Pre-foreclosure in Calgary is identified by tracking public default notices at the Court of King’s Bench, monitoring sudden MLS status changes, and observing physical property distress or neglected maintenance. It represents the critical legal window after a homeowner misses mortgage payments but before the lender officially seizes and auctions the property. By recognizing these early indicators, buyers can secure undervalued real estate while offering distressed homeowners a viable financial exit strategy.

Key Takeaways

- Early Detection: Pre-foreclosure begins when a lender issues formal notices after 90 days of missed payments.

- Legal Pathways: Alberta primarily utilizes the Judicial Sale process, which includes a standard 6-month redemption period.

- Public Records: Savvy investors track Lis Pendens filings and court documents to find off-market opportunities.

- Risk Mitigation: Thorough title searches are mandatory, as 74% of inexperienced buyers miss hidden liens or tax arrears.

- Homeowner Solutions: Acting within the first 30 days of a default notice increases negotiation success rates by 40%.

- Alternative Financing: Bridge loans and equity financing are essential tools for navigating tight distressed property timelines.

Understanding the 2026 Calgary Real Estate Climate

The economic landscape of 2026 has introduced unique challenges and opportunities within the Alberta housing sector. According to recent data from the Canada Mortgage and Housing Corporation (CMHC), distressed properties in the province have risen by 12% over the past year. This uptick is largely driven by shifting interest rates and evolving employment dynamics in the energy and tech sectors.

Pre-foreclosure is not a finalized legal status; rather, it is a transitional phase. It occurs when a borrower defaults on their loan obligations, prompting the lender to initiate recovery protocols. However, during this period, the homeowner retains full ownership rights and can legally sell the asset to satisfy the debt.

As Marcus Thorne, Senior Real Estate Analyst at the Alberta Property Institute, explains: “Identifying a pre-foreclosure early isn’t just about securing a discount; it’s about providing a viable exit strategy for a homeowner in distress. In 2026, the most successful transactions are those that solve a problem for the seller before the courts take over.”

The Legal Framework: Alberta’s Foreclosure Process

To accurately identify and act on these properties, one must understand the provincial laws governing debt recovery. Alberta’s real estate laws outline two primary paths for distressed properties: Judicial Sales and Power of Sale agreements.

The Judicial Sale is the most common route in Calgary. It requires court oversight, which extends timelines but ensures fairness for the borrower. During this process, the court grants a specific timeframe for the homeowner to repay the arrears, known as calculating the redemption period. Conversely, a Power of Sale allows lenders to act faster without heavy judicial involvement, though it is less common for standard residential mortgages in the province.

Comparing Legal Recovery Methods

| Feature | Judicial Sale | Power of Sale |

|---|---|---|

| Oversight | Court-supervised process | Lender-driven timeline |

| Average Timeline | 60-90 day minimum (often longer) | 30-45 day average |

| Resolution Method | Public auction or court-approved listing | Direct listing permitted |

| Redemption Rights | Typically 6 months granted by judge | Limited, ends upon property sale |

