Calgary homeowners can accelerate their equity payoff by utilizing secondary financing to consolidate high-interest unsecured debt, fund value-adding property renovations, or invest in income-producing assets, all while preserving the low fixed interest rate of their primary mortgage. By strategically redirecting the monthly cash flow saved from debt consolidation directly toward principal payments, property owners can shave years off their amortization schedule and build long-term wealth significantly faster than traditional payment methods allow.

Key Takeaways

- Secondary financing allows you to tap into up to 80% of your property’s value without triggering expensive Interest Rate Differential (IRD) penalties on your primary loan.

- Consolidating high-interest credit cards (averaging 18-22%) into a subordinate lien can save thousands annually, which should be redirected into principal reduction.

- Applying lump-sum payments from Alberta energy sector bonuses directly to your principal can reduce your amortization by 3 to 7 years.

- Switching to an accelerated bi-weekly payment schedule results in 13 full annual payments, dramatically reducing lifetime interest costs.

- Strategic renovations in high-demand Calgary neighborhoods like Mount Royal or Bridgeland can yield equity returns exceeding 150% of the project cost.

- Interest paid on funds borrowed for investment purposes may be tax-deductible under Canada Revenue Agency (CRA) guidelines.

Understanding Home Equity and Subordinate Liens in Alberta

In the fast-paced 2026 Alberta real estate market, your property is more than just a residence; it is a highly leveraged financial instrument. Home equity represents the portion of your property that you own outright—calculated by subtracting your outstanding mortgage balance from the current fair market value. For example, if your Aspen Woods home is appraised at $980,000 and your primary mortgage balance is $550,000, you possess $430,000 in raw equity.

Accessing this capital does not require selling the home or breaking your current lending agreement. Subordinate liens, commonly referred to as secondary mortgages, sit behind your primary loan on the property title. This structure is incredibly advantageous in a fluctuating economic climate because it isolates the new borrowing from your original terms. Understanding how compounding frequency impacts your debt is crucial when structuring these secondary loans, as daily or semi-annual compounding can significantly alter your long-term payoff trajectory.

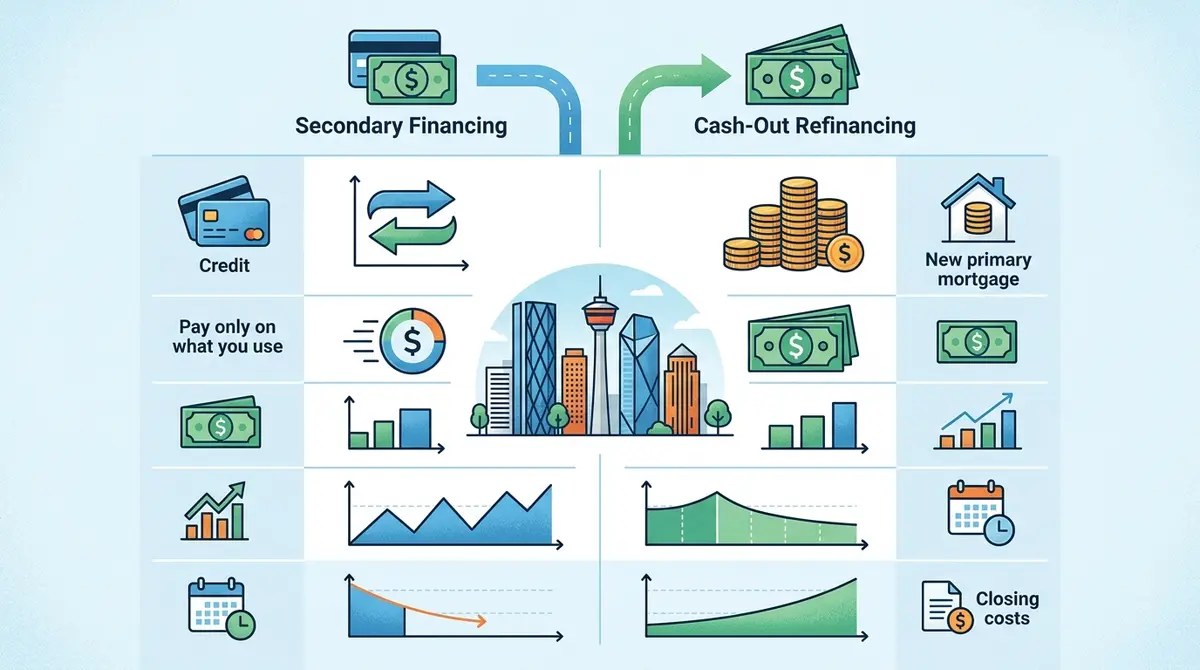

Refinancing vs. Secondary Financing: Which Accelerates Wealth Faster?

