In Alberta, the foreclosure process typically takes between 6 to 18 months from the first missed payment to the final resolution. However, this timeline heavily depends on the homeowner’s equity position, how quickly they respond to legal notices, and current provincial court backlogs. If a borrower ignores lender communications, property loss can occur in as little as four months. Conversely, actively defending the action and negotiating with lenders can extend the timeline significantly, providing crucial months to secure alternative financing or sell the property on the open market.

Key Takeaways

- Action starts fast: Lenders can initiate legal proceedings after just one missed mortgage payment, typically sending a demand letter within 15 to 30 days.

- The 20-day rule: Once served with a Statement of Claim, Alberta homeowners have exactly 20 days to file a Statement of Defence or Demand for Notice.

- Redemption periods vary: Courts generally grant a 6-month redemption period for homeowners with equity, but this can be reduced to 1 day if the property has negative equity.

- Two distinct outcomes: Proceedings usually end in either a Judicial Sale (where the property is auctioned) or a Foreclosure Order (where title transfers directly to the lender).

- Deficiency risks: If your home sells for less than the mortgage balance, lenders can pursue your other assets unless a specific Foreclosure Order is granted.

- Early intervention works: Over 68% of cases are resolved without property loss when homeowners engage legal and financial advisors before court filings occur.

Understanding the Alberta Foreclosure Timeline in 2026

Navigating mortgage challenges can feel overwhelming, especially when complex legal terminology enters the conversation. In Alberta’s evolving 2026 real estate landscape, the legal mechanism allowing lenders to reclaim property is strictly governed by the Law of Property Act and the Court of King’s Bench. Unlike some jurisdictions where lenders can seize property without court approval, Alberta requires a judicial process. This judicial oversight ensures a balance between lender protections and homeowner rights.

Predicting the exact duration of property recovery proceedings remains challenging due to case-specific variables. While the average duration spans 6 to 18 months, external factors play a massive role. Research from the Canadian Bar Association indicates that court backlogs in major centers like Calgary and Edmonton can delay hearings by 60 to 90 days. Furthermore, the speed of progression is heavily dictated by the borrower’s response. Immediate action pauses filings, while ignoring correspondence accelerates the lender’s legal rights.

As David Chen, Senior Real Estate Analyst at the Alberta Financial Institute, explains: “Homeowners who actively participate in the legal process and file a defense within the initial 20-day window increase their chances of retaining their property by over 40%. Silence is the most expensive mistake a borrower can make.”

What Triggers Legal Action from Lenders?

Understanding the precise triggers of legal action is crucial for any homeowner facing financial strain. While each case differs, financial institutions follow strict protocols when borrowers breach their mortgage terms. Recognizing these red flags early can mean the difference between a negotiated resolution and total property loss.

Missed payments remain the leading cause of mortgage enforcement. Data shows that 62% of cases in Alberta start after just one overdue installment. Lenders typically issue formal warnings within 15 days of a late payment. However, missed payments are not the only trigger. According to the Financial Consumer Agency of Canada, defaults can also include unpaid property taxes exceeding 90 days, lapsed home insurance coverage, or significant structural damage that reduces the property’s value.

When a breach occurs, lenders send a demand letter. These documents specify strict deadlines—usually 10 to 30 days—to settle the arrears. Ignoring these letters allows lenders to advance the process. If you are confused about the paperwork you are receiving, understanding the difference between a notice of default and a statement of claim is your first line of defense.

Step-by-Step: The Legal Process in Alberta

When mortgage payments lapse, lenders follow a structured legal path to recover losses. Homeowners who recognize these steps gain critical time to respond effectively. Here is the standard step-by-step progression in 2026:

- The Demand Letter (Days 15-30): After a missed payment, the lender’s legal counsel sends a formal demand for payment. This outlines the total arrears, legal fees incurred to date, and a deadline for rectification.

- Filing the Statement of Claim (Days 30-60): If the demand expires unmet, the lender files a Statement of Claim with the Alberta Court of King’s Bench. A Lis Pendens (notice of pending litigation) is also registered against your property title, preventing you from selling or refinancing without addressing the debt.

- The Borrower’s Response Window (Days 60-80): Upon being served, you have exactly 20 days to respond. You can file a Statement of Defence if you dispute the claims, or a Demand for Notice if you don’t dispute the debt but want to be kept informed of court dates. Responding to a Statement of Claim correctly is vital to preventing a default judgment.

- The Order Nisi and Redemption Period (Months 3-9): If the lender proves their case, the court issues an Order Nisi. This confirms the debt amount and establishes the redemption period—a specific timeframe granted to the borrower to pay off the arrears or the entire mortgage.

- Final Resolution (Months 9-18): If the redemption period expires without payment, the lender will apply for either a Judicial Sale or a Final Order. Understanding the timeline for a final order of foreclosure helps you know exactly when your legal rights to the property will terminate.