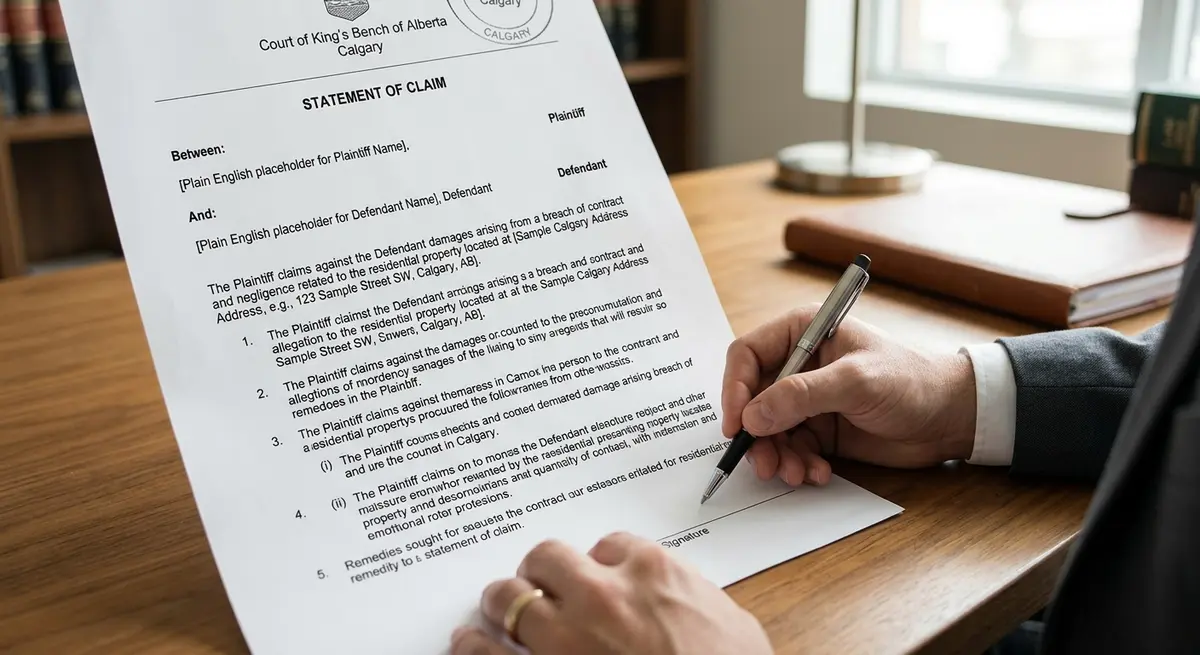

Understanding the difference between a notice of default and a statement of claim is vital. The former is a warning; the latter officially initiates the judicial process.

7 Telltale Signs a Calgary Property is in Pre-Foreclosure

Spotting these opportunities requires a blend of public record research and keen market observation. Here are the most reliable methods to identify homes entering the distress cycle in 2026.

- Court Registry Filings: The most definitive proof is found at the Alberta Court of King’s Bench. When a lender files a Statement of Claim, it becomes public record. Investors routinely monitor these filings to identify motivated sellers before properties hit the open market.

- Lis Pendens on Title: A Certificate of Lis Pendens (pending litigation) is registered against the property title to warn potential buyers of an ongoing legal dispute. Learning the process of discharging a lis pendens is crucial for anyone looking to purchase these assets.

- Unresolved Municipal Tax Liens: Financial distress rarely happens in isolation. Homeowners falling behind on mortgages often miss property tax payments first. Municipal records showing severe tax arrears are strong leading indicators.

- Sudden MLS Status Changes: Properties that frequently bounce between “Active,” “Pending,” and “Relisted” often indicate financing fall-throughs or desperate sellers. Listings with vague descriptions like “As-Is” or “Schedule A Required” are classic red flags.

- Visible Property Neglect: Physical distress mirrors financial distress. Overgrown lawns, uncollected mail, deferred exterior maintenance, and winterized plumbing in occupied homes suggest the owner lacks capital for basic upkeep.

- Aggressive Price Reductions: In a stable 2026 market, a property dropping its asking price by 5-10% every few weeks signals an urgent need to liquidate before a bank-imposed deadline.

- Demand Letters and Door Notices: While harder to spot publicly, official lender notices taped to front doors or frequent visits from property preservation companies are undeniable signs of impending legal action.

Assessing the Risks: What Buyers Need to Know

Acquiring distressed real estate is not without significant peril. Thorough evaluations are required to minimize surprises that could destroy profit margins or saddle a buyer with unmanageable debt. According to Service Alberta’s Land Titles Office guidelines, buyers inherit certain encumbrances if they do not perform adequate due diligence.

David Chen, Director of Risk Assessment at BuildSafe Canada, warns: “Many investors underestimate the structural liabilities of distressed homes. A thorough inspection can save you from a 20% capital drain post-purchase. We consistently see 15-20% repair cost variations between initial estimates and actual requirements.”

Beyond physical inspections, legal scrutiny is paramount. A comprehensive title search reveals hidden expenses, such as secondary financing, mechanic’s liens, or condominium corporation caveats. Research from the Alberta Real Estate Association (AREA) indicates that 74% of inexperienced buyers miss hidden liens when attempting DIY title assessments.

Strategic Solutions for Distressed Homeowners

Addressing these challenges demands a balanced approach. Strategic planning helps buyers identify viable opportunities while supporting homeowners in incredibly difficult circumstances. Early intervention is the most effective way to halt the legal machinery.

Homeowners should contact their lenders immediately after missing a payment. The Financial Consumer Agency of Canada strongly advises against ignoring bank communications. Acting within 30 days of default notices increases negotiation success rates by 40%.

Elena Rostova, a prominent Financial Strategist, notes: “Time is the most critical asset in pre-foreclosure. Engaging the lender within the first 30 days of a missed payment drastically improves the odds of a favorable resolution, whether that’s a loan modification or an approved short sale.”

Viable solutions for homeowners include:

- Payment Deferments: Temporary pauses on obligations to allow the borrower to recover from short-term financial shocks.

