The foreclosure process in Alberta is a formal legal mechanism initiated by lenders through the Court of King’s Bench to recover outstanding mortgage debt when a borrower defaults. In 2026, this process typically begins with a demand letter after two missed payments, followed by a Statement of Claim, and includes a mandatory redemption period allowing homeowners to settle arrears or sell the property. Understanding these strict judicial timelines is critical for protecting your equity and exploring alternative financing solutions before a final order is granted.

Key Takeaways

- Judicial Oversight: Alberta primarily utilizes a judicial foreclosure system, meaning the courts oversee and approve every major step of the recovery proceedings.

- Early Warning Signs: Legal action typically commences after 30 to 60 days of consecutive missed payments, though unpaid property taxes or lapsed insurance can also trigger defaults.

- The Redemption Window: Courts generally grant a 6-month redemption period, providing a critical timeframe to refinance, sell, or negotiate a forbearance agreement.

- Deficiency Risks: If a property sells for less than the mortgage balance, borrowers may be subject to deficiency judgments, making them personally liable for the shortfall.

- Proactive Defense: Filing a Statement of Defense or Demand for Notice ensures you are kept informed of all court applications and prevents lenders from obtaining default judgments.

Understanding the 2026 Alberta Foreclosure Landscape

When homeowners fall behind on their financial obligations, lenders possess the legal right to reclaim the property to mitigate their losses. However, the legal framework in Alberta is designed to balance the rights of the financial institution with the protections afforded to the borrower. In 2026, shifting economic variables, including fluctuating interest rates and evolving housing inventory, have directly influenced how aggressively lenders pursue recovery.

According to recent data published by the Canada Mortgage and Housing Corporation (CMHC), the mortgage delinquency rate in Alberta hovers around 0.32% as of early 2026. While this represents a relatively small percentage of total mortgages, it translates to thousands of families facing severe financial distress. Most defaults are not born of negligence, but rather unexpected life events such as job loss, medical emergencies, or marital separation.

As Dr. Elena Rostova, Senior Economic Analyst at the Alberta Real Estate Research Institute, explains: “Lenders in 2026 are increasingly utilizing automated risk-assessment tools. The moment an account flags 60 days past due, the file is automatically transferred to their legal department. Homeowners no longer have the luxury of informal, prolonged grace periods.”

Common Triggers for Legal Action

While missed monthly installments are the most recognized catalyst, several other breaches of contract can initiate proceedings:

- Property Tax Arrears: Municipalities can place a lien on a home for unpaid taxes. Because municipal liens take priority over mortgages, lenders will often pay the tax arrears and immediately demand reimbursement from the borrower, initiating legal action if unpaid.

- Lapsed Homeowners Insurance: Mortgage contracts require the property to be continuously insured. If a policy lapses, the lender may force-place expensive insurance and add the premium to the mortgage balance.

- Unauthorized Alterations: Significant structural changes made without municipal permits or lender approval can devalue the asset, triggering a technical default.