The Critical Role of the Redemption Period

The redemption period is arguably the most important phase for Alberta homeowners. It is a court-ordered window of time designed to give you a final opportunity to save your home. During this period, you remain in the home and retain ownership.

In Alberta, the standard redemption period is six months. However, this is not guaranteed. The length of time granted by the judge depends heavily on the amount of equity in the property. If you have substantial equity (e.g., your home is worth $500,000 and your mortgage is $300,000), the court will almost certainly grant the full six months. This allows ample time to sell the property at fair market value or secure alternative financing.

Conversely, if the property has negative equity (you owe more than the home is worth), the lender’s lawyer will argue that a long redemption period only increases their losses. In these cases, judges frequently reduce the period to one month, or sometimes even one day. Properly calculating your redemption period with a legal professional ensures you know exactly how much time you have to execute a rescue strategy.

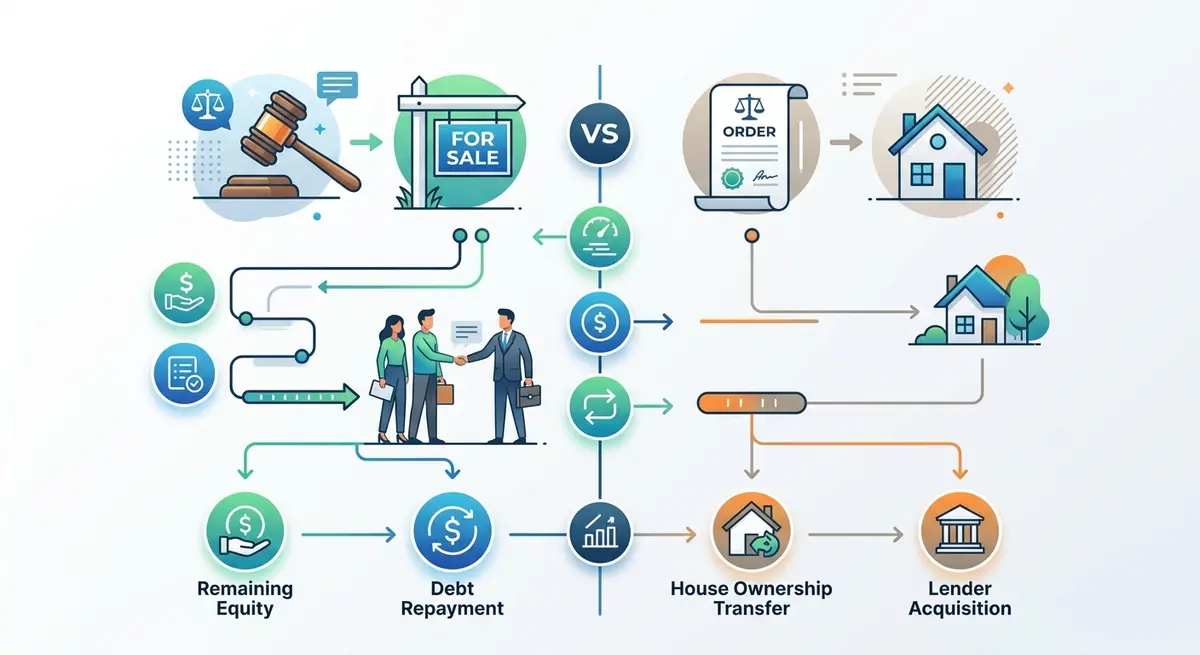

Judicial Sale vs. Foreclosure Order: What is the Difference?

If the redemption period expires and the debt remains unpaid, the court must decide how the lender will recover their funds. In Alberta, this results in one of two distinct legal outcomes: a Judicial Sale or a Foreclosure Order. Understanding the difference is critical because it determines whether you will walk away debt-free or face years of financial hardship.

| Feature | Judicial Sale | Foreclosure Order |

|---|---|---|

| Process | Property is listed and sold under court supervision. | Title is transferred directly to the lender. |

| Equity Return | If sold for more than the debt, surplus goes to the borrower. | Borrower forfeits all equity to the lender. |

| Shortfall Risk | Borrower is liable for any deficiency (shortfall). | Debt is fully discharged; no further liability. |

| Best For… | Properties with high equity. | Properties with negative equity. |

A Judicial Sale is essentially a court-ordered real estate transaction. The property is listed, often with a realtor chosen by the lender, and sold to the highest acceptable bidder. If the sale price covers the mortgage, legal fees, and real estate commissions, any remaining funds are returned to you. However, if the property sells for less than what is owed, you are legally responsible for the difference.