- Loan Modifications: Extending the amortization period or lowering the interest rate to reduce monthly carrying costs.

- Refinancing: Leveraging existing equity to consolidate debt. Exploring cash-out refinancing options can provide the liquidity needed to bring the primary mortgage into good standing.

- Strategic Sales: Selling the property on the open market before the court issues a final order, thereby preserving the owner’s credit rating.

Financing a Pre-Foreclosure Purchase in 2026

For buyers, traditional financing is often too slow to meet the accelerated timelines of a distressed sale. Lenders typically send demand letters after 90 days of missed payments, starting a ticking clock that requires rapid capital deployment.

A 2026 study by the Canadian Bankers Association highlights that traditional mortgage approvals can take up to 45 days—time that a distressed seller simply does not have. Consequently, investors must rely on agile financial instruments.

Bridge loans are highly effective for simultaneous property transactions, providing immediate cash to close the deal while long-term financing is secured. Additionally, self-employed investors or those with complex income structures often utilize stated income financing to bypass the lengthy income verification processes of major banks.

When structuring these deals, buyers must also be prepared for the legal hurdles. If the property has already entered the court system, buyers must understand the mechanics of responding to a statement of claim and how to present an offer that satisfies the master in chambers.

Navigating the Final Stages of the Court Process

If a homeowner cannot resolve the debt and a buyer cannot secure the property during the initial pre-foreclosure window, the process moves toward its conclusion. The court will eventually issue a final order, which transfers the title to the lender or approves a judicial sale to a third party.

Understanding the final order of foreclosure timeline is critical for investors who wish to bid on the property at the end of the redemption period. Once this order is granted, the homeowner’s right to redeem the property is extinguished, and the asset is liquidated to recover the lender’s capital.

Sarah Jenkins, a Calgary-based real estate attorney, emphasizes: “The 2026 market dynamics in Calgary require buyers to look beyond the MLS. The real opportunities lie in the Court of King’s Bench filings, but you must have your legal and financial teams aligned before you ever make an offer.”

Conclusion

Navigating distressed property scenarios in Calgary requires sharp awareness, rigorous due diligence, and strategic financial planning. Recognizing early financial strain indicators—from overdue tax payments to public court filings—enables proactive solutions for both buyers and sellers. Thorough evaluations of property value, legal obligations, and repair costs remain essential for risk management in 2026.

Understanding Alberta’s specific legal timelines, including the judicial sale process and redemption periods, helps buyers act decisively. Partnering with specialized professionals streamlines these complex transactions, ensuring compliance with provincial regulations while maximizing investment potential.

If you are navigating a complex real estate transaction or need expert guidance on alternative financing solutions, professional support can transform uncertainty into opportunity. Contact us today to discuss personalized strategies aligned with Calgary’s evolving market dynamics.

Frequently Asked Questions (FAQ)

What defines pre-foreclosure in Calgary’s real estate market?

Pre-foreclosure occurs when a homeowner defaults on mortgage payments, prompting the lender to issue a formal notice of default. In Alberta, this phase initiates a legal process that typically includes a redemption period (often 6 months) where owners can resolve debts or sell the property before losing ownership.

How does pre-foreclosure differ from full foreclosure legally?

Pre-foreclosure is a transitional period where the homeowner still retains title and control of the property. Full foreclosure involves a final court order that legally transfers ownership to the lender or a third-party buyer, permanently eliminating the original owner’s redemption rights.

What indicators suggest a property is entering pre-foreclosure?

Key signs include public legal filings at the Court of King’s Bench, Lis Pendens registrations on the property title, abrupt MLS status changes, unresolved municipal tax liens, and visible neglect like overgrown lawns or deferred maintenance.

Where can buyers find pre-foreclosure listings in Alberta?

Buyers can find these opportunities by searching the Alberta Court of King’s Bench registry for Statements of Claim. Additionally, working with real estate agents who specialize in distressed properties or monitoring specialized investment platforms can yield off-market leads.

What steps can homeowners take to halt the legal process?

Homeowners should contact their lenders immediately to negotiate repayment plans, request loan modifications, or explore refinancing options. Engaging financial specialists early can help restructure debt or secure bridge financing to stabilize the situation before court intervention.

What legal risks come with purchasing distressed properties?

Buyers face significant risks, including inheriting hidden debts, secondary mortgages, or unpaid property taxes. Conducting a comprehensive title search and partnering with a qualified real estate lawyer is mandatory to ensure compliance with Alberta laws and avoid unexpected liabilities.