A common dilemma for property owners is deciding between breaking their current mortgage to refinance or taking out a subordinate loan. Refinancing replaces your existing mortgage entirely, which resets your amortization clock and often triggers severe prepayment penalties. According to the Bank of Canada, fluctuating overnight rates make holding onto a low-rate primary mortgage a top priority for savvy investors.

As David Chen, a Calgary-based Real Estate Economist, explains: “Breaking a primary mortgage with a 2.5% fixed rate in the 2026 market to access $100,000 in equity is financial self-sabotage. The Interest Rate Differential penalties alone can wipe out any perceived benefits. Subordinate financing preserves that foundational low rate.”

| Feature | Cash-Out Refinance | Secondary Financing |

|---|---|---|

| Primary Mortgage Rate | Lost / Reset to current market rates | Preserved entirely |

| Prepayment Penalties | High (Often 3 months interest or IRD) | None on the primary loan |

| Maximum LTV Limit | Typically 80% | Up to 80-85% depending on the lender |

| Funding Speed | 30 to 45 days | 10 to 14 days |

When comparing secondary loans to cash-out refinancing, the math heavily favors subordinate liens for short-term capital needs or debt consolidation, specifically because the blended interest rate of the two loans remains lower than a completely new, higher-rate primary mortgage.

Strategic Debt Management: The Math Behind Equity Acceleration

The most powerful application of secondary financing is strategic debt consolidation. High-interest revolving credit acts as a parasite on your household cash flow, preventing you from making meaningful principal payments on your property. By converting unsecured debt into secured debt, you drastically lower your carrying costs.

Consider a Calgary household carrying $50,000 in credit card debt at an average interest rate of 19.9%. The annual interest cost is roughly $9,950. By utilizing a subordinate lien at 7.5% to clear this debt, the annual interest drops to $3,750. This creates $6,200 in newly freed cash flow. The secret to accelerating your equity payoff is not to absorb this $6,200 into your lifestyle, but to redirect 100% of it toward principal reduction strategies on your primary or secondary loan. This compounding effect rapidly builds your net worth.

5 Proven Strategies to Pay Off Your Financing Faster

Once you have secured your capital, implementing an aggressive repayment framework is essential. Here are the most effective methods utilized by top-performing Alberta homeowners in 2026:

- Deploy Energy Sector Bonuses: Alberta’s robust energy and tech sectors frequently distribute performance bonuses. According to Statistics Canada, the average corporate bonus in Alberta exceeds $8,500 annually. Applying just 50% of this as a lump-sum payment directly to your principal can shave up to 3.5 years off a standard 25-year amortization.

- Implement Accelerated Bi-Weekly Payments: Instead of making 12 monthly payments, divide your monthly payment in half and pay it every two weeks. This results in 26 half-payments, equating to 13 full monthly payments per year. This single extra payment goes entirely toward the principal.

- Align Payments with Economic Cycles: Calgary’s economy can be cyclical. During peak earning months, voluntarily increase your payment amount by 15-20%. Most lenders allow up to a 20% annual increase in your regular payment amount without penalty.

- Utilize the Smith Maneuver: If you are borrowing against your home to invest in income-producing assets (like dividend stocks or a rental property), the interest on that borrowed capital may be tax-deductible, effectively lowering your borrowing cost and allowing you to reinvest the tax return into your mortgage.

- Round Up Your Payments: If your bi-weekly payment is $842, round it up to $900. This seemingly small $58 increase is applied directly to the principal balance, drastically reducing the lifetime interest paid.

Navigating Calgary Neighborhood Trends for Maximum Valuation

Your property’s location dictates how quickly natural market appreciation builds your equity. In Q1 2026, the Calgary real estate market demonstrated hyper-localized growth. Data from the Canada Mortgage and Housing Corporation (CMHC) indicates that inner-city neighborhoods like Mount Royal and Bridgeland saw property values increase by 8.2%, whereas suburban areas like McKenzie Towne stabilized at a healthy 5.1% growth rate.

Homeowners can artificially accelerate this equity growth through targeted renovations funded by their secondary loan. A $30,000 investment in a legal basement suite in a transit-heavy corridor like Kensington can increase the property’s appraised value by $65,000 to $80,000, yielding an immediate return on investment while generating monthly rental income to service the new debt.

Common Pitfalls: When Accelerated Payments Harm Financial Stability

While aggressive debt reduction is admirable, over-leveraging can jeopardize your household’s financial foundation. A critical mistake Calgary homeowners make is depleting their liquid emergency savings to make lump-sum mortgage payments. If a sudden job loss or medical emergency occurs, having a paid-down mortgage but zero cash in the bank forces individuals to rely on high-interest credit cards, restarting the debt cycle.