Financial Consequences: Deficiency Judgments and Costs

Losing a home through legal proceedings creates lasting financial ripples. Beyond losing shelter, homeowners risk losing years of equity growth and facing additional debt obligations. Market fluctuations and lender actions can compound these challenges significantly.

When a Judicial Sale results in a shortfall, lenders may pursue a deficiency judgment. This legal tool allows them to recover the remaining money through aggressive collection methods. If you are unaware of how these are calculated, reviewing deficiency judgment calculations is essential. Recent data shows 35% of forced sales in Alberta result in deficiencies averaging $48,000. Once a judgment is granted, borrowers face severe wage garnishment risks, frozen bank accounts, and seized assets.

Furthermore, the legal and administrative costs of this process are staggering, and they are almost entirely passed on to the borrower. A 2026 Alberta legal study revealed that average lender legal costs range from $3,000 to $8,000. These fees, along with property appraisal costs, title search fees, and property management expenses, are added directly to your outstanding mortgage balance. Every ignored letter or missed deadline increases final costs by roughly 15% to 20%.

Proven Strategies to Stop or Delay the Process in 2026

Alberta homeowners facing mortgage challenges have multiple pathways to regain control. Immediate action often determines whether you keep your property or face a forced sale. Consider these proven strategies when navigating complex financial circumstances.

1. File a Statement of Defence: Filing a defense pauses proceedings while challenging lender claims. This legal document requires valid grounds, such as disputing the total arrears amount, proving payments were made on time, or identifying errors in the lender’s legal paperwork. While it requires legal fees, it buys critical time to explore alternatives.

2. Negotiate a Forbearance Agreement: Many lenders prefer negotiated settlements over lengthy court battles. A forbearance agreement temporarily reduces or pauses your monthly payments, giving you time to recover from a short-term financial hardship (like a job loss or medical emergency). The missed payments are typically added to the end of the mortgage term.

3. Refinance Through Alternative Lenders: If traditional banks refuse to help, private lenders often provide solutions based on property equity rather than credit scores. Exploring cash-out refinancing options can allow you to pay off the demanding lender entirely, consolidate other debts, and start fresh with a new mortgage term.

4. Execute a Short Sale: If you have negative equity and cannot afford the home, you can request permission from the lender to sell the property for less than the mortgage balance. While this damages your credit, it is far less severe than a forced judicial sale and often prevents deficiency judgments.

According to the Bank of Canada, fluctuating interest rates in 2026 have made refinancing more complex, but not impossible. One recent Calgary case involved a family facing debt consolidation challenges. By restructuring their home equity through a private lender during their redemption period, they paid out the bank, avoided court filings entirely, and saved over $62,000 in equity that would have been lost at auction.

Frequently Asked Questions (FAQ)

How many missed payments trigger legal action in Alberta?

Technically, a lender can begin legal action after just one missed payment. However, most lenders will send warning letters and attempt to contact you for 30 to 60 days before officially filing a Statement of Claim with the courts.

Can I sell my house before the bank takes it?

Yes. You have the legal right to sell your property at any point before the court issues a Final Order or approves a Judicial Sale. Selling the home yourself during the redemption period is often the best way to preserve your equity and pay off the lender.

What happens if the house sells for less than I owe?

If the court orders a Judicial Sale and the property sells for less than your mortgage balance, you are legally responsible for the shortfall. The lender can obtain a deficiency judgment to garnish your wages or seize other assets to recover the remaining debt.

How long do I have to respond to a Statement of Claim?

In Alberta, you have exactly 20 days from the date you are served with a Statement of Claim to file a Statement of Defence or a Demand for Notice at the courthouse. Failing to respond allows the lender to proceed with a default judgment.

Does losing my home ruin my credit permanently?

While it severely impacts your credit score (often dropping it by 200-300 points) and remains on your credit report for six to seven years, it is not permanent. You can begin rebuilding your credit immediately through secured credit cards and responsible financial habits.

Can I negotiate with my lender after court proceedings start?

Yes, negotiations can happen at any stage. Lenders generally prefer to avoid the costs and delays of court. If you can propose a realistic repayment plan or secure refinancing, lenders will often agree to pause or withdraw the legal action.

Conclusion

Understanding the timeline of property recovery proceedings in Alberta is your strongest defense against losing your home. From the initial demand letter to the expiration of the redemption period, the legal framework provides multiple opportunities for homeowners to intervene. The average 6 to 18-month timeline offers a window to negotiate, refinance, or sell, but only if you act decisively. Ignoring legal notices will only accelerate the process, inflate your debt with legal fees, and expose you to severe financial consequences like deficiency judgments.

If you have received a demand letter or a Statement of Claim, time is of the essence. You do not have to navigate this complex legal system alone. There are proven strategies to protect your equity, stop the legal filings, and regain your financial stability. Contact our team today to explore your options and find a solution tailored to your unique situation.