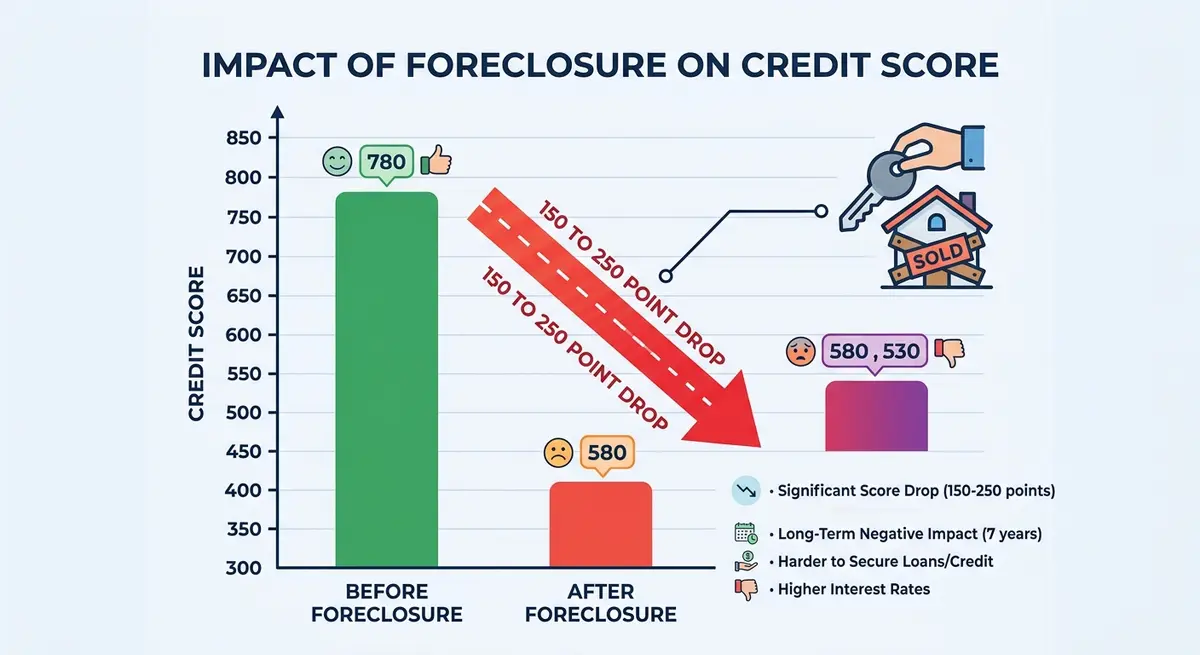

Losing a home to foreclosure in Calgary triggers an immediate 150 to 250-point drop in your credit score, with the derogatory mark remaining on your Equifax and TransUnion reports for six years from the date of default. Furthermore, Alberta’s legal framework allows lenders to pursue deficiency judgments, meaning unpaid mortgage balances can continue to damage your borrowing capacity, inflate future interest rates, and even lead to wage garnishment if left unresolved.

Key Takeaways

- Immediate Score Drop: Expect a severe reduction of 150-250+ points upon the filing of a foreclosure or power of sale.

- Six-Year Penalty: The derogatory R9 rating remains visible to all prospective lenders for six full years.

- Deficiency Judgments: Alberta law permits lenders to sue for the shortfall if the home sells for less than the mortgage balance.

- Dual Reporting Damage: Unpaid deficiency balances report as separate collection accounts, compounding the initial credit damage.

- Rebuilding is Possible: Using secured credit instruments and payment automation can begin restoring lender confidence within 18 to 24 months.

The Immediate Impact of Foreclosure on Your Credit Profile

When a property is repossessed, the financial ripple effects are instantaneous and severe. For Calgary residents navigating the 2026 economic landscape, a foreclosure is not just the loss of an asset; it is a fundamental restructuring of your financial identity. Credit bureaus process these events with strict categorization.

According to Marcus Thorne, Senior Risk Analyst at Equifax Canada, “A foreclosure is categorized as an R9 rating—the most severe derogatory mark possible in the Canadian credit system—which immediately signals high default risk to future creditors.” This R9 rating replaces your previous mortgage payment history.

Borrowers typically witness their scores plummet by 150 to 250 points within seven days of the legal proceedings concluding. If you started with an excellent score of 780, you could easily find yourself in the low 500s. This drop is amplified by the 30, 60, and 90-day late payment markers that inevitably precede the final property seizure.

