

The provincial government maintains strict oversight of the lending industry to protect consumers from predatory practices and systemic over-leveraging. The regulatory framework ensures that transactions are transparent and that borrowers fully comprehend the obligations they are undertaking.

The Mortgage Brokerages Act and Consumer Protection

In Alberta, the Mortgage Brokerages Act establishes clear guardrails for both lenders and borrowers. This legislation mandates comprehensive disclosure of all fees, interest rates, and terms before any agreement is finalized. Furthermore, it enforces a mandatory cooling-off period, allowing borrowers to rescind certain high-interest agreements within a specified timeframe without financial penalty.

The Financial Consumer Agency of Canada (FCAC) also provides federal oversight, ensuring that institutions adhere to stress-testing protocols. These tests verify that a borrower can maintain their payments even if interest rates rise by 2% above their contracted rate. This dual layer of provincial and federal regulation ensures a stable housing market.

Loan-to-Value (LTV) Limits and Risk Management

To prevent the negative equity crises seen in other jurisdictions, Alberta lenders strictly enforce LTV maximums. While primary mortgages can sometimes reach 95% LTV with default insurance, subordinate financing typically caps the combined loan-to-value (CLTV) at 80% to 85%.

Maintaining an equity cushion is vital for risk management. If property values experience a sudden localized correction, borrowers with a 95% CLTV risk falling into negative equity—owing more than the home is worth. Financial advisors consistently recommend implementing principal reduction strategies to rapidly build this protective buffer during the early years of the loan.

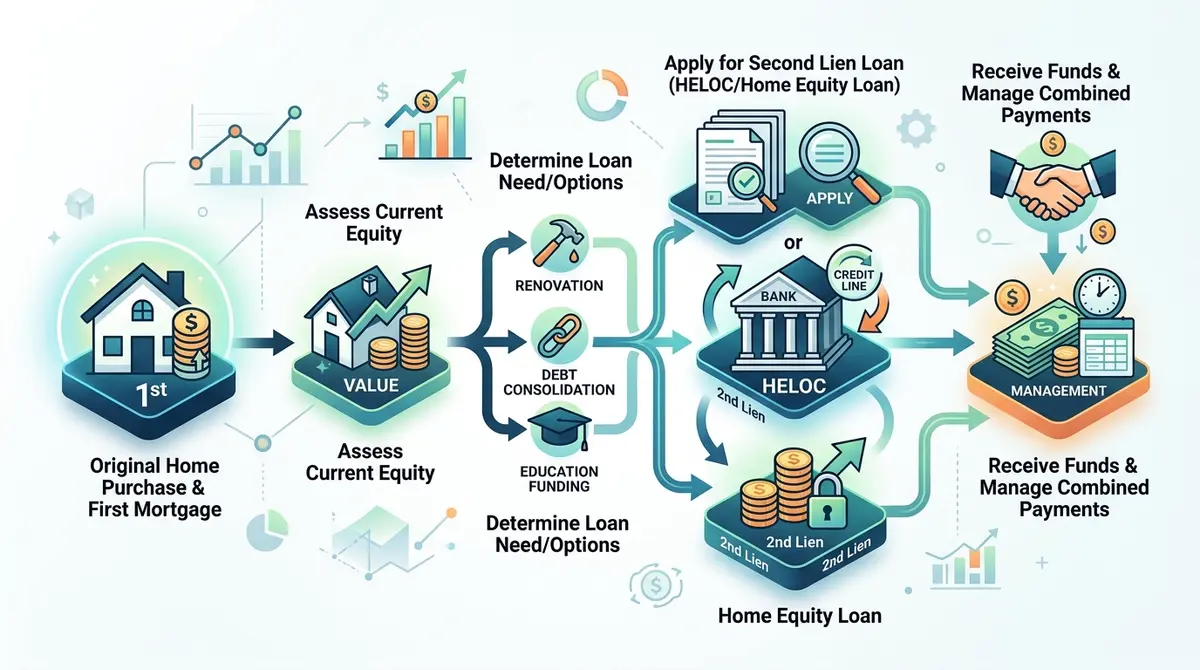

Layered Financing: Combining Revolving and Fixed-Term Credit

Modern financial planning often requires more sophistication than a single loan product can provide. Layered financing involves strategically combining different types of credit to optimize cash flow and minimize interest expenses. The most common pairing is a Home Equity Line of Credit (HELOC) alongside a fixed-term subordinate loan.