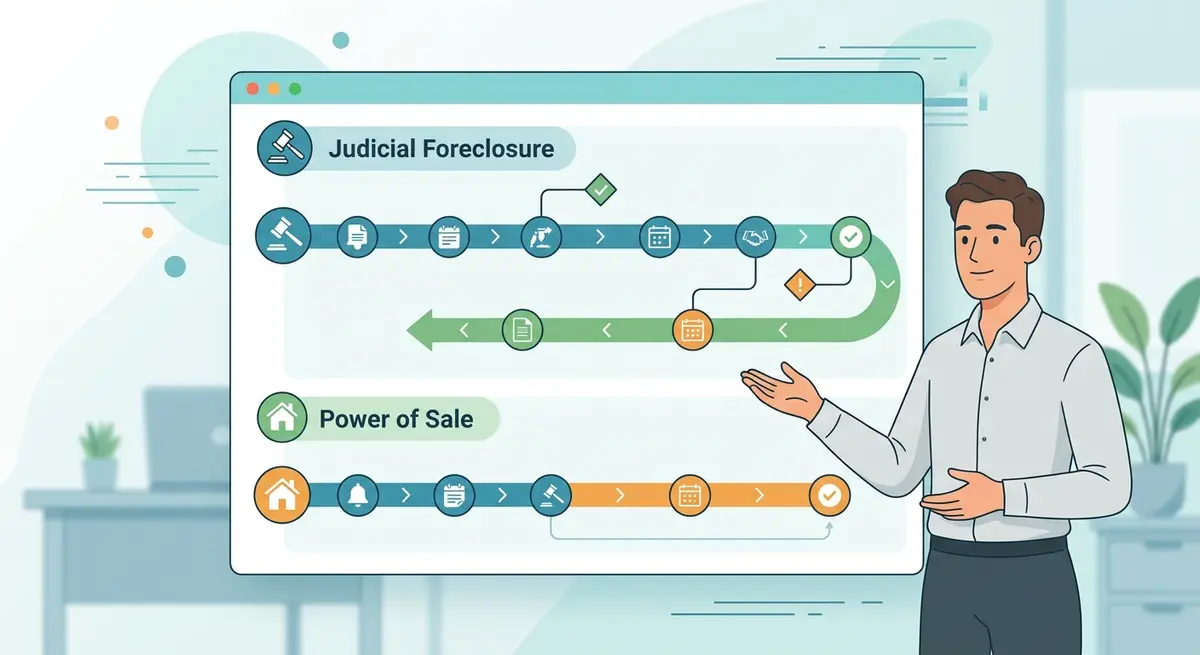

Step-by-Step: How the Foreclosure Process Unfolds in Alberta

Navigating financial difficulties requires a precise understanding of the structured approach lenders take when contractual obligations are breached. The timeline is strictly governed by the Alberta Court of King’s Bench. Here is the chronological progression of a standard judicial foreclosure in 2026.

Step 1: The Demand Letter (15 to 30 Days)

Before any court documents are filed, the lender’s legal counsel will issue a formal Demand Letter. This document outlines the exact amount in arrears, including late fees and initial legal costs, and provides a strict deadline—usually 10 to 15 days—to bring the account into good standing. Responding during this window is the most cost-effective way to halt the escalation.

Step 2: Filing the Statement of Claim

If the Demand Letter expires without resolution, the lender files a Statement of Claim. This is the official commencement of a lawsuit. The document details the total debt owed, the property’s legal description, and the remedies the lender is seeking (such as possession of the property or a judicial sale). It is crucial to understand the distinction between early warnings and formal lawsuits, which is detailed in our guide on the Notice of Default vs. Statement of Claim in Alberta.

Step 3: Filing a Statement of Defense or Demand for Notice

Upon being served the Statement of Claim, the borrower has exactly 20 days (if served in Alberta) to file a response at the courthouse. Failing to respond allows the lender to proceed with a “default judgment,” rapidly accelerating the loss of the property. Filing a Demand for Notice ensures the borrower receives copies of all future court applications, while a Statement of Defense is used to dispute the lender’s calculations or legal standing. For a comprehensive walkthrough, review our resource on responding to a Statement of Claim.

Step 4: The Redemption Period

If the court validates the lender’s claim, a judge will issue a Redemption Order. This order establishes the amount required to pay out the mortgage entirely and sets a specific timeframe for the borrower to do so. In Alberta, the standard redemption period is six months, though courts can shorten this to one day if the property is abandoned or if the mortgage balance far exceeds the property’s value. Understanding how this timeline works is vital; you can learn more about Alberta foreclosure redemption periods here.

Step 5: Final Order or Judicial Sale

If the redemption period expires and the debt remains unpaid, the lender will apply for either a Final Order of Foreclosure (where the lender takes title to the property in full satisfaction of the debt) or an Order for Sale (where the property is listed with a real estate agent). The specific route depends heavily on the property’s appraised equity. Borrowers should familiarize themselves with the Final Order of Foreclosure timeline to anticipate these final stages.

Judicial Foreclosure vs. Power of Sale: Key Distinctions

While Alberta is predominantly a judicial foreclosure jurisdiction, certain corporate mortgages or specific contract clauses may allow for a Power of Sale. Understanding which legal mechanism applies to your situation dictates your timeline and negotiation leverage.

| Feature | Judicial Foreclosure | Power of Sale |

|---|---|---|

| Court Involvement | Extensive. Every step requires a judge’s approval. | Minimal. Lenders can sell without court orders. |

| Average Timeline | 9 to 18 months. | 45 to 90 days. |

| Borrower Equity | Strictly protected. Surplus funds return to the borrower. | Protected, but rapid sales may yield lower market prices. |

| Deficiency Risk | High, depending on the mortgage type (CMHC insured vs. conventional). | Borrower remains liable for any shortfall after the sale. |

Marcus Thorne, a senior litigation partner recognized by the Law Society of Alberta, notes: “In 2026, we are seeing lenders attempt to expedite the process by arguing for shortened redemption periods based on declining neighborhood valuations. Borrowers must present their own independent appraisals to counter these aggressive tactics.”

The True Financial Costs of Property Disputes

Ignoring legal notices does not simply result in the loss of a home; it actively destroys the borrower’s accumulated wealth. The costs associated with legal recovery are added directly to the outstanding mortgage balance, rapidly eroding any existing equity.

Typical expenses incurred during a standard 12-month judicial process include:

- Lender’s Legal Fees: $3,500 to $7,000+ (depending on whether the borrower contests the claim).

- Property Appraisals: $400 to $800 per report (often required multiple times).

- Property Management & Securing: $1,000 to $2,500 (if the property is deemed vacant).