Understanding Alberta’s Foreclosure Process and Timelines

Navigating property repossession requires a clear understanding of how local systems operate. In Alberta, the timeline from the first missed payment to the final loss of property involves several distinct legal phases. Lenders typically flag accounts after 30 days of delinquency, but formal legal action usually requires three consecutive missed payments.

Once the lender decides to act, they will issue formal legal notices like a statement of claim. This triggers a specific legal window where the homeowner has the opportunity to cure the default. The courts will determine the Alberta foreclosure redemption periods, which typically last six months but can be shortened to as little as one day if the property is abandoned or holds no equity.

During this period, the damage to your credit is ongoing. Every month that the mortgage remains in default, a new negative marker is added to your credit file, dragging your score down further before the actual foreclosure is even finalized.

Power of Sale vs. Judicial Foreclosure: Credit Implications

Property owners facing financial strain in Calgary often encounter different legal pathways for resolving mortgage defaults. Alberta’s system allows lenders to pursue either a power of sale or a judicial foreclosure. While both result in property loss, their timelines and secondary credit impacts vary.

A power of sale allows lenders to sell the property without extensive court orders if the mortgage contract includes this specific clause. This streamlined approach typically completes within 3 to 4 months. Conversely, judicial foreclosures require heavy court supervision and can extend from 8 to 12 months.

| Feature | Power of Sale | Judicial Foreclosure |

|---|---|---|

| Average Timeline | 90 – 120 Days | 240 – 360 Days |

| Court Involvement | Minimal (Bypasses extensive hearings) | Mandatory (Requires multiple appearances) |

| Credit Reporting Duration | 6 Years from default | 6 Years from default |

| Delinquency Accumulation | Shorter period of late payments reported | Extended period of late payments reported |

In complex judicial cases, borrowers may also be subjected to the foreclosure questioning process, a legal proceeding under oath that determines asset distribution and borrower liability. The longer a judicial foreclosure drags on, the more months of “missed payments” accumulate on your credit report prior to the final R9 status.

The Hidden Danger: Deficiency Judgments in Alberta

When a property sells at auction for less than the outstanding mortgage balance, borrowers face a devastating secondary financial hurdle. Unlike some non-recourse jurisdictions, Alberta law permits lenders to pursue borrowers for this shortfall, known as a deficiency judgment.

As Elena Rostova, a Calgary-based real estate attorney, notes: “Alberta’s allowance for deficiency judgments means losing your home is often just the first chapter of financial distress. The lingering unsecured debt can paralyze a borrower’s credit for nearly a decade if not managed proactively.”

If a $500,000 home is repossessed and sold for $420,000, the remaining $80,000 becomes a legally collectible debt. Understanding the nuances of calculating deficiency judgments is critical, as lenders will add legal fees and accrued interest to this total.

This creates a dual-reporting nightmare on your credit file. You will have the original foreclosure mark, plus a massive collection account for the deficiency. If ignored, lenders can escalate this to court-ordered wage garnishment after foreclosure, forcibly taking a percentage of your paycheque and further destroying your financial stability.

Long-Term Financial Repercussions of Property Loss

The aftermath of a foreclosure extends far beyond the immediate loss of property and the initial credit score plunge. The negative entries remain visible to all financial institutions for a minimum of six years, reshaping your borrowing capabilities across every facet of life.

A 2026 report by TransUnion Canada revealed that 68% of borrowers with a recent foreclosure faced outright rejections for standard auto loans within the first two years. Those who were approved faced interest rates 4% to 9% higher than the prime market average.

Furthermore, the rental market in Calgary has become increasingly reliant on credit checks. Landlords routinely screen out applicants with recent R9 ratings, forcing displaced homeowners to rely on private rentals with exorbitant security deposits or co-signers. Even employment opportunities in the financial or government sectors can be jeopardized, as many employers now conduct background credit checks for roles requiring fiduciary responsibility.

Step-by-Step Guide: How to Rebuild Your Credit Post-Foreclosure

Recovering from a foreclosure requires deliberate action, patience, and strict financial discipline. While the six-year reporting period cannot be erased, you can dilute the impact of the foreclosure by layering positive data on top of your credit file.

Follow these proven steps to rehabilitate your credit profile in 2026:

- Audit Your Credit Reports: Obtain free copies of your reports from both Equifax and TransUnion. Ensure the foreclosure date is accurate, as this dictates when the mark will eventually fall off. Dispute any duplicate collection accounts related to the same mortgage.

- Settle Deficiency Balances: If you have a deficiency judgment, negotiate a settlement or payment plan. An “unpaid collection” is vastly more damaging than a “settled collection.”