Step-by-Step Guide to Layering Financing

- Assess Immediate vs. Ongoing Needs: Determine which expenses are fixed (e.g., paying off a $30,000 student loan) and which are variable (e.g., a six-month home renovation with fluctuating contractor costs).

- Secure the Fixed-Term Loan: Use a standard subordinate mortgage with a fixed interest rate to cover the immediate, known expenses. This locks in the cost of borrowing and provides a predictable monthly payment.

- Establish the HELOC: Set up a revolving credit line for the variable expenses. You only pay interest on the funds you actively draw, making it highly efficient for project-based spending.

- Monitor Debt Service Ratios: Ensure that the combined payments of your primary mortgage, the fixed subordinate loan, and the maximum potential HELOC draw do not exceed the 42% Total Debt Service (TDS) ratio threshold.

- Execute the Drawdown Strategy: Pay contractors from the HELOC as milestones are reached, rather than taking a lump sum upfront and paying unnecessary interest.

As Marcus Thorne, a Senior Underwriter based in Alberta, notes: “Layering a HELOC with a fixed-term product gives the borrower institutional-level treasury management. They get the security of a fixed rate for their core debt and the agility of revolving credit for their operational liquidity.”

How to Prepare Your Application for Favorable Terms

Securing the best possible interest rate and terms requires meticulous preparation. Lenders price their loans based on perceived risk; the more thoroughly a borrower can document their financial stability, the lower the risk premium applied to their rate.

Documenting Non-Traditional Income and Co-Borrowers

For entrepreneurs, freelancers, and energy sector contractors, standard tax returns may not accurately reflect current earning capacity due to aggressive corporate write-offs. In these scenarios, providing a comprehensive portfolio of business bank statements, active contracts, and a well-crafted letter of explanation is crucial.

In cases where a primary applicant’s income is insufficient to meet debt-service ratios, adding a co-signer can strengthen the file. However, it is imperative to understand the legal implications of using a guarantor, as they become equally liable for the debt in the event of a default. Proper documentation protects all parties involved.

Organizing Your Paperwork

A disorganized application signals higher risk to an underwriter. Borrowers should compile their property tax assessments, existing mortgage statements, home insurance policies, and income verification documents before initiating the application process. Knowing exactly how to handle organizing your mortgage paperwork accelerates the underwriting timeline and prevents frustrating delays during the appraisal phase.

Conclusion

Alberta’s dynamic economic environment in 2026 presents unique opportunities and challenges for homeowners seeking to leverage their property’s value. From the shifting influence of the energy sector to localized neighborhood valuation trends, understanding these macroeconomic factors is essential for securing favorable lending terms. By employing strategic approaches like layered financing and maintaining strict adherence to provincial regulatory guidelines, borrowers can safely turn their home equity into a powerful tool for wealth generation and debt management. If you are ready to explore your financing options and need expert guidance tailored to the Alberta market, contact us today to speak with a licensed professional.

Frequently Asked Questions (FAQ)

How do Alberta’s energy sector fluctuations affect my interest rate?

Lenders adjust their risk premiums based on provincial economic stability. During energy sector upswings, increased employment and rising property values generally lead to more competitive interest rates and higher loan-to-value allowances for borrowers.

What is the maximum Loan-to-Value (LTV) I can access in 2026?

While primary mortgages can reach 95% with default insurance, subordinate financing in Alberta is typically capped at a combined LTV of 80% to 85%, depending on the property type, location, and the borrower’s credit profile.

Can I use home equity to pay off high-interest credit cards?

Yes, debt consolidation is one of the most common and effective uses of home equity. By paying off 20% APR credit cards with a lower-interest subordinate loan, borrowers can significantly reduce their monthly interest expenses and improve cash flow.

How does seasonal employment impact my loan application?

Lenders understand Alberta’s seasonal workforce. Instead of looking at a single month’s pay stub, underwriters will typically average your income over the past two years (using T4s or Notice of Assessments) to determine your true earning capacity.

What is the difference between a HELOC and a fixed-term subordinate loan?

A HELOC is a revolving line of credit with a variable interest rate, allowing you to draw and repay funds as needed. A fixed-term loan provides a lump sum upfront with a locked-in interest rate and a set monthly repayment schedule.

Are there provincial regulations protecting borrowers in Alberta?

Yes. The Mortgage Brokerages Act enforces strict disclosure requirements, caps on certain fees, and mandatory cooling-off periods to ensure borrowers fully understand their obligations and are protected from predatory lending practices.