- Court Filing Fees: $250 to $500.

Furthermore, if the property is eventually sold by the court and the proceeds do not cover the total debt (including these accumulated fees), the lender may pursue the borrower for the remaining balance. This is particularly true for insured mortgages. To understand how these shortfalls are computed, read our guide on deficiency judgment calculations in Alberta.

Actionable Strategies to Halt Legal Proceedings

Receiving a Statement of Claim is intimidating, but it is not the end of the road. Alberta law provides multiple avenues for homeowners to cure defaults, provided they act decisively during the redemption period.

1. Negotiating a Forbearance Agreement

If the financial hardship is temporary (e.g., a short-term medical leave or temporary unemployment), lenders may agree to a forbearance plan. This pauses legal action and allows the borrower to add the arrears to the back of the loan or pay them off over an extended period. According to 2026 banking industry reports, approximately 22% of initial defaults are resolved through structured forbearance.

2. Refinancing or Accessing Home Equity

If you have substantial equity in your home but are struggling with cash flow, refinancing the mortgage to a longer amortization period can lower monthly payments. Alternatively, securing secondary financing can provide the lump sum needed to pay off the arrears and legal fees, effectively stopping the lawsuit. Borrowers weighing these options should compare the benefits of secondary financing versus cash-out refinancing.

3. Spousal Buyouts and Separation Mortgages

Relationship breakdowns are a leading cause of mortgage defaults. When two incomes are reduced to one, maintaining the property becomes unfeasible. In these scenarios, one partner can utilize a spousal buyout program to purchase the other’s equity, restructure the debt, and remove the departing spouse from the title and liability. Detailed strategies for this scenario can be found in our guide to spousal buyouts and separation mortgages.

4. Voluntary Sale

If retaining the property is financially impossible, listing the home on the open market during the redemption period is vastly superior to allowing the court to sell it. A traditional real estate sale typically commands a higher purchase price than a judicial sale, preserving more of your equity and protecting your credit rating from the severe impact of a finalized foreclosure.

Why Local Expertise Matters in 2026

The real estate market in Alberta is highly localized. Strategies that work in a booming market may fail in a stagnant one. Lenders assess risk based on neighborhood-specific data, recent comparable sales, and localized economic indicators. Navigating this complex intersection of real estate valuation and judicial procedure requires specialized knowledge.

Working with professionals who understand the nuances of the Court of King’s Bench and maintain relationships with major lenders can dramatically alter the outcome of a dispute. Whether it involves challenging an improperly served notice, securing emergency bridge financing, or negotiating a graceful exit strategy, expert intervention is the most reliable way to protect your financial future.

Frequently Asked Questions (FAQ)

How long do lenders wait before initiating legal action in Alberta?

Lenders typically issue a formal demand notice after 30 to 60 days of missed payments. If the arrears are not resolved within the timeframe specified in the letter (usually 15 days), they will file a Statement of Claim with the court to officially begin proceedings.

Can I stop the process after court documents have been filed?

Yes. Borrowers can halt the proceedings at almost any point prior to the Final Order by paying the arrears and accumulated legal costs. Filing a Statement of Defense also provides an opportunity to dispute the lender’s claims and negotiate terms.

What is a redemption period, and how long does it last?

The redemption period is a court-ordered window allowing the borrower to pay off the mortgage debt or sell the property. In Alberta, the standard duration is six months, though judges can reduce this if the property has negative equity or has been abandoned.

Will I owe money if the bank sells my house for less than the mortgage?

If you have a conventional mortgage (20%+ down payment), Alberta law generally protects you from deficiency judgments. However, if your mortgage is insured by CMHC, Sagen, or Canada Guaranty, you remain personally liable for any shortfall after the property is sold.

How does a foreclosure impact my credit score?

A finalized foreclosure is one of the most damaging events for a credit profile, typically remaining on your credit report for six to seven years. It severely limits your ability to secure future housing, loans, or even certain types of employment.

Can I sell my home privately while under a Statement of Claim?

Yes, you retain the right to sell your property during the redemption period. Selling privately on the open market is highly recommended, as it usually results in a higher sale price compared to a court-ordered judicial sale, helping preserve your remaining equity.

Conclusion

Facing the prospect of losing your home is an overwhelming experience, but understanding the structured legal framework in Alberta provides a roadmap for defense. The 2026 economic landscape requires homeowners to be proactive; ignoring demand letters or court filings only accelerates the loss of equity and limits available solutions. By utilizing the redemption period effectively—whether through refinancing, negotiating forbearance, or executing a strategic sale—you can regain control of your financial trajectory.

Time is the most critical factor when dealing with property disputes. If you have received a demand letter or a Statement of Claim, immediate action is required to preserve your rights and your wealth. Get in touch with our team today to explore personalized, actionable strategies designed to protect your home and secure your financial future.