- Acquire Secured Credit: Apply for a secured credit card. By placing a $500 to $1,000 deposit, you gain a revolving credit line. Use it for small, recurring expenses (like streaming subscriptions) and pay the balance in full every single month.

- Automate All Payments: Your payment history accounts for 35% of your total credit score. Set up automatic withdrawals for utilities, cell phones, and secured cards to ensure you never miss a due date again.

- Keep Utilization Low: The Financial Consumer Agency of Canada (FCAC) recommends keeping your credit utilization below 30%. If your secured card has a $1,000 limit, never let the statement balance exceed $300.

Consistent, on-time payments will slowly rebuild lender confidence. Many borrowers see their scores cross back into the “fair” or “good” categories within 24 to 36 months of dedicated rebuilding.

Proactive Strategies to Prevent Foreclosure and Protect Your Score

The most effective way to handle the credit impact of a foreclosure is to prevent the legal process from finalizing. Early intervention transforms crises into manageable challenges. If you anticipate missing a payment, contact your lender immediately—ideally within 15 days of the due date.

Calgary financial institutions often prioritize negotiated settlements over immediate litigation. Lenders may offer forbearance agreements, temporarily pausing or reducing payments while you recover from a job loss or medical emergency. While a forbearance may still result in a temporary credit dip, it is infinitely less damaging than an R9 foreclosure rating.

For self-employed individuals or those with non-traditional income facing cash flow issues, exploring alternative financing can save the home. Leveraging stated income second mortgages can provide the necessary capital to bring the primary mortgage current, protecting your long-term credit health and keeping you in your property.

Why Professional Financial Guidance Matters in 2026

Navigating the complexities of Alberta real estate law and credit bureau algorithms demands specialized expertise. Attempting to negotiate with massive banking institutions alone often results in unfavorable terms or accelerated legal action.

David Thompson, Lead Strategist at The Second Mortgage Store, emphasizes: “We see clients in 2026 who assume a power of sale wipes their slate clean. In reality, structured credit rehabilitation must begin the day the property is transferred. Understanding the exact foreclosure trustee responsibilities ensures borrowers aren’t taken advantage of during the asset liquidation phase.”

Local experts provide customized debt management strategies, from interpreting complex loan clauses to drafting formal modification requests. By utilizing professional mediation, over 78% of distressed borrowers find viable solutions that preserve both their home equity and their credit scores.

Conclusion

The impact of a foreclosure on your credit in Calgary is undeniably severe, resulting in massive score drops, six years of derogatory reporting, and the looming threat of deficiency judgments. However, a foreclosure is a financial setback, not a life sentence. By understanding Alberta’s specific legal timelines, addressing shortfalls proactively, and implementing strict credit-rebuilding habits, you can restore your fiscal health.

Whether you are currently facing missed payments or are trying to rebuild after a property loss, expert guidance is your most valuable asset. Don’t navigate this complex legal and financial maze alone. Get in touch with our team today to explore personalized strategies that protect your credit and secure your financial future.

Frequently Asked Questions (FAQ)

How long does a foreclosure stay on my credit report in Alberta?

A foreclosure remains on your Equifax and TransUnion credit reports for six years from the date of your first missed payment that led to the default. During this time, it will display as an R9 rating, which is the most severe negative mark.

Can I buy another house after a foreclosure in Calgary?

Yes, but you will typically need to wait at least two to three years and demonstrate completely flawless credit behavior during that time. You will likely need to rely on “B-lenders” or private mortgages initially, which come with higher interest rates and require larger down payments.

What is a deficiency judgment and how does it affect my credit?

A deficiency judgment occurs when your foreclosed home sells for less than what you owe, and the lender sues you for the difference. This appears as a separate, massive collection account on your credit report, compounding the damage of the initial foreclosure.

Will a power of sale hurt my credit less than a judicial foreclosure?

Both processes result in an R9 rating and stay on your report for six years. However, a power of sale is generally faster, meaning fewer months of “late payment” history accumulate on your file compared to a drawn-out judicial foreclosure.

How fast can I improve my credit score after losing my home?

If you immediately settle any deficiency balances and open a secured credit card, you can start seeing measurable score improvements within 12 to 18 months. However, returning to a “prime” score (720+) will usually take the full six years until the foreclosure falls off.

Can a lender garnish my wages for a foreclosure shortfall in Alberta?

Yes. If the lender successfully obtains a deficiency judgment against you in an Alberta court, they can legally apply to garnish your wages or seize funds from your bank accounts to satisfy the remaining debt.