Financial advisors recommend maintaining a minimum of three to six months of living expenses in a highly liquid account (like a High-Interest Savings Account or TFSA) before aggressively attacking mortgage principal. Furthermore, it is vital to monitor your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. Households allocating more than 44% of their gross income to debt servicing face a significantly higher risk of default during economic downturns. If you are adding a spouse to your home equity loan to qualify for better rates, ensure both parties understand the joint liability and cash flow commitments.

Tax Implications of Secondary Financing in Alberta

Navigating the tax landscape is a crucial component of wealth acceleration. The Canada Revenue Agency (CRA) has strict guidelines regarding the deductibility of mortgage interest. In Canada, interest paid on a mortgage for your primary residence is generally not tax-deductible. However, the “use of funds” principle applies: if you extract equity via a subordinate lien and use those specific funds to purchase an investment property, invest in a business, or buy dividend-paying stocks, the interest on that specific borrowed amount becomes tax-deductible against the income generated.

As Sarah Jenkins, Senior Underwriter at Alberta Financial Group, notes: “Proper documentation is non-negotiable. You must maintain a clear paper trail showing the borrowed equity moving directly from the lender into the investment vehicle. Commingling these funds with your personal checking account can void the tax deductibility.”

For self-employed individuals, verifying self-employed mortgage income can be complex, but utilizing equity to inject capital into your own business can offer substantial corporate tax advantages. Always consult with a Chartered Professional Accountant (CPA) to structure these transactions legally and efficiently.

The 2026 Underwriting Process: Securing Your Equity Loan

Accessing your property’s value has become highly streamlined. Top-tier lenders in Alberta utilize a precise five-step underwriting process to ensure rapid funding while mitigating risk:

- Needs Assessment & Equity Calculation: Lenders evaluate your current mortgage balance against conservative automated valuation models (AVMs) to determine your maximum borrowing threshold.

- Property Appraisal: A licensed appraiser conducts a full internal and external review of the property to establish the exact fair market value.

- Income Verification: Borrowers submit recent pay stubs, T4s, or Notices of Assessment. For entrepreneurs, securing financing with low taxable income is possible through stated-income programs that analyze bank statements rather than strict tax returns.

- Document Review: Legal and financial disclosures are reviewed. Preparing a comprehensive secondary mortgage document checklist in advance can cut processing times in half.

- Funding and Disbursement: Once approved, funds are typically disbursed through a real estate lawyer or notary within 10 to 14 business days.

Conclusion

Unlocking your property’s value through a subordinate lien is one of the most effective financial maneuvers available to Calgary homeowners in 2026. By bypassing the severe penalties associated with refinancing, you can access the capital needed to consolidate high-interest debt, fund lucrative renovations, or invest in income-producing assets. The key to true wealth building lies in the execution: redirecting your monthly savings into aggressive principal reduction strategies like accelerated bi-weekly schedules and strategic lump-sum payments. When managed with discipline, this approach transforms your home from a static living space into a dynamic wealth-generating asset.

Ready to explore how much capital you can safely access? Get in touch with our team today for a confidential assessment of your property’s valuation and tailored financing options.

Frequently Asked Questions (FAQ)

Can I pay off a secondary loan early without facing penalties?

This depends entirely on the terms of your specific contract. Open loans allow for full repayment at any time without penalty, while closed loans typically feature prepayment privileges (such as paying up to 15% of the original principal annually) but charge penalties for full early discharge. Always review the prepayment clause before signing.

How does a subordinate lien affect my credit score?

Initially, the hard credit inquiry and the addition of new debt may cause a slight, temporary dip in your credit score. However, if you use the funds to consolidate maxed-out revolving credit cards, your credit utilization ratio will plummet, which typically results in a significant boost to your credit score within 30 to 60 days.

What is the maximum Loan-to-Value (LTV) ratio allowed in Alberta?

In 2026, most alternative and private lenders in Alberta will allow you to borrow up to 80% of your home’s appraised value, combining both your primary and secondary mortgages. In rare, highly qualified scenarios involving prime urban real estate, some lenders may extend this to 85% LTV.

Do I need a perfect credit score to qualify?

No. Because the loan is secured against the hard asset of your real estate, lenders are primarily concerned with the amount of equity available rather than just your credit score. Borrowers with bruised credit or non-traditional income sources can frequently secure approvals based on the strength of the property’s equity.

Is the interest rate fixed or variable?

Both options are available in the current market. Fixed rates provide payment stability and protect you against Bank of Canada rate hikes, making them ideal for strict budgeting. Variable rates are often initially lower and offer more flexible penalty structures if you plan to sell the property or pay off the loan quickly.

Can I use the borrowed funds for a down payment on a second property?

Yes. Leveraging the equity in your primary residence to secure a down payment for a rental property or vacation home is a highly common wealth-building strategy. Furthermore, the interest paid on the portion of the loan used for the investment property may be tax-deductible against the rental income generated.